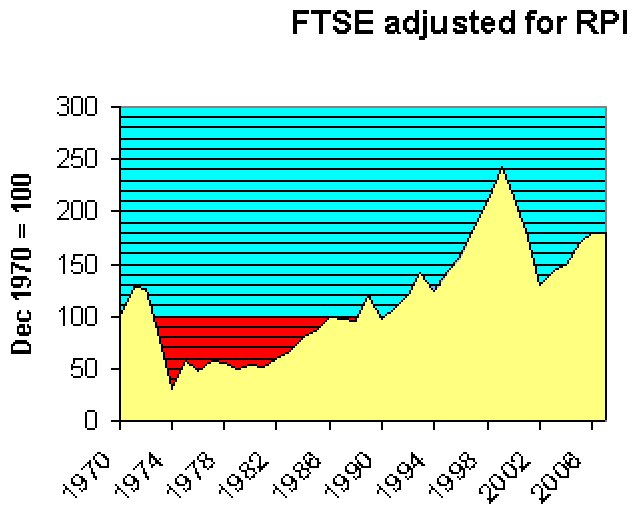

According to iTulip, we are at Step D in a timetable (published in January 2005) that implies we have quite some years to go before a housing upturn.

Their point about real estate being an illiquid market seems valid to me, and I've suggested before now that we should expect a decline and a long stall, rather than an equity-style crash.

Saturday, July 12, 2008

Zimbabwe: racism and international meddling

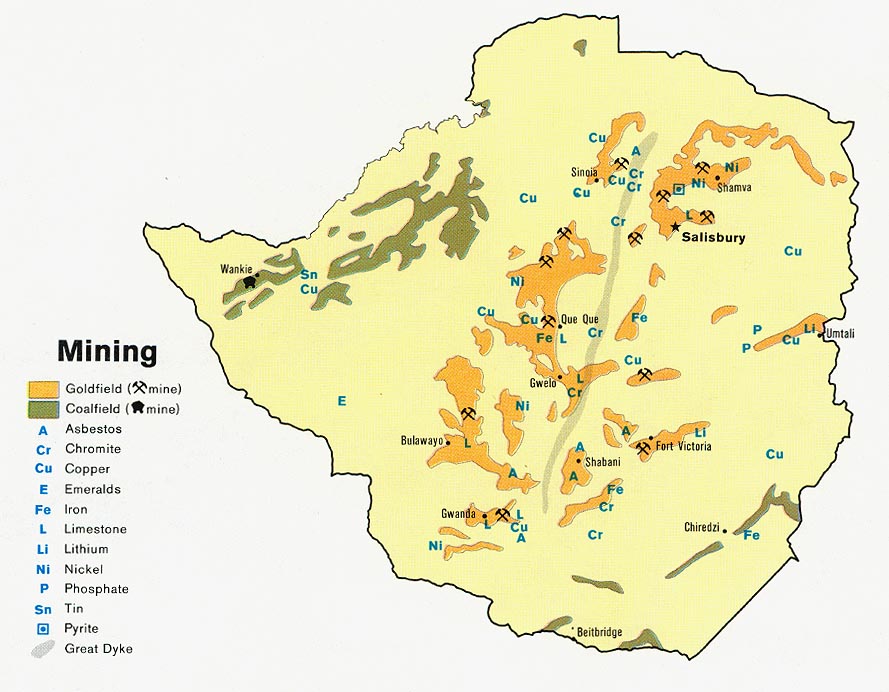

Mines in Zimbabwe

Mines in ZimbabweZimbabwe on Saturday welcomed the failure of a Western-backed U.N. Security Council resolution to impose sanctions over its violent presidential elections, calling it a victory over racism and meddling in its affairs. (Reuters)

Racist...

Robert Mugabe is a member of the Shona tribe (as is opposition leader Morgan Tsvangirai), which comprises 70% of the population of Zimbabwe, occupying the centre and north of the country.

The Matabele (Ndebele) tribe, who tend to live in the southern part, make up half of the remaining minority, and (not surprisingly, in view of their post-Independence massacres by Mugabe's troops) are supporters of the MDC (Movement for Democratic Change). ''The denial of food to opposition strongholds has replaced overt violence as the government's principal tool of repression,'' the ICG wrote in August 2002.

Meddling...

Zimbabwe's natural resources include "coal, chromium ore [10% of the world's reserves], asbestos, gold, nickel, copper, iron ore, vanadium, lithium, tin, platinum group metals" (CIA World Factbook), and there are 10 or so foreign-owned mining companies operating there. The Zimbabwean kleptocracy has turned from seizing farms (which they either don't know how to run, or can't be bothered to), to grabbing controlling interests in foreign-owned firms, and a 25% no-compensation stake in mining companies. Presumably, in the latter case, they'll leave the operational side to the experts.

In 2005, the Chinese government and Chinese businesses supplied T-shirts for ZANU-PF supporters, jets and trucks for the Army, and the architectural plans and blue tiles for Mugabe's new 25-bedroom mansion. The recent attempt (April 2008) to ship a load of arms in, so that Mr Mugabe could deal with his little local difficulty, was described by the Chinese as "normal military trade". Annual trade between these two countries was expected to reach $500 million this year.

Zimbabwe is touting Russia for trade and business deals, including tourism (uniformed hunting trips in Matabeleland?)

Perhaps the reason 84-year-old Mugabe is hanging on, is that he and his entourage have a tiger by the tail. How could they get out of their land-locked country alive?

UPDATE

But why Russia? The New York Times fishes for an explanation as to why Russia indicates some willingness to consider sanctions, and then reneged, dragging China with her. The NYT is baffled, limply quoting the US Ambassador to the UN: “Something happened in Moscow.”

Could it be that Zimbabwe in itself has little interest for Russia, but this veto is a dog-whistle to other African nations where the Ivans may develop more serious business links?

Or could it be, as this blogger hypothesises, part of the Great Game between Russia and the US, particularly reflecting missile defence technology?

How skilfully does Robert Mugabe, the Dom Mintoff of East Africa, play off great nations against one another! If only his skills benefitted his country, also.

Stephen Glover, in today's Grumbler:

The English libel laws used to be much loved by the rich and famous, and to a large degree London remains the libel capital of the world to which freebooters of all nationalities, including our own, flock in order to pick up some usually undeserved loot.

Now these and other folk have fastened on to Article Eight of the Human Rights Act. Of course, their and everyone else's privacy must be respected, but so must the right of a free Press to write about the private misbehaviour - more often financial rather than sexual - of the rich and powerful.

Does Mr Glover think this should apply to celeb journalists, also? It seems to me that some members of the Fourth Estate are rich and powerful, when compared to the rest of us.

The English libel laws used to be much loved by the rich and famous, and to a large degree London remains the libel capital of the world to which freebooters of all nationalities, including our own, flock in order to pick up some usually undeserved loot.

