Australian blogger The Contrarian Investor points out differences between now and the 1930s that mean gold is merely another speculative investment, not the sure-fire winner it was then.

Having said that, there is a strong psychological / political / historical / economic strand in gold, and it is significant that central banks are now net purchasers. And China recently announced its intention to increase holdings from 1,000 tonnes to 6 or 10 times that over the next decade, having already boosted them from a level of 600 tonnes in 2003. China is now the world's largest producer of mined gold.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sunday, January 31, 2010

The Brits are dumber than the Yanks; and Keynes will always beat Hayek

Shakespeare's plays imply a great deal about his audience, and so does the video below (hat-tip to Nathan Martin). I have not seen material like this made by and for the British market. Why not?

Economists are still warbling the lays of the free market, but I haven't seen them explain how Western prices and incomes can dwindle on the global market when our debt is huge and fixed. I think the best we can hope for is to manage our fall in average living standards, so that it happens more slowly.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Economists are still warbling the lays of the free market, but I haven't seen them explain how Western prices and incomes can dwindle on the global market when our debt is huge and fixed. I think the best we can hope for is to manage our fall in average living standards, so that it happens more slowly.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, January 30, 2010

Investors to turn from the US to emerging markets?

Last October, James Quinn, senior director of strategic planning at The Wharton School of University of Pennsylvania, reviewed the US as an economy in which to invest, and he concludes:

An aging country dependent upon oil and debt for sustenance is not the ideal place to invest, and that may be the conclusion that many come to, giving a boost to emerging economies. Domestically, technology – including medical technology - and alternative energy look to provide the best chance for the United States to regain some of its lost prosperity, and therefore are potential areas of focus for investors.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

An aging country dependent upon oil and debt for sustenance is not the ideal place to invest, and that may be the conclusion that many come to, giving a boost to emerging economies. Domestically, technology – including medical technology - and alternative energy look to provide the best chance for the United States to regain some of its lost prosperity, and therefore are potential areas of focus for investors.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

UK GDP and forcing the money supply: flogging a dead horse?

A few days ago, I charted the relationship between GDP and the money supply as measured by M4 (bank lending to the private sector). We now hear that estimated GDP for 2009 was negative 4.8% (the worst since 1921) and the Bank of England's website shows bank lending grew in the first 3 quarters of 2009 by 5.1% annualised.

The BoE's figures for M4 only go back to the spring of 1963, and in all the time since then GDP has never been negative, yet with all this stimulus (and the enormous central bank quantitative easing that forced it) it still fell, so who knows what might have happened without it.

It seems to me that the doctor has been disguising the symptoms, and the illness still has a long way to run.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

The BoE's figures for M4 only go back to the spring of 1963, and in all the time since then GDP has never been negative, yet with all this stimulus (and the enormous central bank quantitative easing that forced it) it still fell, so who knows what might have happened without it.

It seems to me that the doctor has been disguising the symptoms, and the illness still has a long way to run.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Friday, January 29, 2010

If only

If only Judge Judy could be asking the questions at the Chilcot Enquiry today.

"Don't bother me with this nonsense."

"Are you on medication?"

"Speak not!"

"I don't believe you."

"That's not what I asked you, sir."

"I don't give a rat's tutu for your pain and suffering."

"Baloney!"

"On my worst day, I'm smarter than you on your best day."

"What you have said doesn't make sense, and I'll tell you why."

"Quiet! When my lips start to move, your lips stop."

"Are you chewing gum?"

"Stop messing with your papers. Look into my eyes, that's how I know if you're telling me the truth."

"Is English your primary language, sir?"

"They don't pay me enough for this." (Bert, quietly: "Oh, yes, they do.")

"Goodbye, have a nice life."

Oh, if only...

"Don't bother me with this nonsense."

"Are you on medication?"

"Speak not!"

"I don't believe you."

"That's not what I asked you, sir."

"I don't give a rat's tutu for your pain and suffering."

"Baloney!"

"On my worst day, I'm smarter than you on your best day."

"What you have said doesn't make sense, and I'll tell you why."

"Quiet! When my lips start to move, your lips stop."

"Are you chewing gum?"

"Stop messing with your papers. Look into my eyes, that's how I know if you're telling me the truth."

"Is English your primary language, sir?"

"They don't pay me enough for this." (Bert, quietly: "Oh, yes, they do.")

"Goodbye, have a nice life."

Oh, if only...

Sunday, January 24, 2010

Investment review (and is cash a good investment?)

FURTHER UPDATE

Reportedly, Swiss-born and Thai-resident investment guru Marc Faber has recently repeated his view that the US cannot escape crisis (e.g. in pension funding) and will be forced to increase the money supply, so further weakening the dollar, at which point, he says, it will become necessary to invest in equities in order to mitigate the effects of inflation. But not yet...

"In that situation you are better off in equities. I am not saying that you should buy equities today. But the dollar will go down, they will have to print a lot of money."

Meanwhile, a sober Australian blogger-commentator opines that the UK may face a currency crisis within the next 3 - 5 years, followed by Japan and the USA (though Portugal, Ireland, Italy and Greece may have their crises before all these three).

UPDATE

Since writing this article today, I have read Steve Keen's discussion of the causes of the Great Depression and how our situation now is worse than it was then. Professor Keen, one of the very few to predict the credit crunch, says:

"...since debt today is so much larger (relative to GDP) than it was at the start of the Great Depression, the dangers are either that the fall in demand could be steeper, or that the decline could be much more drawn out than in the 1930s."

____________________________________________________

An industry expert writes

Howard Marks, chairman of a large investment firm, publishes his quarterly report to investors (hat-tip to Michael Panzner).

Panzner picks out a couple of points - the stock market rally is not based on improvement in economic fundamentals, and commercial real estate looks to be a difficult area for some time yet - but Marks concludes, I think a little tentatively, that "most assets are valued about fairly today". This conclusion dovetails with Marks' business, which is sifting and selecting stocks that his company judges are good buys.

Market manipulation?

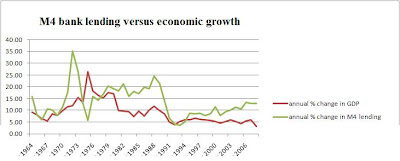

Like Panzner, however, I tend to be more bearish - I am part of that "wall of worry" that the American investment establishment is desperate for us all to climb up, or over. It seems to me that, as others have said before, nothing that led to the present crisis has yet been fixed. Some days ago, I looked at the relationship between bank lending and Gross Domestic Product (GDP) in the UK, and I reproduce below a graph I made to represent year-on-year percentage changes in both:

Two things stand out: firstly, the banks consistently increase the money supply more than the growth of GDP, which a monetarist would say is inflationary. Secondly, the general trend since the mid-1970s appears to be a slowing of economic growth, despite all the monetary stimulus. Instead, the extra cash (aka "liquidity") went into a combination of spending on imports (how much of the stuff in your house and on your driveway was made here?) and rising asset prices (houses and shares). Now the tide has turned, unless we're prepared to return quickly to our former reckless borrowing.

