A few days ago on the Broad Oak Blog, I referred to Brad Setser's theory that China has been using the UK to make purchases of US Treasury securities, and that this may offer a different view of what has been happening recently (the apparent reduction in Chinese support for US debt).

In response to a comment, I suggested that the reason for this supposed system of proxy purchases was to allay the fears of the American public.

It occurs to me now, belatedly, that the recent reduction in direct Chinese holdings, coupled with the increase in holding by the UK, may be a preparation for a self-protective (or even punitive) dump of Treasuries using the same intermediaries. If their direct holdings remained relatively unchanged, the Chinese could (if their nominees stayed quiet) deny responsibility and forestall a backlash from American public opinion.

Showing posts with label Treasury securities. Show all posts

Showing posts with label Treasury securities. Show all posts

Friday, February 19, 2010

Tuesday, February 16, 2010

China extending secret support for USA

Reportedly, China has radically reduced its holdings of US Treasury securities; actually, the truth may be exactly the opposite - see my post on the Broad Oak Blog.

Monday, August 31, 2009

Splat

A couple of days ago I said that US debt default would splat the US far worse than its trading partners; of course, I missed the point. The real danger is rejection of US debt and the US dollar by its foreign purchasers, and both Karl Denninger and Jesse see that as an outcome of the Japanese election result.

Thursday, July 23, 2009

Out of their depth

The first serious, sensible, important piece I've seen from Toby Young, and it's a corker. He reflects on the well-heeled but louche and rackety Bullingdon Club, of which David Cameron and Boris Johnson were members:

... the theatrical element of Oxford's secret clubs and societies, the fact that so much of their activity seemed designed to dazzle and mystify bemused onlookers, is precisely what makes them such ideal training grounds for British public life.

... you don't have to be to the manor born to become a member of Britain's ruling class - or even particularly clever. You don't need charisma or sexual confidence or a sense of entitlement. All you need is the wherewithal to pretend to be someone who has these qualities. Provided you can do a reasonable impression of a person with the right stuff - and provided you wear the right uniform - that's enough to propel you to the top.

... you don't have to be to the manor born to become a member of Britain's ruling class - or even particularly clever. You don't need charisma or sexual confidence or a sense of entitlement. All you need is the wherewithal to pretend to be someone who has these qualities. Provided you can do a reasonable impression of a person with the right stuff - and provided you wear the right uniform - that's enough to propel you to the top.

... The discovery that all these young pretenders make when they take their seats at the Cabinet table, or become QCs, or pocket £100million on a complicated land deal, is that the people at the very pinnacle of British society - the people pulling the levers of power - are exactly like them.

complicated land deal, is that the people at the very pinnacle of British society - the people pulling the levers of power - are exactly like them.

There is no such thing as the real McCoy, just a bunch of schoolboys parading around in the contents of the dressing-up box. They don't feel like frauds, because everyone else in this elite little club is as fraudulent as they are.

And when all is well, they get away with it. But when it comes to an emergency, a crisis needing skill, grit and sacrifice?

My father served his 25 in the British Army, and my mother used to say, "Thank God for civilians," i.e. the experienced people that would come in on callup when war broke out. Doubtless it's different now, with our much reduced and far more battle-experienced Armed Services, but in my father's career he met more than a few "educated idiots." Does the current crop of politicians and bankers have what it takes, including the moral fibre, to get us out of this mess? Or when it gets too tough, will they jump, like "Lord Jim" Blair, leaving us to our fate?

My father served his 25 in the British Army, and my mother used to say, "Thank God for civilians," i.e. the experienced people that would come in on callup when war broke out. Doubtless it's different now, with our much reduced and far more battle-experienced Armed Services, but in my father's career he met more than a few "educated idiots." Does the current crop of politicians and bankers have what it takes, including the moral fibre, to get us out of this mess? Or when it gets too tough, will they jump, like "Lord Jim" Blair, leaving us to our fate?

... the theatrical element of Oxford's secret clubs and societies, the fact that so much of their activity seemed designed to dazzle and mystify bemused onlookers, is precisely what makes them such ideal training grounds for British public life.

