Following comments on the last post, I see the feeling that scores should be settled is spreading - see Denninger and a threatening post to which he's linked.

UPDATE

And Jim Kunstler, too.

Tuesday, December 23, 2008

Every little thing's gonna be all right

From what I read, some people are becoming survivalist: storing food, water, medicines, cash, even weapons.

Perhaps it's no coincidence that BBC is currently screening a remake of Terry Nation's gripping 1975 post-catastrophe series, "Survivors". But that series assumes that most people have died suddenly because of a virus, so the ecosystem has not been destroyed by desparate, starving victims. I don't think Survivors is the model we should use. If we are to survive, it'll be together, in our populous societies, because if society breaks down, you and I are unlikely to emerge as the last people standing. Lone heroes don't win; this is a fantasy.

I think spare supplies are a good idea, because there could be some disruption, which could affect the very young and elderly; so we need ways to keep warm, eat and have clean water in an emergency. And it's important to make your home secure against a rise in burglary, which is associated with economic downturns; and not to go out after dark without at least one or two companions. Weapons are another matter: "guns in the home are far more likely to be used against members of the household than against intruders."

Pace the doomsters, the UK and the USA will feed itself. We may end up eating more veg and less meat; and we may be using public transport instead of cars; personally, that would simply take me back to the 70s, when I was slimmer and fitter. Globally and locally, there is enough to feed the world, although not enough to overfeed it or encourage unproductive men to sire children.

Two aspects of the current crisis worry me:

1. The present method of organising resources may be replaced, not by one dreamed of by well-fed Western socialists, but by a cruel, remote, commanding elite as in North Korea or East Germany, who far from minimising scarcity will use it to get and maintain power.

2. The transition from this system to whatever replaces it, may be disorderly and involve suffering for many people.

This is why I think the underlying issue for us is to preserve and strengthen democracy, to increase the chances that both the journey and the journey's end are acceptable.

Perhaps it's no coincidence that BBC is currently screening a remake of Terry Nation's gripping 1975 post-catastrophe series, "Survivors". But that series assumes that most people have died suddenly because of a virus, so the ecosystem has not been destroyed by desparate, starving victims. I don't think Survivors is the model we should use. If we are to survive, it'll be together, in our populous societies, because if society breaks down, you and I are unlikely to emerge as the last people standing. Lone heroes don't win; this is a fantasy.

I think spare supplies are a good idea, because there could be some disruption, which could affect the very young and elderly; so we need ways to keep warm, eat and have clean water in an emergency. And it's important to make your home secure against a rise in burglary, which is associated with economic downturns; and not to go out after dark without at least one or two companions. Weapons are another matter: "guns in the home are far more likely to be used against members of the household than against intruders."

Pace the doomsters, the UK and the USA will feed itself. We may end up eating more veg and less meat; and we may be using public transport instead of cars; personally, that would simply take me back to the 70s, when I was slimmer and fitter. Globally and locally, there is enough to feed the world, although not enough to overfeed it or encourage unproductive men to sire children.

Two aspects of the current crisis worry me:

1. The present method of organising resources may be replaced, not by one dreamed of by well-fed Western socialists, but by a cruel, remote, commanding elite as in North Korea or East Germany, who far from minimising scarcity will use it to get and maintain power.

2. The transition from this system to whatever replaces it, may be disorderly and involve suffering for many people.

This is why I think the underlying issue for us is to preserve and strengthen democracy, to increase the chances that both the journey and the journey's end are acceptable.

Monday, December 22, 2008

Why banks?

Banks require re-capitalisation. The capital is required to cover losses. Capital is also needed for assets returning onto their balance sheet (as the vehicles of the “shadow banking system” are unwound). This capital is required to restore bank balance sheets. Additional capital will be needed to support future growth. Availability of capital, high cost of new capital and dilution of earnings will impinge upon future performance.

Satyajit Das (htp: Jesse)

Nope. Banks need destroying, as does all this bank-created debt. The mistake is to try to keep things as they are. How did we come to buy houses "on tick", then cars, and now our clothes and groceries? Why is there any lending for consumption, seeing how it only means reduced future consumption? Why should banks be kept going, requiring a significant proportion of our earnings, so that wages have to be high for us to live on what's left, making us uncompetitive with the developing world?

I am reminded of the pitiless response of the Comte d'Argenson to the satirist, Desfontaines:

Desfontaines: I must live.

D'Argenson : I do not see the necessity.

Satyajit Das (htp: Jesse)

Nope. Banks need destroying, as does all this bank-created debt. The mistake is to try to keep things as they are. How did we come to buy houses "on tick", then cars, and now our clothes and groceries? Why is there any lending for consumption, seeing how it only means reduced future consumption? Why should banks be kept going, requiring a significant proportion of our earnings, so that wages have to be high for us to live on what's left, making us uncompetitive with the developing world?

I am reminded of the pitiless response of the Comte d'Argenson to the satirist, Desfontaines:

Desfontaines: I must live.

D'Argenson : I do not see the necessity.

Sunday, December 21, 2008

The lesser of two weevils

In an apocalyptic - but carefully-reasoned - post, Karl Denninger says that when the deficit expansion stops, US government spending will have to be cut by 50 - 60%, unless there is to be a "general default" on debts.

I have no idea what a general default would look like, but in a closely-interwoven and distant-from-nature modern industrial society I can only fear it might prove utterly destructive. So we're back to contemplating the lesser, but still vast disaster.

I also have no idea how much worse it might be in the UK.

Someone else please read this unberobed OT prophet and tell me where he's wrong.

PS

While the Obama Administration cannot take a 'weak dollar' policy it is the only practical way to correct the imbalances brought about by the last 20 years of systemic manipulation. It is either that, or the selective default on sovereign debt, most likely through conflict, a hot or cold war.

Saturday, December 20, 2008

Christmas viewing

Hilarious new animation in which the daring but accident-prone duo attempt to undo the damage caused by an idiot who sold off half of Britain's gold and let the bankers blow up the economy. From the makers of "The Wrong Assets" and the full-length "The Curse Of The Weird Scotsman".

Hilarious new animation in which the daring but accident-prone duo attempt to undo the damage caused by an idiot who sold off half of Britain's gold and let the bankers blow up the economy. From the makers of "The Wrong Assets" and the full-length "The Curse Of The Weird Scotsman".How will the future look?

