The global financial crisis is also a local issue for the UK, dubbed the

'global capital of money-laundering' in a Private Eye magazine investigation by Richard Brooks (August 2012).

The role of the financial sector in Britain ballooned in the years before the breakdown:

this 2011 report by the Bank of England (pdf) shows that its annual growth was 6%, twice that of the economy as a whole.

That's why we need it. But why does the rest of the world need it to be in London?

In part the answer is that, as David Malone explains below, our system is particularly good at handling money without asking too many awkward questions. Shell companies make it hard to track down who is running businesses.

Moreover, unless money is definitely proved to have come from illegal activities, the authorities are unable to treat money transfers as criminal "money-laundering". Malone's only censored post to date, from which he quotes sections here, was a detailed investigation for Reuters into alleged money-laundering in Cyprus; but his original piece fell foul of that (perfectly logical, of course) lack-of-predicate-crime rule.

In this context it's worth remembering that the UK is also known as the "

libel capital of the world", with potentially big payouts for plaintiffs if the defendant cannot prove his allegations (

up to three years ago, it could get much worse than a civil court case: there was such a thing as criminal libel, punishable by imprisonment - this was what caused Private Eye's then editor Richard Ingrams to throw in the sponge when Sir James Goldsmith pursued him in July 1976).

And now, following the Leveson inquiry into abuses by mainstream journalists,

bloggers may find themselves at risk of high financial penalties, without having the legal and financial resources of the conventional Press to help defend themselves.

I also reproduce here a piece by France-based blogger John Ward, reporting on the vast quantities of cash held in offshore banks that might (if captured onshore) otherwise contribute up to a trillion pounds to the UK economy.

In a digitised world, capital can zip around the globe far faster than leaden-footed regulators and tax authorities. Cyber-money is also very useful for dodging attempts by local banks to grab it to shore up their reserves, as we are seeing in Cyprus - and

this article on Charles Hugh Smith's site goes further, implying that EU banks may have influenced a delay in the European Central Bank's enforcement action against the island, to allow them time to extract most of their cash before the shutters went down.

Finally, delay can help bosses as well as the banks they run: there is

much noise being made at the moment about "examining powers to take legal action" against three directors of HBOS who were on watch when billions were lost by their company; but the Financial Services Authority has a

strict time limit of three years to take disciplinary action against individuals, and that deadline has come and gone. A cynic might wonder why exactly the FSA missed it, but the fact remains that we have to obey the law as it stands, so I don't expect any retrospective ruling against these people, who are far from the only ones to have (allegedly) overseen significant losses in the banking sector.

My sincere thanks to David Malone and John Ward for permission to reproduce their posts.

________________________________________________

Making the Truth Illegal – revisited

“Making the Truth Illegal” is the title of the only post I have ever removed from this blog.

I removed it because I was threatened with legal consequences if I did not. (Plus, I would like to add, some of the way I had written the blog post was stupid and could have hurt someone who had helped me.)

The post concerned an article I had written for Reuters which they decided they could not/would not publish. Reuters pulled the article because they and I had been threatened, by a major European Bank, with legal consequences if they did not. The title of the article was “Cyprus, Magnitsky and the truth about Money Laundering.”

Although I cannot publish the article I can show you how it began and tell you how it is, that the truth it contained was made illegal.

The article began:

Money laundering is the life blood of organized crime. Without it crime would simply not pay. But who does the laundering? The easy and obvious answer is criminals. But that is completely wrong and is at the root of our inability to stop it.

Criminals are the people who need money laundering. They are the clients. But they do not, themselves, know how to launder money. The only people who do know, and who are in positions to do it, are those whose day jobs are the many professional services which make up laundering: the accountants, lawyers, company registration and management agents, account managers in banks and company directors in companies that have no reason to be, other than to pass hot money through an endless spin cycle. In organized crime, criminals provide the crime but professionals provide the organization.