... you don't have to be to the manor born to become a member of Britain's ruling class - or even particularly clever. You don't need charisma or sexual confidence or a sense of entitlement. All you need is the wherewithal to pretend to be someone who has these qualities. Provided you can do a reasonable impression of a person with the right stuff - and provided you wear the right uniform - that's enough to propel you to the top.

... you don't have to be to the manor born to become a member of Britain's ruling class - or even particularly clever. You don't need charisma or sexual confidence or a sense of entitlement. All you need is the wherewithal to pretend to be someone who has these qualities. Provided you can do a reasonable impression of a person with the right stuff - and provided you wear the right uniform - that's enough to propel you to the top.... The discovery that all these young pretenders make when they take their seats at the Cabinet table, or become QCs, or pocket £100million on a

complicated land deal, is that the people at the very pinnacle of British society - the people pulling the levers of power - are exactly like them.

complicated land deal, is that the people at the very pinnacle of British society - the people pulling the levers of power - are exactly like them.There is no such thing as the real McCoy, just a bunch of schoolboys parading around in the contents of the dressing-up box. They don't feel like frauds, because everyone else in this elite little club is as fraudulent as they are.

And when all is well, they get away with it. But when it comes to an emergency, a crisis needing skill, grit and sacrifice?

{kind=link}

My father served his 25 in the British Army, and my mother used to say, "Thank God for civilians," i.e. the experienced people that would come in on callup when war broke out. Doubtless it's different now, with our much reduced and far more battle-experienced Armed Services, but in my father's career he met more than a few "educated idiots." Does the current crop of politicians and bankers have what it takes, including the moral fibre, to get us out of this mess? Or when it gets too tough, will they jump, like "Lord Jim" Blair, leaving us to our fate?

My father served his 25 in the British Army, and my mother used to say, "Thank God for civilians," i.e. the experienced people that would come in on callup when war broke out. Doubtless it's different now, with our much reduced and far more battle-experienced Armed Services, but in my father's career he met more than a few "educated idiots." Does the current crop of politicians and bankers have what it takes, including the moral fibre, to get us out of this mess? Or when it gets too tough, will they jump, like "Lord Jim" Blair, leaving us to our fate?We're going to find out sooner than we'd like, if Denninger is right. He's looking at new Treasury debt issuance of $235 billion in the next week alone, and is busily folding his kitchen foil into a helmet:

Folks, this is how you get detonation of a nation's monetary and political system. Timing the "event" it is not easy, but the certainty of outcome given this sort of outrageously irresponsible activity is not in doubt.

I'm increasing my stock of things that "will never go to zero" and keeping my ear to the ground. The "short the phone book but make sure you get out fast before you get trampled" moment approaches - mark my words.

Sunday, July 19, 2009

Step by step - how the dollar is recycled via China

A propos China and monetary inflation, please see two very useful and enlightening articles by The Contrarian Investor - this explaining why the money supply is growing there, and this detailing the steps by which money from the US goes on a round trip to China and back.

Sunday, June 14, 2009

Giant US slush fund?

Karl Denninger continues to reflect on a story that hasn't had much coverage - two Japanese have been caught in Italy, attempting to smuggle $134 BILLION in bearer bonds. KD thinks it's part of secret additional financing for the US.

This is not quite as ludicrously James Bond-ish as it seems. Bear in mind that some time ago, Brad Setser studied Treasury bond purchases by China and the UK and concluded that the latter country was acting as an additional conduit for the former's loans.

Good news for the Italians - their law says they'll take 40% of the contraband.

This is not quite as ludicrously James Bond-ish as it seems. Bear in mind that some time ago, Brad Setser studied Treasury bond purchases by China and the UK and concluded that the latter country was acting as an additional conduit for the former's loans.

Good news for the Italians - their law says they'll take 40% of the contraband.

Monday, April 13, 2009

Protecting against inflation

Before we start, please read my disclaimer above!