Thanks to the glacial catchup by the mainstream media, the public is finally worrying about economic depression, and consoling itself with the thought that we've messed it up for everyone, so at least the Chinese won't prosper and come over here as tourists, overdressed, overpaid and taking too many pictures for their digital photoframes at home.

Thanks to the glacial catchup by the mainstream media, the public is finally worrying about economic depression, and consoling itself with the thought that we've messed it up for everyone, so at least the Chinese won't prosper and come over here as tourists, overdressed, overpaid and taking too many pictures for their digital photoframes at home. Short-sighted, I think. On the CapitalistsatWork blog, I comment:

I think we should turn our eyes, not on the Depression, but how things will look afterwards. The East will generate demand as it aspires to the lifestyle we used to enjoy, and meantime we have been allowing them to transfer the means of production to their co-prosperity sphere. So the Chinese factories will re-open, perhaps after some of the light industry has relocated to Thailand, the poorer parts of India, and other neighbouring regions?

And I shouldn't discount India as potentially the real industrial powerhouse of the 21st Century, while China scrabbles about annexing territory for extra lebensraum, water and wood.

I think, by the way, that econinvestguru Marc Faber took up residence in Chiang Mai, northern Thailand, not to pursue a monastic existence (hardly characteristic of the formerly ponytailed playboy), but because he's close to "where it's at", or even better (and typical of this farsighted man), where it will be.

Friday, December 19, 2008

Europe is keeping China (and America) going

A very interesting piece by Brad Setser, where he shows that the EU's currency strength and growing imports from China have offset the levelling in demand from America. His bottom line is that China's making money from us and lending it to the US.

Default

I relayed Jesse's comments on Ecuador's moves to default here on November 28th, and now it's happened. Any big ones coming, do you think?

Wednesday, December 17, 2008

The seventh seal

Denninger's question:

With the $7 trillion dollars we have committed we could have literally given every homeowner with a mortgage a fifty percent reduction in the principal outstanding.

This would have instantaneously stopped all of the foreclosures by putting all (essentially) homes into positive equity - overnight!

So why wasn't this done?

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.

This is the fourth horseman of the financial apocalypse that Michael Panzner predicted, as summarized here on Bearwatch on May 10, 2007.

UPDATE: Jesse comments on another fresh sum - tens of billions - needed to cover AIG's losses. As he says, there is an air of expectancy; but also of unreality, like the announcement of a major war.

With the $7 trillion dollars we have committed we could have literally given every homeowner with a mortgage a fifty percent reduction in the principal outstanding.

This would have instantaneously stopped all of the foreclosures by putting all (essentially) homes into positive equity - overnight!

So why wasn't this done?

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.

His answer: the government is trying to cover the staggering bets of the derivatives market. With borrowed money. The Treasury has swallowed the grenade and put its fingers in its ears.This is the fourth horseman of the financial apocalypse that Michael Panzner predicted, as summarized here on Bearwatch on May 10, 2007.

UPDATE: Jesse comments on another fresh sum - tens of billions - needed to cover AIG's losses. As he says, there is an air of expectancy; but also of unreality, like the announcement of a major war.

Inappropriate gloat

I came to the US fresh out of university, and went to graduate school. Consequently, I was mostly oblivious to the details of 'real life', like taxes, bills and repairs.

Working my way into the system, it all seemed that it couldn't possibly work: too many people with no discernible talent were earning too much, and prices were lower than I thought they should be, particularly fuel prices. I thought the problem was that I wasn't intelligent enough, and just didn't understand.

The one personal satisfaction that I can get from the current mess is that I was right - it doesn't make sense.

Working my way into the system, it all seemed that it couldn't possibly work: too many people with no discernible talent were earning too much, and prices were lower than I thought they should be, particularly fuel prices. I thought the problem was that I wasn't intelligent enough, and just didn't understand.

The one personal satisfaction that I can get from the current mess is that I was right - it doesn't make sense.

WeaselWordWatch update: "Quantitative Easing"

Okay, it's a phrase, not a word. But 4,094 references on Google News in the last 24 hours. And Mish is at it, too, though of course in an ironic way.

On yer bike

Thus Denninger:

Bernanke clearly thinks ... that he can "restart borrowing." ... This is causing the dollar to get slammed - at least for a little while... These sorts of actions ignite wars. Choose between a trade war (about 75% chance) and a shooting war (the other 25%).

The dollar weakness, by the way, won't last. Either sort of war puts every other nation in the world in worse shape than us, which over time leads to the same place - "we're screwed but they're screwed worse."

He's not wrong. Total US debt, foreign and domestic, has recently been calculated as 392% of GDP; but alas for us Brits, UK external (foreign) debt alone is running at 400%. I just don't know what a like-for-like comparison would show.

The TV news here tried to put a merry gloss on sterling's collapse, reporting how it helps exporters like a bicycle firm they visited. A bit desperate: the start of the 'Oxford Automobile and Cycle Agency’, this isn't. You know you're in trouble when they tell you to "smile, smile, smile."

Tuesday, December 16, 2008

Unstoppable

From an engineering standpoint, I think that this crisis was unavoidable. Once we de-coupled the concept of wealth from production, we generated a positive-feedback loop. The profits from manipulating money were greater than could be made in manufacturing, and so even more money flowed in.

I cannot help but think of Douglas Adams' 'Shoe Event Horizon', where eventually every shop becomes a shoe shop.

I cannot help but think of Douglas Adams' 'Shoe Event Horizon', where eventually every shop becomes a shoe shop.

The answer is blowing in the wind

I said on Friday, "I think 2008 will be seen in retrospect as the year that the global balance of power underwent a sudden tectonic shift, from West to East." I forgot to add, "...and from North to South, too"; but Michael Panzner is not alone in seeing America's exclusion from the Brazilian summit as a straw in the wind.

In the news

Conservative leader David Cameron is making noises about prosecuting crooked bankers. Nice to see he's getting with my program.

Also in the Daily Mail, Alex Brummer says Madoff has queered the pitch for hedge funds generally. Damn: I had started to look at how to set one up, using links supplied by Jim from San Marcos. If I'd started a couple of years ago, I'd have got everyone into cash and made a packet for them and myself. 2 and 20, 2 and 20.

