After the stockmarket ructions, pension funds are getting more cagey and thinking about weighting more towards bonds (htp: Pension Pulse). (A seminar I went to maybe 10 years ago predicted this trend.) Bill Gross of Pimco is also thinking that way; at the same moment when others reckon the recession's over, or nearly so.

My concern is that the market is now so volatile that only active traders will be interested. The smoothing approach of British with-profits funds has been undermined by downswings so sharp that more than once recently, they have had to apply penalties to investors seeking to exit early; which in turn will make those investors less inclined to reinvest in with-profits, and indeed quite possibly put them off investment generally.

That, plus the need to take more income as the population ages, plus a poorer next generation that will work longer, be taxed more and have less in State and other pension provision, plus the burgeoning of the world population, the gradual equalization of world average income (and it's a very low average), plus increasing ecological limits to fast-buck-type growth, all tend to make me more a bear than a bull for as far as I can see, whatever may happen in the short term as a result of desperate overstimulation with fiat cash.

Yes, there'll be opportunities for the agile financial player; but for the mom-and-pop saver?

Showing posts with label bonds. Show all posts

Showing posts with label bonds. Show all posts

Tuesday, September 22, 2009

Sunday, July 19, 2009

Step by step - how the dollar is recycled via China

A propos China and monetary inflation, please see two very useful and enlightening articles by The Contrarian Investor - this explaining why the money supply is growing there, and this detailing the steps by which money from the US goes on a round trip to China and back.

Locking the doors

The dethroning of the US dollar as the international trading currency is under way. New bonds issued by the International Monetary Fund in the form of "Special Drawing Rights" are related to a basket of currencies, thus diluting the dollar element and reducing America's opportunity to cheat the world by devaluation.

The same article describes a Chinese proposal to start issuing bonds denominated in renminbi, so that if the dollar does drop against the Chinese currency, all that will happen is that the dollar cost of the capital debt will increase.

It occurs to me that such extra security for lenders may help interest rates to remain lower than they otherwise would be. So the threat to borrowers is not that interest rates will increase, but that debt outstanding will continue to feel heavy, since inflation won't lighten the burden. In fact, the burden of foreign debt could get worse, if the dollar weakens in this new foreign-currency-mortgage era.

Another factor, which may be a deliberate strategy with an eye to the above, is China's own expansion of credit. If monetary inflation goes global - including in the East - then there's less hope that Western businesses could use relative currency devaluation to increase the demand for their goods and services. Manufacturers here will still be unable to compete and debt will grow. Our creditors will own us - we'll "owe our soul to the company store".

It's time to grasp the nettle - bust the banks who got us into this, have a tremendous clearout of debt from the system, reset wages and prices at lower (more internationally competitive) levels, get the people back to work and shrink the dead weight of government and its dependants.

That, or see what's left of our wealth leak away, and then suffer all the above as well - at even lower levels of per capita assets and income.

Doubtless the politically-favoured option is the latter - "Let it all happen on someone else's watch, after we've made ourselves into the New European Aristocracy and gone to our country estates." This would be a mistake. The palace of Versailles didn't protect Louis XVI, nor Waldsiedlung the East German communist elite.

The same article describes a Chinese proposal to start issuing bonds denominated in renminbi, so that if the dollar does drop against the Chinese currency, all that will happen is that the dollar cost of the capital debt will increase.

It occurs to me that such extra security for lenders may help interest rates to remain lower than they otherwise would be. So the threat to borrowers is not that interest rates will increase, but that debt outstanding will continue to feel heavy, since inflation won't lighten the burden. In fact, the burden of foreign debt could get worse, if the dollar weakens in this new foreign-currency-mortgage era.

Another factor, which may be a deliberate strategy with an eye to the above, is China's own expansion of credit. If monetary inflation goes global - including in the East - then there's less hope that Western businesses could use relative currency devaluation to increase the demand for their goods and services. Manufacturers here will still be unable to compete and debt will grow. Our creditors will own us - we'll "owe our soul to the company store".

It's time to grasp the nettle - bust the banks who got us into this, have a tremendous clearout of debt from the system, reset wages and prices at lower (more internationally competitive) levels, get the people back to work and shrink the dead weight of government and its dependants.

