Our primary concern at this stage is no longer our readers' portfolios but their ability to weather a US dollar crisis if one erupts. In response, we are increasing our gold allocation to 30% and moving all Treasury holdings to the very shortest maturities, to three month Treasury bills, until we see indications that conditions are stabilizing. We encourage you to engage with the community to actively discuss strategies that are appropriate for you.

The rest is here.

Showing posts with label iTulip. Show all posts

Showing posts with label iTulip. Show all posts

Tuesday, February 24, 2009

Thursday, November 20, 2008

The reality goggles are smeared

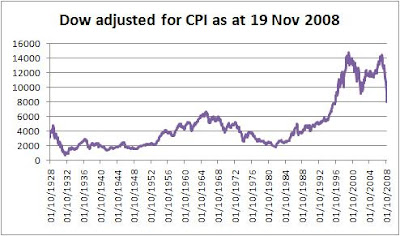

This project of mine is echoed by Eric Janszen of iTulip. His graph and red line suggests what I've been saying recently, that the Dow's trend (if it has one) could be to 6,000 points, with an overshoot to 4,000.

My independently-researched version:

iTulip's:

iTulip's:

My independently-researched version:

iTulip's: It's really hard to see the past in our own terms. I'm trying to do it using the Consumer Price Index, which opens another can of worms about the composition and weighting of that index, especially since (I understand) it affects government statistics and benefits. However, you have to start somewhere.

The first thing to note is how freakish recent years have been. If you connect previous start-of-month highs (August 1929, January 1966) and extended the line, you'd expect the recent Dow highs of 1999 and 2007 to be no more than 10,000 points.

And as for the lows: the drop from 1929 to 1932 was 86% "in real terms"; from 1966 to 1982, 73%; and so far since 1999, 46% - but this last from an amazing historical high. And the 350%-plus American debt-to-GDP ratio is quite unprecedented.

So the history of the last 80 years offers no clear guide as to what could happen next. If proportionately as severe as 1932, the Dow could dive to about 2,100 points; if like 1982, just below 4,000. BUT the second of these great waves crashed rather less than the first, so maybe the third will be even more merciful, perhaps a top-to-bottom fall of only 60%, i.e. end up at c. 5,900.

I note that the Dow has closed tonight at 7,552.29. What a fast fall we've seen - will it spring back sharply and then recommence its decline, as in previous cycles, or is it popping like a balloon?

Methodology

I've noted the Dow as it stood on the first trading day each month, starting October 1928 and ending November 2008 (plus where it stood yesterday - 7.997.28 - since we've seen a further steep fall). Then I've noted the historical CPI as at the end of the previous month in each case. Then, looking at the latest Dow figure, I've adjusted historical Dow figures accordingly (i.e. Dow then/CPI then, times CPI now).

Sources: Dow: Yahoo! Finance; CPI: InflationData.com

UPDATE

iTulip today also reproduces its graph on holdings at the Federal Reserve bank, underscoring the point that the current crisis has features that we can scarcely compare to anything in the last 80 years. Except that it's unlikely to be good news.

Wednesday, October 01, 2008

More from iTulip

Eric Janszen gives us his take on the brouhaha:

This iTulip post describes the process whereby the current deflation may suddenly turn into inflation.

This one warns against Bill-bashing for its own sake, which may be cutting off your nose to spite your face - something must be done, he says, because the market does NOT self-correct. I would suggest that it might, if the government and banks hadn't "intervened" long ago to create a fiat currency. Once that's happened, we're playing the game for the benefit of bankers and politicians, and by their rules.

This iTulip post describes the process whereby the current deflation may suddenly turn into inflation.

This one warns against Bill-bashing for its own sake, which may be cutting off your nose to spite your face - something must be done, he says, because the market does NOT self-correct. I would suggest that it might, if the government and banks hadn't "intervened" long ago to create a fiat currency. Once that's happened, we're playing the game for the benefit of bankers and politicians, and by their rules.

And the solution?

Anyone who saw Brian Cox as Titus Andronicus at the Swan in Stratford in 1987, can never forget it. I remember seeing a girl in the audience with her mouth hanging open, paralysed, as Titus stunned us with his almost gloating description of his suffering. And what a master Shakespeare was, understanding that when emotion is heightened, it is also complex.