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5: True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5:

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

When Nixon closed the "gold window" (15 August 1971), gold ceased to be a currency backing and became just another thing you could choose to invest in, so let's compare these assets from a little before that turning-point, onwards:

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

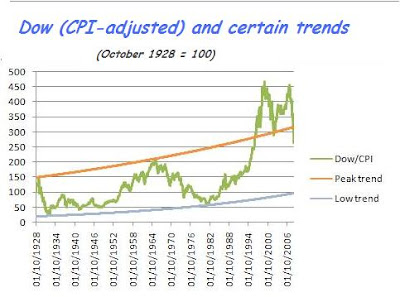

That depends on whether you read this as a statement about gold, or about the Dow. I looked at the Dow in inflation (CPI) terms a while back (December 2008):

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

Back to gold-pricing: it's also notable that the Dow is currently still worth some 8 ounces of gold, but in previous lows (Feb. 1933, March 1980) fell below 2 ounces: So should we still pile into gold, as a hedge against the further collapse of the Dow?

So should we still pile into gold, as a hedge against the further collapse of the Dow?

I think not. Firstly, the Dow may well have a rally, since it's fallen so sharply in such a short time. And secondly, this is missing the point, which is that we are looking to protect wealth against inflation, not against the Dow.

So another question is, how does gold hold its value during periods of price inflation? A period some readers may have lived through, is that after the oil price hike of October 1973. Here is what happened in the 5 years from 1974 to 1978:

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.But let's wind the clock back just a little - let's go back to that closing of the gold window again, and see what happened between August 1971 and the end of 1978:

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

Friday, April 10, 2009

More on bonds, and an alternative view

Antal E. Fekete is a professor of money and banking in San Francisco (such a beautiful place, too). He has a pet thesis about the bond market, which is that every time interest rates halve, effectively the capital value of (older) bonds doubles, to match the yield on new bonds.

So as long as we expect the government to try to stimulate the economy by lowering interest rates, there's a killing to be made in the bond market. Theoretically this could go on forever, even in a low-interest environment - the logic holds if rates go from 0.25% to 0.125% - provided the Treasury doesn't simply go straight to zero interest, of course.

Anyhow, his latest essay says that the monetary stimulus will simply be used to settle debts, since debt gets more and more burdensome in a deflationary depression; and settling debt instead of making and buying more stuff, continues to drive deflation. In this enviroment, few businesses will want to take on more debt (certain and fixed) in the hope of increasing their profits (far from certain, and very variable). On a national level, and following the ideas of Melchior Palyi, he now sees every extra dollar of debt as causing GDP to contract.

Therefore, valuations of most assets will continue to decline - except for bonds, which are now the focus for speculators. To this extent, he agrees with Marc Faber (cited in the previous post): we now have a bubble in government bonds.

But something will go bang. The real world shies from the inevitable conclusions of mathematical models. I think it will come as a crisis in foreigners' confidence in the dollar - there will be a reluctance to buy US Treasuries (we've already seen failed sales of government bonds in the UK recently, and when the next one succeeded, that's because it was a sale of index-linked bonds). Even now, the Chinese have switched from Agencies (debts of States and municipal organisations) to Federal debt, and within the latter, from longer-dated bonds to shorter-dated ones. If government debt was an aircraft, the Chinese would be the passenger insisting on a seat next the emergency exit near the tailplane.

To use a different analogy (one I've used before), drawn from the Lord of the Rings, the rally in the dollar and the flight to US Treasury debt seems to me like the retreat to the fortress of Helm's Deep: a last-ditch defence, doomed to be overwhelmed. Can we see a little figure about to save the day by dropping the Ring of Power into the lava in Mount Doom? We can hope; but you don't make survival plans based purely on optimism.

I therefore expect a transition from deflationary depression to inflationary depression, at some point. Perhaps a sort of 1974 stockmarket moment: an apparent turnaround, which when analysed can be shown to continue the real loss of value for some years. Only when national budgets are brought under strict control, will there be the environment for true growth. I don't see a willingness to tackle that, on either side the Atlantic, so disaster will have to be our teacher.

Thursday, March 19, 2009

Where is all the money going?

I read recently that both in the US and the UK, a significant part of the "quantitative easing" is repurchasing sovereign debt from foreign holders. In other words, money is being created to buy back government bonds from overseas investors.