Now these and other folk have fastened on to Article Eight of the Human Rights Act. Of course, their and everyone else's privacy must be respected, but so must the right of a free Press to write about the private misbehaviour - more often financial rather than sexual - of the rich and powerful.

Does Mr Glover think this should apply to celeb journalists, also? It seems to me that some members of the Fourth Estate are rich and powerful, when compared to the rest of us.

Signs of the times

A BBC Radio 4 topical news comedy programme says that you can't make a movie featuring recession. I beg to differ. I think that we get reflections of how things are now, and inklings of things to come, from contemporary culture - think of Stravinsky's Rites of Spring and how the world changed shortly afterwards. Look out for films that echo these:

And I read long ago that some professional investors look for all sorts of straws in the wind, for example, the length of women's skirts (shorter = more confident, boomtime).

Any similar?

UK economy: between a rock and a hard place

CU has asked me to comment on his latest post on the UK's economic crisis. I'm flattered that someone thinks my opinion is worth anything, but here's my effort:

There's often a kind of self-destructive excitement as a crisis develops, as at the gathering of forces for a war. But the Rupert Brookes will be succeeded by the Wilfred Owens.

I have believed for about 9 years that we are in for an unpleasant time, and that is why I returned to the public sector pro tem at the end of 1999: I really did (and do) think that everybody should prepare for a storm. I have also been encouraging my clients to become/stay cautious, for the last 10 years. I thought we'd returned to sanity in 2003, when the FTSE had halved from its start-2000 peak, but off we went again. From my amateur perspective (and who exactly is an expert on the world economy?), the delay in facing economic reality has allowed the patient's condition to worsen.

Mark Wadsworth's opening comment here was "Sell to rent. Cash is King." Yes, I agree, at this stage. I was talking to my wife last year about selling the house (and, I think, the year before that) but personal circumstances and priorities often trump the cold financial calculations, don't they?

However, I don't think cash will be king for a long period. I can't see the government rapidly shrinking the public sector, and at the same time we shall see reduced earnings, more insolvencies and increasing unemployment in the private sector. The financial sector, which has helped our nation's books to nearly balance, is being hit in banking and investment now, and will (I think) be hit worse in future; that cow will yield far less milk to the Treasury, and so the budget will be even more unbalanced than it is today.

Europe seems keen to enforce a discipline on the Chancellor of the Exchequer, that it has been unwilling to emulate with respect to its own accounts for many years; if the EU continues to take such a rigid line, maybe there will be a tear in the EU fabric, along the line of the English Channel.

Meanwhile, I think Gordon Brown's reputation as a money manager is ruined. As has been said, he failed to fix the roof when the weather was fine. A playboy can seem a financial wizard as long as he keeps partying on his yacht, but the adoring guests will disembark when the holes below the waterline make themselves felt.

(I wonder what would have happened if the Conservatives had won again in 1997? Can we be confident that the consequences would have been better?)

To right the ship of State will take money, or (since we hardly know what faith to place in money any more) perhaps it would be apter to say, wealth. This, I think, is where the "cash is king" slogan will wear thin. At the moment, we see a devaluation/destocking in houses, cars, computers and other big-ticket items. It's a good time for Loadsamoney to go shopping, even if the price of his dried pasta is up 40%.

But when the stocks have been run down to match shrunken demand levels, and Loadsamoney's firm is on the skids, the game will probably change. RPI is on the up, but now the causes are more external than internal: we have forgotten the lessons of WWII and have become very dependent on imports of food and fuel, which are major components of those inflation indices that aim to reflect the circumstances of the ordinary person. So interest rate rises are unlikely to reduce the cost of such necessities, except indirectly insofar as they may help strengthen sterling; yet a weakening in sterling is the hope for our trade in manufactures (the pound has dropped 15% or so against the Euro, in the last year). Indeed, we seem to have a policy of shadowing the plummeting US dollar, as once we shadowed the Deutschmark; perhaps, perceiving this strategy, George Soros will stage another coup, to our country's cost, again.

If revenues are down because of recession (or the D-word), where else will the Chancellor find wealth to repair the yacht? More sale of assets to sovereign wealth funds (there goes the family silver)? More bonds sold to trade-surplus foreigners (but will they have the cash, at a time when their own economies may be slumping together with Western consumer demand)? (Perhaps they will, if the US insists on handing the Chinese mortgage bail-out money - see Mish!)

Left high and dry in public view as the tide of wealth recedes, will be the billions in cash held by the crafty, the nervous and the cautious old. And the subtlest way to steal it is by inflation.

I do not know what will be the best store of wealth when major inflation strikes. All the world's gold currently above ground could be made into a cube that would fit comfortably under the arches of the Eiffel Tower (and historically, a fair bit of it could have been found not far away from the Tour Eiffel, stashed away in French ceiling-bowl lights). The gold market is small enough to be a prey to manipulation both ways.

Perhaps a safer store of value would be NS&I index-linked savings certificates. If inflation gets too bad, the easy way out for the government will be not to launch new issues, and the old ones have a maximum term of 5 years. There could theoretically be a problem for investors, in the effect of inflation between the date of maturity and the date the money is cleared in the investor's bank account, but we must hope that the government will never permit a hyperinflation.

And I note that landowners such as the Duke of Westminster have rarely sold their land because of temporary monetary inflation. Even if house prices do decline towards 3 times earnings, they will always have a value, and if rented out, will create an income. Perhaps Mark's comment would then be reversed: buy to rent, not sell to rent. Even now, as many try to get out from under the mortgage trap, there are signs that renting out property is a promising sector, since (I understand) demand is increasing faster than supply.

I'd be interested to hear other ideas.

There's often a kind of self-destructive excitement as a crisis develops, as at the gathering of forces for a war. But the Rupert Brookes will be succeeded by the Wilfred Owens.

I have believed for about 9 years that we are in for an unpleasant time, and that is why I returned to the public sector pro tem at the end of 1999: I really did (and do) think that everybody should prepare for a storm. I have also been encouraging my clients to become/stay cautious, for the last 10 years. I thought we'd returned to sanity in 2003, when the FTSE had halved from its start-2000 peak, but off we went again. From my amateur perspective (and who exactly is an expert on the world economy?), the delay in facing economic reality has allowed the patient's condition to worsen.

Mark Wadsworth's opening comment here was "Sell to rent. Cash is King." Yes, I agree, at this stage. I was talking to my wife last year about selling the house (and, I think, the year before that) but personal circumstances and priorities often trump the cold financial calculations, don't they?

However, I don't think cash will be king for a long period. I can't see the government rapidly shrinking the public sector, and at the same time we shall see reduced earnings, more insolvencies and increasing unemployment in the private sector. The financial sector, which has helped our nation's books to nearly balance, is being hit in banking and investment now, and will (I think) be hit worse in future; that cow will yield far less milk to the Treasury, and so the budget will be even more unbalanced than it is today.