Of course we could get jesuitical about it and say, but those professionals who launder are criminals. Which would be fine, except that we do not treat them as criminals. Criminals break laws. Professionals do not, they have ‘failures of compliance’. One is considered an active, purposeful ‘doing’ of something, for which punishment is de rigeur. The other is excused as an unfortunate and unintentional ‘not doing’; an oversight, omisssion or failure to do, for which one and one’s employer get admonished to ‘do’ better. And as long as you promise you will, all is considered fine and finished. There may be a small fine but nothing to lose your bonus over. No one senior ever goes to gaol.

Criminals are investigated – by police. Professionals are ‘regulated’ – usually, and rather conveniently, by themselves or colleagues. People who rob banks have legal problems. People in banks, who rob people, or help others to rob them by laundering their money for them, they have regulatory issues. One is serious the other is a joke. How many bankers actually went to prison from Wachovia or Citi or HSBC?

All this might seem rather sweeping. But it is not. It is just that usually we do not get to hear about the people and businesses who do the actual laundering nor what happens to them afterwards. When money laundering is reported it is usually the lurid details of the clients of the money laundering, the drug cartels and terrorist organization, who get all the headlines. Hardly ever do we hear of the launderers themselves. And that is because, as already noted, they are never ‘guilty’ of having ‘done’ anything. But events in Cyprus have recently given us a rare opportunity to lift the sewer’s cover, peer inside and see at least some of the people who failed to act; who by omission, oversight, laziness or complicity, intentionally or otherwise, ‘helped’ to launder money.

As the philosopher Edmund Burke famously noted, “All that is necessary for the triumph of evil is that good men do nothing”.

As you can see the purpose of the article was not simply to prove, what everyone already knew, that Cyprus had indeed been laundering dirty Russian money, but to say something about WHO actually does the laundering. The point was to finger the launderers themselves not their clients. Of course that meant naming companies, lawyers, company directors, company registration agents, and last but not least, the banks and individuals in them. These are, of course, people who are not used to the idea that they can be named, take grave exception to being named and who have the power, I discovered, to make sure they are not.

The article also did one further thing. When you added it all together and told the whole tale in all its detail, with all the names, dates, places and amounts, one further conclusion jumped out. The lawyers, accountants, company directors and bankers, who did the laundering, are also the people who the anti money-laundering system relies upon to police the system and stop the laundering. The inescapable conclusion is that the anti-money laundering system not only does not work, but seems expressly fashioned to make sure it does not work.

It is possible – it happened in the Magnitsky case – for a criminal to buy a bank and be granted a bank license. Yet the law says it is the directors of such a bank who will be relied upon to contact the authorities about suspicious transactions. Criminals don’t often turn themselves in, yet in every country this is the non-system our leaders and financial experts maintain. In the UK the law is set up so that a company can be set up without any due diligence at all being done to determine the character let alone the actual identity of the owner. Because of this ‘loophole’ as the authorities coyly refer to it, the UK is home to tens of thousands of shell companies set up by criminals and used for criminal purposes. This may sound like a fantastic charge and one I cannot possibly substantiate. Yet almost every major case of fraud or money laundering will involve UK shell companies.

Follow the Magnitsky money and you will see it pass thorough UK shell companies. The same goes for the

$64 billion of state money stolen from Kyrgyzstan much of it then passed through UK shell companies. Or the on-going case of

money laundered out of Ukraine by means of a fake oil rig purchase. That money too passed through UK companies.

I could give you plenty of other examples but the important point is that NO ONE in authority can offer a shred of evidence to show that I am wrong no matter how many criminal companies I claim there are likely to be, for one simple reason. THEY HAVE NO IDEA WHO OWNS THE COMPANIES. The system is set up so no one knows. Companies register owners but they can be other companies in other jurisdictions. And it is easy to set up a company in such a way so that no one checks on the owner at all, ever. That is the system we maintain.

Every minister who has ever had the power to change this state of affairs has been aware of this but they have all chosen to leave it that way.