TITUS Ha, ha, ha!

MARCUS Why dost thou laugh? It fits not with this hour.

TITUS Why, I have not another tear to shed.

Humour can also unblock the mind to work creatively in a disaster. But there is also the "We're doomed, I tell ye!" John Laurie type who only cheers up when it's as bad as he always said it would be. Watch out for them, because unconsciously, they may steer events to match their temper.

iTulip explains succinctly, below, the problem caused by the house price crash. For me, though, it's a reminder of how wonderful the old cartoons are.

TITUS Ha, ha, ha!

MARCUS Why dost thou laugh? It fits not with this hour.

TITUS Why, I have not another tear to shed.

Humour can also unblock the mind to work creatively in a disaster. But there is also the "We're doomed, I tell ye!" John Laurie type who only cheers up when it's as bad as he always said it would be. Watch out for them, because unconsciously, they may steer events to match their temper.

iTulip explains succinctly, below, the problem caused by the house price crash. For me, though, it's a reminder of how wonderful the old cartoons are.

Saturday, July 12, 2008

The housing bubble: 5 - 12 years to the turn

According to iTulip, we are at Step D in a timetable (published in January 2005) that implies we have quite some years to go before a housing upturn.

Their point about real estate being an illiquid market seems valid to me, and I've suggested before now that we should expect a decline and a long stall, rather than an equity-style crash.

Their point about real estate being an illiquid market seems valid to me, and I've suggested before now that we should expect a decline and a long stall, rather than an equity-style crash.

Thursday, July 03, 2008

Housing: have we reached the "point of maximum pessimism"?

Blanche Evans of Realty Times thinks the most of the bad news in housing has already been built into the market; she was interviewed on iTulip a couple of years ago, predicting a downturn but also saying that housing would be supported by the government, to some extent.

Benjamin Graham said we should “buy from pessimists and sell to optimists”. The smart money has done the second part, maybe it should look out for the first soon.

Benjamin Graham said we should “buy from pessimists and sell to optimists”. The smart money has done the second part, maybe it should look out for the first soon.

Tuesday, April 22, 2008

Quality down, as well as prices up

Good article in iTulip about the symptoms of inflation to watch out for.

Tuesday, July 31, 2007

We need bad times

iTulip has just issued its latest email newsletter - I do suggest you subscribe, especially since it's free.

Their thesis this time is that the Dow will NOT continue to rise much, because the private investor isn't going to come in and be fleeced again. It's not just "once bitten, twice shy" but the fact that money's getting tighter (energy and food costs rising, etc) and the value of assets (especially houses) is in question. On the other hand, iTulip are not doomsters, either.

My view, for what it's worth, is that we have to wait for something unexpected to trigger a real correction, but the sooner it comes, the better. While our governments put off the evil day with borrowing and monetary inflation, our productive capacity is being exported. One firm I know is having an (atypical for here) bumper year; but whereas once their business used to be moving other people's machinery from one site to another, now they're shipping it abroad. How do you make a living if you sell your tools? Even administrators in bankruptcy can't force you to do that. But the economic folly of our rulers can.

In the British Midlands where I live, I've heard engineers complain (like Lewis Carroll's Oysters) about industrial decline ever since I attended a British Association for the Advancement of Science conference in 1977, but our leaders have plodded on, chatting comfortably to each other like the Walrus and the Carpenter, while the Oysters' numbers dwindled. I drive past new man-about-town city centre flats where only 17 years ago I was talking to a self-employed woman turning metal parts. The mighty Longbridge car plant is a broken shell, and the surrounding area is turning over to drugs, alcohol, crime, teenage gangs, domestic abuse and all the rest.

The system continues apparently unaffected, but I think it's a fool's paradise. Only last night, I watched a TV programme about India. The city of Bangalore (home to tech giant Infosys) is modernising and booming; its university aims to attract the world's best. When industry and learning have gone East, what exactly will the West have that anyone could want? We'd better start making it again now, and at a price that our trading partners are willing to pay. Or at least, make sure we have what we need to produce what we consume, as locally as possible.

