Showing posts with label Dow. Show all posts

Showing posts with label Dow. Show all posts

Sunday, October 18, 2009

Sunday, September 20, 2009

The coming tide

Thanks to Tyrone for his comment directing us to a YouTube presentation by W E Pollock, someone I've viewed with interest before. The comment was in response to an FTAphaville piece that asked why the Dow was rising so strongly.

Pollock, whose presentations are useful to the layman because he is at pains to be clear and calm, notes that the volume of trade is low, which may mislead us as to the value of the market as a whole. It is as if, in a slow-moving housing market, your neighbour suddenly manages to sell his house for much more than expected, because the purchaser has certain private reasons to get in.

He also notes that the gains on the Dow are counteracted by the fall in the dollar's value, and this is a theme I've touched on many times. You have to look at real gains; and even when you think you're beating the present rate of inflation in your country, currency exchange movements may be the early indicators of higher future inflation. This is why, comparing where we are now to the period 1966 - 1982, I think we may yet see the real-terms equivalent of Dow 4,000 and FTSE 2,000.

Pollock goes on to consider gold, over which he puzzles (but then, there's a lot of dirty work and hugger-mugger in that market); and oil - if foreign economies begin to recover and industrial production rises, increasing the demand for oil, then if the dollar continues to be weak the price of energy in the USA will become so high as to damage growth prospects there.

So, where are we with all this?

Even academic economists are beginning (very belatedly) to question the validity of their models. Across the world, the games are so weighted and rigged, the rules so suddenly variable, that we are talking about how things ought to work, rather than how they really do. This is why it's now a fertile ground for conspiracy theorists: there really is a lot of conspiracy. Trouble is, we don't know all of the plots, all of the players, and all of the details.

What I think we can do, is look at the ocean tide, and not at the individual waves.

Historically, Western countries became wealthy on technological advances and were able to sell goods not just to each other, but to undeveloped countries in exchange for cheap resources. Then the latter countries began to industrialise, and goods could be carried at low unit cost in vast bulk across oceans and continents. All that remained was to break down political barriers to trade, as Nixon began to do with his visit to China in 1972.

Trouble is, controlling the rate of change. It's one thing to turn on your oil-fired central heating, another if your fuel storage tank catches fire. We want to carry on as we are (or as we used to be), but poor people are in a hurry to attain our wealthy lifestyles, and are disinclined to progress more slowly. Vast international businesses and globe-trotting billionaires stand to do very well out of facilitating this trade; national politicians are under pressure from their voters to resist it - but on a personal level, will know how rich they themselves will be when they leave office, so long as they don't try too hard for the people who elected them.

So, while I don't quite subscribe to the Dick-Dastardly-and-Mutley view of politician's summits (G-name-a-figure, Bilderberg, et al.), I can see the natural attraction for them of a world (or at least supranational) government. It means being further away from the Great Unwashed, mixing with all the Right People, fine wines and yachts etc; it means going with the flow, helping wealth and power to gather into certain centres, and organising dole handouts to regions that lose out as a result. Only the fools will try to play King Canute.

Imagine the world economies as a series of canal locks descending a steep hill. We are in the top section, the poor countries lower down. Now if all the gates are opened at once, there will be a destructive gush of water; the narrowboats in the top lock sink into the mud; the ones at the bottom float on a higher tide; a brave soul on a surfboard (the international trader) rides a thrilling wave down the hill.

Free-traders will argue that trade brings mutual benefits; but I don't think the argument works when world income disparities are so great. A Dutchman bought Manhattan from the occupying tribe for $24, but I doubt they'd get it back for that price now, not even with 400 years' interest.

It's coming, it's coming fast, it's coming destructively; and the people we pay to stop it are telling us the lies we want to hear and planning their personal advancement*. Let us return the favour.

* “It is a totally wrong notion of people to assume that the government does anything for the people; the government is there to do something for itself, and not for the people” – Marc Faber on GoldSeek, 12 September 2009

Pollock, whose presentations are useful to the layman because he is at pains to be clear and calm, notes that the volume of trade is low, which may mislead us as to the value of the market as a whole. It is as if, in a slow-moving housing market, your neighbour suddenly manages to sell his house for much more than expected, because the purchaser has certain private reasons to get in.