In short we have a system which is conveniently designed so it does not stop money laundering but does make sure no one will be prosecuted. It serves to shield the guilty not stop them.

I realize these are statements that can still be dismissed as ‘conspiracy’. Without the 8000 words of detail the article contained, without the references to over a hundred pages of bank transfers and company records, I am left with just what I know to be the case without being able to show you what convinced me.

All I can do, as promised, is show you the final ‘shell’ which surrounds everything else and which allows the rest of the corrupt system to exist and do its job. The last shell is a legal one and I had not understood its importance, nor its power, until it did its job and stopped me publishing.

This is how it works.

First a few facts. In the Magnitsky case $230 million was stolen from the Russian state. That money was then laundered in a scheme that involved five deaths, a lorry load of bank records that exploded, eight banks, numerous shell companies and complete, abject and total regulatory failure. It is called the Magnitsky case after Sergei Magnitsky who was found dead, handcuffed on the floor of a cell in a Russian prison. His body, photographed at the time, was covered in bruises.

Mr Magnitsky had been arrested and then held without charge or trial in the custody of the Russian Interior Ministry for nearly a year. He had been detained shortly after he had named in official testimony Interior Ministry officials and certain tax officials as the criminals behind the theft. The men he named were the ones who arranged his detention.

BUT, the Interior Ministry held its own investigation. What it found was that although the money had indeed ‘gone missing’, none of the officials Mr Magnitsky had named were, according to their official investigation, guilty of anything other than being ‘tricked’ by person or persons unknown. The Ministry did try to suggest several culprits but two of them died mysteriously of heart attacks a thousand kilometres from their homes before they could testify, while another had, rather embarrassingly, died before the crime he was accused of had even been committed. The Ministry looked silly even by Russian standards and no case was brought.

Eventually the Russian officials accused the deceased Mr Magnitsky of being the mastermind behind the crime he had been investigating. At one point the Russian state said it was going to put him on trial posthumously. So far it has not. And thus the case rests with the conclusion that there was no crime, only a ‘trick’ with no one found guilty.

It was also decided in Mr Magnitsky’s absence that despite the photographic evidence of his beaten body, he had died of natural causes and no crime had been committed there either. Case closed. And that ‘Case closed’ is what it is all about.

In the end it doesn’t matter what actually happened nor what evidence is to hand. As long as some official body does its own ‘investigation’ from which it concludes nothing happened, then nothing did, and the case can be closed. Not only that but if anyone should try to look for themselves at the evidence they cannot refer to anyone or any bank as being involved in criminal behaviour of any kind. Because there wasn’t any.

If no money was stolen – and none was because the Russian said so – then no one could have laundered any. How can you launder money that was not stolen?

The Russian decision meant, in legal parlance, that there was no ‘predicate’ crime – no crime from which other crimes followed. Which means, if one authority says there was no crime, every other authority in every other country, should it want to, can point to this judgment and say, ‘why should we investigate anything if there was no crime in the first place?’

This meant when an official complaint was sent to the Cypriot authorities in 2008 alerting them to the Magnitsky affair, right at its beginning, they could ignore it. And they did. The Cypriot police were sent an official complaint in 2008, and to this day they have never replied to it nor even questioned the people, even Cypriot people, named in it.

In fact even when the Cypriot Authorities were sent another much more detailed complaint in 2012, which gave them dozens of leads and lines of enquiry they wrote back saying,

“…it is important that we firstly obtain information from the Russian authorities about the predicate offence or offences committed in Russia.

Thus we plan to contact the Russian authorities in order to obtain information…”

And of course there was no predicate crime. Not officially. Even though companies were stolen and hundreds of millions did ‘go missing’.

Similarly, in 2010 another complaint was sent about the Magnitsky affair, this time to the Austrian authorities. The complaint alleged that the very large and powerful Austrian bank Raiffeisen, had handled much of the money that had ‘gone missing’. The Austrian authorities opened an investigation which concluded Raiffeisen had done nothing wrong at all. Case closed.