Odds on the bankers and hedgies Getting Away With It? Pretty fair, I'd have thought - especially when you bear in mind (as Denninger points out - and Jesse, too) all the others who could be implicated. To quote Oscar Wilde: "The good ended happily, and the bad unhappily. That is what fiction means."

Also in the Daily Mail, Alex Brummer says Madoff has queered the pitch for hedge funds generally. Damn: I had started to look at how to set one up, using links supplied by Jim from San Marcos. If I'd started a couple of years ago, I'd have got everyone into cash and made a packet for them and myself. 2 and 20, 2 and 20.

Odds on the bankers and hedgies Getting Away With It? Pretty fair, I'd have thought - especially when you bear in mind (as Denninger points out - and Jesse, too) all the others who could be implicated. To quote Oscar Wilde: "The good ended happily, and the bad unhappily. That is what fiction means."

Monday, December 15, 2008

On Competitiveness

Consider a group of players in a game of chance. If all conditions are equal, the long-term results will be randomly distributed, with some big winners, and some big losers.

Change the conditions so that some players have an advantage, and eventually those players will be the only winners. How long this takes depends on the size of the advantage.

This is the basis of the mutation and natural selection portion of evolution theory.

For a generation after World War II, the US had a huge advantage: capital, undamaged manufacturing capacity, cheap energy, and most of the scientists and engineers. Thus, we 'won' the economic game, and it was attributed to Americans being 'better'.

We failed to notice that many other nations were catching up in education and technology. That the government and industry chose to dis-invest in research in the 1980's just accelerated the process.

As the playing field is now level (or even tipped against us), we should carefully consider how to gain back that advantage. We have done so before in the short term: arming in World War II, the Manhattan Project, the Space Race.

Do we have the will to do this when not faced with war, but with long-term economic decline?

Change the conditions so that some players have an advantage, and eventually those players will be the only winners. How long this takes depends on the size of the advantage.

This is the basis of the mutation and natural selection portion of evolution theory.

For a generation after World War II, the US had a huge advantage: capital, undamaged manufacturing capacity, cheap energy, and most of the scientists and engineers. Thus, we 'won' the economic game, and it was attributed to Americans being 'better'.

We failed to notice that many other nations were catching up in education and technology. That the government and industry chose to dis-invest in research in the 1980's just accelerated the process.

As the playing field is now level (or even tipped against us), we should carefully consider how to gain back that advantage. We have done so before in the short term: arming in World War II, the Manhattan Project, the Space Race.

Do we have the will to do this when not faced with war, but with long-term economic decline?

The elephant in the room?

In 'Great Expectations', Charles Dickens wrote: "Annual income 20 pounds, annual expenses twenty pounds and sixpence, result misery" (or words to that effect).

In the 1960's, the US undertook an orgy of spending on the Great Society and the Cold War (including the Vietnam War and Space Race). At the same time, the typical middle-class American lived an extravagant lifestyle, relatively speaking. This was all fueled by cheap American oil, gas and coal.

By 1973, we had used so much that OPEC had us over a barrel, and by 1975 we had our first large trade deficits, which have grown every year.

Since about 1980, not much has come out of our industry that the rest of the world seems to want to buy.

Did we go broke 30 years ago, and are just now noticing it?

In the 1960's, the US undertook an orgy of spending on the Great Society and the Cold War (including the Vietnam War and Space Race). At the same time, the typical middle-class American lived an extravagant lifestyle, relatively speaking. This was all fueled by cheap American oil, gas and coal.

By 1973, we had used so much that OPEC had us over a barrel, and by 1975 we had our first large trade deficits, which have grown every year.

Since about 1980, not much has come out of our industry that the rest of the world seems to want to buy.

Did we go broke 30 years ago, and are just now noticing it?

There's more truth in humour ...

Today's 'Non Sequitur' cartoon strip:

C.E.O. talking in his palatial office talking to a man with a wrench in his hand:

"We crunched the numbers over and over on where we could cut back, and it kept coming down to whatever it is you guys do on the assembly line..."

C.E.O. talking in his palatial office talking to a man with a wrench in his hand:

"We crunched the numbers over and over on where we could cut back, and it kept coming down to whatever it is you guys do on the assembly line..."

In a nutshell

London Banker sums up what went wrong over the past 25 years, in 1,610 words. It's a reprint from May, but he's right to show it again: it pretty much says it all.

Those who are old enough may remember having to do a precis in English. This is a very valuable, rational, intellectual exercise, which perhaps is one of the reasons it was ditched in New Teaching.

Do you think you could distil LB's observations in, say, 600 words?

Those who are old enough may remember having to do a precis in English. This is a very valuable, rational, intellectual exercise, which perhaps is one of the reasons it was ditched in New Teaching.

Do you think you could distil LB's observations in, say, 600 words?

Saturday, December 13, 2008

Two cheers for deflation

A pattern is emerging.

Jörg Guido Hülsmann, on the Mises site, says deflation does not ruin the economy as a whole, but destroys the parasites who exploit the potential of fiat money. Parasites like (alleged) Ponzi-style fraudster Madoff and his clients, who deserve what they've now got, Mish judges.

Jesse says that "financial capitalism" seeks to use the money system to develop a dictatorial New World Order, and will be defeated when the dollar fails as the world's reserve currency.

Brad Setser wonders whether the dollar has reached its zenith; which implies that it may begin heading for its nadir.

Desperately holding back the inevitable is the US Federal Reserve, says Jim from San Marcos, who (although the Fed is refusing FOI requests) suspects that its $2 trillion in emergency loans is equally divided between support for banks, credit cards and the stockmarket. (I wondered what was being used as the robust cloth on the Dow's trampoline, and covert official support may be the answer.)

As I argued yesterday, the straightest path would be to destroy fraudulent, oppressive debt and those who introduced it into the system. For so many families, the bank is the fattest kid at their kitchen table, and nobody knows who invited him.

For a long time, I've been recasting financial issues as issues of power and freedom. If Jesse is correct, we are reaching a turning point in the battle. I hope we may soon say, as Churchill said of El Alamein, "A bright gleam has caught the helmets of our soldiers and warmed and cheered all our hearts." It would be worth the blood, toil, tears and sweat.

Jörg Guido Hülsmann, on the Mises site, says deflation does not ruin the economy as a whole, but destroys the parasites who exploit the potential of fiat money. Parasites like (alleged) Ponzi-style fraudster Madoff and his clients, who deserve what they've now got, Mish judges.