Two things stand out: firstly, the banks consistently increase the money supply more than the growth of GDP, which a monetarist would say is inflationary. Secondly, the general trend since the mid-1970s appears to be a slowing of economic growth, despite all the monetary stimulus. Instead, the extra cash (aka "liquidity") went into a combination of spending on imports (how much of the stuff in your house and on your driveway was made here?) and rising asset prices (houses and shares). Now the tide has turned, unless we're prepared to return quickly to our former reckless borrowing.

A third observation, is that the worst monetary inflation in the last 25 years occurred not under spendthrift Socialist governments, but supposedly prudent Conservative ones (this also holds true for the United States). I wrote a letter to the Spectator magazine to point this out, but they didn't find space for it (perhaps a factor in that decision is that the "Lawson boom" was engineered by a former editor of the Spectator, though the graph above shows the expansion began much earlier than Lawson's 1986 budget; they did print this one, however, which warned of the crash in banking shares).

Another commentator whom I recently referenced, says that the recent US stockmarket recovery is mostly owing to intervention by institutional investors, who own 20% of the market, the implication being that they are trying to encourage the other 80% (the private investors) to join in and, presumably, be fleeced as the former cash-out.

Cycles

A recent study of national economies in the last 800 years (hat-tip to John Mauldin) by Reinhart and Rogoff strongly suggests (as common sense would also suggest) that when debts are very heavy, the economy tips over into recession as we try to repay loans and rebuild savings. Mauldin discounts fears of inflation, because if consumer demand should pick up, there are plenty of resources to meet it. Our problem at the moment is oversupply, which is reflected in the precarious state of airlines, cruise companies, car firms etc - the ad pages tell the story.

Pressure to invest vs. pressure to borrow money

There is pressure to invest, not least because as the populations of developed countries live longer, pension funds have to create more income for the retired. For example, Leo Kolivakis comments on calls for Japan's public pension fund to move money out of bonds and into shares, aiming for higher growth. The fund is worth some $1.4 trillion but only 20% of it is in stocks, about equally divided between Japanese and foreign.

However, according to this source, total world stockmarkets were worth about $46.5 trillion last month, so even if that Japanese fund switched a further 20% into shares, that would only be worth 0.6% of the value of global shares; and even in Japan there are counter-calls to stay safe with bonds. Also, the Japanese are a patriotic lot, and if more of their pension money were to switch into equities (shares) I would expect them to press for a bias in favour of Japanese companies. The effects could therefore be localised, which may be an interesting proposition for the bolder investor.

Even then, there is the question of currency movements. The yen has been held down on the foreign currency exchanges, in an attempt to keep Japanese exports competitively priced, but if Western countries (with all their economic problems) devalue their currencies faster than the yen, it will hit shares in export-oriented Japanese companies. And the managers of Japan's public pension fund must be worrying about this possibility.

Meanwhile, in the USA there has been talk of forcing pension investors out of shares and into annuities, partly (many suspect) because this would create extra demand for Treasury bonds, at a time when the US Government is running out of willing buyers for its debt.

As you can see, there are contrary currents in the oceans of finance.

Will the stimulus money work?

The vast sums loaned to banks have not flowed out into the economy as hoped. Partly it's because banks are still trying to rebuild their reserves (because they loaned far too much during the boom), and partly (I think) because they know that only about half of their losses have been publicly exposed. When the full story is known and its effects felt, there will be more businesses going to the wall. So banks are going to be very careful about who they lend to, and how much; and will charge as much as they can in order to carry on mending their own deficits.

Meanwhile, there's fudging going on. As the Washington Post reported last August, accounting rules had changed in the Spring so that "Under the new rules, banks are not required to set aside money against the portion of a loss judged to be temporary." This appeared to offer a way out of having to show all one's "toxic assets" - all you had to do was maintain (in some plausible way) that valuations would eventually increase again. The catch with a subsequent proposal reported by that Post article, is that long-term loans would have to be fairly valued, i.e. stated as worth what someone else would now pay to take them over. As you may imagine, this has led to much argument and lobbying.

Journalist and investor Charles Hugh Smith thinks we have now got to the end of the line, and the game will play out as follows: a market correction to 6,500 or lower on the Dow Jones Index; a rally up to September; then a fresh, much sharper decline after the November elections "to depths few foresee".

How low could the market go?

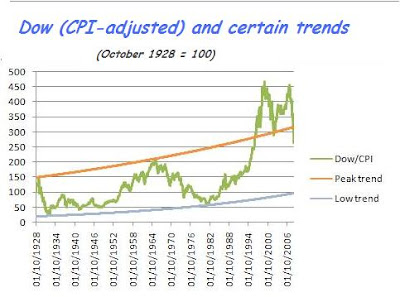

Who knows? This is the point at which people start to look for patterns - in the investment world they're known as "Chartists". Back in December 2008, I looked at the progress of the Dow Jones Index since the heady days before the Wall Street Crash of 1929, and adjusted the figures for inflation as measured by the Consumer Prices Index (CPI). Here's the result:

I think it does show the effect of all the above-GDP-growth-rate monetary stimulus that started in the early 1980s. I think monetary inflation explains why the peaks of end-1999 and 2007 were so extraordinarily high; and I fear that it may lead to a correspondingly extraordinary low.

I think it does show the effect of all the above-GDP-growth-rate monetary stimulus that started in the early 1980s. I think monetary inflation explains why the peaks of end-1999 and 2007 were so extraordinarily high; and I fear that it may lead to a correspondingly extraordinary low.

It is a result against which the political and financial establishment will struggle mightily, because it spells disaster for many of them and most of us.

But my cash isn't earning anything!

Oh yes, it is. It may not be earning much interest, but it could be increasing in value, in a way that is particularly useful if you're a taxpayer.

Let's say you've sold an asset for £100,000, and all such assets then drop in price by 20%. You could, if you judge the price to have hit bottom, repurchase for £80,000 (let's ignore dealing costs, please!). Effectively, you've gained £20,000. Had that £80k asset given you income of £20k, that's a 25% return. A 40% taxpayer would be charged £8k, leaving a net return of £12k, or 15%.

But making a "gain" through asset devaluation doesn't get taxed as income, so you enjoy the full 25% tax-free! The government hasn't yet got round to confiscating capital, so enjoy. (That is, until inflation lets rip, in which case you'll probably want to buy things to get rid of your cash.)

Deflation or inflation?

That's the key question, and no-one has the certain answer, and certainly not as to timing. My personal view is that after ups and downs, we will see that we are in a deflationary period, but there is a danger that governments will somehow find a way to expand the monetary base to devalue their (and our) debts. It takes a while for inflation to work its way through the system, so I suppose the danger can be partially averted by keeping a weather eye out for signs of inflation, and then acting accordingly. I don't see inflation as imminent.

Don't blame me!