The Russians found no crime had been committed on their patch. The Austrians found nothing on their patch either.

This is despite the fact that Raiffeisen did handle the money. But you see handling is NOT laundering. Laundering requires the money be illicit AND that Raiffeisen knew, or reasonably could have known, the money was illicit. And the Austrian regulator concluded that Raiffeisen could not have known there was anything wrong with either the money it was handling, nor the bank from which it came nor the owner of that bank. The owner we are talking about here is the criminal – a convicted criminal who owned his own bank – mentioned earlier. According to Raiffeisen and the Austrian regulator the criminal past of the owner of the bank Raiffeisen was doing business with, could not have been known till a later date.

Now I find this judgement to be difficult to understand since the man in question had been convicted in Russian court in 2006. There are court transcripts of his admission of guilt which I have read. Yet Raiffeisen was handling the money in question in 2008.

BUT it doesn’t matter if I or you find this odd. The only FACT that is important, is that the Austrian regulator looked and found Raiffeisen NOT guilty of any crime. And so they are innocent. Case closed.

This is how you can end up, as I did, compiling facts and dates, evidence of bank transfers subpoenaed in court, which lead you to a conclusion that you are nevertheless not allowed to make public. You can present all the evidence but you must contrive to do it without ever mentioning the name of a crime, nor suggesting any illegal activity in the piece. And of course you certainly cannot conclude in writing what the evidence suggests. If you try to , as I found, you are threatened with the law.

And that is how you make the truth illegal.

If this was just one case it would be horrible but isolated. But it is not. This use of official and legal judgements to squash the truth is exactly what happened in the case of Jonathan Sugarman and UniCredit. He found evidence that UniCredit was very seriously breaking the law. He got an outside company to check and they agreed. The Irish regultor however, said, ‘There’s nothing to see here move along’. And Jonathan was threatened with leagal action if he did not go quietly away and hide.

What does all this mean for money laundering?

Here is how I concluded the article I cannot publish.

People love to talk about the ‘risks to banks and companies’ from money laundering. What risks? Think of the notorious cases of money laundering before Magnitsky: Citi., Wachovia, HSBC. No one was gaoled. No one senior even lost their job. Fines are a joke. Wachovia, for example handled or laundered over $370 billion of dirty or suspect money out of Mexico. They were fined one two thousandth of that amount, just $160 million. As a percentage of the direct financial benefits accrued to Wachovia, from having the dirty money flowing through their books, fines for money laundering are vanishingly small and better thought of as a tip pressed into the palm of a compliant doorman.

In reality, simply looking at the facts of what it has cost the banks in gaol time, fines or even something as intangible as their standing with their regulators and governments, it is very much worth it to launder. As for ‘standing’ or reputation – being guilty of huge money laundering did no harm to Citi when it came to bailing them out. Nothing untoward has happened to Wachovia or HSBC. In short – on a cost benefit analysis I would say it is of huge benefit and virtually no risk, for any bank large enough to be able to launder money, to do so.

And what of all the many companies and professionals, the company agents, lawyers and accountants, who do the jobs which make up the bulk of the work of laundering? Are there any real risks for them? I would say there are few because our system simply does not investigate what they choose to do. Instead it is very careful to only ask them to fill out forms, to self regulate and to ‘comply’.

I think the questions we need to ask ourselves and our politicians is why is it that the financial world is ‘regulated ‘ while we, ordinary citizens, are policed? Why do they have regulations to observe, while we have laws to obey? Why are they asked to merely assess themselves while we are investigated by officers of the law? Who profits from this careful double standard?

When you boil it all down, anti-money laundering is about asking criminals and the law abiding, both, to write reports about themselves. Needless to say the criminals lie. But we pretend not to notice, and so in every country all the paperwork says there is no money laundering going on. Yet hundreds of billions is laundered every year.

