So as long as we expect the government to try to stimulate the economy by lowering interest rates, there's a killing to be made in the bond market. Theoretically this could go on forever, even in a low-interest environment - the logic holds if rates go from 0.25% to 0.125% - provided the Treasury doesn't simply go straight to zero interest, of course.

Anyhow, his latest essay says that the monetary stimulus will simply be used to settle debts, since debt gets more and more burdensome in a deflationary depression; and settling debt instead of making and buying more stuff, continues to drive deflation. In this enviroment, few businesses will want to take on more debt (certain and fixed) in the hope of increasing their profits (far from certain, and very variable). On a national level, and following the ideas of Melchior Palyi, he now sees every extra dollar of debt as causing GDP to contract.

Therefore, valuations of most assets will continue to decline - except for bonds, which are now the focus for speculators. To this extent, he agrees with Marc Faber (cited in the previous post): we now have a bubble in government bonds.

But something will go bang. The real world shies from the inevitable conclusions of mathematical models. I think it will come as a crisis in foreigners' confidence in the dollar - there will be a reluctance to buy US Treasuries (we've already seen failed sales of government bonds in the UK recently, and when the next one succeeded, that's because it was a sale of index-linked bonds). Even now, the Chinese have switched from Agencies (debts of States and municipal organisations) to Federal debt, and within the latter, from longer-dated bonds to shorter-dated ones. If government debt was an aircraft, the Chinese would be the passenger insisting on a seat next the emergency exit near the tailplane.

To use a different analogy (one I've used before), drawn from the Lord of the Rings, the rally in the dollar and the flight to US Treasury debt seems to me like the retreat to the fortress of Helm's Deep: a last-ditch defence, doomed to be overwhelmed. Can we see a little figure about to save the day by dropping the Ring of Power into the lava in Mount Doom? We can hope; but you don't make survival plans based purely on optimism.

I therefore expect a transition from deflationary depression to inflationary depression, at some point. Perhaps a sort of 1974 stockmarket moment: an apparent turnaround, which when analysed can be shown to continue the real loss of value for some years. Only when national budgets are brought under strict control, will there be the environment for true growth. I don't see a willingness to tackle that, on either side the Atlantic, so disaster will have to be our teacher.

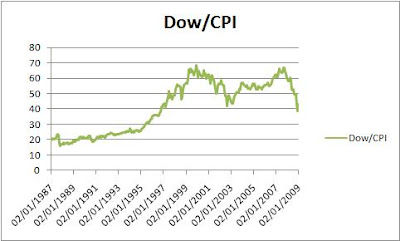

(Data source)

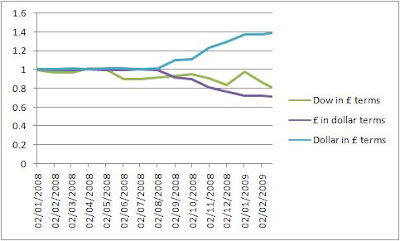

(Data source)

"Bang on target!"

"Bang on target!"