I'm trying to help you - and clarify my own thoughts - with what I've read and learned. But no-one has that crystal ball - of some 20,000 professional economists, only some 12 foretold the Credit Crunch! - and this is not personal advice to you. The best it can do, is stimulate and inform your own thinking, research and decisions. So, please note my disclaimer, reproduced below and elsewhere.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Reportedly, Swiss-born and Thai-resident investment guru Marc Faber has recently repeated his view that the US cannot escape crisis (e.g. in pension funding) and will be forced to increase the money supply, so further weakening the dollar, at which point, he says, it will become necessary to invest in equities in order to mitigate the effects of inflation. But not yet...

"In that situation you are better off in equities. I am not saying that you should buy equities today. But the dollar will go down, they will have to print a lot of money."

Meanwhile, a sober Australian blogger-commentator opines that the UK may face a currency crisis within the next 3 - 5 years, followed by Japan and the USA (though Portugal, Ireland, Italy and Greece may have their crises before all these three).

UPDATE

Since writing this article today, I have read Steve Keen's discussion of the causes of the Great Depression and how our situation now is worse than it was then. Professor Keen, one of the very few to predict the credit crunch, says:

"...since debt today is so much larger (relative to GDP) than it was at the start of the Great Depression, the dangers are either that the fall in demand could be steeper, or that the decline could be much more drawn out than in the 1930s."

____________________________________________________

An industry expert writes

Howard Marks, chairman of a large investment firm, publishes his quarterly report to investors (hat-tip to Michael Panzner).

Panzner picks out a couple of points - the stock market rally is not based on improvement in economic fundamentals, and commercial real estate looks to be a difficult area for some time yet - but Marks concludes, I think a little tentatively, that "most assets are valued about fairly today". This conclusion dovetails with Marks' business, which is sifting and selecting stocks that his company judges are good buys.

Market manipulation?

Like Panzner, however, I tend to be more bearish - I am part of that "wall of worry" that the American investment establishment is desperate for us all to climb up, or over. It seems to me that, as others have said before, nothing that led to the present crisis has yet been fixed. Some days ago, I looked at the relationship between bank lending and Gross Domestic Product (GDP) in the UK, and I reproduce below a graph I made to represent year-on-year percentage changes in both:

Two things stand out: firstly, the banks consistently increase the money supply more than the growth of GDP, which a monetarist would say is inflationary. Secondly, the general trend since the mid-1970s appears to be a slowing of economic growth, despite all the monetary stimulus. Instead, the extra cash (aka "liquidity") went into a combination of spending on imports (how much of the stuff in your house and on your driveway was made here?) and rising asset prices (houses and shares). Now the tide has turned, unless we're prepared to return quickly to our former reckless borrowing.

Two things stand out: firstly, the banks consistently increase the money supply more than the growth of GDP, which a monetarist would say is inflationary. Secondly, the general trend since the mid-1970s appears to be a slowing of economic growth, despite all the monetary stimulus. Instead, the extra cash (aka "liquidity") went into a combination of spending on imports (how much of the stuff in your house and on your driveway was made here?) and rising asset prices (houses and shares). Now the tide has turned, unless we're prepared to return quickly to our former reckless borrowing.A third observation, is that the worst monetary inflation in the last 25 years occurred not under spendthrift Socialist governments, but supposedly prudent Conservative ones (this also holds true for the United States). I wrote a letter to the Spectator magazine to point this out, but they didn't find space for it (perhaps a factor in that decision is that the "Lawson boom" was engineered by a former editor of the Spectator, though the graph above shows the expansion began much earlier than Lawson's 1986 budget; they did print this one, however, which warned of the crash in banking shares).

Another commentator whom I recently referenced, says that the recent US stockmarket recovery is mostly owing to intervention by institutional investors, who own 20% of the market, the implication being that they are trying to encourage the other 80% (the private investors) to join in and, presumably, be fleeced as the former cash-out.

Cycles

A recent study of national economies in the last 800 years (hat-tip to John Mauldin) by Reinhart and Rogoff strongly suggests (as common sense would also suggest) that when debts are very heavy, the economy tips over into recession as we try to repay loans and rebuild savings. Mauldin discounts fears of inflation, because if consumer demand should pick up, there are plenty of resources to meet it. Our problem at the moment is oversupply, which is reflected in the precarious state of airlines, cruise companies, car firms etc - the ad pages tell the story.

Pressure to invest vs. pressure to borrow money

There is pressure to invest, not least because as the populations of developed countries live longer, pension funds have to create more income for the retired. For example, Leo Kolivakis comments on calls for Japan's public pension fund to move money out of bonds and into shares, aiming for higher growth. The fund is worth some $1.4 trillion but only 20% of it is in stocks, about equally divided between Japanese and foreign.

However, according to this source, total world stockmarkets were worth about $46.5 trillion last month, so even if that Japanese fund switched a further 20% into shares, that would only be worth 0.6% of the value of global shares; and even in Japan there are counter-calls to stay safe with bonds. Also, the Japanese are a patriotic lot, and if more of their pension money were to switch into equities (shares) I would expect them to press for a bias in favour of Japanese companies. The effects could therefore be localised, which may be an interesting proposition for the bolder investor.

Even then, there is the question of currency movements. The yen has been held down on the foreign currency exchanges, in an attempt to keep Japanese exports competitively priced, but if Western countries (with all their economic problems) devalue their currencies faster than the yen, it will hit shares in export-oriented Japanese companies. And the managers of Japan's public pension fund must be worrying about this possibility.

Meanwhile, in the USA there has been talk of forcing pension investors out of shares and into annuities, partly (many suspect) because this would create extra demand for Treasury bonds, at a time when the US Government is running out of willing buyers for its debt.

As you can see, there are contrary currents in the oceans of finance.

Will the stimulus money work?

The vast sums loaned to banks have not flowed out into the economy as hoped. Partly it's because banks are still trying to rebuild their reserves (because they loaned far too much during the boom), and partly (I think) because they know that only about half of their losses have been publicly exposed. When the full story is known and its effects felt, there will be more businesses going to the wall. So banks are going to be very careful about who they lend to, and how much; and will charge as much as they can in order to carry on mending their own deficits.

Meanwhile, there's fudging going on. As the Washington Post reported last August, accounting rules had changed in the Spring so that "Under the new rules, banks are not required to set aside money against the portion of a loss judged to be temporary." This appeared to offer a way out of having to show all one's "toxic assets" - all you had to do was maintain (in some plausible way) that valuations would eventually increase again. The catch with a subsequent proposal reported by that Post article, is that long-term loans would have to be fairly valued, i.e. stated as worth what someone else would now pay to take them over. As you may imagine, this has led to much argument and lobbying.

Journalist and investor Charles Hugh Smith thinks we have now got to the end of the line, and the game will play out as follows: a market correction to 6,500 or lower on the Dow Jones Index; a rally up to September; then a fresh, much sharper decline after the November elections "to depths few foresee".

How low could the market go?