This says two things to me: (a) the new money thus created is not going to help kick-start our economies, and (b) foreigners are losing confidence in us and want out, before inflation and defaults shrivel the value of their investment in us. As to the latter point, I said last August that I thought the Chinese wouldn't let themselves be swindled.

So I suspect we are still headed for slump, currency devaluation and, eventually, high interest rates.

Maybe a new currency, to whitewash the mess and make further progress towards some New World Order political grouping - Oceania, Eurasia etc. Any news on the Amero?

This says two things to me: (a) the new money thus created is not going to help kick-start our economies, and (b) foreigners are losing confidence in us and want out, before inflation and defaults shrivel the value of their investment in us. As to the latter point, I said last August that I thought the Chinese wouldn't let themselves be swindled.

So I suspect we are still headed for slump, currency devaluation and, eventually, high interest rates.

Maybe a new currency, to whitewash the mess and make further progress towards some New World Order political grouping - Oceania, Eurasia etc. Any news on the Amero?

Sunday, February 08, 2009

Janszen, Faber: hyperinflation is government policy

(Graph reproduced by iTulip from NowAndFutures.com)

(Graph reproduced by iTulip from NowAndFutures.com)In an extended "Titanic" analogy, Eric Janszen describes what he sees as the government's response to the crisis: "send rescue", "boil the ocean" and if terrified investors refuse to relinquish the security of Treasury bonds, "sink the rafts" by devaluing the currency. Around the world, he sees a policy of inflation and even hyper-inflation. So does chipper doomster Marc Faber, who now thinks we must eventually have 200% inflation in the USA. 1974 - 82, here we come again?

Saturday, January 31, 2009

The Greenback is Red-backed

Brad Setser returns to a favourite theme, China's investment in the US. If I can summarise:

Brad Setser returns to a favourite theme, China's investment in the US. If I can summarise:1. China buys American bonds directly, but also via the UK. Practically all the UK's purchases are on behalf of China.

2. American government bonds are either Treasuries (debts of the government of the USA) or Agencies (debts of US States and local government). Concerned about risk, China has recently been selling Agencies to buy Treasuries, because the latter are backed by the Federal Government.

3. China will continue to invest in the US, because this keeps up demand for the dollar and so keeps down the Chinese currency, the Renminbi. This means that Chinese exports to America will remain very competitive in terms of price.

4. China's continuing support will stop the US dollar from collapsing in the world currency market, as many have feared. Other countries who are also running a trade deficit and need financing, have much more reason to worry.

Wednesday, January 21, 2009

Newsflash

All is well: the Dow has just sailed (well, snailed) back through the 8,000 barrier. But what's this? Brad Setser doesn't know what to think about China's role in US debt financing.

Here he thinks that a downturn in China's production will be panic their already-prudent populace into saving even more money, and

they'll also import less, which will screw our deflation down even tighter:

Bottom line: A big fall in activity in China will tend to drive China’s trade surplus up. It thus would tend to increase — not reduce — China’s (net) purchases of foreign assets. Someone in China will still buying foreign assets — and likely providing indirect support for the Treasury market — even if it is not China’s central bank. A big fall in activity also means less Chinese demand for the world’s products — as well as less Chinese demand for China’s products, which frees up capacity to export. That adds to the deflationary forces in the world economy.

... and here he worries about the switch from long-term purchases of Treasuries, to ones with short maturity dates:

At the same time, it is risky to finance a large external deficit with short-term debt. Even for the US. If the US deficit starts to head back up again — as, for example, the effect of the recent fall in oil prices wears off and a large fiscal stimulus in the US stimulates the world economy — without a shift in the composition of inflows, there would be cause for concern.

It's said that Charles Colson, an aide to President Nixon, had this motto framed in his office: "When you've got them by the balls, their hearts and minds will follow." Funny, until you're on the receiving end.

Here he thinks that a downturn in China's production will be panic their already-prudent populace into saving even more money, and

they'll also import less, which will screw our deflation down even tighter:

Bottom line: A big fall in activity in China will tend to drive China’s trade surplus up. It thus would tend to increase — not reduce — China’s (net) purchases of foreign assets. Someone in China will still buying foreign assets — and likely providing indirect support for the Treasury market — even if it is not China’s central bank. A big fall in activity also means less Chinese demand for the world’s products — as well as less Chinese demand for China’s products, which frees up capacity to export. That adds to the deflationary forces in the world economy.