That, or see what's left of our wealth leak away, and then suffer all the above as well - at even lower levels of per capita assets and income.

Doubtless the politically-favoured option is the latter - "Let it all happen on someone else's watch, after we've made ourselves into the New European Aristocracy and gone to our country estates." This would be a mistake. The palace of Versailles didn't protect Louis XVI, nor Waldsiedlung the East German communist elite.

Monday, April 13, 2009

Protecting against inflation

Before we start, please read my disclaimer above!

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5: True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5:

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

When Nixon closed the "gold window" (15 August 1971), gold ceased to be a currency backing and became just another thing you could choose to invest in, so let's compare these assets from a little before that turning-point, onwards:

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

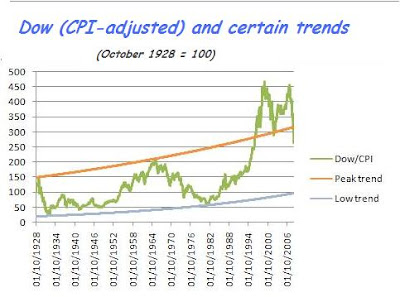

That depends on whether you read this as a statement about gold, or about the Dow. I looked at the Dow in inflation (CPI) terms a while back (December 2008):

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

Back to gold-pricing: it's also notable that the Dow is currently still worth some 8 ounces of gold, but in previous lows (Feb. 1933, March 1980) fell below 2 ounces: So should we still pile into gold, as a hedge against the further collapse of the Dow?

So should we still pile into gold, as a hedge against the further collapse of the Dow?

I think not. Firstly, the Dow may well have a rally, since it's fallen so sharply in such a short time. And secondly, this is missing the point, which is that we are looking to protect wealth against inflation, not against the Dow.

So another question is, how does gold hold its value during periods of price inflation? A period some readers may have lived through, is that after the oil price hike of October 1973. Here is what happened in the 5 years from 1974 to 1978:

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.But let's wind the clock back just a little - let's go back to that closing of the gold window again, and see what happened between August 1971 and the end of 1978:

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

Friday, April 10, 2009

More on bonds, and an alternative view

Antal E. Fekete is a professor of money and banking in San Francisco (such a beautiful place, too). He has a pet thesis about the bond market, which is that every time interest rates halve, effectively the capital value of (older) bonds doubles, to match the yield on new bonds.

So as long as we expect the government to try to stimulate the economy by lowering interest rates, there's a killing to be made in the bond market. Theoretically this could go on forever, even in a low-interest environment - the logic holds if rates go from 0.25% to 0.125% - provided the Treasury doesn't simply go straight to zero interest, of course.

Anyhow, his latest essay says that the monetary stimulus will simply be used to settle debts, since debt gets more and more burdensome in a deflationary depression; and settling debt instead of making and buying more stuff, continues to drive deflation. In this enviroment, few businesses will want to take on more debt (certain and fixed) in the hope of increasing their profits (far from certain, and very variable). On a national level, and following the ideas of Melchior Palyi, he now sees every extra dollar of debt as causing GDP to contract.

Therefore, valuations of most assets will continue to decline - except for bonds, which are now the focus for speculators. To this extent, he agrees with Marc Faber (cited in the previous post): we now have a bubble in government bonds.

But something will go bang. The real world shies from the inevitable conclusions of mathematical models. I think it will come as a crisis in foreigners' confidence in the dollar - there will be a reluctance to buy US Treasuries (we've already seen failed sales of government bonds in the UK recently, and when the next one succeeded, that's because it was a sale of index-linked bonds). Even now, the Chinese have switched from Agencies (debts of States and municipal organisations) to Federal debt, and within the latter, from longer-dated bonds to shorter-dated ones. If government debt was an aircraft, the Chinese would be the passenger insisting on a seat next the emergency exit near the tailplane.

To use a different analogy (one I've used before), drawn from the Lord of the Rings, the rally in the dollar and the flight to US Treasury debt seems to me like the retreat to the fortress of Helm's Deep: a last-ditch defence, doomed to be overwhelmed. Can we see a little figure about to save the day by dropping the Ring of Power into the lava in Mount Doom? We can hope; but you don't make survival plans based purely on optimism.