Who knows? This is the point at which people start to look for patterns - in the investment world they're known as "Chartists". Back in December 2008, I looked at the progress of the Dow Jones Index since the heady days before the Wall Street Crash of 1929, and adjusted the figures for inflation as measured by the Consumer Prices Index (CPI). Here's the result:

I think it does show the effect of all the above-GDP-growth-rate monetary stimulus that started in the early 1980s. I think monetary inflation explains why the peaks of end-1999 and 2007 were so extraordinarily high; and I fear that it may lead to a correspondingly extraordinary low.It is a result against which the political and financial establishment will struggle mightily, because it spells disaster for many of them and most of us.

But my cash isn't earning anything!

Oh yes, it is. It may not be earning much interest, but it could be increasing in value, in a way that is particularly useful if you're a taxpayer.

Let's say you've sold an asset for £100,000, and all such assets then drop in price by 20%. You could, if you judge the price to have hit bottom, repurchase for £80,000 (let's ignore dealing costs, please!). Effectively, you've gained £20,000. Had that £80k asset given you income of £20k, that's a 25% return. A 40% taxpayer would be charged £8k, leaving a net return of £12k, or 15%.

But making a "gain" through asset devaluation doesn't get taxed as income, so you enjoy the full 25% tax-free! The government hasn't yet got round to confiscating capital, so enjoy. (That is, until inflation lets rip, in which case you'll probably want to buy things to get rid of your cash.)

Deflation or inflation?

That's the key question, and no-one has the certain answer, and certainly not as to timing. My personal view is that after ups and downs, we will see that we are in a deflationary period, but there is a danger that governments will somehow find a way to expand the monetary base to devalue their (and our) debts. It takes a while for inflation to work its way through the system, so I suppose the danger can be partially averted by keeping a weather eye out for signs of inflation, and then acting accordingly. I don't see inflation as imminent.

Don't blame me!

I'm trying to help you - and clarify my own thoughts - with what I've read and learned. But no-one has that crystal ball - of some 20,000 professional economists, only some 12 foretold the Credit Crunch! - and this is not personal advice to you. The best it can do, is stimulate and inform your own thinking, research and decisions. So, please note my disclaimer, reproduced below and elsewhere.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

GIGO

The light may be dawning for some of our leaders.

In the recent Congressional hearings with the financial industry, it became quite clear that their evangelical belief in the unregulated free market had blinded them to the simple fact that money is only a medium of exchange, and that wealth cannot be created by the push of a button.

These wizards have cousins in industry, the pointy-haired boss of the Dilbert cartoons, who have been trained by Management specialists to believe that process matters more than productivity, and meetings more than manufacturing.

Their relatives in Education are just as deluded and dangerous. Since it became a university discipline, Education graduates have taken most of the administrative jobs in universities and schools and related ones in government. As each new Education 'paradigm' is introduced, we in the US and UK fall farther behind the Far East, where they teach the 'old way'.

My opinion is that every one of these ideas is doomed to failure, since they rely on two false assumptions:

1. We can magically train our mediocre students to become the teachers of the best and brightest.

2. The 'secret' to improving results is to change the way that teachers do their jobs, rather than changing the way that students behave.

In the recent Congressional hearings with the financial industry, it became quite clear that their evangelical belief in the unregulated free market had blinded them to the simple fact that money is only a medium of exchange, and that wealth cannot be created by the push of a button.

These wizards have cousins in industry, the pointy-haired boss of the Dilbert cartoons, who have been trained by Management specialists to believe that process matters more than productivity, and meetings more than manufacturing.

Their relatives in Education are just as deluded and dangerous. Since it became a university discipline, Education graduates have taken most of the administrative jobs in universities and schools and related ones in government. As each new Education 'paradigm' is introduced, we in the US and UK fall farther behind the Far East, where they teach the 'old way'.

My opinion is that every one of these ideas is doomed to failure, since they rely on two false assumptions:

1. We can magically train our mediocre students to become the teachers of the best and brightest.

2. The 'secret' to improving results is to change the way that teachers do their jobs, rather than changing the way that students behave.

Saturday, January 23, 2010

Still on for deflation

This article, and others that it refers to, takes the view that the currently very high debt-to-GDP ratio, plus plenty of unused or under-used resources, indicate deflation rather than inflation. Cash (or long term US government debt) is king, for these American writers.

As I understand it, the British economy suffers even worse debt problems and also has excess productive capacity, so much the same argument would seem to apply here, too.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

As I understand it, the British economy suffers even worse debt problems and also has excess productive capacity, so much the same argument would seem to apply here, too.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Tuesday, January 19, 2010

Kraft, Cadbury's and the mystery of M&A

Company A buys Company B, using bank borrowing to finance almost 50% of the purchase, which loan it will repay by stripping Company B. Loss of jobs, skills, quite possibly alteration to product quality at some point, quite possibly lower overall profitability for the conglomerate as a result of the takeover (this is, I believe, quite common).

Cui bono? Should there be a rule against financing takeovers with bankster cash?

Cui bono? Should there be a rule against financing takeovers with bankster cash?

Sunday, January 17, 2010

A straw in the guano; "When Giants Fall" by Michael Panzner

After his prescient book "Financial Armageddon", in which Michael Panzner identified four major threats to our economic security, he wrote another called "When Giants Fall", which I have been planning to review for a year now.

The latter is more complex and harder to summarise, but as I see it, essentially it views America's loss of power and prestige as leading to a sort of Balkanization of the world, just as after the death of Tito, Yugoslavia and other Eastern European countries fractured and fought. I once visited a pet shop where there was a large rabbit sitting among the guinea pigs; when I asked why, they told me that guinea pigs will fight to the death for dominance, but one look at the rabbit told them they had no chance and so they decided to get along peaceably.

This global fracture is now under way, with major nations like China and Russia playing a 21st century version of The Great Game, and we see it in little ways as well as the more obvious ones. Mark Steyn, a sharply witty Canadian journalist, comments on the curious case of a South Pacific islet (Nauru) taking it on itself to recognise the nationhood of Abkhazia, currently a province of the Caucasian republic of Georgia (Stalin's birthplace). Naturally, it's for a consideration, in this case money from President Putin, who wants to reabsorb Georgia.

Should we take it seriously? Aren't both these little nations a bit like the Duchy of Grand Fenwick in the film comedy "The Mouse That Roared"?

A single match can start a forest fire. When some Serbs decided to break off from Croatia in the 1990s, they may have started as a rather small, contemptibly scruffy and ill-equipped band, but other players and suppliers got involved and things fell apart very nastily. When there are powerful interests at stake, nothing is insignificant: Russia quibbles about the definition of its continental shelf to lay claim (in 2001) to fossil fuels near the North Pole; China goes back to the 13th century to justify its claim to Tibet, and by extension the (currently) Indian province of Arunachal Pradesh - both containing valuable natural resources that the Chinese need. Relatively small amounts of money and support can recruit votes that matter in international politics and law.