Yes, currency devaluation means inflation and recession, but better that than a full-on, generation-long depression. We've got to take the nasty-tasting medicine while it can still make a difference. But who will force us to do it?

The US Presidential elections are still a year away, and the new President won't take over until January 2009. In the UK, we have a Prime Minister we didn't elect, who could choose to defer the next General Election right up to 2010. If we're going to get the right people to deal with the heavily-disguised crisis we're in today, the economic issues will have to break out into the open within the next 12 months.

In the meantime, investors must prepare for turbulence.

Their thesis this time is that the Dow will NOT continue to rise much, because the private investor isn't going to come in and be fleeced again. It's not just "once bitten, twice shy" but the fact that money's getting tighter (energy and food costs rising, etc) and the value of assets (especially houses) is in question. On the other hand, iTulip are not doomsters, either.

My view, for what it's worth, is that we have to wait for something unexpected to trigger a real correction, but the sooner it comes, the better. While our governments put off the evil day with borrowing and monetary inflation, our productive capacity is being exported. One firm I know is having an (atypical for here) bumper year; but whereas once their business used to be moving other people's machinery from one site to another, now they're shipping it abroad. How do you make a living if you sell your tools? Even administrators in bankruptcy can't force you to do that. But the economic folly of our rulers can.

In the British Midlands where I live, I've heard engineers complain (like Lewis Carroll's Oysters) about industrial decline ever since I attended a British Association for the Advancement of Science conference in 1977, but our leaders have plodded on, chatting comfortably to each other like the Walrus and the Carpenter, while the Oysters' numbers dwindled. I drive past new man-about-town city centre flats where only 17 years ago I was talking to a self-employed woman turning metal parts. The mighty Longbridge car plant is a broken shell, and the surrounding area is turning over to drugs, alcohol, crime, teenage gangs, domestic abuse and all the rest.

The system continues apparently unaffected, but I think it's a fool's paradise. Only last night, I watched a TV programme about India. The city of Bangalore (home to tech giant Infosys) is modernising and booming; its university aims to attract the world's best. When industry and learning have gone East, what exactly will the West have that anyone could want? We'd better start making it again now, and at a price that our trading partners are willing to pay. Or at least, make sure we have what we need to produce what we consume, as locally as possible.

Yes, currency devaluation means inflation and recession, but better that than a full-on, generation-long depression. We've got to take the nasty-tasting medicine while it can still make a difference. But who will force us to do it?

The US Presidential elections are still a year away, and the new President won't take over until January 2009. In the UK, we have a Prime Minister we didn't elect, who could choose to defer the next General Election right up to 2010. If we're going to get the right people to deal with the heavily-disguised crisis we're in today, the economic issues will have to break out into the open within the next 12 months.

In the meantime, investors must prepare for turbulence.

Saturday, July 14, 2007

More on real inflation figures via iTulip

Further to my post of 9 July re "real" inflation, I have received the following comment from the originator of the charts - thanks.

I am the author of the charts referenced above. For the latest, see here:

http://homepage.mac.com/ttsmyf/RD_RJShomes_PSav.html

http://homepage.mac.com/ttsmyf/recDJIAtoRD.html

http://homepage.mac.com/ttsmyf/newestHousData.gif

FYI, thru today 7/12 for the Real Dow, and thru 2007 Q1 (= mid-Feb 2007) for Real Homes: Real Dow is 2.24x the +1.64 %/yr curve, which is a 55% drop thereto, and Real Homes national (green points) is 1.78x the ca. 54 level, which is a 44% drop thereto.

I am the author of the charts referenced above. For the latest, see here:

http://homepage.mac.com/ttsmyf/RD_RJShomes_PSav.html

http://homepage.mac.com/ttsmyf/recDJIAtoRD.html

http://homepage.mac.com/ttsmyf/newestHousData.gif

{kind=link}

FYI, thru today 7/12 for the Real Dow, and thru 2007 Q1 (= mid-Feb 2007) for Real Homes: Real Dow is 2.24x the +1.64 %/yr curve, which is a 55% drop thereto, and Real Homes national (green points) is 1.78x the ca. 54 level, which is a 44% drop thereto.

Subscribe to:

Posts (Atom)