Europe seems keen to enforce a discipline on the Chancellor of the Exchequer, that it has been unwilling to emulate with respect to its own accounts for many years; if the EU continues to take such a rigid line, maybe there will be a tear in the EU fabric, along the line of the English Channel.

Meanwhile, I think Gordon Brown's reputation as a money manager is ruined. As has been said, he failed to fix the roof when the weather was fine. A playboy can seem a financial wizard as long as he keeps partying on his yacht, but the adoring guests will disembark when the holes below the waterline make themselves felt.

(I wonder what would have happened if the Conservatives had won again in 1997? Can we be confident that the consequences would have been better?)

To right the ship of State will take money, or (since we hardly know what faith to place in money any more) perhaps it would be apter to say, wealth. This, I think, is where the "cash is king" slogan will wear thin. At the moment, we see a devaluation/destocking in houses, cars, computers and other big-ticket items. It's a good time for Loadsamoney to go shopping, even if the price of his dried pasta is up 40%.

But when the stocks have been run down to match shrunken demand levels, and Loadsamoney's firm is on the skids, the game will probably change. RPI is on the up, but now the causes are more external than internal: we have forgotten the lessons of WWII and have become very dependent on imports of food and fuel, which are major components of those inflation indices that aim to reflect the circumstances of the ordinary person. So interest rate rises are unlikely to reduce the cost of such necessities, except indirectly insofar as they may help strengthen sterling; yet a weakening in sterling is the hope for our trade in manufactures (the pound has dropped 15% or so against the Euro, in the last year). Indeed, we seem to have a policy of shadowing the plummeting US dollar, as once we shadowed the Deutschmark; perhaps, perceiving this strategy, George Soros will stage another coup, to our country's cost, again.

If revenues are down because of recession (or the D-word), where else will the Chancellor find wealth to repair the yacht? More sale of assets to sovereign wealth funds (there goes the family silver)? More bonds sold to trade-surplus foreigners (but will they have the cash, at a time when their own economies may be slumping together with Western consumer demand)? (Perhaps they will, if the US insists on handing the Chinese mortgage bail-out money - see Mish!)

Left high and dry in public view as the tide of wealth recedes, will be the billions in cash held by the crafty, the nervous and the cautious old. And the subtlest way to steal it is by inflation.

I do not know what will be the best store of wealth when major inflation strikes. All the world's gold currently above ground could be made into a cube that would fit comfortably under the arches of the Eiffel Tower (and historically, a fair bit of it could have been found not far away from the Tour Eiffel, stashed away in French ceiling-bowl lights). The gold market is small enough to be a prey to manipulation both ways.

Perhaps a safer store of value would be NS&I index-linked savings certificates. If inflation gets too bad, the easy way out for the government will be not to launch new issues, and the old ones have a maximum term of 5 years. There could theoretically be a problem for investors, in the effect of inflation between the date of maturity and the date the money is cleared in the investor's bank account, but we must hope that the government will never permit a hyperinflation.

And I note that landowners such as the Duke of Westminster have rarely sold their land because of temporary monetary inflation. Even if house prices do decline towards 3 times earnings, they will always have a value, and if rented out, will create an income. Perhaps Mark's comment would then be reversed: buy to rent, not sell to rent. Even now, as many try to get out from under the mortgage trap, there are signs that renting out property is a promising sector, since (I understand) demand is increasing faster than supply.

I'd be interested to hear other ideas.

Zimbabwe: racism and international meddling

Zimbabwe on Saturday welcomed the failure of a Western-backed U.N. Security Council resolution to impose sanctions over its violent presidential elections, calling it a victory over racism and meddling in its affairs. (Reuters)

Racist...

Robert Mugabe is a member of the Shona tribe (as is opposition leader Morgan Tsvangirai), which comprises 70% of the population of Zimbabwe, occupying the centre and north of the country.

The Matabele (Ndebele) tribe, who tend to live in the southern part, make up half of the remaining minority, and (not surprisingly, in view of their post-Independence massacres by Mugabe's troops) are supporters of the MDC (Movement for Democratic Change). ''The denial of food to opposition strongholds has replaced overt violence as the government's principal tool of repression,'' the ICG wrote in August 2002.

Meddling...

Zimbabwe's natural resources include "coal, chromium ore [10% of the world's reserves], asbestos, gold, nickel, copper, iron ore, vanadium, lithium, tin, platinum group metals" (CIA World Factbook), and there are 10 or so foreign-owned mining companies operating there. The Zimbabwean kleptocracy has turned from seizing farms (which they either don't know how to run, or can't be bothered to), to grabbing controlling interests in foreign-owned firms, and a 25% no-compensation stake in mining companies. Presumably, in the latter case, they'll leave the operational side to the experts.

In 2005, the Chinese government and Chinese businesses supplied T-shirts for ZANU-PF supporters, jets and trucks for the Army, and the architectural plans and blue tiles for Mugabe's new 25-bedroom mansion. The recent attempt (April 2008) to ship a load of arms in, so that Mr Mugabe could deal with his little local difficulty, was described by the Chinese as "normal military trade". Annual trade between these two countries was expected to reach $500 million this year.

Zimbabwe is touting Russia for trade and business deals, including tourism (uniformed hunting trips in Matabeleland?)

Perhaps the reason 84-year-old Mugabe is hanging on, is that he and his entourage have a tiger by the tail. How could they get out of their land-locked country alive?

UPDATE

But why Russia? The New York Times fishes for an explanation as to why Russia indicates some willingness to consider sanctions, and then reneged, dragging China with her. The NYT is baffled, limply quoting the US Ambassador to the UN: “Something happened in Moscow.”

Could it be that Zimbabwe in itself has little interest for Russia, but this veto is a dog-whistle to other African nations where the Ivans may develop more serious business links?

Or could it be, as this blogger hypothesises, part of the Great Game between Russia and the US, particularly reflecting missile defence technology?

How skilfully does Robert Mugabe, the Dom Mintoff of East Africa, play off great nations against one another! If only his skills benefitted his country, also.

How skilfully does Robert Mugabe, the Dom Mintoff of East Africa, play off great nations against one another! If only his skills benefitted his country, also.

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Friday, July 11, 2008

UK the financial "black sheep"

The UK now has the worst fiscal profile of any developed country in the North Atlantic sphere.

Daily Telegraph (htp: Mish)

Daily Telegraph (htp: Mish)

Are oil speculators to blame?

Russell Roberts at Cafe Hayek discusses a spam email from United Airlines, which blames speculation for much of the high price of oil. Naturally, he puts on his quizzical econ spectacles and says it's like blaming a thermometer for hot weather; but maybe that's just a bit too sideways.

For isn't it interesting that in 20 years, the proportion of oil contracts purchased by middlemen who don't deliver, has risen from 21% to 66%?