Panzner's book examines all sorts of potential consequences of the weakening of the "world's policeman", and no-one knows how matters will progress. The situation is so complex that chaos theory could be relevant - the flutter of the butterfly's wings triggering a hurricane thousands of miles away.

So what can we do about it? I think all we can do, is to become generally more cautious and store resources to cope with emergencies. Like Boy Scouts, we must "be prepared"; as our grandparents would say, "don't put all your eggs in one basket".

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

The latter is more complex and harder to summarise, but as I see it, essentially it views America's loss of power and prestige as leading to a sort of Balkanization of the world, just as after the death of Tito, Yugoslavia and other Eastern European countries fractured and fought. I once visited a pet shop where there was a large rabbit sitting among the guinea pigs; when I asked why, they told me that guinea pigs will fight to the death for dominance, but one look at the rabbit told them they had no chance and so they decided to get along peaceably.

This global fracture is now under way, with major nations like China and Russia playing a 21st century version of The Great Game, and we see it in little ways as well as the more obvious ones. Mark Steyn, a sharply witty Canadian journalist, comments on the curious case of a South Pacific islet (Nauru) taking it on itself to recognise the nationhood of Abkhazia, currently a province of the Caucasian republic of Georgia (Stalin's birthplace). Naturally, it's for a consideration, in this case money from President Putin, who wants to reabsorb Georgia.

Should we take it seriously? Aren't both these little nations a bit like the Duchy of Grand Fenwick in the film comedy "The Mouse That Roared"?

A single match can start a forest fire. When some Serbs decided to break off from Croatia in the 1990s, they may have started as a rather small, contemptibly scruffy and ill-equipped band, but other players and suppliers got involved and things fell apart very nastily. When there are powerful interests at stake, nothing is insignificant: Russia quibbles about the definition of its continental shelf to lay claim (in 2001) to fossil fuels near the North Pole; China goes back to the 13th century to justify its claim to Tibet, and by extension the (currently) Indian province of Arunachal Pradesh - both containing valuable natural resources that the Chinese need. Relatively small amounts of money and support can recruit votes that matter in international politics and law.

Panzner's book examines all sorts of potential consequences of the weakening of the "world's policeman", and no-one knows how matters will progress. The situation is so complex that chaos theory could be relevant - the flutter of the butterfly's wings triggering a hurricane thousands of miles away.

So what can we do about it? I think all we can do, is to become generally more cautious and store resources to cope with emergencies. Like Boy Scouts, we must "be prepared"; as our grandparents would say, "don't put all your eggs in one basket".

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, January 16, 2010

Mrs Thatcher and inflation: a letter to the Spectator

Sir;

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Wednesday, January 13, 2010

Debt, the financial sector and economic growth

Someone who occasionally reads and comments on my older blog has a formulation of real growth: increase in GDP less increase in debt. I've finally taken the bait and invested time to look at this, for the UK, and it's intriguing.

First, I've taken figures for M4 bank lending, from the Bank of England's website. This gives the quarterly increase as a percentage, re-expressed as an annual equivalent figure. I've used Excel to average the four quarters for each calendar year. Since the information is only available from partway through 1963, I use the estimated annual percentage increase from 1964 onwards.

For GDP, I use the Measuring Worth site and the "UK nominal GDP" figures (i.e. x million pounds, not adjusted for inflation), and again give the percentage increase year-on-year (the last available year here is 2008).

Here's the resulting graph for increases in M4 and GDP (click on graph to enlarge):

What is obvious is that apart from a short time in the early 1990s, lending has risen far more than GDP for the last 30 years. That extra money went somewhere, and it seems that all it did was inflate asset prices, in the stockmarket and in housing, at the same time that global trade has kept down wages and consumer prices.

Between 1964 and 1981, GDP increased by an average 12.69% and M4 by 15.16% - a difference of 2.48% per year. But from 1982 to 2008, GDP increased annually on average by 6.63% and M4 by 12.32% - a difference of 5.69% p.a. Compounded up over the past quarter century, that extra difference may explain how financiers have become so large and powerful. In the USA, according to Robert Creamer , the financial sector accounted for 8% of national GDP over the last 10 years, but made 41% of the profits.

I can't say when it will end, but equally I can't see this going on forever. This is why I am inclined to listen to the Jeremiahs who warn us of further economic setbacks, despite strong recent rises in the stockmarkets.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

First, I've taken figures for M4 bank lending, from the Bank of England's website. This gives the quarterly increase as a percentage, re-expressed as an annual equivalent figure. I've used Excel to average the four quarters for each calendar year. Since the information is only available from partway through 1963, I use the estimated annual percentage increase from 1964 onwards.

For GDP, I use the Measuring Worth site and the "UK nominal GDP" figures (i.e. x million pounds, not adjusted for inflation), and again give the percentage increase year-on-year (the last available year here is 2008).

Here's the resulting graph for increases in M4 and GDP (click on graph to enlarge):

What is obvious is that apart from a short time in the early 1990s, lending has risen far more than GDP for the last 30 years. That extra money went somewhere, and it seems that all it did was inflate asset prices, in the stockmarket and in housing, at the same time that global trade has kept down wages and consumer prices.Between 1964 and 1981, GDP increased by an average 12.69% and M4 by 15.16% - a difference of 2.48% per year. But from 1982 to 2008, GDP increased annually on average by 6.63% and M4 by 12.32% - a difference of 5.69% p.a. Compounded up over the past quarter century, that extra difference may explain how financiers have become so large and powerful. In the USA, according to Robert Creamer , the financial sector accounted for 8% of national GDP over the last 10 years, but made 41% of the profits.

I can't say when it will end, but equally I can't see this going on forever. This is why I am inclined to listen to the Jeremiahs who warn us of further economic setbacks, despite strong recent rises in the stockmarkets.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Tuesday, January 12, 2010

Interactive long-term house price graphs

Via Australian economist Steve Keen, here is a tool from The Economist magazine to help you see how house prices have changed over time. This may help you guess whether current prices are too high, too low or Goldilocks!

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Preparing for the worst is not for loners

Charles Hugh Smith offers some sensible general principles for making it through what he sees as likely very difficult, disrupted times ahead. Key recommendations include broadening your skills, and developing social networks. I think he's right - Robinson Crusoe is not the model for how to survive in our populous countries.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

More warning signs

Update: see "Jesse" on speculation about recent curious purchases of US Treasury bonds.

__________________________________________

"Mish" looks at two countries experiencing trouble - Argentina and Venezuela - and point out that European banks are exposed to risk in that area.

"George Washington" thinks the recent rise in the stockmarket has been because of activity by "hedgies, pension funds, banks and other institutional investors", including possibly even clandestine intervention by the government itself (I've seen this allegation before). However, in the US 80% of stocks are owned by individuals, not these corporate entities, so the suspicion is that the rally has been engineered to encourage the private investor to return to the market.

It doesn't seem to be working - much of the money withdrawn from stocks has gone into bonds (I think the unfortunate private investor may lose again if - as I fear - interest rates rise and bond values plummet).