Jesse says that "financial capitalism" seeks to use the money system to develop a dictatorial New World Order, and will be defeated when the dollar fails as the world's reserve currency.

Brad Setser wonders whether the dollar has reached its zenith; which implies that it may begin heading for its nadir.

Desperately holding back the inevitable is the US Federal Reserve, says Jim from San Marcos, who (although the Fed is refusing FOI requests) suspects that its $2 trillion in emergency loans is equally divided between support for banks, credit cards and the stockmarket. (I wondered what was being used as the robust cloth on the Dow's trampoline, and covert official support may be the answer.)

As I argued yesterday, the straightest path would be to destroy fraudulent, oppressive debt and those who introduced it into the system. For so many families, the bank is the fattest kid at their kitchen table, and nobody knows who invited him.

For a long time, I've been recasting financial issues as issues of power and freedom. If Jesse is correct, we are reaching a turning point in the battle. I hope we may soon say, as Churchill said of El Alamein, "A bright gleam has caught the helmets of our soldiers and warmed and cheered all our hearts." It would be worth the blood, toil, tears and sweat.

Friday, December 12, 2008

History repeats itself - because it's getting old

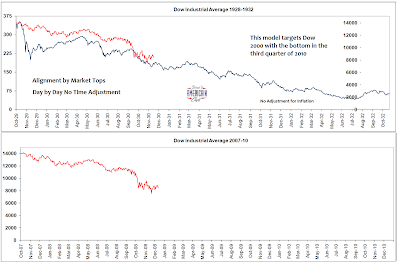

Jesse extrapolates the Dow and sees it heading for 2,000 points:

As my select and distinguished readers now know, I'm an optimist (by the standards of unfolding reality), and I say, not so. I say, maybe 4,000 - 5,000, adjusted for CPI.

The comparison I'd urge is not with 1929-32 (stockmarket deflation exacerbated by monetary strictness), but (in inflation-adjusted terms) from January 1966 to July 1982: stockmarket deflation prolonged and partially disguised by monetary inflation; I said so here and here, last month. I maintain that the bear market began in 2000 and the symptoms were masked by the terrible extra debts taken on over the last 8 years. Karl Denninger showed us yesterday that these debts account for all the US GDP growth since the New Millennium, plus $9 trillion.

The debate about inflation and deflation continues, though from a British perspective we've seen practically the whole of the rest of the world become one-third more expensive in sterling terms, in only five months. However, Einstein's theory of relativity rejects the notion of any absolute standpoint, and we shall see next year which other currencies mimic sterling's vertiginous fall.

In these shifting times, it becomes very hard to discern real value; but however hard to measure, it exists nevertheless. There is a real bill to pay for our excesses, and I think 2008 will be seen in retrospect as the year that the global balance of power underwent a sudden tectonic shift, from West to East. Yes, the East will suffer for a while, too, but it has long been acquiring the means of production and developing its local markets, and will emerge from the crisis ahead of us.

And there will also - must also - be an intergenerational shift of power, within our Western societies. As globalization continues and real income and real house prices decline, existing debt (set in fixed terms) will become proportionately greater, until the weight is too great to bear; and the worst of it falls on the people who are also struggling to raise families and save something, however inadequate, for their old age. They cannot be crucified in this way. How can savers be taxed at 20% and workers at (effectively, on margin, including National Insurance) 40%? Real wealth must flow from one to the other, just to maintain civilization. I think either savings must be taxed more (perhaps the removal of tax exemption for some savings products will be the start), or inflation must come, though I don't know how long the play will go on before the denouement.

We did have another option, and I was only half-joking: cancel mortgage debts on a massive scale (bankrupting the banks and the bankers, and serve them right). Then, with our productive populace relatively unencumbered, it would be possible to let Western wages and prices fall to much nearer Eastern levels, and we could begin to compete.

As my select and distinguished readers now know, I'm an optimist (by the standards of unfolding reality), and I say, not so. I say, maybe 4,000 - 5,000, adjusted for CPI.

The comparison I'd urge is not with 1929-32 (stockmarket deflation exacerbated by monetary strictness), but (in inflation-adjusted terms) from January 1966 to July 1982: stockmarket deflation prolonged and partially disguised by monetary inflation; I said so here and here, last month. I maintain that the bear market began in 2000 and the symptoms were masked by the terrible extra debts taken on over the last 8 years. Karl Denninger showed us yesterday that these debts account for all the US GDP growth since the New Millennium, plus $9 trillion.

The debate about inflation and deflation continues, though from a British perspective we've seen practically the whole of the rest of the world become one-third more expensive in sterling terms, in only five months. However, Einstein's theory of relativity rejects the notion of any absolute standpoint, and we shall see next year which other currencies mimic sterling's vertiginous fall.

In these shifting times, it becomes very hard to discern real value; but however hard to measure, it exists nevertheless. There is a real bill to pay for our excesses, and I think 2008 will be seen in retrospect as the year that the global balance of power underwent a sudden tectonic shift, from West to East. Yes, the East will suffer for a while, too, but it has long been acquiring the means of production and developing its local markets, and will emerge from the crisis ahead of us.

And there will also - must also - be an intergenerational shift of power, within our Western societies. As globalization continues and real income and real house prices decline, existing debt (set in fixed terms) will become proportionately greater, until the weight is too great to bear; and the worst of it falls on the people who are also struggling to raise families and save something, however inadequate, for their old age. They cannot be crucified in this way. How can savers be taxed at 20% and workers at (effectively, on margin, including National Insurance) 40%? Real wealth must flow from one to the other, just to maintain civilization. I think either savings must be taxed more (perhaps the removal of tax exemption for some savings products will be the start), or inflation must come, though I don't know how long the play will go on before the denouement.

We did have another option, and I was only half-joking: cancel mortgage debts on a massive scale (bankrupting the banks and the bankers, and serve them right). Then, with our productive populace relatively unencumbered, it would be possible to let Western wages and prices fall to much nearer Eastern levels, and we could begin to compete.

I prefer Alexander's handling of the Gordian knot, to Gordon Brown's. For me, debt forgiveness is the way; but that's too radical, it seems. Instead, inflation will have to diminish the real value of debt, but jerkily, as the debt-holders periodically jack up interest rates in a fighting retreat. All to hide from reality. "Oh, what a tangled web we weave..."