He also notes that the gains on the Dow are counteracted by the fall in the dollar's value, and this is a theme I've touched on many times. You have to look at real gains; and even when you think you're beating the present rate of inflation in your country, currency exchange movements may be the early indicators of higher future inflation. This is why, comparing where we are now to the period 1966 - 1982, I think we may yet see the real-terms equivalent of Dow 4,000 and FTSE 2,000.

Pollock goes on to consider gold, over which he puzzles (but then, there's a lot of dirty work and hugger-mugger in that market); and oil - if foreign economies begin to recover and industrial production rises, increasing the demand for oil, then if the dollar continues to be weak the price of energy in the USA will become so high as to damage growth prospects there.

So, where are we with all this?

Even academic economists are beginning (very belatedly) to question the validity of their models. Across the world, the games are so weighted and rigged, the rules so suddenly variable, that we are talking about how things ought to work, rather than how they really do. This is why it's now a fertile ground for conspiracy theorists: there really is a lot of conspiracy. Trouble is, we don't know all of the plots, all of the players, and all of the details.

What I think we can do, is look at the ocean tide, and not at the individual waves.

Historically, Western countries became wealthy on technological advances and were able to sell goods not just to each other, but to undeveloped countries in exchange for cheap resources. Then the latter countries began to industrialise, and goods could be carried at low unit cost in vast bulk across oceans and continents. All that remained was to break down political barriers to trade, as Nixon began to do with his visit to China in 1972.

Trouble is, controlling the rate of change. It's one thing to turn on your oil-fired central heating, another if your fuel storage tank catches fire. We want to carry on as we are (or as we used to be), but poor people are in a hurry to attain our wealthy lifestyles, and are disinclined to progress more slowly. Vast international businesses and globe-trotting billionaires stand to do very well out of facilitating this trade; national politicians are under pressure from their voters to resist it - but on a personal level, will know how rich they themselves will be when they leave office, so long as they don't try too hard for the people who elected them.

So, while I don't quite subscribe to the Dick-Dastardly-and-Mutley view of politician's summits (G-name-a-figure, Bilderberg, et al.), I can see the natural attraction for them of a world (or at least supranational) government. It means being further away from the Great Unwashed, mixing with all the Right People, fine wines and yachts etc; it means going with the flow, helping wealth and power to gather into certain centres, and organising dole handouts to regions that lose out as a result. Only the fools will try to play King Canute.

Imagine the world economies as a series of canal locks descending a steep hill. We are in the top section, the poor countries lower down. Now if all the gates are opened at once, there will be a destructive gush of water; the narrowboats in the top lock sink into the mud; the ones at the bottom float on a higher tide; a brave soul on a surfboard (the international trader) rides a thrilling wave down the hill.

Free-traders will argue that trade brings mutual benefits; but I don't think the argument works when world income disparities are so great. A Dutchman bought Manhattan from the occupying tribe for $24, but I doubt they'd get it back for that price now, not even with 400 years' interest.

It's coming, it's coming fast, it's coming destructively; and the people we pay to stop it are telling us the lies we want to hear and planning their personal advancement*. Let us return the favour.

* “It is a totally wrong notion of people to assume that the government does anything for the people; the government is there to do something for itself, and not for the people” – Marc Faber on GoldSeek, 12 September 2009

Thursday, September 17, 2009

The night they raided Minsky

Australian economist Steve Keen summarises Hyman Minsky's Financial Instability Hypothesis, which is that you get bubble after bubble, each time increasing the debt, until the process simply cannot continue and all will be catastrophically revealed.

So he's another forecasting and fearing systemic collapse - like Marc Faber and Max Keiser recently - and now Karl Denninger.

As the Dow heads for 10,000, the FTSE soars above 5,000 but gold seems now to be consistently drifting beyond the $1,000 breakwater, I feel of the bankers, traders and politicians, as Talleyrand said of the Bourbons, that "They have learned nothing and forgotten nothing."

So he's another forecasting and fearing systemic collapse - like Marc Faber and Max Keiser recently - and now Karl Denninger.

As the Dow heads for 10,000, the FTSE soars above 5,000 but gold seems now to be consistently drifting beyond the $1,000 breakwater, I feel of the bankers, traders and politicians, as Talleyrand said of the Bourbons, that "They have learned nothing and forgotten nothing."