I therefore expect a transition from deflationary depression to inflationary depression, at some point. Perhaps a sort of 1974 stockmarket moment: an apparent turnaround, which when analysed can be shown to continue the real loss of value for some years. Only when national budgets are brought under strict control, will there be the environment for true growth. I don't see a willingness to tackle that, on either side the Atlantic, so disaster will have to be our teacher.

Prepare for a bond rout

What Mr. Greenspan and Mr. Bernanke have achieved is historically quite unique. They have managed to create a bubble in everything, everywhere in the world: in real estate, equities, commodities, art, worthless collectibles; even bond prices continued to rise as interest rates fell due to loose monetary policy. Since 2007 and 2008, everything has collapsed. But government bond prices continue to rise, and went ballistic between November 2008 and December 2008, when 10- and 30-year Treasury yields collapsed. So my view would be that this was the last bubble they managed to inflate. From here on, the government bond market will fall. In other worlds, the trend will be for interest rates to actually go up.

(Highlight mine.) Read the rest of Peter Schiff's interview with Marc Faber here.

PS: Faber indicates something like the following portfolio to Schiff:

Commodities (e.g. oil, agriculture): 20%

Emerging markets: 10% - 20%

Gold (in physical form): 10%

Cash (the US dollar, for now): 50%

(Highlight mine.) Read the rest of Peter Schiff's interview with Marc Faber here.

PS: Faber indicates something like the following portfolio to Schiff:

Commodities (e.g. oil, agriculture): 20%

Emerging markets: 10% - 20%

Gold (in physical form): 10%

Cash (the US dollar, for now): 50%

Thursday, March 19, 2009

Where is all the money going?

I read recently that both in the US and the UK, a significant part of the "quantitative easing" is repurchasing sovereign debt from foreign holders. In other words, money is being created to buy back government bonds from overseas investors.

This says two things to me: (a) the new money thus created is not going to help kick-start our economies, and (b) foreigners are losing confidence in us and want out, before inflation and defaults shrivel the value of their investment in us. As to the latter point, I said last August that I thought the Chinese wouldn't let themselves be swindled.

So I suspect we are still headed for slump, currency devaluation and, eventually, high interest rates.

Maybe a new currency, to whitewash the mess and make further progress towards some New World Order political grouping - Oceania, Eurasia etc. Any news on the Amero?

This says two things to me: (a) the new money thus created is not going to help kick-start our economies, and (b) foreigners are losing confidence in us and want out, before inflation and defaults shrivel the value of their investment in us. As to the latter point, I said last August that I thought the Chinese wouldn't let themselves be swindled.

So I suspect we are still headed for slump, currency devaluation and, eventually, high interest rates.

Maybe a new currency, to whitewash the mess and make further progress towards some New World Order political grouping - Oceania, Eurasia etc. Any news on the Amero?

Thursday, March 05, 2009

Wake Up!

Jim Mellon and Al Chalabi, authors of "Wake up!" , have emailed their latest interesting and useful newsletter. It concludes:

Our strongest recommendations are as follows:

• Prepare for rising inflation – continue to buy gold;

• Sell government bonds;

• Look for cheaply valued strong stocks – BAE and BP in the UK are two examples, and in the US we like Pfizer.

• Deploy cash wisely – our current favourites are, believe it or not, the British pound; the yen is weakening, but at 100 yen to the dollar it is a buy again.

• Avoid the US dollar and the Euro.

Like that bit about the pound - I was scratching around looking for something to save what's left of the savings.

Our strongest recommendations are as follows:

• Prepare for rising inflation – continue to buy gold;

• Sell government bonds;

• Look for cheaply valued strong stocks – BAE and BP in the UK are two examples, and in the US we like Pfizer.

• Deploy cash wisely – our current favourites are, believe it or not, the British pound; the yen is weakening, but at 100 yen to the dollar it is a buy again.

• Avoid the US dollar and the Euro.

Like that bit about the pound - I was scratching around looking for something to save what's left of the savings.

Wednesday, February 25, 2009

Theft by inflation has begun already

The UK Debt Management Office website shows that a UK Treasury bond offering 5% annual interest is, because of its current traded price, actually yielding 2.522793%.