And isn't there a big Space Hopper of excess liquidity squmphing around the world's markets and destabilising them, as Dr Marc Faber claims? Indeed, Faber has spent years making money from predicting the future movement of this excess. In an interview on "Financial Sense" on January 12, Faber said:

... we had during the excessive consumption period 1998-2006, a current account deficit in the US that increased from 2% of GDP to over 7% of GDP, and at the end was supplying the world with $800 billion annually. And this river flows into the world through the American current account deficits, and essentially provided the world with the so-called excess liquidity and created booms in everything from art prices to commodities, stocks, bonds, real estate, what not.

I suggest that now that the Space Hopper has been punctured, the speculators riding it have been squmphing around even faster, trying to visit as many markets as they can before their toy goes totally flat.

For isn't it interesting that in 20 years, the proportion of oil contracts purchased by middlemen who don't deliver, has risen from 21% to 66%?

And isn't there a big Space Hopper of excess liquidity squmphing around the world's markets and destabilising them, as Dr Marc Faber claims? Indeed, Faber has spent years making money from predicting the future movement of this excess. In an interview on "Financial Sense" on January 12, Faber said:

... we had during the excessive consumption period 1998-2006, a current account deficit in the US that increased from 2% of GDP to over 7% of GDP, and at the end was supplying the world with $800 billion annually. And this river flows into the world through the American current account deficits, and essentially provided the world with the so-called excess liquidity and created booms in everything from art prices to commodities, stocks, bonds, real estate, what not.

I suggest that now that the Space Hopper has been punctured, the speculators riding it have been squmphing around even faster, trying to visit as many markets as they can before their toy goes totally flat.

Thursday, July 10, 2008

Time for some bankers to pack their bags

Karl Denninger continues his holy-roller rant against banks, supervisory authorities etc and reiterates the need for all the financial horror to be made plain. This is what ought to happen, but I'd have thought it's obvious that the results are likely to be so painful that delaying tactics will continue for as long as possible.

One of the outcomes, he thinks, will be major lawsuits:

We haven't even gotten to litigation risk yet, but you can bet we will. I envision racketeering suits coming in the next year or so as its rather apparent to me that this was not some "rogue deal" but rather a systematic approach to intentional understatement of risk.

I wonder how many banking and rating agency executives are even now quietly liquidating their assets and checking which countries do not have extradition agreements with the USA.

Brunei, Kuwait, the Maldives, the Philippines, Qatar, Tunisia and the UAE could be bearable; some might even allow you to buy a drink. Samoa?

Vietnam's on the rise, even if the dong is under pressure at the moment. Dr Marc Faber has an interest there, and he is no fool.

One of the outcomes, he thinks, will be major lawsuits:

We haven't even gotten to litigation risk yet, but you can bet we will. I envision racketeering suits coming in the next year or so as its rather apparent to me that this was not some "rogue deal" but rather a systematic approach to intentional understatement of risk.

I wonder how many banking and rating agency executives are even now quietly liquidating their assets and checking which countries do not have extradition agreements with the USA.

Brunei, Kuwait, the Maldives, the Philippines, Qatar, Tunisia and the UAE could be bearable; some might even allow you to buy a drink. Samoa?

Vietnam's on the rise, even if the dong is under pressure at the moment. Dr Marc Faber has an interest there, and he is no fool.

Why were construction companies caught in the credit crunch?

That's my question. Years ago I went to a Midlands construction company to prospect them for business, and learned that they had a long-term strategy of buying land when the market was depressed and developing it when the upturn came (well, duh, you're saying, doubtless). They'd done this for several business cycles, as (I assume) any well-established firm in their sector would have done.

It was obvious to me ages ago that house prices had gotten silly. How did major building companies get it so wrong this time, when watching the trend is so fundamental to their survival?

It was obvious to me ages ago that house prices had gotten silly. How did major building companies get it so wrong this time, when watching the trend is so fundamental to their survival?

Commodities fall needed to rescue share prices

Special education funding increases clientele

Over at Cafe Hayek, the cheery US econ blog, a report that funding special needs in education turns schools into bounty hunters and expands the market. The increasing value of "Special Ed" brings more marginal land under cultivation, so to speak.

Being in this field myself, I hear rumours that the UK's current approach to individual assessment and funding of special needs will eventually be phased out, to be replaced by some formula for grants to schools, perhaps based on such factors as the proportion of pupils receiving free school meals. Presumably the schools will then have to be more expert in diagnosing and addressing such special needs as may exist among their intake, but I wonder whether the extra funding will be used strictly for that purpose - or pay for more computers, sports equipment, an upgrade to the Head's Lexus, who knows?

On the other hand, you could hardly have a lengthier, more cumbersome and expensive approach to special needs diagnosis, than the one we have now. I get letters from educational psychologists dictated onto their snappy little digital dictaphones, but typed 6 - 8 weeks later and finally received (by second class post) after a further two weeks. Good thing these kids aren't being treated for busted legs.

Being in this field myself, I hear rumours that the UK's current approach to individual assessment and funding of special needs will eventually be phased out, to be replaced by some formula for grants to schools, perhaps based on such factors as the proportion of pupils receiving free school meals. Presumably the schools will then have to be more expert in diagnosing and addressing such special needs as may exist among their intake, but I wonder whether the extra funding will be used strictly for that purpose - or pay for more computers, sports equipment, an upgrade to the Head's Lexus, who knows?

On the other hand, you could hardly have a lengthier, more cumbersome and expensive approach to special needs diagnosis, than the one we have now. I get letters from educational psychologists dictated onto their snappy little digital dictaphones, but typed 6 - 8 weeks later and finally received (by second class post) after a further two weeks. Good thing these kids aren't being treated for busted legs.

Wednesday, July 09, 2008

Education, literacy and discipline

A thread began at Alice's, originally about the decline in manufacturing industry, but moving on to the expense and alleged uselessness of public services, particularly education - bring back the cane, we're turning out kids who can't read, etc. Here's some news from the front:

When it was available, corporal punishment didn't have to be used often. An unexpected consequence of the ban-the-cane soft-handedness is that children are now assaulted by each other much more frequently, and quite often in the classroom in front of the teacher - whom G*d help if she (and it will usually be a she, these days) tries to get involved.

But as to functional illiteracy, in the absence of old-style discipline (and I agree that schools are not nearly brutal enough), maybe we've got almost as far as we can go, because we're swimming against strong tides. In the past, we had a literate culture and media, and parents who reinforced social rules and had aspirations for their children. The children of today are more likely to have complex and dysfunctional homes, their TVs (I often turn off at 9 to avoid the crapshed) and computers are full of violent fantasy and their neighbourhoods are ruled by postcode-based gangs rather than the police.

With the best will in the world, teachers cannot impose marital fidelity, sobriety, male employment, moral self-restraint in public entertainment, and the free run of the Queen's writ throughout her realm. Quite seriously, we in the education system can hear the creaking and groaning from the pit props in the mine.