Sunday, September 13, 2009

20:20 hindsight and the coming stock collapse

Look at this fascinating interactive graphic from the New York Times, about the shrinking and swelling of the major US financial firms. They may not have seen it coming, but boy can they see clearly in the rear-view mirror. (htp: Barry Ritholtz)

So, is all well again?

Denninger thinks not. To get back to where we were in 2000, either debt has to be slashed (this isn't the path chosen by the powers-that-be over the last couple of years) or GDP and incomes have to soar (how? Who are we suddenly going to sell loads more to?).

Given a choice of the impossible and the merely unpleasant, it looks as though there must be a large-scale default sometime - either of actual debt, or of current and/or future government-provided benefits (or both).

In the meantime, the monetary pumping may erode the dollar's value and cause a highly misleading leap in nominal stock prices. Like I said yesterday, I think we could be looking at a re-run of the mid-70s to 1982. I remember an old financial adviser colleague reminiscing about the stockmarket "boom" of 1974, but he didn't mention the inflationary context, which is what concerns Marc Faber - the fundamentals are still all wrong.

So, is all well again?

Denninger thinks not. To get back to where we were in 2000, either debt has to be slashed (this isn't the path chosen by the powers-that-be over the last couple of years) or GDP and incomes have to soar (how? Who are we suddenly going to sell loads more to?).

Given a choice of the impossible and the merely unpleasant, it looks as though there must be a large-scale default sometime - either of actual debt, or of current and/or future government-provided benefits (or both).

In the meantime, the monetary pumping may erode the dollar's value and cause a highly misleading leap in nominal stock prices. Like I said yesterday, I think we could be looking at a re-run of the mid-70s to 1982. I remember an old financial adviser colleague reminiscing about the stockmarket "boom" of 1974, but he didn't mention the inflationary context, which is what concerns Marc Faber - the fundamentals are still all wrong.

What's good for the [Dow] ISN'T good for the country

Jesse: It is possible that the Fed monetizes sufficiently to reinflate an equity bubble, essentially whoring out the Dollar and the real economy for the sake of the financial or FIRE sector.

This is what I have been thinking - that the stock indices are now fundamentally disconnected from the health of the economy.

This is what I have been thinking - that the stock indices are now fundamentally disconnected from the health of the economy.

Saturday, September 12, 2009

Dow now, and then - "Brief Encounter"

Discussing the Dow, I have previously suggested that instead of looking back to 1929, we might use the period 1966 - 1982 as a comparator. I've adjusted January 1966 and December 1999 to = 100 and oddly enough, the beginning of September 2009 sees the Dow past and present at a fairly similar point.

Discussing the Dow, I have previously suggested that instead of looking back to 1929, we might use the period 1966 - 1982 as a comparator. I've adjusted January 1966 and December 1999 to = 100 and oddly enough, the beginning of September 2009 sees the Dow past and present at a fairly similar point.Is it too fanciful to say that we're now in the equivalent of about 1976?

Monday, August 31, 2009

Marc Faber - total breakdown ahead

... in my view, the big crisis is ahead of us. It may come in 4 or 5 years' time, maybe only in 10 years' time, but the total breakdown of the system is ahead of us and it will devastate the global economy. (4:18 on)

You have to decide whom to believe. Including Steve Keen, it's said that only 12 professional economists worldwide foresaw the crunch, although there are 10 - 15,000 practising in the US alone. So the majority verdict is useless. To me, Faber has the ring of truth.

The good news, such as it is, is that we may have a few years to prepare.

As to perceived turning points, I looked at this last December:

Monday, August 10, 2009

Back where we started

As concern grows for the future of the dollar, we should reinterpret stock movements to take account of currency exchange fluctuations. The above chart shows the Dow since the start of the year (red line) and adjusted for relative value of the US dollar against the Euro (green line).

As concern grows for the future of the dollar, we should reinterpret stock movements to take account of currency exchange fluctuations. The above chart shows the Dow since the start of the year (red line) and adjusted for relative value of the US dollar against the Euro (green line).If you have any suggestions as to what other currency to use instead, I'd be glad to read them. I fear that future weakening of the British pound and the US dollar may well undermine apparent future recoveries on their stock exchanges.

Thursday, July 02, 2009

Dow 400?

Tim Iacono quotes the Elliott Wave people:

For the record, EWFF also shows a "grand supercycle," beginning in January 2000 and ending at 400. Yes, that was FOUR HUNDRED.