But the risk of default, almost as high as Italy's government debt and far higher than even the USA's, is (as Jesse quotes) currently priced at 1.63%. (The market currently prices the risk of USA default at 1%.)

So after insuring for risk, 5-year UK sovereign debt earns you less than 0.893%.

Inflation, as measured by the Consumer Price Index*, now runs at 3%. In other words, a "safe" government bond loses you more than 2% a year.

And that's before inflation really gets going.

_____________________________________

*The Retail Price Index is a different measure of inflation, which takes into account mortgage costs. So after recent savage cuts in the bank rate, currently RPI should be negative. But wait until the private capital credit strike leads to higher interest rates, and judge.

But the risk of default, almost as high as Italy's government debt and far higher than even the USA's, is (as Jesse quotes) currently priced at 1.63%. (The market currently prices the risk of USA default at 1%.)

So after insuring for risk, 5-year UK sovereign debt earns you less than 0.893%.

Inflation, as measured by the Consumer Price Index*, now runs at 3%. In other words, a "safe" government bond loses you more than 2% a year.

And that's before inflation really gets going.

_____________________________________

*The Retail Price Index is a different measure of inflation, which takes into account mortgage costs. So after recent savage cuts in the bank rate, currently RPI should be negative. But wait until the private capital credit strike leads to higher interest rates, and judge.

Sunday, February 08, 2009

Denninger demystifies "the Fed"

You tend to get a clear and concise explanation from somebody, when they either blow their cool or are in a hurry to get somewhere else. Here, in a very crisp and useful post, Karl Denninger blows away the conspiracy theories surrounding the Federal Reserve.

He explain that his beef with them is that they are acting ultra vires (very damagingly), and notes that there is, unfortunately, no statutory penalty for their doing so. The caning will, he thinks, have to be administered by the bond market instead.

Some, like Eric Janszen of iTulip, would say that's exactly what the government intends.

He explain that his beef with them is that they are acting ultra vires (very damagingly), and notes that there is, unfortunately, no statutory penalty for their doing so. The caning will, he thinks, have to be administered by the bond market instead.

Some, like Eric Janszen of iTulip, would say that's exactly what the government intends.

Monday, February 02, 2009

IN- vs. DE- and an upcoming opportunity

Jesse echoes my hunch: deflation now, inflation soon-ish, with high interest rates for a bit. At that latter point, get your annuity and /or bonds, and benefits as rates subside. A guess, but it's comforting to see wise owls coming to the same conclusion.

You now have our investment gameplan for what is likely to be the rest of Jesse's life.

No, no "Jesse"; live long and prosper.

You now have our investment gameplan for what is likely to be the rest of Jesse's life.

No, no "Jesse"; live long and prosper.

Friday, January 23, 2009

Could US interest rates rise?

Brad Setser notes that far from declining in this recession, China's trade surplus is increasing, because although exporting less, it is also importing less. He estimates that China owns $900 billion of US Treasury bonds (and rising), some purchased indirectly via the UK.

However, enormous spending by the US means that it will have to issue a further $900 billion in bonds, and Setser opines, "China isn’t going to double its Treasury holdings in 2009."

If America needs to borrow more than China is willing to lend, the money must come from somewhere else, at a time when it's getting short generally. I have also recently read reports of concerns about the credit rating for US government bonds, which also supports the idea that rates will have to rise to pay for the increased risk of default.

How far will the dollar will be supported by this tendency? At least, in relation to sterling?

The UK is supposed to be an even worse basket case in terms of overall indebtedness, and that may make it politically very difficult to match rates with the US, because it could accelerate the rate of British house repossessions and business bankruptcies, even faster than in the US. So the pound could possibly fall even further against the dollar.

Perhaps Mr Cameron is right to warn that for the UK, the money may run out soon. Then we will have to pay high interest rates after all. And at last, we may be forced to borrow from the IMF and retrench savagely. Back to 1976. And will 1979 return? Cometh the hour, cometh the strong woman?

So, what's the implication of all this for the investor? Sell bonds and buy gold (despite its already high price) now, then reverse the process when high interest rates hit us?

However, enormous spending by the US means that it will have to issue a further $900 billion in bonds, and Setser opines, "China isn’t going to double its Treasury holdings in 2009."

