The Mail says Ed Balls predicted the crash in 2007, which is why he urged Brown to hold a snap election.

Out of 20,000 professional economists, Oz econ academic Steve Keen reckons only some 20 saw it coming. EB has an econ-academic background; so has his brother Andrew, who joined bond investment giant Pimco in 2006. Did the latter have interesting conversations with the former in 2007?

Clearly we need Balls' insight - as long as his concern is not limited to party success. What is he predicting now, I wonder?

READER: PLEASE CLICK THE REACTION BELOW - THANKS!

All original material is copyright of its author. Fair use permitted. Contact via comment. Unless indicated otherwise, all internet links accessed at time of writing. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Showing posts with label systemic crisis. Show all posts

Showing posts with label systemic crisis. Show all posts

Sunday, January 18, 2015

Thursday, August 14, 2014

Is your money safe in the bank? - revisited

John Ward reports that some South African bank savers are now having their accounts raided to shore up a different bank, African Bank Investments Ltd. Even more disturbingly, the example he quotes is of a customer whose SA bank is part of the international Barclays group, so the link stretches back to the UK itself.

Almost exactly seven years ago, and over a year before the global banking crisis of 2008/9 hit us, I warned British readers that protection for their savings was limited. At that time (August 2007), you were guaranteed 100% of the first 2,000 in your account, and only 90% of the next £33,000. So the maximum compensation in the case of a bank wipeout, even if you had millions, was £31,700.

Now, and as a result of the crisis (and more importantly, to prevent a system-destroying general run on the banks) the "guarantee" has been increased to 100% of the first £85,000 per person (see FSCS here). That's per bank group, so if you have more than one bank account make sure they're not part of the same group.

But why is a guarantee needed in the first place? Surely the money you have deposited is yours, same as if you'd asked them to look after your house deeds.

Not at all. Here is the law as explained by Toby Baxendale on The Cobden Centre website in 2010:

The key case is Carr v Carr 1811 (reported in Merivale (541 n) 1815 – 17). A testator in making his bequest said “whatever debts might be due to him…at the time of his death”, the key question in this case being whether “a cash balance due to him on his banker’s account” passed by this bequest. The Master of the Rolls, Sir William Grant held that it did. He reasoned that it was not a depositum; a sealed bag of money could be, but this generally deposited money could not possibly have an ‘earmark’. Grant concluded on this point, “when money is paid into a banker’s, he always opens a debtor and creditor account with the payor. The banker employs the money himself, and is liable merely to answer the drafts of his customers to that amount.” For the legal scholars among you, Vaisey v Reynolds 1828 and Parker v Merchant 1843 both affirmed this position.

In Davaynes v Noble 1816 it was argued in front of Grant that a banker is a bailee rather than a debtor. Rejecting that argument, Grant said “money paid into a banker’s becomes immediately a part of his general assets; and he is merely a debtor for the amount.”

In Sims v Bond 1833 the Chief Justice of the Queens Bench Division affirmed in judgement “sums which are paid to the credit of a customer with a banker, though usually called deposits, are, in truth, loans by the customer to the banker.”

The House of Lords, then the highest court in the land, had its say on the matter in Foley v Hill and Others 1848, duly reported in the Clerk’s Reports, House of Lords 1847-66 (pages 28 and 36-7). In summary, the appellant in 1829 opened a bank account with the respondent bankers. Two further deposits we added in 1830 and in 1831 interest was still added. In 1838 the appellant brought proceedings against the respondent bankers seeking recovery of both the principle and interest. The counsel cleverly tried to argue that it was the duty of the respondent bankers to keep all the accounts up to date at all times and thus there was more to this relationship than that of debtor and creditor.

The Lord Chancellor Cottenham said the following in judgement

Thus the settled position of the law is that when you deposit, the bank becomes the owner of the money deposited and you become a creditor to the bank.

We have now established that you shouldn't have more than £85,000 in any group of banks.

Strictly speaking, it's not the government's guarantee, it's the FSCS's: "The Financial Services Compensation Scheme (FSCS) is backed by government" (my italics). The FSCS runs a fund and pays claims out of money it levies on UK financial institutions. In a bad - not the worst possible - situation it can borrow from the Treasury, and has done so, as this official attempt to reassure us says:

What if a giant goes bust? Is there enough cash?

The FSCS has paid out more than £26bn and helped more than 4.5m people since 2001. We are funded by the industry, but the FSCS can borrow money from the Treasury if the compensation costs of a major failure are more than the industry can meet. That is what happened when banks failed in 2008.