I also suspect that if the individual re-entered the market because of what appears to be leveraged (boosted with borrowed money) speculation by the institutions, the latter would then cash-in and leave the individual holding the baby. This pattern is known as a "sucker rally".

But if the private investor is not "suckered" back into the market, then institutions will race to get out again (suckering each other, faute de mieux) and we could see a sharp fall in stocks. This, I assume would confirm the private investor's worst suspicions and lead him/her to pull even more out of the market.

Some, including myself, have suggested that the real bottom (at some point, goodness knows when) in the stockmarket may be somewhere around 4,000 on the Dow and 2,000 on the FTSE (adjusted for inflation, if that takes off). It may never happen, but Google "Dow 4000" and see some quite respectable commentators bandying around that idea.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

__________________________________________

"Mish" looks at two countries experiencing trouble - Argentina and Venezuela - and point out that European banks are exposed to risk in that area.

"George Washington" thinks the recent rise in the stockmarket has been because of activity by "hedgies, pension funds, banks and other institutional investors", including possibly even clandestine intervention by the government itself (I've seen this allegation before). However, in the US 80% of stocks are owned by individuals, not these corporate entities, so the suspicion is that the rally has been engineered to encourage the private investor to return to the market.

It doesn't seem to be working - much of the money withdrawn from stocks has gone into bonds (I think the unfortunate private investor may lose again if - as I fear - interest rates rise and bond values plummet).

I also suspect that if the individual re-entered the market because of what appears to be leveraged (boosted with borrowed money) speculation by the institutions, the latter would then cash-in and leave the individual holding the baby. This pattern is known as a "sucker rally".

But if the private investor is not "suckered" back into the market, then institutions will race to get out again (suckering each other, faute de mieux) and we could see a sharp fall in stocks. This, I assume would confirm the private investor's worst suspicions and lead him/her to pull even more out of the market.

Some, including myself, have suggested that the real bottom (at some point, goodness knows when) in the stockmarket may be somewhere around 4,000 on the Dow and 2,000 on the FTSE (adjusted for inflation, if that takes off). It may never happen, but Google "Dow 4000" and see some quite respectable commentators bandying around that idea.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Measure your pessimism

Hat-tip to Credit Writedowns. I'm relieved to see that I'm still at the Teddy/Cub stage!

Hat-tip to Credit Writedowns. I'm relieved to see that I'm still at the Teddy/Cub stage! DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Human Nature?

Today, I started my 27th year of teaching at a State-supported US university. Compared with 1984, we have the same number of students, fewer full-time teaching faculty, and twice as many administrators. In the past 8 years alone, the non-academic budget has grown from 44% to 60% of the budget.

This week, we start discussions on increasing teaching loads (which will, of course, require more administrators to 'organize' things).

I see this trend in business, government, medicine and the military. Is it just the human condition that the non-productive take over everything?

I recall that, when the Mongols took over a city, they killed the bureaucrats, and took the scholars home with them. The Allies did much the same in Germany in 1945.

Perhaps they had the right idea?

This week, we start discussions on increasing teaching loads (which will, of course, require more administrators to 'organize' things).

I see this trend in business, government, medicine and the military. Is it just the human condition that the non-productive take over everything?

I recall that, when the Mongols took over a city, they killed the bureaucrats, and took the scholars home with them. The Allies did much the same in Germany in 1945.

Perhaps they had the right idea?

Monday, January 11, 2010

Climate change and industrial activity

Could the current cold weather be partly related to a downturn in fossil-fuel-powered manufacturing and transportation? I only ask because I seem to recall reading/hearing that big freezes also happened in the 70s, and after both World wars.

Why a turnaround in the economy is not imminent

"Mish" collates a number of emails and comments to reinforce his thesis that we are set for a long and very difficult deflation, for a variety of reasons. One of his respondents is noted Australian economist Steve Keen, one of the dozen or so (out of perhaps 20,000 professional economists worldwide) who foresaw the credit crunch; Keen thinks it would have been better to give money to debtors directly, rather than to the banks, who will simply hoard the cash as so few now wish to borrow the way they used to.

Vitaliy Katsenelson looks at history and finds: "Over the last 200 years, every long-lasting bull market (and we just had a supersized one from 1982 to 2000) was followed by a range-bound market that lasted about 15 years or so (the only exception was the Great Depression)." He expects the market to bounce up and down and "At the end of this wild ride, when the excitement subsides and the dust settles, index investors and buy-and-hold stock collectors will find themselves not far from where they started in 2000," so he recommends that we analyze individual companies and timing our purchases according to when we think their particular stocks are undervalued.

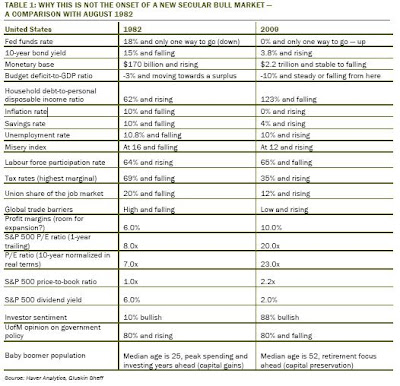

David Rosenberg tabulates lots of ways in which the present circumstances are not like those in 1982 (when the market began to turn upwards in real terms):

By the way, that last statistic about median ages startled me, so I looked elsewhere for information on general US demographics, rather than just the "baby boomers". This graph says that the median age of the US population as a whole rose from 26 years in 1929 to nearly 30 post WWII, then fell to below 28 in the late 1960s, after which there was a steady rise to over 34 years by 1994. This site estimates the median age in 2006/2008 at 36.7 years. Demographic change has had and is going to have an enormous impact on government budgets and the stockmarket.

Bill Gross (of PIMCO, which recently announced its plan to be a net seller of UK bonds) laments the corruption of government that makes him wary of trading in the US at present. He thinks that relative to more fiscally responsible governments like Germany, countries like the USA, UK and Japan will have higher interest rates and this will, of course, hit the value of their bonds and stocks.

Finally, Warren Pollock's politico-economic overview sees threats to two key stabilisers in the world economy - Saudi Arabia and China. Problems there could begin a wider unravelling of current arrangements.

So, as I have done for the last 10 years or more, I am urging caution and the making of emergency plans.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Vitaliy Katsenelson looks at history and finds: "Over the last 200 years, every long-lasting bull market (and we just had a supersized one from 1982 to 2000) was followed by a range-bound market that lasted about 15 years or so (the only exception was the Great Depression)." He expects the market to bounce up and down and "At the end of this wild ride, when the excitement subsides and the dust settles, index investors and buy-and-hold stock collectors will find themselves not far from where they started in 2000," so he recommends that we analyze individual companies and timing our purchases according to when we think their particular stocks are undervalued.