If America needs to borrow more than China is willing to lend, the money must come from somewhere else, at a time when it's getting short generally. I have also recently read reports of concerns about the credit rating for US government bonds, which also supports the idea that rates will have to rise to pay for the increased risk of default.

How far will the dollar will be supported by this tendency? At least, in relation to sterling?

The UK is supposed to be an even worse basket case in terms of overall indebtedness, and that may make it politically very difficult to match rates with the US, because it could accelerate the rate of British house repossessions and business bankruptcies, even faster than in the US. So the pound could possibly fall even further against the dollar.

Perhaps Mr Cameron is right to warn that for the UK, the money may run out soon. Then we will have to pay high interest rates after all. And at last, we may be forced to borrow from the IMF and retrench savagely. Back to 1976. And will 1979 return? Cometh the hour, cometh the strong woman?

So, what's the implication of all this for the investor? Sell bonds and buy gold (despite its already high price) now, then reverse the process when high interest rates hit us?

Saturday, January 10, 2009

The next wave of bailouts

It's not just the banks that are short of money. Many US States and local authorities are also suffering financial problems, and this is affecting the trade in their bonds, i.e. their borrowings on the money market. ("What are bonds, exactly?" - see here.)

Michael Panzner reports that municipal bonds ("munis") offer a better yield than US Treasury bonds, but the difference is still not enough to pay for the extra risk. Professional investors are short-selling "munis". i.e. betting that they will fall in price. A steep fall may indicate imminent bankruptcy, and some say this is on the way for many authorities, as Mish reported at the end of December.

So, what will happen when the US Government is seen to be buying everybody's bad debts?

People (even here in the UK, where we tend to wait patiently for our wise rulers to solve all) are beginning to worry about inflation, and are thinking about investing again. An article in Elliott Wave International warns us not to be panicked into parting with our cash, and reminds us:

... there are periods when inflation does erode the value of cash. I mean, look at the seven years leading up to the October 2007 peak in U.S. stocks: big gains in the stock indexes, while inflation was eroding cash. No way did cash do as well as stocks during that time.

Right?

Wrong. Cash outperformed stocks in the seven years leading up to the 2007 stock market high. That outperformance has only increased in the time since.

Since this is the view I took and communicated to clients in the 1990s, you will understand that I didn't make much money as a financial adviser. But it was certainly good advice, even if it was based on strongly-felt intuition rather than macroeconomic analysis.

Not that analysis guarantees results, in a world where the money game's rules are changed at will by politicians with a host of agendas that they don't share with us ordinary types. But my current guess is that the stockmarket will halve again in the next few years, when compared with the cost of living.

Michael Panzner reports that municipal bonds ("munis") offer a better yield than US Treasury bonds, but the difference is still not enough to pay for the extra risk. Professional investors are short-selling "munis". i.e. betting that they will fall in price. A steep fall may indicate imminent bankruptcy, and some say this is on the way for many authorities, as Mish reported at the end of December.

So, what will happen when the US Government is seen to be buying everybody's bad debts?

People (even here in the UK, where we tend to wait patiently for our wise rulers to solve all) are beginning to worry about inflation, and are thinking about investing again. An article in Elliott Wave International warns us not to be panicked into parting with our cash, and reminds us:

... there are periods when inflation does erode the value of cash. I mean, look at the seven years leading up to the October 2007 peak in U.S. stocks: big gains in the stock indexes, while inflation was eroding cash. No way did cash do as well as stocks during that time.

Right?

Wrong. Cash outperformed stocks in the seven years leading up to the 2007 stock market high. That outperformance has only increased in the time since.

Since this is the view I took and communicated to clients in the 1990s, you will understand that I didn't make much money as a financial adviser. But it was certainly good advice, even if it was based on strongly-felt intuition rather than macroeconomic analysis.

Not that analysis guarantees results, in a world where the money game's rules are changed at will by politicians with a host of agendas that they don't share with us ordinary types. But my current guess is that the stockmarket will halve again in the next few years, when compared with the cost of living.

Thursday, January 08, 2009

Where to turn?

