Presiding over indebtedness... or as helpless as King Canute?

"Eventually" is happening now, as it happens. We were looking for a place to rent, found one on the Internet at £595/month, looked round it last week and the agent handed us a details sheet with the asking rent: £450.

Schiff's on a roll - read him. It's long, but worthwhile, epecially the predictive part at the end. An Eastern credit strike, a collapsing dollar, rapid inflation, price controls and the development of a black market.

Schiff's on a roll - read him. It's long, but worthwhile, epecially the predictive part at the end. An Eastern credit strike, a collapsing dollar, rapid inflation, price controls and the development of a black market.

Scott Burns at MSN Money (htp: Michael Panzner) calculates that unfunded government programs for social security and Medicare ($46 trillion) represent a debt equivalent to around 90% of all consumers' net worth ($51.5 trillion). If Americans' net assets decline by a further 10%, then effectively the American citizen is bust.

Scott Burns at MSN Money (htp: Michael Panzner) calculates that unfunded government programs for social security and Medicare ($46 trillion) represent a debt equivalent to around 90% of all consumers' net worth ($51.5 trillion). If Americans' net assets decline by a further 10%, then effectively the American citizen is bust. A killer graph here from Charles Hugh Smith. Interestingly, the steady real decline of average incomes begins at almost exactly the same time as Nixon shut the "gold window".

A killer graph here from Charles Hugh Smith. Interestingly, the steady real decline of average incomes begins at almost exactly the same time as Nixon shut the "gold window".

I still think we're in a sort of re-run of the 70s. Cash will be forced out of accounts and into the market, where it will still lose value, but nothing like as badly as if left rotting in banks and building societies. The Great Theft is on its way.

If you follow Marc Faber, you'll know that he's currently suggesting holding half your wad as cash, since the bubble hasn't really burst yet; but other than that, he's thinking 10% gold and 40% in a combination of resource and emerging market stocks.

The world's average per capita income is $8k - $9k; as globalisation continues the levelling-out process, the East will never be as rich as we once were, but they'll be less poor. For us, on the other hand, this may be the last chance to put something away for our future.

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

When Nixon closed the "gold window" (15 August 1971), gold ceased to be a currency backing and became just another thing you could choose to invest in, so let's compare these assets from a little before that turning-point, onwards:

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

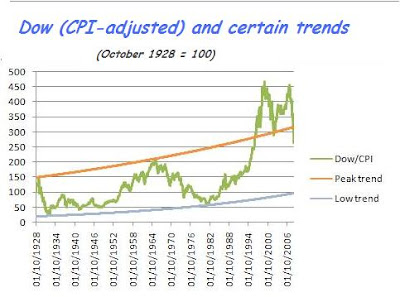

That depends on whether you read this as a statement about gold, or about the Dow. I looked at the Dow in inflation (CPI) terms a while back (December 2008):

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

Back to gold-pricing: it's also notable that the Dow is currently still worth some 8 ounces of gold, but in previous lows (Feb. 1933, March 1980) fell below 2 ounces: So should we still pile into gold, as a hedge against the further collapse of the Dow?

So should we still pile into gold, as a hedge against the further collapse of the Dow?

I think not. Firstly, the Dow may well have a rally, since it's fallen so sharply in such a short time. And secondly, this is missing the point, which is that we are looking to protect wealth against inflation, not against the Dow.

So another question is, how does gold hold its value during periods of price inflation? A period some readers may have lived through, is that after the oil price hike of October 1973. Here is what happened in the 5 years from 1974 to 1978:

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide. The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms). The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend: There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

The "real Dow", i.e. nominal value divided by the CPI inflation index, was about 14.6 in October 1928 and is now at c. 33.5.

The "real Dow", i.e. nominal value divided by the CPI inflation index, was about 14.6 in October 1928 and is now at c. 33.5.

(Values at 01 Oct 1928 = 1)

(Values at 01 Oct 1928 = 1)