________________________________________________

Now, John Ward's post: A story goes global, and damns the self-styled elite

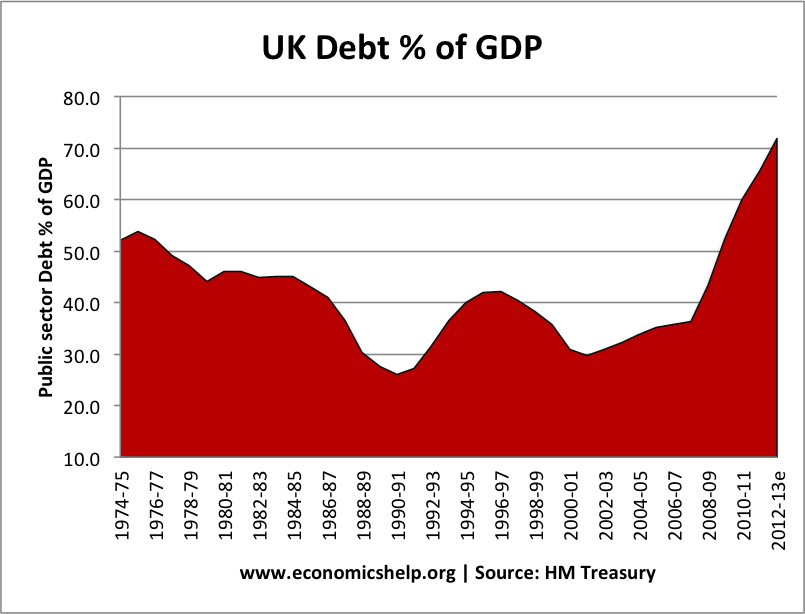

UK debt versus GDP…would be transformed if tax evaders paid their way

The amount of tax-haven monies controlled by British banking is estimated to be £1.26trillion. That is six NHS budgets, twenty defence budgets, eighteen welfare budgets, and five UK State pension budgets planned for the UK’s 2014 fiscal year. The evasion total is the same size as the entire public sector pension fund, and only slightly smaller than Britain’s total national debt.Last Friday, every French newspaper’s front-page from the Rightist

Le Figaro to the Leftist

Liberation led with the series of offshore tax haven scandals now threatening to overwhelm President Francois Hollande. In the UK, the Virgin Islands name-and-blame game has put David Cameron very seriously on the back foot. And the obvious connection between Tory newspaper

The Daily Telegraph’s ownership and the Sark tax-evasion scandals there has shaken many from their torpor of bland acceptance. Throughout Europe’s citizenry this morning, there is a growing feeling that – far from being a tiny minority – rich-businessman tax evasion is the norm.

The Irish Times last Saturday threw up a staggering statistic: over 30,000 Irish firms have directors registered in offshore jurisdictions. Furthermore, in Sark specifically – population 600 – there are more than 11,000 bank accounts of directors registered to Irish firms – 18 for every island resident. There are roughly 560,000 business enterprises in the Irish Republic, of which no more than 240,000 could be described as turning over enough to make directors’ offshore holdings worthwhile. Thus an incredible 1 in 8 of the country’s business élite is stealing from the taxman.

This isn’t going down well among Ireland’s poorer classes – not least because Enterprise Ireland’s own data showed that over a thousand of its business members received government funding in 2010, with a total of 86 receiving commitments for financial support in excess of €100,000 for significant R&D projects. Life is a thing of give and take, but for Ireland’s top earners it seems to be all take and no give.

Coming in the wake of similar behaviour over the last five years from the West’s bankers and the Greek econo-political class, there is something about offshore – and the Virgin Islands story in particular – that seems to have completed a synapse connection….thus allowing the penny to drop at last: the ordinary folks are being gang-raped by greed on all sides.