Teachers will continue to be moderately well-remunerated as long as our rulers maintain the pretence that schools can do the principal work of child-rearing; when the scales fall from our eyes and we start to take responsibility for our offspring and the example we set them, schools will go back to standardised textbooks and employ humble, low-paid functionaries to steer the children through them. The public purse will benefit, and more importantly so will the next generation, for whom the present one has so little regard.

When it was available, corporal punishment didn't have to be used often. An unexpected consequence of the ban-the-cane soft-handedness is that children are now assaulted by each other much more frequently, and quite often in the classroom in front of the teacher - whom G*d help if she (and it will usually be a she, these days) tries to get involved.

But as to functional illiteracy, in the absence of old-style discipline (and I agree that schools are not nearly brutal enough), maybe we've got almost as far as we can go, because we're swimming against strong tides. In the past, we had a literate culture and media, and parents who reinforced social rules and had aspirations for their children. The children of today are more likely to have complex and dysfunctional homes, their TVs (I often turn off at 9 to avoid the crapshed) and computers are full of violent fantasy and their neighbourhoods are ruled by postcode-based gangs rather than the police.

With the best will in the world, teachers cannot impose marital fidelity, sobriety, male employment, moral self-restraint in public entertainment, and the free run of the Queen's writ throughout her realm. Quite seriously, we in the education system can hear the creaking and groaning from the pit props in the mine.

Teachers will continue to be moderately well-remunerated as long as our rulers maintain the pretence that schools can do the principal work of child-rearing; when the scales fall from our eyes and we start to take responsibility for our offspring and the example we set them, schools will go back to standardised textbooks and employ humble, low-paid functionaries to steer the children through them. The public purse will benefit, and more importantly so will the next generation, for whom the present one has so little regard.

Tuesday, July 08, 2008

Dinner at G8

WORLD leaders sat down to an 18-course gastronomic extravaganza at a G8 summit in Japan, which is focusing on the food crisis.

Don't scoff.

Don't scoff.

I've tried to work up an alternative menu, esp. for Gordon Brown's place (roast turkey?), but so far all I can manage is the wine:

Sweet Cherie (n/a)

Sancerre smiles

Beau jolly

Sham pain

Con yak

Emerging markets inflation could break the current system

... says Nouriel Roubini, and there's already a fund to speculate on consequential revaluation of developing world currencies, according to this.

Inside the news media

A comment from "Ryan" on the previous post is too good not to feature up-front (hope you don't mind, Ryan):

My sister is a journalist, but stays away from the nationals. She points out that the big papers get all their real news from Reuters and the local papers, then work it up into a much bigger story. They don't employ many real reporters or journalists - its too expensive. They prefer talking heads that can offer news-views which add a narrative to a story dug up by someone else and which matches the editorial line of the paper.

My sister also tells me that the papers have dirt on almost every public figure, but they CHOOSE who to turn over. This gives them enormous power over those that they chose to support - they can make you king one day and pauper the next. You can see they do this all the time with celebs, building them up one year and tearing them down the next, but we never imagine that they employ the same tactics with politicians - but they do.

She used to tell me all the tactics that papers would use to tell a story their way with their own spin on it. For instance, how often have you seen a phrase along the lines of "A spokesman said"? No name given. Why? It means the line was made up by the writer and attributed to someone real to give it substance. "A spokesmon", "unnamed sources", "A source within the Labour party" etc etc etc. Yes, they may all refer to a real person - but they could just have been made up by the journo to get his opinion across whilst making it sound like he has his finger on the pulse.

She showed me a story that she sold to the Guardian for £50. It was one column inch. The Guardian worked it up to half a page - all of it made up and based on opinion. She was pissed off: "I should have got £2500 if the story had really been that big!"

Take a story, remove the bits that are attributable to named sources - and what is left is usually made up. The attributable bit has probably come right from Reuters. That's why I don't read papers anymore and rarely watch TV news. Its 90% made up by wet-behind-the- ears kids that know nothing about the world we live in but make up a narrative for the news that suits their editor.

Can anyone else give us any more on the ways of journalists and the news media, please?

My sister is a journalist, but stays away from the nationals. She points out that the big papers get all their real news from Reuters and the local papers, then work it up into a much bigger story. They don't employ many real reporters or journalists - its too expensive. They prefer talking heads that can offer news-views which add a narrative to a story dug up by someone else and which matches the editorial line of the paper.

My sister also tells me that the papers have dirt on almost every public figure, but they CHOOSE who to turn over. This gives them enormous power over those that they chose to support - they can make you king one day and pauper the next. You can see they do this all the time with celebs, building them up one year and tearing them down the next, but we never imagine that they employ the same tactics with politicians - but they do.

She used to tell me all the tactics that papers would use to tell a story their way with their own spin on it. For instance, how often have you seen a phrase along the lines of "A spokesman said"? No name given. Why? It means the line was made up by the writer and attributed to someone real to give it substance. "A spokesmon", "unnamed sources", "A source within the Labour party" etc etc etc. Yes, they may all refer to a real person - but they could just have been made up by the journo to get his opinion across whilst making it sound like he has his finger on the pulse.

She showed me a story that she sold to the Guardian for £50. It was one column inch. The Guardian worked it up to half a page - all of it made up and based on opinion. She was pissed off: "I should have got £2500 if the story had really been that big!"

Take a story, remove the bits that are attributable to named sources - and what is left is usually made up. The attributable bit has probably come right from Reuters. That's why I don't read papers anymore and rarely watch TV news. Its 90% made up by wet-behind-the- ears kids that know nothing about the world we live in but make up a narrative for the news that suits their editor.

Can anyone else give us any more on the ways of journalists and the news media, please?

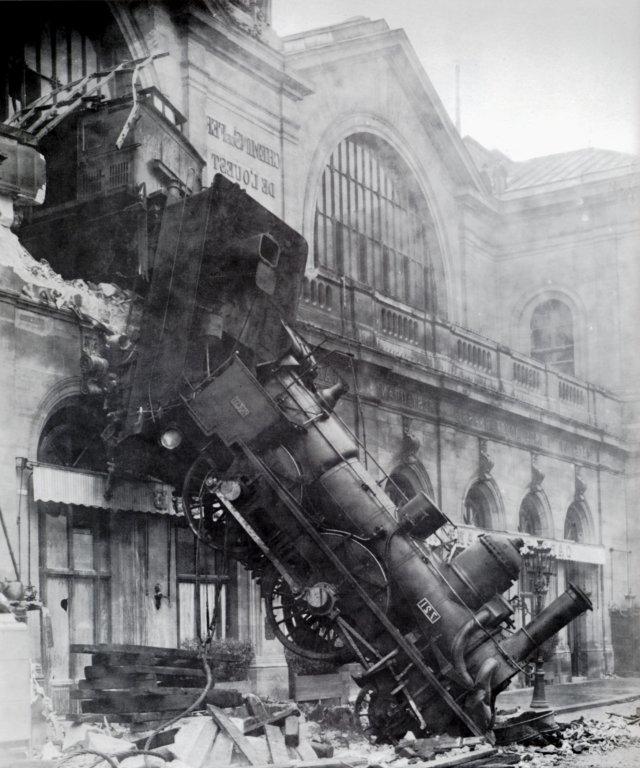

Here is the news

Lead story on Classic FM news this morning: "It looks like Britain's heading for a recession."