So consumers can be reassured the FSCS will always have the money to pay compensation. No-one has ever lost a penny of protected deposits and no-one ever will.

What about "bail-ins", like the case referred to by John Ward above?

For example, in the event of a building society's insolvency, depositors' claims used to rank below other unsecured creditors and so were more likely than the latter to be required to accept something other than their money back. This is now changing:

"...the BRRD has been agreed and will require us to introduce a slightly different form of depositor preference. It will require a two tier preference, where:

We anticipate that the Directive will come into force by May 2014. The transposition deadline is 1 January 2015."

The Government's general guiding principle is to reassure depositors that they won't be fleeced in a crisis:

"Section 60B [of the Banking Act] requires the Treasury, when making these regulations, to have regard to the desirability of “ensuring that pre-resolution shareholders and creditors of a bank do not receive less favourable treatment than they would have received had the bank entered insolvency immediately before the coming into effect of the initial instrument” (the first instrument made by the Bank in the resolution)."

Why are they doing this? Well, here's Oz comedy pair Clarke and Dawe on the effect of the Cyprus bank bail-in:

Still:

(a) I don't see anything that limits the power of the FSCS and others to alter or suspend their guarantees, if they feel they have to;

(b) a leading barrister has given his views (in 2011 on CityWire) on the potential case against the FSCS's fund-raising powers;

(c) the Emergency Powers Act of 1920 allows the Privy Council to do pretty much whatever it likes in the short run, if it determines that there is an emergency*;

(d) anything can happen, and in a very bad situation some of those things could be beyond the Government's power to control;

(e) theft by inflation is always a threat, and despite a long campaign by me my MP has so far refused to stand up at Prime Minister's Question Time and ask when the Government is going to restore National Savings Index-Linked Certificates.

Where does the Cabinet hold their own families' cash? Be useful to keep that under observation, maybe. It might not just be the Russians or tax-dodgers who want to shift money out of the UK, and Europe in general. And why is the Chinese government encouraging its citizens to hold gold?

_________________________

UPDATE: *I'm a bit behind the curve here - we now have what seems a much further-reaching and potentially sinister provision: http://en.wikipedia.org/wiki/Civil_Contingencies_Act_2004

READER: PLEASE CLICK THE REACTION BELOW - THANKS!

All original material is copyright of its author. Fair use permitted. Contact via comment. Unless indicated otherwise, all internet links accessed at time of writing. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Almost exactly seven years ago, and over a year before the global banking crisis of 2008/9 hit us, I warned British readers that protection for their savings was limited. At that time (August 2007), you were guaranteed 100% of the first 2,000 in your account, and only 90% of the next £33,000. So the maximum compensation in the case of a bank wipeout, even if you had millions, was £31,700.

Now, and as a result of the crisis (and more importantly, to prevent a system-destroying general run on the banks) the "guarantee" has been increased to 100% of the first £85,000 per person (see FSCS here). That's per bank group, so if you have more than one bank account make sure they're not part of the same group.

But why is a guarantee needed in the first place? Surely the money you have deposited is yours, same as if you'd asked them to look after your house deeds.

Not at all. Here is the law as explained by Toby Baxendale on The Cobden Centre website in 2010:

The Current State of the Law

The key case is Carr v Carr 1811 (reported in Merivale (541 n) 1815 – 17). A testator in making his bequest said “whatever debts might be due to him…at the time of his death”, the key question in this case being whether “a cash balance due to him on his banker’s account” passed by this bequest. The Master of the Rolls, Sir William Grant held that it did. He reasoned that it was not a depositum; a sealed bag of money could be, but this generally deposited money could not possibly have an ‘earmark’. Grant concluded on this point, “when money is paid into a banker’s, he always opens a debtor and creditor account with the payor. The banker employs the money himself, and is liable merely to answer the drafts of his customers to that amount.” For the legal scholars among you, Vaisey v Reynolds 1828 and Parker v Merchant 1843 both affirmed this position.

In Davaynes v Noble 1816 it was argued in front of Grant that a banker is a bailee rather than a debtor. Rejecting that argument, Grant said “money paid into a banker’s becomes immediately a part of his general assets; and he is merely a debtor for the amount.”

In Sims v Bond 1833 the Chief Justice of the Queens Bench Division affirmed in judgement “sums which are paid to the credit of a customer with a banker, though usually called deposits, are, in truth, loans by the customer to the banker.”

