How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5:

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

When Nixon closed the "gold window" (15 August 1971), gold ceased to be a currency backing and became just another thing you could choose to invest in, so let's compare these assets from a little before that turning-point, onwards:

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

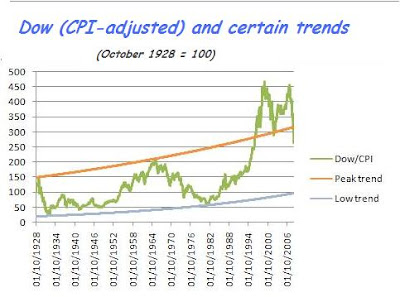

That depends on whether you read this as a statement about gold, or about the Dow. I looked at the Dow in inflation (CPI) terms a while back (December 2008):

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

Back to gold-pricing: it's also notable that the Dow is currently still worth some 8 ounces of gold, but in previous lows (Feb. 1933, March 1980) fell below 2 ounces: So should we still pile into gold, as a hedge against the further collapse of the Dow?

So should we still pile into gold, as a hedge against the further collapse of the Dow?

I think not. Firstly, the Dow may well have a rally, since it's fallen so sharply in such a short time. And secondly, this is missing the point, which is that we are looking to protect wealth against inflation, not against the Dow.

So another question is, how does gold hold its value during periods of price inflation? A period some readers may have lived through, is that after the oil price hike of October 1973. Here is what happened in the 5 years from 1974 to 1978:

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide. The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend: There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.