People are starting to run around looking for a haven for wealth. German bond issues partially unsold; US bonds yielding virtually nothing yet at risk of default and dollar devaluation; the UK's economic fundamentals worse than America's (without the advantage of having the world's reserve currency); others saying the PIGS (Portugal, Greece, Italy, Spain) may crash out of the Euro, and that the Euro itself may not see out another ten years.

Marc Faber is predicting that precious metals will outperform equities and bonds; this commentator reckons silver will outperform gold.

Dear me.

Marc Faber is predicting that precious metals will outperform equities and bonds; this commentator reckons silver will outperform gold.

Dear me.

Wednesday, December 17, 2008

The seventh seal

Denninger's question:

With the $7 trillion dollars we have committed we could have literally given every homeowner with a mortgage a fifty percent reduction in the principal outstanding.

This would have instantaneously stopped all of the foreclosures by putting all (essentially) homes into positive equity - overnight!

So why wasn't this done?

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.

This is the fourth horseman of the financial apocalypse that Michael Panzner predicted, as summarized here on Bearwatch on May 10, 2007.

UPDATE: Jesse comments on another fresh sum - tens of billions - needed to cover AIG's losses. As he says, there is an air of expectancy; but also of unreality, like the announcement of a major war.

With the $7 trillion dollars we have committed we could have literally given every homeowner with a mortgage a fifty percent reduction in the principal outstanding.

This would have instantaneously stopped all of the foreclosures by putting all (essentially) homes into positive equity - overnight!

So why wasn't this done?

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.This is the fourth horseman of the financial apocalypse that Michael Panzner predicted, as summarized here on Bearwatch on May 10, 2007.

UPDATE: Jesse comments on another fresh sum - tens of billions - needed to cover AIG's losses. As he says, there is an air of expectancy; but also of unreality, like the announcement of a major war.

Wednesday, October 15, 2008

More dire warnings

Karl Denninger is predicting a bond and currency crash in the US if banks aren't forced to disclose exactly what they do and don't have, so we can let the insolvent go down and release the liquidity into the right channels.

I hope the right path is taken, because my brother lives there.

By the way, in body language terms I read Hank Paulson as a hell of a bully. He looks like a totalitarian danger to me.

I hope the right path is taken, because my brother lives there.

By the way, in body language terms I read Hank Paulson as a hell of a bully. He looks like a totalitarian danger to me.

Wednesday, September 17, 2008

"... return OF capital, not ON capital"

I noted yesterday that foreigners were rushing to stuff cash into the US Treasury pillow. Brad Setser chimes in, explaining that although there's no yield (see his graph below), at least the capital is safe. We hope.

Tuesday, September 16, 2008

What will happen to interest rates?

Jim in San Marcos envisages eventual interest rate rises worldwide, to 10-15%. Commenting on the preceding post, Nikolay disagrees and James asks the question. I'm trying to understand the situation, like everyone else, so I'll have a go at thinking aloud:

Nikolay makes the point that people are becoming more concerned about the return OF their money, than the interest ON their money. So money-holders will limit demand for their cash by being picky about who they'll lend it to; control by quality screening, not by price.

Also, if people who habitually live on credit become frightened - and I think they are - then they will start trying to live within their means.

And discretionary expenditure could be reduced and/or redirected, not necessarily towards the cheapest end. I was listening to someone in the UK fashion industry on R4 yesterday, and they said far from everyone turning to Primark, the trend was to buy better quality, less of it, and make it last longer. Note that it's budget airlines like XL (competing on price) that are in danger of going down - they don't have much "fat to survive the winter".

From another angle, as the supply of cash and credit is dwindling, so are prices of houses and many other big-ticket items - look at the deals on cars and computers.

So it's possible to imagine that the contraction in credit may be approximately matched by a contraction in demand for credit, at least for a time. Bankruptcies and house repossessions will burn off a lot of debt, so we'll see a lot of ordinary people cleaned out and possibly more bank failures, especially as (in response to reduced expenditure) unemployment grows.

Thus we could see a recession in which the government tries to stimulate consumer demand by cutting interest rates - and this may not work, because many won't want (or be able to afford) to take on debt at any price; and those who do have cash and are watching prices fall, will hang off, waiting for further falls - as happened in Japan.

But Jim himself has acknowledged that rates may be cut in the short term. What about the longer term?