And I thought I was being Eeyorish at 2,000.

For the record, EWFF also shows a "grand supercycle," beginning in January 2000 and ending at 400. Yes, that was FOUR HUNDRED.

And I thought I was being Eeyorish at 2,000.

Sunday, June 07, 2009

Thursday, May 14, 2009

Dow 4,000 yet again

The Mogambo Guru is off on one of his comedy riffs again, and reiterating his devotion to gold, but here's a statistic he quotes midway:

“the price-to-earnings ratio for the Dow Jones Industrial Index is now a hefty 43.1! It should be, historically, less than 20!”

Do the math, as they say. In fact, I'll do it for you now: take the Dow at close the night before Mogambo ranted (8,469.11) and multiply by 20/43.1. Result: 3,929.98.

I gues the question is, is the current low level of company earnings a temporary matter caused by recent dislocations, or is it set to continue as the economic climate darkens?

Plus, as we all know, the market can stay irrational longer than you can stay solvent. But I still think that, adjusted for what now seems inevitable high inflation, we're going to see Dow 4,000 sometime, as I graphed back in December:

“the price-to-earnings ratio for the Dow Jones Industrial Index is now a hefty 43.1! It should be, historically, less than 20!”

Do the math, as they say. In fact, I'll do it for you now: take the Dow at close the night before Mogambo ranted (8,469.11) and multiply by 20/43.1. Result: 3,929.98.

I gues the question is, is the current low level of company earnings a temporary matter caused by recent dislocations, or is it set to continue as the economic climate darkens?

Plus, as we all know, the market can stay irrational longer than you can stay solvent. But I still think that, adjusted for what now seems inevitable high inflation, we're going to see Dow 4,000 sometime, as I graphed back in December:

Monday, April 20, 2009

Straws in the wind, the flight of birds

Yesterday, I read the entrails and thought the market was due to tank. Today, the FTSE drops 102 points, the Dow 290. Tomorrow - "¿Quien sabe?"

Monday, April 13, 2009

Protecting against inflation

Before we start, please read my disclaimer above!

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5: True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5:

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

When Nixon closed the "gold window" (15 August 1971), gold ceased to be a currency backing and became just another thing you could choose to invest in, so let's compare these assets from a little before that turning-point, onwards:

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

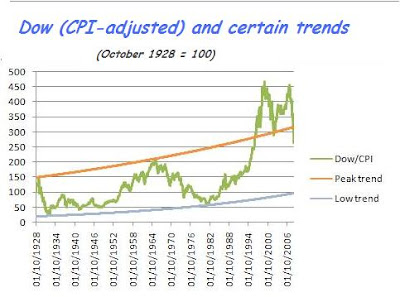

That depends on whether you read this as a statement about gold, or about the Dow. I looked at the Dow in inflation (CPI) terms a while back (December 2008):

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

Back to gold-pricing: it's also notable that the Dow is currently still worth some 8 ounces of gold, but in previous lows (Feb. 1933, March 1980) fell below 2 ounces: So should we still pile into gold, as a hedge against the further collapse of the Dow?

So should we still pile into gold, as a hedge against the further collapse of the Dow?

I think not. Firstly, the Dow may well have a rally, since it's fallen so sharply in such a short time. And secondly, this is missing the point, which is that we are looking to protect wealth against inflation, not against the Dow.

So another question is, how does gold hold its value during periods of price inflation? A period some readers may have lived through, is that after the oil price hike of October 1973. Here is what happened in the 5 years from 1974 to 1978:

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.But let's wind the clock back just a little - let's go back to that closing of the gold window again, and see what happened between August 1971 and the end of 1978:

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

Friday, April 10, 2009

Gold and the Dow

The Dow has certainly varied in its relationship with gold. The monthly low points since 1928 were February 1933 (1.95 ounces) and March 1980 (1.24 ounces).

As of 1st April, it was the equivalent of 8.4 ounces. So although gold has risen substantially since the 2000 watershed, one could argue that either gold still has a long way to rise, or the Dow a long way to fall, before the next bottoming-out.

As of 1st April, it was the equivalent of 8.4 ounces. So although gold has risen substantially since the 2000 watershed, one could argue that either gold still has a long way to rise, or the Dow a long way to fall, before the next bottoming-out.