As many of us always suspected, the insouciant wealth-accumulation obsession of frontal-lobe afflicted bankers is what joins them at the hip with the top earners in business – regardless of which country or culture one surveys. The ever-unpleasant HSBC’s Guernsey operation was

last November shown to be shielding £699m in 4,388 accounts in Jersey – with one investor holding £6million. The average balance is £337,000. Equally, the true extent of American and German fat cat tax-evasion has been unearthed by the German Federal Intelligence Service. It is conducting a widespread investigation into Lichtenstein banking – and that of Luxembourg – where tens of thousands of US and Bundesrepublik tax evaders are hiding massive amounts of cash.

A 2012 study of 60 large US companies found that they deposited $166 billion in offshore accounts during 2012, sheltering over 40% of their profits from U.S. taxes. Yet Wolfgang Schäuble has invested a great deal of spin-time trying to suggest that Cyprus shielding the wealth of crooked Russians was atypically evil enough to warrant Berlin’s snaffling of the island’s potential energy economy. This is now shown to have been bollocks not just as a rationale, but also in its alleged uniqueness. And some of Wolfie’s mates appear to be up their eyes in similar operations around the world.

But the burgeoning scandal is more embarrassing for David ‘Legup’ Cameron than any other leader because, as the Guardian for once reported accurately at the weekend, ‘one nation in particular has ties to offshore havens everywhere. It’s a veritable nexus of offshore influence, related to havens in the Caribbean, and much closer to home. That nation is, of course, the United Kingdom.’

As so often happens today, without the leaking of more than 2m offshore files to the International Consortium of Investigative Journalists (ICIJ), the extent of this three-faced hypocrisy would be unknown to us still. So while George Osborne talks a good game about “all being in this together” – and Cameron witters on about “not wanting to associate with” tax evaders – the reality is their administration and bankrolling ranks are crammed with some of the worst offenders and facilitators. Lord Green ran HSBC for years, Jeremy Hunt is an aggressive tax-avoider, the Barclay Brothers run Sark, Boris Johnson is a particular favourite of the Sarkist-Banking fraternity, and numerous large Tory donors are among the wealthy ripping off Sovereign revenue offices: more than 175,000 UK companies have directors in offshore jurisdictions.

The ICIJ’s project uncovered a network of empty holding companies and names essentially rented out to fill out boards of non-existent corporations, including a British couple listed as active in more than 2,000 entities. This is a mirror image of the tiny survey conducted

by The Slog last week into the identity of those who were early departees from the Cyprus depositor haircut.

For me, however, it is a calculation of the totals involved globally that change these revelations from being just another “it’s the rich what gets the sorrow” yarn into something that just might – we live and hope – finally get Middle England off its sofa and angry enough to demand justice.

A 2012 report from the

Tax Justice Network (a UK company) estimated that between $21 trillion and $32 trillion is sheltered from taxes in unreported tax havens worldwide. Tax havens have 1.2% of the world’s population and hold 26% of the world’s wealth – including 31% of the net profits of United States multinationals. We are indeed talking about ‘a tiny minority’ here – the usual suspects – but also a colossal percentage of the money that should have been paid in Sovereign taxes. Financial opinion leaders I asked last week for an estimate of the percentage of offshore monies administered by British banking thought the number to be between 40 and 60%.

Being kind to the perpetrators and assuming (a) the lower end of those estimates and (b) lowest assessments of global market size and (c) a net tax rate of 15% being evaded, the Government of the United Kingdom knowingly loses

almost exactly a trillion pounds in tax revenue thanks to the havenism endemic in the banking system it is supposed to regulate.

That is six NHS budgets, twenty defence budgets, eighteen welfare budgets, and five UK State pension budgets planned for the UK’s 2014 fiscal year. The evasion total is the same size as the entire public sector pension fund (itself a disgrace of illegal embezzlement) and only slightly smaller than Britain’s

total national debt.

It is a mind-boggling 70% of United Kingdom GDP.But here’s the final brass-necked irony: stand by for an attempt by the

Global Looters to use this tax evasion reality as the excuse for stealing the savings of everyone with over £100,000 in a bank account that

isn’t offshore….and represents the life-savings of a law-abiding taxpayer.

________________________________________________

Principal articles reproduced / referenced above:All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.