David Rosenberg tabulates lots of ways in which the present circumstances are not like those in 1982 (when the market began to turn upwards in real terms):

By the way, that last statistic about median ages startled me, so I looked elsewhere for information on general US demographics, rather than just the "baby boomers". This graph says that the median age of the US population as a whole rose from 26 years in 1929 to nearly 30 post WWII, then fell to below 28 in the late 1960s, after which there was a steady rise to over 34 years by 1994. This site estimates the median age in 2006/2008 at 36.7 years. Demographic change has had and is going to have an enormous impact on government budgets and the stockmarket.

Bill Gross (of PIMCO, which recently announced its plan to be a net seller of UK bonds) laments the corruption of government that makes him wary of trading in the US at present. He thinks that relative to more fiscally responsible governments like Germany, countries like the USA, UK and Japan will have higher interest rates and this will, of course, hit the value of their bonds and stocks.

Finally, Warren Pollock's politico-economic overview sees threats to two key stabilisers in the world economy - Saudi Arabia and China. Problems there could begin a wider unravelling of current arrangements.

So, as I have done for the last 10 years or more, I am urging caution and the making of emergency plans.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sunday, January 10, 2010

NEST - compulsory pension savings for employees

In the UK, many people face an impoverished retirement. Stakeholder Pensions were introduced in 2001 as a simple and cheap form of retirement saving, but even now, nearly 12 million people have no pension plan, or a very small one. There are reasons for this - including being too poor to invest enough to make a worthwhile difference to one's retirement income.

From 2012, this will change. A compulsory scheme will be introduced in workplaces, for people that haven't already joined a scheme. It's been called by different names and has just been rebranded "NEST" - the National Employment Savings Trust. (The logo (see left) reportedly cost £363,000 to dream up - the equivalent of over 100 years' worth of maximum contributions to a NEST plan.)

There was an earlier, and in my view better, scheme mooted by one-man think tank the Rt Hon Frank Field MP, who set up the Pensions Reform Group in 1999 to address the issue. They came up with the idea of a Universal Protected Pension, which has 5 principles:

1. Together with the Basic State Pension, an extra (funded) pension should eventually lift all pensioners permanently above the poverty line, by providing a total minimum income of 25-30% of average earnings. Those who are able and willing, can pay in more to get more.

2. It should be for everybody.

3. It should operate as a redistributive scheme: everybody pays a proportion of their earnings (so higher earners pay more), but everybody will get the same benefits.

4. The layer on top of the Basic State Pension should be funded - i.e. it would become an enormous investment fund. Without this, the whole scheme would be another expensive unfunded Government undertaking and at risk of being cut or abolished when the national budget gets tight.

5. It should be kept independent of the Government, to keep the politicians' hands off it.

Like other ideas by Mr Field, this one has been well thought-out. And like some of his other ideas, it's been ignored, or badly adapted. Perhaps, in this case, it's because politicians understand the temptation of (4) too well to think that (5) would work.

Let's look at (1 - 3) as well. Without compulsion, many workers not only would not join, but might be foolish to join. This is because of the way the benefit system works. If you reach retirement with an income of less than a certain weekly amount, the State will top it up. So if you know that is going to happen, it's not worth saving up out of your earned income - you'll just get less by way of a free top-up, so it's as though your personal provision was being taxed at 100%.

To answer this objection, the State first discounts each pound of income you provided for yourself, then re-awards you a "Savings Credit" of 60p. But this is still, effectively, a "tax rate" of 40% - Higher Rate Tax for the poor. This explains Steve Bee's comment on NEST:

Now all we need is for the government guys to fix things so that the pension savings of low to moderate earners can’t be devalued by the unfortunate way pension savings currently interact with the means-tested entitlements that are provided for the elderly and we’ll be cooking on gas.

Not surprisingly, financial advisers find themselves in a quandary when advising lower-paid people about funding for retirement!

Under Frank Field's group's proposals, there would be no decision to make, since contributions would be compulsory. But also, however little you contributed, you would still attain the overall target income of 25-30% of average earnings and be above the notional poverty line, so the complicated and self-defeating system of Pension Credit and Savings Credit would be redundant.

Instead, the NEST is universal only for those who aren't already in a scheme, and you only get the results of what you and your employer have put in - no redistribution effect. Presumably the employer will take into account what he/she has to contribute to the pension, when calculating what pay rises to give you, so it's not even "free money" from the employer. In effect, we have a variant on the current unsatisfactory system, plus compulsion.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, January 09, 2010

Simon Johnson on the coming disaster

Simon Johnson comments on renewed speculative activity by the banks. He fears that the next bubble-and-pop may be in emerging markets, especially China.

For those who wish to understand more, Simon's website, The Baseline Scenario, offers a beginner's guide to the global financial crisis (GFC).

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

For those who wish to understand more, Simon's website, The Baseline Scenario, offers a beginner's guide to the global financial crisis (GFC).

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Which books should we burn?

Welsh pensioners are buying books as fuel. Discounting differences in book size, and assuming you could gather all copies of the same title, which books would you burn?

On his deathbed, the poet Virgil requested his friends to burn his "Aeneid". Does an author have the right to do this?

On his deathbed, the poet Virgil requested his friends to burn his "Aeneid". Does an author have the right to do this?

GDP: friend or foe?

I attended the British Association for the Advancement of Science Conference in Birmingham in 1977, and even then economists were asking whether GDP was a useful measure. The example I remember was eating more sweets and consequently visiting the dentist more often.

Should we be quite so concerned about goosing GDP with quantitative easing etc, or is it just a trap to make us continue misallocating resources?

Should we be quite so concerned about goosing GDP with quantitative easing etc, or is it just a trap to make us continue misallocating resources?

Marmite Easter Egg

According to a team of astronomers, the Milky Way is surrounded by a shell of invisible "dark matter" (Htp: Yves Smith).

But the supermassive black hole at the centre of our galaxy is gpoing to take longer to shloop us up than we thought previously.

We have a bit more time to eat that strawberry.

But the supermassive black hole at the centre of our galaxy is gpoing to take longer to shloop us up than we thought previously.

We have a bit more time to eat that strawberry.

Wednesday, January 06, 2010

Propaganda time

There's a passage in Evelyn Waugh's comic novel Scoop where gentleman nature columnist William Boot, sent on foreign assignment owing to an administrative mix-up, receives instructions from his newspaper's owner:

LORD COPPER PERSONALLY REQUIRES VICTORIES STOP ON RECEIPT OF THIS CABLE VICTORY STOP CONTINUE CABLING VICTORIES UNTIL FURTHER NOTICE STOP

I was reminded of this today when I heard (via Classic FM) the cheery news that Marks & Spencer has enjoyed an increase in like-for-like sales over the last three-month period. As far as I know, "like-for-like" just means sales turnover in monetary terms, and it's perfectly possible to achieve this if you offer deep discounts, which is what they were doing before Christmas ("3 for 2" on clothes and Christmas gifts, for example). It keeps the show on the road, but it's bound to affect profits - though you may be able to disguise that impact if you mix it up with savings from property sales (27 stores) and redundancies (1,200).