The US economy in a nutshell

"Wages are sticky downward": American car workers are still trying to fight gravity, i.e. globalization's effect on wage rates. Denninger think that if it's anything more than a bargaining ploy, it will finish most of the US car industry.

And after them? Who else could have their work outsourced? White-collar workers should not look on unconcerned. Save money while you can, while wages are still ahead of minimum spending requirements.

Meanwhile, up in the clouds, a hedge fund manager has (allegedly) admitted his business was a fraud, losing $50 billion; more than three times the car-makers' bailout fund currently under discussion.

And after them? Who else could have their work outsourced? White-collar workers should not look on unconcerned. Save money while you can, while wages are still ahead of minimum spending requirements.

Meanwhile, up in the clouds, a hedge fund manager has (allegedly) admitted his business was a fraud, losing $50 billion; more than three times the car-makers' bailout fund currently under discussion.

How we got here? [by Paddington]

In my opinion, the boom and bust cycles of the past 30 years or so reflect the deep denial of the real world from our leaders in business, government and education.

Much of that is due to the dearth of quantitative and scientific influence on decision-making. President Bush even down-graded the science advisor from the Cabinet.

For decades, students in the US and UK have avoided mathematics, science and engineering. Becoming a teacher meant getting an education degree, rather than knowledge of any particular discipline, as if the skills of teaching were at some mystical higher level than mere content. In business schools, students shunned accounting and finance, and flocked to management and marketing, as the former required too much mathematics and computer knowledge.

This meant a whole generation of managers unable to make decisions based on facts.

Managers in business are brothers under the skin with bureaucrats in government, and the administrators in education, all of whom make wild assertions and demands of subordinates that are completely at odds with reality.

Much of that is due to the dearth of quantitative and scientific influence on decision-making. President Bush even down-graded the science advisor from the Cabinet.

For decades, students in the US and UK have avoided mathematics, science and engineering. Becoming a teacher meant getting an education degree, rather than knowledge of any particular discipline, as if the skills of teaching were at some mystical higher level than mere content. In business schools, students shunned accounting and finance, and flocked to management and marketing, as the former required too much mathematics and computer knowledge.

This meant a whole generation of managers unable to make decisions based on facts.

Managers in business are brothers under the skin with bureaucrats in government, and the administrators in education, all of whom make wild assertions and demands of subordinates that are completely at odds with reality.

Thursday, December 11, 2008

Toll me back from thee to my sole Self

Just caught a minute of BBC1's Question Time, chaired by the garrulous and self-regarding David Dimbleby. Self-regarding literally, this time, as he watched Will Self lay into the career-crazy fascists of New Labour, who now propose to persecute the unemployed after a decade of encouraging them to remain on benefit. As he says, they had the time, the money and the ideology to sort it out, and they didn't do it; and in some damningly characteristic way, they're slapping people who are down already. Lethal. I may have to start liking the white-nosed sleazebag, after all.

His target is the type who may not have realized that they were driving David Kelly to suicide, but probably don't much care that they did, so long as the trail was brushed. My only concern is that the public generally may be starting to feel as I do, in which case we are entering dangerous territory.

His target is the type who may not have realized that they were driving David Kelly to suicide, but probably don't much care that they did, so long as the trail was brushed. My only concern is that the public generally may be starting to feel as I do, in which case we are entering dangerous territory.

Bookends: deflation and inflation

On one side, the redoubtable Mish scorns those who think inflation is a clear and present danger:

On one side, the redoubtable Mish scorns those who think inflation is a clear and present danger:...Those who think inflation is about prices alone were busy shorting treasuries, and looking the wrong direction for over a year. Only after the stock market fell 50% and gasoline prices crashed did the media start picking up on "deflation". Only those who knew what a destruction in credit would do to jobs, to lending, to retail sales, to the stock market, to corporate bond yields and to treasury yields got it right...

Those who stick to a monetary definition of inflation pointing at M3, MZM, base money supply, or even Money AMS, are selecting a definition that makes absolutely no practical sense. Worse yet they do it screaming about bond-bubbles at yields of 5% or higher, all because they refuse to see or admit the destruction of credit is happening far faster than the Fed is printing...

The trick now is to figure out how long deflation will last, not whether we are in it. Humpty Dumpty is of no use, he cannot even see where we are.

On the other end, Jesse recalls Moscow in 1997, before the currency popped:

...They were desperate times, and you could see that there was a climactic crisis coming. It is easy to talk about this sort of thing, a thousand to one devaluation of your home currency, but harder to understand the impact. Imagine that you have $500,000 in savings for your retirement. Now imagine that within two years it is effectively reduced to $5,000 or less, and you will understand how disconcerting a currency crisis can be.

If you don't think a financial panic is possible here in the US, just take a look at the negative returns on short term T bills, and you will get a taste of the leading edge.

One of the best descriptions of the Weimar experience I have ever read was by Adam Fergusson titled "When Money Dies: The Nightmare of the Weimar Collapse." It is notoriously difficult to obtain, but it does the best job in describing how a currency collapse can come on like a lightning strike, although in retrospect everyone could have seen it coming. Denial is a strong narcotic. People believe in their institutions and ignore history until they are staring on the edge of the abyss.

I was right, but I didn't know why

Karl Denninger crunches the numbers: in the last 8 years, US GDP has increased by $14 trillion, but debts by $23 trillion, so effectively accounting for all the GDP growth in that time and still leaving a deficit of $9 trillion...

... we haven't had an expansion in GDP over the last eight years. Congress and its organs of reporting economic "facts" have lied. We have in fact actually seen about a 10% contraction in real GDP from 2000 levels; all of the so-called "expansion" of the Bush Administration has been a lie intended to prevent recognition and working through of the recession that should have happened in 2000.

Now, I sensed this during the last 8 years and felt it coming before then, and have recently said so several times. I'm only grateful that technical whizzes like Karl have managed to spell it out. If only we had taken our lumps after the technology bust of 2000.

... we haven't had an expansion in GDP over the last eight years. Congress and its organs of reporting economic "facts" have lied. We have in fact actually seen about a 10% contraction in real GDP from 2000 levels; all of the so-called "expansion" of the Bush Administration has been a lie intended to prevent recognition and working through of the recession that should have happened in 2000.