FLASH: Queen Anne's dead.

Where does the news come from? Is it any use? Other than weather forecasts, the last usable information I can remember is from the summer of 1987, when I learned that Sir James Goldsmith had sold all his shares on the Paris Bourse, which confirmed my feelings about the way the market was going - but that item came from Private Eye magazine.

December 1, 1978: publication of the Times and Sunday Times suspended for 11 months. During the journalists' industrial dispute, a spoof paper comes out, called "Not The Times". At that time, a strap line for the Financial Times was ""Don't you wish you were better informed?", so the send-up featured a picture of a steam locomotive that had crashed right through the wall of a railway terminus and down onto the pavement beneath, with the headline "What could you have done, had you been better informed?"

FLASH: Queen Anne's dead.

Where does the news come from? Is it any use? Other than weather forecasts, the last usable information I can remember is from the summer of 1987, when I learned that Sir James Goldsmith had sold all his shares on the Paris Bourse, which confirmed my feelings about the way the market was going - but that item came from Private Eye magazine.

December 1, 1978: publication of the Times and Sunday Times suspended for 11 months. During the journalists' industrial dispute, a spoof paper comes out, called "Not The Times". At that time, a strap line for the Financial Times was ""Don't you wish you were better informed?", so the send-up featured a picture of a steam locomotive that had crashed right through the wall of a railway terminus and down onto the pavement beneath, with the headline "What could you have done, had you been better informed?"

Useless, or trivial. As the Poet Laureate Alfred Austin wrote about the terminally-ill King Edward:

"Along the wire the electric message came,

He is no better, He is much the same."

So, who determines the news agenda? Are journalists much cop any more? Are they allowed to be?

... which brings us back to gold.

A quote from the Economist article cited yesterday:

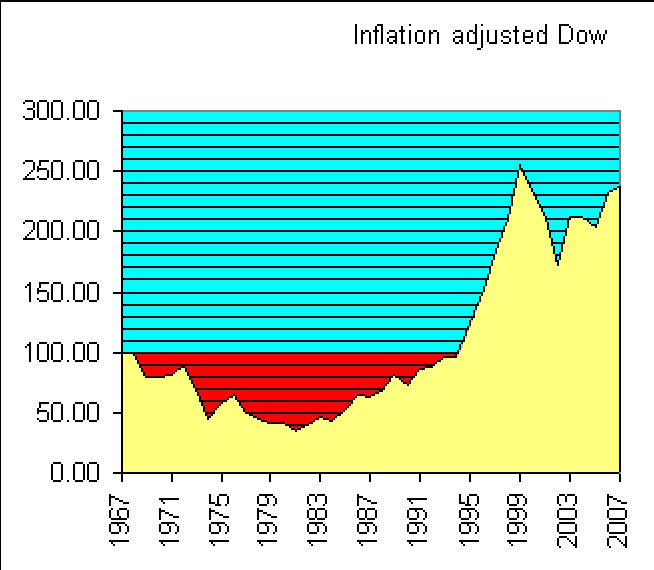

real returns from American shares were just 0.1% a year from 1966-81; they fell a dismal 1.3% a year from 1973 to 1981.

Although that performance was much better than the painfully negative returns suffered by holders of government bonds, it was a long way short of the 6-7% returns that shares have historically achieved. Gold was a much better inflation hedge, earning an annual 10.9% in real terms between 1966 and 1981.

Which is, I suppose, what Marc Faber means by recommending gold at this point.

real returns from American shares were just 0.1% a year from 1966-81; they fell a dismal 1.3% a year from 1973 to 1981.

Although that performance was much better than the painfully negative returns suffered by holders of government bonds, it was a long way short of the 6-7% returns that shares have historically achieved. Gold was a much better inflation hedge, earning an annual 10.9% in real terms between 1966 and 1981.

Which is, I suppose, what Marc Faber means by recommending gold at this point.

Monday, July 07, 2008

Inflation bad for investors as well as depositors

I wondered recently what was the effect of inflation on shares - are they a hedge? Past history suggests not.

Now there is corroboration from a more distinguished source - the Economist.

And Nicola Horlick says don't buy shares for 2 - 3 years.

Well now, I've been leading the experts for a while. When I call the bottom correctly, it'll be time to start my own hedge fund. Usual terms: 2 and 20.

Now there is corroboration from a more distinguished source - the Economist.

And Nicola Horlick says don't buy shares for 2 - 3 years.

Well now, I've been leading the experts for a while. When I call the bottom correctly, it'll be time to start my own hedge fund. Usual terms: 2 and 20.

Sunday, July 06, 2008

Government and homelessness

The "Pathfinder" project for urban renewal has come in for some criticism, because so far it's meant a net loss of 9,000 homes and many of those whose houses have been demolished have not received sufficient compensation to buy something similar elsewhere (see here and here, with an attempt at more balanced discussion in the Liverpool Daily Post).

I suspect we don't have a housing shortage, but a housing misallocation. There are lots of old people rattling around in houses too large for them, and too expensive for them to maintain properly. And how many million bedrooms have been converted into domestic gyms, games rooms etc? We simply expect far more space than we used to, and so the "shortage" is a function of our choices.

But there is a limit on land space, if we want to retain the capacity to feed ourselves in hard times. Maybe we should review policies on housing, housing benefit, local taxation etc. And the policy of using foreign labour to keep down wage rates, and so create traps for our working and under-classes. And is there a Gramscian plan to undermine the cultural cohesion of the country by means of deliberate negligence in border controls, with the side-effect of worsening the pressure on accommodation?

Governments have a talent for creating problems that will long survive them. After four centuries, Northern Ireland still has its difficulties. And look at Fiji, where a century ago British planters imported Indians for indentured service periods of ten years. By the end of their contractual decade, quite naturally the labourers had married, had children and put down roots in the island. The historical result is festering resentment between ethnic groups, leading to outbursts such as George Speight's rebellion in 2000.

Similarly, covering England's green and pleasant land with concrete, tarmac and brick will also have persistent unpleasant consequences. And is there any way to change it back? Could we put a foot depth of earth along a disused motorway to convert it to arable use? So, new building on agricultural land, flood plains etc is tricky, and now we are seeing some of the problems of brownfield development.

But there's a huge number of houses built in the Thirties that need refurbishment. There may be a boom in plumbers, plasters, electricians and bricklayers; while at the same time we may see growing white-collar unemployment, as a result of outsourced information-processing. Maybe the working class will be victorious, after all, while the chattering classes fill holes in their shoes and jumpers with old copies of the Guardian.