Not that we got that contextualisation on the radio, of course. We are becoming skeptical news consumers, like Russians in the days when they said "v Pravde net izvestiy, v Izvestiyakh net pravdy" (In the Truth there is no news, and in the News there is no truth). It's a shame that we can't rely on mainstream news media, because when forced to the blogosphere to find out what's going on, we discover that not everyone who approaches you in a tatty coat tied together with rope is an Old Testament prophet.

But there's also plenty of stuff from more respectable sources, too. Michael Panzner ( who provides a great scan-and-select service for the economics newsfollower) directs us to this column by Morgan Stanley expert Stephen Roach. Brief highlights:

1. Only about half of an estimated $3.4 trillion in asset losses have been officially written off so far, according to the IMF.

2. The slowdown is worldwide, so other nations are unlikely to take up the slack.

3. The American consumer is not able or willing to resume spending as before.

4. 45% of China's economic activity is in "fixed investment" (building roads, factories etc) and there is a risk that they may be creating a lot of "white elephants".

Money is still changing hands here, but Roach says this is "fueled by a temporary boost from the inventory cycle", i.e. vendors are flogging-off surplus stock at bargain prices - which is why I've cited the feelgood M&S article above. After that, I think, comes cool reality - maybe continued lower prices, but also lower wages, lower profits, higher unemployment and an increase in bankruptcies.

Roach estimates a 40% chance of a "double dip" global recession this year. He also fears that economic stimulus will not be withdrawn quickly enough when a recovery comes, so possibly yet another bubble will be created. Another risk, in his view, is that the US will seek to protect domestic industry against Chinese imports; this could threaten the financial arrangements between the two countries, weaken the dollar and raise inflation.

Is it really not possible for radio and TV news to give a rounder picture of reality?

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

LORD COPPER PERSONALLY REQUIRES VICTORIES STOP ON RECEIPT OF THIS CABLE VICTORY STOP CONTINUE CABLING VICTORIES UNTIL FURTHER NOTICE STOP

I was reminded of this today when I heard (via Classic FM) the cheery news that Marks & Spencer has enjoyed an increase in like-for-like sales over the last three-month period. As far as I know, "like-for-like" just means sales turnover in monetary terms, and it's perfectly possible to achieve this if you offer deep discounts, which is what they were doing before Christmas ("3 for 2" on clothes and Christmas gifts, for example). It keeps the show on the road, but it's bound to affect profits - though you may be able to disguise that impact if you mix it up with savings from property sales (27 stores) and redundancies (1,200).

Not that we got that contextualisation on the radio, of course. We are becoming skeptical news consumers, like Russians in the days when they said "v Pravde net izvestiy, v Izvestiyakh net pravdy" (In the Truth there is no news, and in the News there is no truth). It's a shame that we can't rely on mainstream news media, because when forced to the blogosphere to find out what's going on, we discover that not everyone who approaches you in a tatty coat tied together with rope is an Old Testament prophet.

But there's also plenty of stuff from more respectable sources, too. Michael Panzner ( who provides a great scan-and-select service for the economics newsfollower) directs us to this column by Morgan Stanley expert Stephen Roach. Brief highlights:

1. Only about half of an estimated $3.4 trillion in asset losses have been officially written off so far, according to the IMF.

2. The slowdown is worldwide, so other nations are unlikely to take up the slack.

3. The American consumer is not able or willing to resume spending as before.

4. 45% of China's economic activity is in "fixed investment" (building roads, factories etc) and there is a risk that they may be creating a lot of "white elephants".

Money is still changing hands here, but Roach says this is "fueled by a temporary boost from the inventory cycle", i.e. vendors are flogging-off surplus stock at bargain prices - which is why I've cited the feelgood M&S article above. After that, I think, comes cool reality - maybe continued lower prices, but also lower wages, lower profits, higher unemployment and an increase in bankruptcies.

Roach estimates a 40% chance of a "double dip" global recession this year. He also fears that economic stimulus will not be withdrawn quickly enough when a recovery comes, so possibly yet another bubble will be created. Another risk, in his view, is that the US will seek to protect domestic industry against Chinese imports; this could threaten the financial arrangements between the two countries, weaken the dollar and raise inflation.

Is it really not possible for radio and TV news to give a rounder picture of reality?

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Tuesday, January 05, 2010

Money fund or mattress?

When I first started in financial services, Albany Life (now Canada Life) had a reassuringly-named "Guaranteed Money Fund"; some time ago, this was quietly rebranded "Money Fund" (see page 19 of this brochure).

It's a sign of the times. Money market funds are supposed to be rock-solid - only one ever failed to return 100 cents in the dollar between 1971 and late 2008. But when Lehman Brothers collapsed in September 2008, it caused losses to a large and venerable US money market fund called The Reserve Primary Fund, which owned some Lehman debt. Initially, the loss was not great - Lehman debt represented only 1% of Reserve Primary's total assets - but there was a one-hour window in which investors could get their cash out at 100 cents on the dollar. Naturally, big investment companies, watching their computer screens, were in the best position to know what was going on and act accordingly. So they jumped out of Reserve Primary, in such volume that the Lehman debt was now worth 3% of the remaining (much shrunken) assets.

For the safety-conscious, there is hardly anything more disturbing than discovering that something you trust in completely is not entirely reliable. So a panic started, with investors exiting money funds generally, until the United States government said it would guarantee such funds. At least, it would guarantee those funds that agreed to pay an insurance premium to the government; and only investments made on or before 19th September 2008.

Now the rules on money funds are to be reviewed and understandably, it raises deep suspicions. In this recent post, Tyler Durden looks at a proposal to suspend your right to realize your money market investment, in a time of exceptional turbulence. Of course, that is exactly the time that you would wish to get out, and given the experience of September 2008 it would not be surprising to find that the institutional investors had already moved out before the suspension came into force.

It is important, because according to Durden's article about a third of all mutual funds' (the US equivalent of the UK's unit trusts) assets are in money market funds, and according to this Wikipedia article one-third of all money market funds are held by private investors. So the fear is that Joe Public would be left holding the baby if there should be a run on money market funds.

I think the fear is overdone. The measures discussed by Durden (see the paragraphs re "Recommendation 3") are clearly intended to make mutual fund investment into the money market safer, and less exciting in terms of gains; those funds that try to achieve better returns with higher risk are to be clearly identified and segregated, with tighter regulation plus provisions for emergency backing from central bankers. And removing promises re withdrawal on demand lessens the chances of a panic, by moderating expectations - it's like those commercial property funds that warn the investor that there could be a delay of up to 6 months if he/she wants to cash out.

Besides, even 97 cents in the dollar is a good return, when stocks have, at some points, lost as much as 50% of their value (e.g. between the end of 1999 and the summer of 2003).

A wider issue is the preferential treatment given to one class of investor over another. If The Reserve Primary Fund had cut its realizable value to 99 cents on the dollar immediately and for everybody, it might have prevented the panic, which was at least partly due to not wishing to be the last one left holding the worthless asset.