... and here he worries about the switch from long-term purchases of Treasuries, to ones with short maturity dates:

At the same time, it is risky to finance a large external deficit with short-term debt. Even for the US. If the US deficit starts to head back up again — as, for example, the effect of the recent fall in oil prices wears off and a large fiscal stimulus in the US stimulates the world economy — without a shift in the composition of inflows, there would be cause for concern.

It's said that Charles Colson, an aide to President Nixon, had this motto framed in his office: "When you've got them by the balls, their hearts and minds will follow." Funny, until you're on the receiving end.

Saturday, January 17, 2009

A hand hovers over the chain

Marc Sobel:

Marc Sobel:Do I understand the net of this posting to be that the US is much more vulnerable to a quick run on the debt, i.e. being mainly financed by short term debt which constantly has to be rolled over ?

Brad Setser:

Yes, that risk is rising...

Read the whole thing here.

Tuesday, January 13, 2009

Smugness, alla Italia

Jonathan Russell writes in the Telegraph:

Spain's finances are in the dock thanks to Standard & Poor's, the spreads on Greek bonds have soared and Germany's economy is set to deteriorate faster than ours, according to the OECD. Suddenly the euro doesn't seem like such a one-way bet.

But where is the usual suspect, Italy, in all this euro-doom? Sitting pretty according to its finance minister Giulio Tremonti. The country didn't get involved in the sub-prime crisis and GDP figures could be significantly better than reported.

How do you work this out? "Our banks suffered little from the sub-prime crisis. There are few of them where English is spoken," he told Les Echos newspaper, no doubt not in English.

And GDP? "One should be suspicious of GDP figures …they do not include the informal economy."

The Italian "informal economy"? I'm sure there is another word for that.

And as one of my earlier posts shows, they've also invested less than 1% of their officially-declared GDP in US Treasuries.

Spain's finances are in the dock thanks to Standard & Poor's, the spreads on Greek bonds have soared and Germany's economy is set to deteriorate faster than ours, according to the OECD. Suddenly the euro doesn't seem like such a one-way bet.

But where is the usual suspect, Italy, in all this euro-doom? Sitting pretty according to its finance minister Giulio Tremonti. The country didn't get involved in the sub-prime crisis and GDP figures could be significantly better than reported.

How do you work this out? "Our banks suffered little from the sub-prime crisis. There are few of them where English is spoken," he told Les Echos newspaper, no doubt not in English.

And GDP? "One should be suspicious of GDP figures …they do not include the informal economy."

The Italian "informal economy"? I'm sure there is another word for that.

And as one of my earlier posts shows, they've also invested less than 1% of their officially-declared GDP in US Treasuries.

Saturday, January 03, 2009

Murky business

Brad Setser does a very interesting bit of detective work and concludes that much of the UK's holdings of US Treasury securities, are on behalf of China. He gives us a graph demonstrating that when the UK's official holding declines sharply (usually in June), China's suddenly rises.

Setser estimates that China owns $1.425 trillion in Treasuries and Agencies, which is equivalent to about 10% of US GDP. ("Treasuries" are debts directly owed by the US Government, "agencies" are debts of the US Government's organisations, as explained in this Federal Reserve handbook from 2004.)

He ends by calling for more transparency in British accounts of these holding - that would be most welcome all round, generally. Half our problems (and, I assume, opportunities for fatcat swindlers) stem from our not knowing the real position of the world's finances.

Setser estimates that China owns $1.425 trillion in Treasuries and Agencies, which is equivalent to about 10% of US GDP. ("Treasuries" are debts directly owed by the US Government, "agencies" are debts of the US Government's organisations, as explained in this Federal Reserve handbook from 2004.)

He ends by calling for more transparency in British accounts of these holding - that would be most welcome all round, generally. Half our problems (and, I assume, opportunities for fatcat swindlers) stem from our not knowing the real position of the world's finances.