I know it can happen, because it did happen in the Thirties - read Helen Forrester, whose debt-burdened middle-class father made the mistake of leaving London post-Crash, to return to his Liverpool birthplace, where the parish had no statutory obligation to support him. Helen wrote that if the Depression comes again, the things to stock up will be newspapers, razor blades and soap. And in her case, a purse inside her clothes so that her own family couldn't steal her meagre savings.

I suspect we don't have a housing shortage, but a housing misallocation. There are lots of old people rattling around in houses too large for them, and too expensive for them to maintain properly. And how many million bedrooms have been converted into domestic gyms, games rooms etc? We simply expect far more space than we used to, and so the "shortage" is a function of our choices.

But there is a limit on land space, if we want to retain the capacity to feed ourselves in hard times. Maybe we should review policies on housing, housing benefit, local taxation etc. And the policy of using foreign labour to keep down wage rates, and so create traps for our working and under-classes. And is there a Gramscian plan to undermine the cultural cohesion of the country by means of deliberate negligence in border controls, with the side-effect of worsening the pressure on accommodation?

Governments have a talent for creating problems that will long survive them. After four centuries, Northern Ireland still has its difficulties. And look at Fiji, where a century ago British planters imported Indians for indentured service periods of ten years. By the end of their contractual decade, quite naturally the labourers had married, had children and put down roots in the island. The historical result is festering resentment between ethnic groups, leading to outbursts such as George Speight's rebellion in 2000.

Similarly, covering England's green and pleasant land with concrete, tarmac and brick will also have persistent unpleasant consequences. And is there any way to change it back? Could we put a foot depth of earth along a disused motorway to convert it to arable use? So, new building on agricultural land, flood plains etc is tricky, and now we are seeing some of the problems of brownfield development.

But there's a huge number of houses built in the Thirties that need refurbishment. There may be a boom in plumbers, plasters, electricians and bricklayers; while at the same time we may see growing white-collar unemployment, as a result of outsourced information-processing. Maybe the working class will be victorious, after all, while the chattering classes fill holes in their shoes and jumpers with old copies of the Guardian.

I know it can happen, because it did happen in the Thirties - read Helen Forrester, whose debt-burdened middle-class father made the mistake of leaving London post-Crash, to return to his Liverpool birthplace, where the parish had no statutory obligation to support him. Helen wrote that if the Depression comes again, the things to stock up will be newspapers, razor blades and soap. And in her case, a purse inside her clothes so that her own family couldn't steal her meagre savings.

Saturday, July 05, 2008

What are recessions and bear markets?

I'm reading picky definitions, e.g. a bear market is one that drops 20% in two months, and a recession is two quarters of negative GDP.

Says who?

What we're in now waddles and quacks like a duck, and darned if it isn't a duck. I say we're in a recession and a bear market, and have been so since the year 2000. A recession, because our manufacturing industries are in steeper decline and will take the rest of the economy down slowly with them*; a bear market, because the stockmarket is more likely to go down than up, over the course of the next year or two.

I once paid for a repair to a slow leak in one of my tyres, and only when I ran over a nail did I discover that the repair had been effected using an old-fashioned inner tube. It went totally flat in two seconds. Thank goodness I wasn't on the motorway. Now, any problems, I get a new tyre.

Monetary inflation was used as an inner tube to repair the economy from around 2003 on. Subprime was the nail.

* For corroboration see "Alice" on the UK current account deficit and our declining trade.

Says who?

What we're in now waddles and quacks like a duck, and darned if it isn't a duck. I say we're in a recession and a bear market, and have been so since the year 2000. A recession, because our manufacturing industries are in steeper decline and will take the rest of the economy down slowly with them*; a bear market, because the stockmarket is more likely to go down than up, over the course of the next year or two.

I once paid for a repair to a slow leak in one of my tyres, and only when I ran over a nail did I discover that the repair had been effected using an old-fashioned inner tube. It went totally flat in two seconds. Thank goodness I wasn't on the motorway. Now, any problems, I get a new tyre.

Monetary inflation was used as an inner tube to repair the economy from around 2003 on. Subprime was the nail.

* For corroboration see "Alice" on the UK current account deficit and our declining trade.

Friday, July 04, 2008

Make the punishment fit the crime

Blaming the prophets

In this week's Spectator, Christopher Fildes discusses the way short-sellers get blamed for market falls, although they take hair-raising risks in doing so. He paraphrases Fred Schwed on the unfairness of such criticism: "In good times, he said, nobody minded the short sellers except their families, who minded going bankrupt. In bad times they were a receptacle for blame." I'd go back further:

But who wants to be foretold the weather? It is bad enough when it comes, without our having the misery of knowing about it beforehand. The prophet we like is the old man who, on the particularly gloomy-looking morning of some day when we particularly want it to be fine, looks round the horizon with a particularly knowing eye, and says:

"Oh no, sir, I think it will clear up all right. It will break all right enough, sir."

"Ah, he knows", we say, as we wish him good-morning, and start off; "wonderful how these old fellows can tell!"

And we feel an affection for that man which is not at all lessened by the circumstances of its NOT clearing up, but continuing to rain steadily all day.

"Ah, well," we feel, "he did his best."

For the man that prophesies us bad weather, on the contrary, we entertain only bitter and revengeful thoughts.

"Going to clear up, d'ye think?" we shout, cheerily, as we pass.

"Well, no, sir; I'm afraid it's settled down for the day," he replies, shaking his head.

"Stupid old fool!" we mutter, "what's HE know about it?" And, if his portent proves correct, we come back feeling still more angry against him, and with a vague notion that, somehow or other, he has had something to do with it.

Jerome K Jerome: "Three Men In A Boat", Chapter 5

So, don't blame me, please, but I still think investors won't be out of the woods until 2010.

But who wants to be foretold the weather? It is bad enough when it comes, without our having the misery of knowing about it beforehand. The prophet we like is the old man who, on the particularly gloomy-looking morning of some day when we particularly want it to be fine, looks round the horizon with a particularly knowing eye, and says:

"Oh no, sir, I think it will clear up all right. It will break all right enough, sir."

"Ah, he knows", we say, as we wish him good-morning, and start off; "wonderful how these old fellows can tell!"

And we feel an affection for that man which is not at all lessened by the circumstances of its NOT clearing up, but continuing to rain steadily all day.

"Ah, well," we feel, "he did his best."

For the man that prophesies us bad weather, on the contrary, we entertain only bitter and revengeful thoughts.

"Going to clear up, d'ye think?" we shout, cheerily, as we pass.

"Well, no, sir; I'm afraid it's settled down for the day," he replies, shaking his head.

"Stupid old fool!" we mutter, "what's HE know about it?" And, if his portent proves correct, we come back feeling still more angry against him, and with a vague notion that, somehow or other, he has had something to do with it.

Jerome K Jerome: "Three Men In A Boat", Chapter 5

So, don't blame me, please, but I still think investors won't be out of the woods until 2010.