The House of Lords, then the highest court in the land, had its say on the matter in Foley v Hill and Others 1848, duly reported in the Clerk’s Reports, House of Lords 1847-66 (pages 28 and 36-7). In summary, the appellant in 1829 opened a bank account with the respondent bankers. Two further deposits we added in 1830 and in 1831 interest was still added. In 1838 the appellant brought proceedings against the respondent bankers seeking recovery of both the principle and interest. The counsel cleverly tried to argue that it was the duty of the respondent bankers to keep all the accounts up to date at all times and thus there was more to this relationship than that of debtor and creditor.

The Lord Chancellor Cottenham said the following in judgement

Money, when paid into a bank, ceases altogether to be the money of the principal; it is by then the money of the banker, who is bound to return an equivalent by paying a similar sum to that deposited with him when he is asked for it. The money paid into a banker’s is money known by the principal to be placed there for the purpose of being under the control of the banker; it is then the banker’s money; he is known to deal with it as his own; he makes what profit of it he can, which profit he retains to himself, paying back only the principal, according to the custom of bankers in some places, or the principal and a small rate of interest, according to the custom of bankers in other places. The money placed in custody of a banker is, to all intents and purposes, the money of the banker, to do with it as he pleases; he is guilty of no breach of trust in employing it; he is not answerable to the principal if he puts it into jeopardy, if he engages in a hazardous speculation; he is not bound to keep it or deal with it as the property of his principal; but he is, of course, answerable for the amount, because he has contracted, having received that money, to repay to the principal, when demanded, a sum equivalent to that paid into his hands.

That has been the subject of discussion in various cases, and that has been established to be the relative situation of banker and customer. That being established to be the relative situations of banker and customer, the banker is not an agent or factor, but he is a debtor.

Thus the settled position of the law is that when you deposit, the bank becomes the owner of the money deposited and you become a creditor to the bank.

We have now established that you shouldn't have more than £85,000 in any group of banks.

Strictly speaking, it's not the government's guarantee, it's the FSCS's: "The Financial Services Compensation Scheme (FSCS) is backed by government" (my italics). The FSCS runs a fund and pays claims out of money it levies on UK financial institutions. In a bad - not the worst possible - situation it can borrow from the Treasury, and has done so, as this official attempt to reassure us says:

What if a giant goes bust? Is there enough cash?

The FSCS has paid out more than £26bn and helped more than 4.5m people since 2001. We are funded by the industry, but the FSCS can borrow money from the Treasury if the compensation costs of a major failure are more than the industry can meet. That is what happened when banks failed in 2008.

So consumers can be reassured the FSCS will always have the money to pay compensation. No-one has ever lost a penny of protected deposits and no-one ever will.

What about "bail-ins", like the case referred to by John Ward above?

For example, in the event of a building society's insolvency, depositors' claims used to rank below other unsecured creditors and so were more likely than the latter to be required to accept something other than their money back. This is now changing:

"...the BRRD has been agreed and will require us to introduce a slightly different form of depositor preference. It will require a two tier preference, where:

- eligible deposits from natural persons and SMEs have a higher priority ranking in insolvency than the claims of ordinary unsecured creditors

- covered deposits have a higher priority ranking in insolvency than the part of eligible deposits from natural persons and SMEs that exceed the coverage limit

We anticipate that the Directive will come into force by May 2014. The transposition deadline is 1 January 2015."

The Government's general guiding principle is to reassure depositors that they won't be fleeced in a crisis:

"Section 60B [of the Banking Act] requires the Treasury, when making these regulations, to have regard to the desirability of “ensuring that pre-resolution shareholders and creditors of a bank do not receive less favourable treatment than they would have received had the bank entered insolvency immediately before the coming into effect of the initial instrument” (the first instrument made by the Bank in the resolution)."

Why are they doing this? Well, here's Oz comedy pair Clarke and Dawe on the effect of the Cyprus bank bail-in:

Still:

(a) I don't see anything that limits the power of the FSCS and others to alter or suspend their guarantees, if they feel they have to;

(b) a leading barrister has given his views (in 2011 on CityWire) on the potential case against the FSCS's fund-raising powers;

(c) the Emergency Powers Act of 1920 allows the Privy Council to do pretty much whatever it likes in the short run, if it determines that there is an emergency*;

(d) anything can happen, and in a very bad situation some of those things could be beyond the Government's power to control;

(e) theft by inflation is always a threat, and despite a long campaign by me my MP has so far refused to stand up at Prime Minister's Question Time and ask when the Government is going to restore National Savings Index-Linked Certificates.