More on bonds, and an alternative view

Antal E. Fekete is a professor of money and banking in San Francisco (such a beautiful place, too). He has a pet thesis about the bond market, which is that every time interest rates halve, effectively the capital value of (older) bonds doubles, to match the yield on new bonds.

So as long as we expect the government to try to stimulate the economy by lowering interest rates, there's a killing to be made in the bond market. Theoretically this could go on forever, even in a low-interest environment - the logic holds if rates go from 0.25% to 0.125% - provided the Treasury doesn't simply go straight to zero interest, of course.

Anyhow, his latest essay says that the monetary stimulus will simply be used to settle debts, since debt gets more and more burdensome in a deflationary depression; and settling debt instead of making and buying more stuff, continues to drive deflation. In this enviroment, few businesses will want to take on more debt (certain and fixed) in the hope of increasing their profits (far from certain, and very variable). On a national level, and following the ideas of Melchior Palyi, he now sees every extra dollar of debt as causing GDP to contract.

Therefore, valuations of most assets will continue to decline - except for bonds, which are now the focus for speculators. To this extent, he agrees with Marc Faber (cited in the previous post): we now have a bubble in government bonds.

But something will go bang. The real world shies from the inevitable conclusions of mathematical models. I think it will come as a crisis in foreigners' confidence in the dollar - there will be a reluctance to buy US Treasuries (we've already seen failed sales of government bonds in the UK recently, and when the next one succeeded, that's because it was a sale of index-linked bonds). Even now, the Chinese have switched from Agencies (debts of States and municipal organisations) to Federal debt, and within the latter, from longer-dated bonds to shorter-dated ones. If government debt was an aircraft, the Chinese would be the passenger insisting on a seat next the emergency exit near the tailplane.

To use a different analogy (one I've used before), drawn from the Lord of the Rings, the rally in the dollar and the flight to US Treasury debt seems to me like the retreat to the fortress of Helm's Deep: a last-ditch defence, doomed to be overwhelmed. Can we see a little figure about to save the day by dropping the Ring of Power into the lava in Mount Doom? We can hope; but you don't make survival plans based purely on optimism.

I therefore expect a transition from deflationary depression to inflationary depression, at some point. Perhaps a sort of 1974 stockmarket moment: an apparent turnaround, which when analysed can be shown to continue the real loss of value for some years. Only when national budgets are brought under strict control, will there be the environment for true growth. I don't see a willingness to tackle that, on either side the Atlantic, so disaster will have to be our teacher.

Thursday, April 09, 2009

Thursday, April 02, 2009

What goes up

Dow over 8k, FTSE over 4k...

I dont know where Im going

But, I sure know where Ive been

Hanging on the promises

In songs of yesterday

An Ive made up my mind,

I aint wasting no more time

But, here I go again

Here I go again

(Whitesnake)

Maybe the national brokers are right. I don't think so.

I dont know where Im going

But, I sure know where Ive been

Hanging on the promises

In songs of yesterday

An Ive made up my mind,

I aint wasting no more time

But, here I go again

Here I go again

(Whitesnake)

Maybe the national brokers are right. I don't think so.

Tuesday, March 17, 2009

Alle aussteigen!

As the Dow heads cheerily in the direction of 9,000, some may consider this an opportunity to get off if they missed the stop last time round.

Or have the wise actions of our leaders solved all?

Or have the wise actions of our leaders solved all?

Monday, March 16, 2009

Bonner: 1966 - 1982 , and Dow 5,000

Bill Bonner, in the Daily Reckoning, confirms what I've said here many times: we need to measure investment performance in inflationary terms, and done that way, the last cycle ran from 1966 to 1982. The implication for us now?

We only bring this up to warn readers: these major cycles take time. So far, the Dow has only gotten down to the ’66 TOP. Now, it has to get to the ’82 BOTTOM…adjusted for inflation. Where would that be?

Well….as we recall, the Dow was barely at 1,000 when the bull market began. And if [we] adjust that to consumer price inflation, we come to a 2,000 – 3,000.

However, the 1982 bottom was higher than the 1932 bottom, so I'm hoping it will be no worse than 4,000. Having said that, the levels of governmental and personal debt now are quite unprecedented.

Here's the graph I did last October, again:

Subscribe to:

Posts (Atom)