Now, I sensed this during the last 8 years and felt it coming before then, and have recently said so several times. I'm only grateful that technical whizzes like Karl have managed to spell it out. If only we had taken our lumps after the technology bust of 2000.

What went wrong? A post-match analysis of the Credit Crunch

Jesse quotes Joseph Stiglitz, and summarises five key moments:

1. Reagan's nomination of Alan Greenspan to replace Paul Volcker as Fed Chairman

2. The Repeal of Glass-Steagall and the Cult of Self-Regulation

3. Bush Tax Cuts for Upper Income Individuals, Corporations, and Speculation

4. Failure to Address Rampant Accounting Fraud Driven by Excessive and Flawed Compensation Models

5. Providing Enormous Bailouts to the Banks without Engaging Systemic Reform for the Underlying Causes of the Failure

1. Reagan's nomination of Alan Greenspan to replace Paul Volcker as Fed Chairman

2. The Repeal of Glass-Steagall and the Cult of Self-Regulation

3. Bush Tax Cuts for Upper Income Individuals, Corporations, and Speculation

4. Failure to Address Rampant Accounting Fraud Driven by Excessive and Flawed Compensation Models

5. Providing Enormous Bailouts to the Banks without Engaging Systemic Reform for the Underlying Causes of the Failure

Rude, funny, true

A near-the knuckle piece from The Onion, illustrating why education is a challenge. The combination of idiot argot and po-faced journalistic style is almost Wodehousian. (htp: Paddington)

Wednesday, December 10, 2008

Barefoot businesses

Many years ago, China pioneered the idea of "barefoot doctors": cheap physicians with a bagful of the most commonly prescribed medicines, providing a low-cost service to the many. This blog thinks the days of glitzy steel-and chrome offices and hot and cold running secretaries are numbered; the model of the future is the pavement stall and the home garage.

(htp: Jesse)

(htp: Jesse)

Heart of Darkness

My news aggregator has picked up news of a startling new discovery, though I fear some details may have been scrambled during transmission:

There is a giant financial black hole at the centre of our finances, a study has confirmed.

Austrian cashtronomers tracked the movement of dozens of banks circling the centres of Western economies.

The black hole in each is the equivalent of four million jobs.

Black holes are obligations whose interest is so great that nothing - including charismatic political leaders - can escape them.

According to experts, the results suggest that thriving economies form around giant debts in the way that a pearl forms around grit.

Treasury ministers on both sides of the Atlantic say that there is no reason to be concerned: provided enough cash is directed into the black holes, they will fill up and the economy will continue to revolve as normal.

Austrian cashtronomers tracked the movement of dozens of banks circling the centres of Western economies.

The black hole in each is the equivalent of four million jobs.

Black holes are obligations whose interest is so great that nothing - including charismatic political leaders - can escape them.

According to experts, the results suggest that thriving economies form around giant debts in the way that a pearl forms around grit.

Treasury ministers on both sides of the Atlantic say that there is no reason to be concerned: provided enough cash is directed into the black holes, they will fill up and the economy will continue to revolve as normal.

Here we go

Jesse interprets the Federal Reserve's request to issue its own debt, as a preparation for selective default on public debt issued by the Treasury.

Now then, cheat China (pop. 1.3 billion, army personnel 2.3 million)- or the UK (pop. 61 million, army personnel 100,000)? Tough call...

Now then, cheat China (pop. 1.3 billion, army personnel 2.3 million)- or the UK (pop. 61 million, army personnel 100,000)? Tough call...

Tuesday, December 09, 2008

Time Management [Guest post by Paddington]

For decades, much was made of the fact that American workers were the most productive of the Western world. Business articles derided the 35-hour work week of the French and Germans.

However, about 10 years ago, there was a study that showed that the French and German workers were much more productive per hour.

This supports my long-held belief that a typical worker averages 6-7 hours of productive work per day. Give them a short-term project and they will work harder and faster, but be less productive afterwards. Tell them that they are going to work overtime, and they will not work as hard in the regular day. Presented with too much work (for them), many will actually do less.

Realizing this is one of the things that has made my job (university teaching) better. I could do my work in less time, so that I had time for myself and my family, rather than twiddling my thumbs at my desk for 8 hours.

In short, people need time to goof off and socialize, and it makes them work better.

However, about 10 years ago, there was a study that showed that the French and German workers were much more productive per hour.

This supports my long-held belief that a typical worker averages 6-7 hours of productive work per day. Give them a short-term project and they will work harder and faster, but be less productive afterwards. Tell them that they are going to work overtime, and they will not work as hard in the regular day. Presented with too much work (for them), many will actually do less.

Realizing this is one of the things that has made my job (university teaching) better. I could do my work in less time, so that I had time for myself and my family, rather than twiddling my thumbs at my desk for 8 hours.

In short, people need time to goof off and socialize, and it makes them work better.

Bide-a-Wii

The West is worrying about indebtedness and global competition, and China is devaluing the renminbi to maintain its trading advantage.

It's time for electronic warfare. Not hacking into the military system - that's so obvious, and it was so uncharacteristically direct of the Chinese to do it. No, I think the counterattack is through computer games.

Fund the provision of PSPs, Xboxes, Wiis and a host of absorbing games (e.g. Morrowind, Gears of War) as pseudo-benevolent gifts to bright young Chinese kids. With any luck, the effect will be the same as here: early, heavy adoption by the ASD/OCD types who might otherwise become the core of the mathematics/engineering/science elite that keep the rest of the population warm, well-fed and protected against disease.

If that doesn't work, only power cuts can save us.

Monday, December 08, 2008

WeaselWordWatch: "Quantitative Easing"

Google references now 177,000 (up from 159,000 yesterday); 1,663 news references in the last 24 hours.

Excuse me while I quantitatively ease a balloon, then stick a pin into it for a non-gradual relaxation.

Excuse me while I quantitatively ease a balloon, then stick a pin into it for a non-gradual relaxation.

The MSM take up the punishment theme

Nassim Taleb and Pablo Triana echo my call for condign punishment for the white-collar thieves.

Sunday, December 07, 2008

Worrying about the wrong things

We teach regularly in schools about drugs, guns and gangs... actually, the real threats to life - that we can do something about -are much less dramatic:

I packed in smoking over 30 years ago - but this coming year, I'd better do something about the weight.