Where does the Cabinet hold their own families' cash? Be useful to keep that under observation, maybe. It might not just be the Russians or tax-dodgers who want to shift money out of the UK, and Europe in general. And why is the Chinese government encouraging its citizens to hold gold?

_________________________

UPDATE: *I'm a bit behind the curve here - we now have what seems a much further-reaching and potentially sinister provision: http://en.wikipedia.org/wiki/Civil_Contingencies_Act_2004

READER: PLEASE CLICK THE REACTION BELOW - THANKS!

All original material is copyright of its author. Fair use permitted. Contact via comment. Unless indicated otherwise, all internet links accessed at time of writing. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Tuesday, March 02, 2010

Hope

My brother sends me a link to a polemic by Joe Bageant. My reply:

A passionate polemic, seductive in its combination of apparent political and financial savviness, high-level generalization, defrocked moral preaching, enemy-finding, self-pitying despair, self-castigation. Clearly one who has adopted Marcuse's Marxian-Freudian notion of "introjection". And one who secretly welcomes gotterdammerung because (surely) it is the necessary precondition of rebirth and the Golden Society. Don't believe his reference to species extinction - if he believed that he wouldn't bother to praise the international South American bartering system.

Yes, the system is in crisis - but it's fixable. The US medical system is about 3 times more expensive per capita than in the UK, there's a lot of room to cut costs. When the dollar crashes and house prices hit the floor, people won't have to earn the same money as before to make a living, and they'll begin to compete in the global market. And we surely don't really need the level of material possessions we have now, nice though it can be.

Where I do agree with this Jeremiah, is that a load of fat b*st*rds will have to be trimmed.

Put me down as a hope fiend.

A passionate polemic, seductive in its combination of apparent political and financial savviness, high-level generalization, defrocked moral preaching, enemy-finding, self-pitying despair, self-castigation. Clearly one who has adopted Marcuse's Marxian-Freudian notion of "introjection". And one who secretly welcomes gotterdammerung because (surely) it is the necessary precondition of rebirth and the Golden Society. Don't believe his reference to species extinction - if he believed that he wouldn't bother to praise the international South American bartering system.

Yes, the system is in crisis - but it's fixable. The US medical system is about 3 times more expensive per capita than in the UK, there's a lot of room to cut costs. When the dollar crashes and house prices hit the floor, people won't have to earn the same money as before to make a living, and they'll begin to compete in the global market. And we surely don't really need the level of material possessions we have now, nice though it can be.

Where I do agree with this Jeremiah, is that a load of fat b*st*rds will have to be trimmed.

Put me down as a hope fiend.

Sunday, April 19, 2009

The deflationary bust

Looking around "Financial Sense"...

Professor Antal E. Fekete revisits his deflationary theory: we have passed a crucial point in debt accumulation. From now (actually, from 2006, he says) onward, the more politicians attempt to stimulate it with debt, the faster the economy will shrink. Gold, the machine's "governor" that set limits to debt, was decoupled from the system a century ago - it got in the way of war financing.

Stephen Tetreault says if there's a rise in stocks, sell: "I do not see a positive bullish catalyst in the making as we head into the earnings sector other than a potential short squeeze, relief rally that should which should be sold into." He notes that deflation means those that can, are paying down debt, but also lenders are widening the margins between the interest they pay and the interest they charge, which gives further impetus to deflation.

Tony Allison says, sooner or later energy is going to cost more. He's thinking about the right point to speculate, the rest of us should consider the effect of higher energy costs on family budgets, and therefore on how reduced disposable income will be allocated.

Captain Hook foresees a time when "the public finally gives up the ghost on stocks in general, correspondingly they will fully embrace the likelihood of deflation, which will trigger a temporary collapse in commodity prices, led by their paper representations." He thinks this will be the time when physical gold will win; I wonder whether that is so, when most of us are so dependent on an electronic system. We're not farmers, selling corn and cattle to each other; the machine cannot be allowed to stop. That's why I think there will be, for a time, a switch to currency inflation; then perhaps a rerun of the early Eighties, as someone public-spirited in public life takes unpopular action to prevent the dive into the abyss.

For E. M. Forster's extraordinarily accurate vision of the future, written in 1909, please click the last link above. Telephone, TV, a populace paralysed by lethargy and wealth in its bedrooms...

Professor Antal E. Fekete revisits his deflationary theory: we have passed a crucial point in debt accumulation. From now (actually, from 2006, he says) onward, the more politicians attempt to stimulate it with debt, the faster the economy will shrink. Gold, the machine's "governor" that set limits to debt, was decoupled from the system a century ago - it got in the way of war financing.