More unemployment, lower profits etc will shrink the tax base and increase the benefit burden. The budget won't balance without cuts in the public pay sector (= even less tax, even more benefits) or more government borrowing - I don't see how we in the UK could be taxed much more. So there's a danger that while consumer debt leads the way into recession, increased government demand for debt (and increased concern about government creditworthiness) may then lead the way to higher interest rates on State bonds.

When the State has more dependents, it will also find that not everything is going down in price. Food and fuel are must-haves, so benefits will have to be increased to cover the cost of such items. There will be more poor, and they will each need more. And the government will have to borrow more.

Or start devaluing the currency. Then all bets are off.

So here's a scenario: interest rates kept low, or cut; then government borrowing rises, while the economy burrows into a slump; then the real "credit crunch": the moment when the government, like an ad-man under pressure, needs a feelgood episode and, despite having sworn off it for life, reaches for the booze or the white powder, in this case inflation.

More and more, Michael Panzer's dire financial drama seems plausible.

Nikolay makes the point that people are becoming more concerned about the return OF their money, than the interest ON their money. So money-holders will limit demand for their cash by being picky about who they'll lend it to; control by quality screening, not by price.

Also, if people who habitually live on credit become frightened - and I think they are - then they will start trying to live within their means.

And discretionary expenditure could be reduced and/or redirected, not necessarily towards the cheapest end. I was listening to someone in the UK fashion industry on R4 yesterday, and they said far from everyone turning to Primark, the trend was to buy better quality, less of it, and make it last longer. Note that it's budget airlines like XL (competing on price) that are in danger of going down - they don't have much "fat to survive the winter".

From another angle, as the supply of cash and credit is dwindling, so are prices of houses and many other big-ticket items - look at the deals on cars and computers.

So it's possible to imagine that the contraction in credit may be approximately matched by a contraction in demand for credit, at least for a time. Bankruptcies and house repossessions will burn off a lot of debt, so we'll see a lot of ordinary people cleaned out and possibly more bank failures, especially as (in response to reduced expenditure) unemployment grows.

Thus we could see a recession in which the government tries to stimulate consumer demand by cutting interest rates - and this may not work, because many won't want (or be able to afford) to take on debt at any price; and those who do have cash and are watching prices fall, will hang off, waiting for further falls - as happened in Japan.

But Jim himself has acknowledged that rates may be cut in the short term. What about the longer term?

More unemployment, lower profits etc will shrink the tax base and increase the benefit burden. The budget won't balance without cuts in the public pay sector (= even less tax, even more benefits) or more government borrowing - I don't see how we in the UK could be taxed much more. So there's a danger that while consumer debt leads the way into recession, increased government demand for debt (and increased concern about government creditworthiness) may then lead the way to higher interest rates on State bonds.

When the State has more dependents, it will also find that not everything is going down in price. Food and fuel are must-haves, so benefits will have to be increased to cover the cost of such items. There will be more poor, and they will each need more. And the government will have to borrow more.

Or start devaluing the currency. Then all bets are off.

So here's a scenario: interest rates kept low, or cut; then government borrowing rises, while the economy burrows into a slump; then the real "credit crunch": the moment when the government, like an ad-man under pressure, needs a feelgood episode and, despite having sworn off it for life, reaches for the booze or the white powder, in this case inflation.

More and more, Michael Panzer's dire financial drama seems plausible.

Bonds to crash?

The Fed may lower its funds rate in the short term, but Jim in San Marcos is predicting steep rises in worldwide interest rates and (therefore) a sell0ff in suddenly-very-uncompetitive bonds.

Saturday, August 30, 2008

Financial Apocalypse Now

Cash, Gold, and Swiss gov't bonds.

In 7 years, it could very well be that a Krugerrand buys a decent house!

... says an anonymous commentator on Nourishing Obscurity, after listing multiple dire threats to our wealth and security. Any other expert care to give a view - and put his/her name to it?

In 7 years, it could very well be that a Krugerrand buys a decent house!

... says an anonymous commentator on Nourishing Obscurity, after listing multiple dire threats to our wealth and security. Any other expert care to give a view - and put his/her name to it?

Subscribe to:

Posts (Atom)