I packed in smoking over 30 years ago - but this coming year, I'd better do something about the weight.

I packed in smoking over 30 years ago - but this coming year, I'd better do something about the weight.

You know you're in trouble when...

... they give a new name to an old crime, in this case, dubbing inflation "quantitative easing".

This phrase yielded an estimated 159,000 results on Google today; watch for imminent "Google result hyperinflation" with respect to this weaselly term. Sackerson is offering a prize for the first sighting of a cartoon in the MSM featuring it.

P.S. 3,210 Google-found news items have it (all dates); 970 in the past month but 1,619 in the last day (how does that statfreak happen?) The earliest news reference found via Google is July 1, 1995 - relating to China's commercial bank reform. A Communist plot, then!

Death to the paper tigers! We demand only tigers with intrinsic value!

This phrase yielded an estimated 159,000 results on Google today; watch for imminent "Google result hyperinflation" with respect to this weaselly term. Sackerson is offering a prize for the first sighting of a cartoon in the MSM featuring it.

P.S. 3,210 Google-found news items have it (all dates); 970 in the past month but 1,619 in the last day (how does that statfreak happen?) The earliest news reference found via Google is July 1, 1995 - relating to China's commercial bank reform. A Communist plot, then!

Death to the paper tigers! We demand only tigers with intrinsic value!

The free market and redistribution of wealth

Jesse argues the free market case: interventions just make things worse; real wages in Western economies must decline; international currencies must float freely.

Okay, if we also have some other system of supporting our workers through the change, instead of import tariffs and other protectionist measures. You can't drop masses of people from a great height and expect society to remain stable.

A lot of our present arrangements - health, education, welfare - seem to me to be a fairly inefficient way of transferring wealth from the upper strata to the lower, less the cost and inconvenience of all the system servicers in between.

Why don't we get honest and open about the need for wealth redistribution, balanced with the need to encourage enterprise? Could we get rid of weaselly taxes and insidious benefit traps? All we need is some way of levelling the playing field between groups of workers in very different parts of the world, in such a way as not to force the game to be abandoned by either side. Can anyone propose a system of financial support - could some form of the Citizens' Basic Income be made to work?

Okay, if we also have some other system of supporting our workers through the change, instead of import tariffs and other protectionist measures. You can't drop masses of people from a great height and expect society to remain stable.

A lot of our present arrangements - health, education, welfare - seem to me to be a fairly inefficient way of transferring wealth from the upper strata to the lower, less the cost and inconvenience of all the system servicers in between.

Why don't we get honest and open about the need for wealth redistribution, balanced with the need to encourage enterprise? Could we get rid of weaselly taxes and insidious benefit traps? All we need is some way of levelling the playing field between groups of workers in very different parts of the world, in such a way as not to force the game to be abandoned by either side. Can anyone propose a system of financial support - could some form of the Citizens' Basic Income be made to work?

Saturday, December 06, 2008

What is "Common Purpose"?

Googling this term, one gets (a) lots of stuff by Common Purpose and/or a Julia Middleton, (b) lots of favourable stuff about either or both, and (c) a handful of snarling "stop-them" sites. I shouldn't bother asking any more, except it seems that this organisation does have connexions with many influential people and organizations.

What is the "Common Purpose" of the eponymous outfit? Who exactly is this Julia Middleton, and why has she become so apparently prominent? Is it a McKinsey-type thing, or a McCarthy-type thing? Can anyone who isn't obviously a nutter tell me, in cool and rational terms?

What is the "Common Purpose" of the eponymous outfit? Who exactly is this Julia Middleton, and why has she become so apparently prominent? Is it a McKinsey-type thing, or a McCarthy-type thing? Can anyone who isn't obviously a nutter tell me, in cool and rational terms?

And as for the D-word...

The Economist Intelligence Unit democracy index has moved the UK up from 23rd place in 2006 to 21st place in 2008. Of course, this was before the government started nationalising the banks and arresting the Opposition.

Even so, the Civil Liberties strand has fallen in two years from 9.12 to 8.82; and the competition seems to be weakening anyway, as the 2008 report notes:

...following a decades-long global trend in democratisation, the spread of democracy has come to a halt. Comparing the results for 2008 with those from the first edition of the index, which covered 2006, shows that the dominant pattern in the past two years has been stagnation. Although there is no recent trend of outright regression, there are few instances of significant improvement. However, the global financial crisis, resulting in a sharp and possibly protracted recession, could threaten democracy in some parts of the world.

Even so, the Civil Liberties strand has fallen in two years from 9.12 to 8.82; and the competition seems to be weakening anyway, as the 2008 report notes:

...following a decades-long global trend in democratisation, the spread of democracy has come to a halt. Comparing the results for 2008 with those from the first edition of the index, which covered 2006, shows that the dominant pattern in the past two years has been stagnation. Although there is no recent trend of outright regression, there are few instances of significant improvement. However, the global financial crisis, resulting in a sharp and possibly protracted recession, could threaten democracy in some parts of the world.

Press release from September:

Transparency International’s global Corruption Perceptions Index (CPI) 2008, launched today, shows a significant worsening of the way the UK’s attitude to corruption is seen in the world. The UK’s score has dropped from 8.4 last year to only 7.7 today: the first time it has ever fallen from the high rating of more than 8 (10 is the highest a country can score on the Index).

The UK's engrained complacency over its failure to take international corruption seriously is now further exposed to public scrutiny. The UK has a wretched foreign bribery prosecution record compared to most of its G7 peers. It was strongly criticised this summer by the OECD body responsible for ensuring that members comply with the 1997 OECD Anti-Bribery Convention and may now face tougher measures by the OECD if it continues to fail.

The top 20:

Transparency International’s global Corruption Perceptions Index (CPI) 2008, launched today, shows a significant worsening of the way the UK’s attitude to corruption is seen in the world. The UK’s score has dropped from 8.4 last year to only 7.7 today: the first time it has ever fallen from the high rating of more than 8 (10 is the highest a country can score on the Index).

The UK's engrained complacency over its failure to take international corruption seriously is now further exposed to public scrutiny. The UK has a wretched foreign bribery prosecution record compared to most of its G7 peers. It was strongly criticised this summer by the OECD body responsible for ensuring that members comply with the 1997 OECD Anti-Bribery Convention and may now face tougher measures by the OECD if it continues to fail.