Tuesday, November 18, 2008

Latest figures on foreign holdings of U.S. Treasuries

The U.S. Treasury statistics issued today list 29 foreign holders of their securities. Between them, the three above account for $110.3 billion of the $110.6 billion increase. What is is to have friends, I suppose.

The U.S. Treasury statistics issued today list 29 foreign holders of their securities. Between them, the three above account for $110.3 billion of the $110.6 billion increase. What is is to have friends, I suppose.Wednesday, October 22, 2008

Throw the grenade, or put it in your pocket?

I was educated in the wrong things. Karl Denninger explains - in a way I struggle to understand fully - how the US government's schemes to support the banks must ultimately be financed by Treasury bonds on such a scale as to seriously damage their credit rating and pump up interest rates to a ruinous level.

This is a consequence of avoiding taking the right action, i.e. finding out who's insolvent and letting them go bust. I still remember Henry Paulson's panicky look when Congress threw out the bailout bill the first time.

Once you've pulled the pin out of a grenade, you can throw it, or you can hang on to it. Madly, it looks as though the government is following the latter course, and hopes to be able to handle the consequences.

UPDATE

Relevant to the above is Wat's resume of public debt history in the UK since World War II, showing how important it is NOT to get into debt, to fight inflation and control the finances.

This is a consequence of avoiding taking the right action, i.e. finding out who's insolvent and letting them go bust. I still remember Henry Paulson's panicky look when Congress threw out the bailout bill the first time.

Once you've pulled the pin out of a grenade, you can throw it, or you can hang on to it. Madly, it looks as though the government is following the latter course, and hopes to be able to handle the consequences.

UPDATE

Relevant to the above is Wat's resume of public debt history in the UK since World War II, showing how important it is NOT to get into debt, to fight inflation and control the finances.

Saturday, October 11, 2008

Refuge, flight, battle rejoined, victory, retribution

Brad Setser looks at a flood of demand for US Treasuries and suspects that it's central banks shifting into the securest dollar asset they can find; and away from other dollar-denominated assets.

Brad Setser looks at a flood of demand for US Treasuries and suspects that it's central banks shifting into the securest dollar asset they can find; and away from other dollar-denominated assets.The first comment on the same post says that the next stage is a run on the dollar.

Continuing the Tolkien fantasy theme, one recalls the flight to Helm's Deep, and the eventual breach. Ultimately, though at a cost, the good side wins, of course (Denninger explains today how we can face the mess and clean it up).

Time to revisit Michael Panzner's "Financial Armageddon" - reviewed here in May of last year.

If he's right - and he's been right so far - it's first cash, then out of cash. But there's not enough gold to act as the world's currency (unless a horrific amount of wealth is permanently destroyed), and if we start up a new fiat currency, the moral criminals of the banking class will play the game all over again.

I note that Max Hastings in the Daily Mail calls for bankers to be "named and shamed"; this is milksop stuff. Yet they're still going to get billions in bonuses this year! Why does the Proceeds of Crime Bill not apply? Heavy, heavy fines, so that generations of bankers and traders will remember and hesitate. How about the last 5 years' bonuses, as a benchmark? Punitur quia peccatum est ("punishment is to be inflicted, because a crime has been committed").

But even that's not enough. What about the political class that opened the financial sluices to alleviate the discomfort of 2002-2003? And did it several times before, too? (See Jesse today on Greenspan's bubbles.) How do we mete out condign punishment to those greedy for power, as well as those for money?

I repeat, this is a crisis of democracy.

Friday, September 19, 2008

Murky support for the dollar

Brad Setser looks at data from the US Treasury International Capital System (TIC), trying to work out what's been going on in the money supply and why the dollar hasn't collapsed in all this brouhaha. Setser, who gave evidence to a Congressional committee last year, admits that the picture is not clear, despite his expertise.

He thinks real purchases of Treasury securities (2000 - mid-2007) are about double the official amounts, and points out that when the dollar weakens, it is supported by further buying from central banks. Also, Americans have sold a lot of foreign equities recently and the money has come home.

A significant change in the pattern is the reduction of private holdings of Treasury securities - more and more, the support is coming from official sources, as the following graph suggests:

This seems to me like another straw in the wind: "power to the people", not.

Subscribe to:

Posts (Atom)