Stephen Tetreault says if there's a rise in stocks, sell: "I do not see a positive bullish catalyst in the making as we head into the earnings sector other than a potential short squeeze, relief rally that should which should be sold into." He notes that deflation means those that can, are paying down debt, but also lenders are widening the margins between the interest they pay and the interest they charge, which gives further impetus to deflation.

Tony Allison says, sooner or later energy is going to cost more. He's thinking about the right point to speculate, the rest of us should consider the effect of higher energy costs on family budgets, and therefore on how reduced disposable income will be allocated.

Captain Hook foresees a time when "the public finally gives up the ghost on stocks in general, correspondingly they will fully embrace the likelihood of deflation, which will trigger a temporary collapse in commodity prices, led by their paper representations." He thinks this will be the time when physical gold will win; I wonder whether that is so, when most of us are so dependent on an electronic system. We're not farmers, selling corn and cattle to each other; the machine cannot be allowed to stop. That's why I think there will be, for a time, a switch to currency inflation; then perhaps a rerun of the early Eighties, as someone public-spirited in public life takes unpopular action to prevent the dive into the abyss.

For E. M. Forster's extraordinarily accurate vision of the future, written in 1909, please click the last link above. Telephone, TV, a populace paralysed by lethargy and wealth in its bedrooms...

Monday, March 30, 2009

The "correction" will come soon

Michael Panzner reminds us that he predicted hyperinflation to follow after deflation, and quoting Edward Chancellor's recent article, thinks the phase change may be on its way. Chancellor answers the argument about global oversupply by reference to run-down inventories, widespread bankruptcies etc - there is now less productive capacity than there was, and what's left is not running smoothly.

A sleep-deprived Jim Kunstler experiences some of this disruption in a Colorado over-dependent on the vagaries of aviation, and rehearses his central theme that US living standards must (in his view) drop 20 to 50 per cent, whether through deflationary depression or savings-destroying inflation. He thinks the page will turn soon, too - maybe in June.

I said to my brother this weekend, that I think America can cope with being poorer, though the adjustment will be nasty; I didn't think it could survive being so rich. Look at what all that easy, phoney, fraudulent wealth did: that gallery of fat rogues in Wall Street and elsewhere, while the poor were exploited with credit cards and doomed home loans.

Kunstler's healing vision is bucolic, like Alexander Pope's:

Another age shall see the golden ear

Imbrown the slope, and nod on the parterre,

Deep harvests bury all his pride has planned,

And laughing Ceres reassume the land.

Friday, January 23, 2009

Very scary

Sunday, November 23, 2008

Bank crashes and the Basel Accords

I need information and understanding - please help me, somebody.

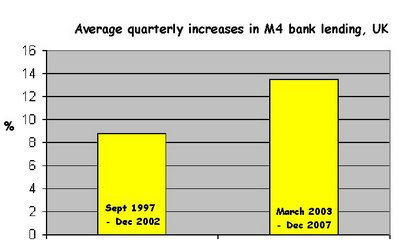

I've pointed out more than once that M4 bank lending in the UK accelerated from 2003 on, and I suspected it was something to do with reducing bank capital adequacy requirements, so the government (via its regulators) would have been implicated. In other words, I've been looking for the villain of the piece, and the smoking gun.

But do you think I can find them?

What I have found so far is references to the Basel Accords, Basel I and Basel II. Basel I became law in the G10 countries including the UK in 1992, and Basel II was published in 2004. The general drift, I understand, is to encourage a uniformity of approach to systemic financial risk, and to introduce a system of risk-weighting bank capital according to what the banks are lending against or investing in. What a success that has proved! Perhaps we should refer to the scheme as "Basel Fawlty".

But can somebody help unpack and simplify what actually happened? Is it, for example, possible that this system was perceived by the banks as a more pliable alternative to fixed minimum reserve ratios, and so they reduced the cash in their vaults to the very least that they could tweak the definitions? For example, we have read many times how mortgage-backed securities are at the heart of the subprime problem, because the packages could be represented as having much less risk than they actually contained.

So is the present crisis an unintended consequence of more elastic international regulation, dating back as far as the early 1990s?

Monday, October 29, 2007

Rapid fire

{kind=link}

Duff McDonald in New York Magazine (Saturday) goes through various doomsters' scenarios. How many bullets can we dodge, especially when the system is becoming automated?

By the way, he says CNBC calls Peter Schiff "Dr Doom" - surely that would be Marc Faber?

Subscribe to:

Posts (Atom)