The top 20:

(htp: Hatfield Girl)

(htp: Hatfield Girl)

BTW: Zimbabwe is not even in the bottom 10 of the list.

An expert writes

The words...

In truth, gold has been a poor investment for a long time...

Other safe havens have done much better... Government bonds... Swiss franc...

Gold rises and falls with oil, copper and wheat, and all the other things that get turned into stuff in factories. It is still a useful metal. But it is not money — and after its failure to rally in this crisis, even the most dogmatic gold bug may well have to admit that.

(Matthew Lynn in The Spectator)

The picture...

Friday, December 05, 2008

Corruption Competition

Jeremy Clarke's dragoman introduces a brilliant new system of classification:

The Egyptian government is 100 per cent corrupt. In other countries the government is 10 per cent corrupt or maybe 20 or 50 per cent. Here in Egypt it is 100 per cent corrupt. I am telling you.

You are invited to argue the case for one or more "other countries" to be considered as runners-up in this competition.

(Please have regard for libel law.)

China to devalue its currency?

I said some time ago that Far Eastern creditors weren't going to let themselves be swindled by currency depreciation; now it is rumoured that China (and maybe another country also) will take their revenge and begin a dangerous round of competitive devaluation around the world.

Hurray for a radical

I sympathise with Mish; but getting it done would be like a goat persuading a tiger to turn vegetarian.

If deflation is not the problem, what is?

The problem is fractional reserve lending that allows banks to leverage lending 12-1 and broker dealers like the now defunct Bear Stearns and Lehman 40-1. It does not take much to cause a run on the bank when leverage is 40-1. Fannie Mae is leveraged many times more than that.

Without that excessive leverage, no one would be in trouble over falling prices. Actually everyone would benefit. The cure is not to defeat deflation, the cure is to embrace deflation and stop fractional reserve lending and the serially bubble blowing activities of the Fed.

I support abolishing the Fed and the elimination of fractional reserve lending. Those are the only long term cures to the problems we face.

If deflation is not the problem, what is?

The problem is fractional reserve lending that allows banks to leverage lending 12-1 and broker dealers like the now defunct Bear Stearns and Lehman 40-1. It does not take much to cause a run on the bank when leverage is 40-1. Fannie Mae is leveraged many times more than that.

Without that excessive leverage, no one would be in trouble over falling prices. Actually everyone would benefit. The cure is not to defeat deflation, the cure is to embrace deflation and stop fractional reserve lending and the serially bubble blowing activities of the Fed.

I support abolishing the Fed and the elimination of fractional reserve lending. Those are the only long term cures to the problems we face.

Tuesday, December 02, 2008

The dangers of harmony

I'm still convinced that many in the financial community deserve far harsher treatment than they've so far received - if they didn't know what would happen, they should have.

But I've been casting about for some deeper structural reason - what allowed financiers to kid themselves that they were acting reasonably, or at least assure themselves that they had followed official guidelines and were "covered"?

So I looked for something relating to the regulation of fractional reserves, and came across references to the Basel Accords (I and II). These are an attempt to "harmonise" central banking policies in developed nations, and perhaps can serve as an object lesson (especially for EU enthusiasts) about international legislation.

Here is the conclusion of an analysis of the two Accords (highlights mine):

One very important fact to assess is the achievements and limitations of each Basel Accord. The first Basel Accord, Basel I, was a groundbreaking accord in its time, and did much to promote regulatory harmony and the growth of international banking across the borders of the G-10 and the world alike. On the other hand, its limited scope and rather general language gives banks excessive leeway in their interpretation of its rules, and, in the end, allows financial institutions to take improper risks and hold unduly low capital reserves.

Basel II, on the other hand, seeks to extend the breadth and precision of Basel I, bringing in factors such as market and operational risk, market-based discipline and surveillance, and regulatory mandates. On the other hand, in the words of Evan Hawke, the U.S. Comptroller of the Currency under George W. Bush, Basel II is “complex beyond reason” (Jones, 37), extending to nearly four hundred pages without indices, and, in total, encompassing nearly one thousand pages of regulation.

The author's concern is that the rules can permit the risk of assets in emerging markets to be understated, and as it turns out the Trojan horse came in through another gate; but in complexity lies opportunity, and in rule-following lies the illusion that personal responsibility is thereby written off.

But I've been casting about for some deeper structural reason - what allowed financiers to kid themselves that they were acting reasonably, or at least assure themselves that they had followed official guidelines and were "covered"?

So I looked for something relating to the regulation of fractional reserves, and came across references to the Basel Accords (I and II). These are an attempt to "harmonise" central banking policies in developed nations, and perhaps can serve as an object lesson (especially for EU enthusiasts) about international legislation.

Here is the conclusion of an analysis of the two Accords (highlights mine):

One very important fact to assess is the achievements and limitations of each Basel Accord. The first Basel Accord, Basel I, was a groundbreaking accord in its time, and did much to promote regulatory harmony and the growth of international banking across the borders of the G-10 and the world alike. On the other hand, its limited scope and rather general language gives banks excessive leeway in their interpretation of its rules, and, in the end, allows financial institutions to take improper risks and hold unduly low capital reserves.

Basel II, on the other hand, seeks to extend the breadth and precision of Basel I, bringing in factors such as market and operational risk, market-based discipline and surveillance, and regulatory mandates. On the other hand, in the words of Evan Hawke, the U.S. Comptroller of the Currency under George W. Bush, Basel II is “complex beyond reason” (Jones, 37), extending to nearly four hundred pages without indices, and, in total, encompassing nearly one thousand pages of regulation.

The author's concern is that the rules can permit the risk of assets in emerging markets to be understated, and as it turns out the Trojan horse came in through another gate; but in complexity lies opportunity, and in rule-following lies the illusion that personal responsibility is thereby written off.

Monday, December 01, 2008

The eyes, look at the eyes

I referred recently to some BNP supporters as "scrubbed-up thugs"; sadly, that also is the impression given by some New Labour apparatchiks.

I referred recently to some BNP supporters as "scrubbed-up thugs"; sadly, that also is the impression given by some New Labour apparatchiks.Is it true that, like Cordelia and the Fool, Ed Balls and Nick Griffin have never been seen together?

{kind=link}

Subscribe to:

Posts (Atom)