Thursday, July 03, 2008

Credit default insurance and murky dealings

You have to have car insurance, it's a legal requirement. So it occurred to me a long time ago that you could make some money selling very low-cost car insurance that (when you looked at the fine print) promised nothing, thus making a safe profit for the company, fooling the regulators and satisfying the cheapskate customer, all at the same time. Fine, till the regulators find out.

According to Karl Denninger today, this is exactly what's happened in the case of UBS insuring one of its mortgage debt packages against default losses. The insurer, it's alleged, has totally inadequate capital for the insurance it's undertaken, but the insurance suited UBS because it permitted the stinking package to be left off the balance sheet.

Oh, to be a lawyer now.

According to Karl Denninger today, this is exactly what's happened in the case of UBS insuring one of its mortgage debt packages against default losses. The insurer, it's alleged, has totally inadequate capital for the insurance it's undertaken, but the insurance suited UBS because it permitted the stinking package to be left off the balance sheet.

Oh, to be a lawyer now.

Housing: have we reached the "point of maximum pessimism"?

Blanche Evans of Realty Times thinks the most of the bad news in housing has already been built into the market; she was interviewed on iTulip a couple of years ago, predicting a downturn but also saying that housing would be supported by the government, to some extent.

Benjamin Graham said we should “buy from pessimists and sell to optimists”. The smart money has done the second part, maybe it should look out for the first soon.

Benjamin Graham said we should “buy from pessimists and sell to optimists”. The smart money has done the second part, maybe it should look out for the first soon.

Peter Schiff using the word "collapse"

Some hot collars in this discussion. But a question does arise for me, which is this: if the US economy has to be rebased on savings and investments, but the sinking dollar raises prices of food, fuel etc, it's going to be very hard to find the money to improve the savings rate. Especially if those who have serious money are doing what Schiff and others would recommend as their financial advisers, i.e. buying foreign stocks and holding foreign currency.

And the same goes for us in the UK, I would think.

Wednesday, July 02, 2008

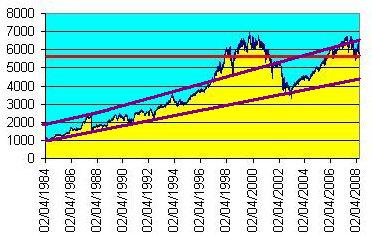

Could deflation reduce the price of gold?

Last year, Robert McHugh predicted that the Dow would drop to 9,000, at least in terms of the price of gold. By January 22 this year, that had happened.

But people like Karl Denninger have been saying for a long time that the outcome of the credit crunch will be deflationary, and Mr Denninger is more emphatic than ever about that now. And that's not just the view of a private investor who backs his judgment with his own hard-earned money: the Bank for International Settlements (htp: Michael Panzner) also thinks deflation a serious possibility.

I recently did a little primitive chartism and thought it possible that the Dow might revert to what looks like a longer-term trend line that includes the 9,000 mark.

Turning to the price of gold, it has certainly soared over the past few years, but there's been debate about manipulation. Frank Veneroso thinks central banks have been releasing stocks of gold to keep the price down, yet at the same time it is suspected that speculators have been boosting the price, possibly using leveraging (borrowing extra cash to increase the returns).

So another way for McHugh's prediction to come true (again), would be for both the Dow and the gold price to come down together. The ratio implicit in his prediction (13.51) could imply that the Dow hits 9,000 and gold drops to about $666 per ounce, or about 30% off where it is now.

Not impossible, if leveraged speculators have to disinvest to repay their borrowings in a hurry; and it would still only be a reversion to where gold was two years ago (and even then, nearly double what it had been three years before that).

But people like Karl Denninger have been saying for a long time that the outcome of the credit crunch will be deflationary, and Mr Denninger is more emphatic than ever about that now. And that's not just the view of a private investor who backs his judgment with his own hard-earned money: the Bank for International Settlements (htp: Michael Panzner) also thinks deflation a serious possibility.

I recently did a little primitive chartism and thought it possible that the Dow might revert to what looks like a longer-term trend line that includes the 9,000 mark.

Turning to the price of gold, it has certainly soared over the past few years, but there's been debate about manipulation. Frank Veneroso thinks central banks have been releasing stocks of gold to keep the price down, yet at the same time it is suspected that speculators have been boosting the price, possibly using leveraging (borrowing extra cash to increase the returns).

So another way for McHugh's prediction to come true (again), would be for both the Dow and the gold price to come down together. The ratio implicit in his prediction (13.51) could imply that the Dow hits 9,000 and gold drops to about $666 per ounce, or about 30% off where it is now.

Not impossible, if leveraged speculators have to disinvest to repay their borrowings in a hurry; and it would still only be a reversion to where gold was two years ago (and even then, nearly double what it had been three years before that).

Investment challenges in a bear market

If you don't believe me, believe a sophisticated investor like Karl Denninger:

No, the test is whether you keep your money in a Bear market. Note that I didn't say "make money". I said keep your money.

If you have the same amount of money now in your investment accounts as you did at SPX 1576 in October, you are doing better than 90% of all institutional money managers and 95% of all individual investors. This puts you in the top 5% - and that's just by going to cash in October and sitting on your hands.

If you've actually made money since then, you're in the top 1%.

Tuesday, July 01, 2008

The potential for Near Eastern industrialisation

Why shouldn't the eastern seaboard of the Mediterranean bcome a manufacturing centre to rival any in the world?

- There is still a vast amount of oil in Arabia, but water, too - e.g. under the Judean desert, plus three aquifers under the Sahara.

- The dry atmospheric conditions are conducive to the long-term storage of stocks of new cars, planes etc.

- The sunny region would be very suitable for "green" energy systems, too, such as solar updraft towers.

- The Arab leaders have enormous reserves of capital.

- There are many people in those countries who would benefit enormously from the work and wealth if their countries industrialised.

- There is land a-plenty for development.

- The eastern Med is beautifully located for producers to get their goods by sea to Western European and North African markets, and the Red Sea for the Middle and Far East.

Monday, June 30, 2008

Marc Faber update: take refuge in gold

Dr Faber has become a gold bug again, but is expecting a correction in other commodities. In a climate of low interest rates and high inflation, Adrian Ash seconds the call for gold.

And here's an extract from Faber's monthly "Market Comment" three years ago (July 5, 2005):

... Lastly, think about the following situation. The US manufacturing sector becomes very weak. The housing market falls and consumption declines. But oil goes through the roof because the empire of eternally rising home prices has just bombed Iran (very likely, in my opinion). Now the Fed cuts interest rates and eases massively. Just think what the stock, bond, foreign exchange, and gold market will do? The initial reaction might be a flight to safety – into government bonds and gold, and out of stocks. But, thereafter, a massive sell-off in bonds could occur as inflationary pressures build from sky high energy prices and massive money printing.

I have to confess, that I am not so sure exactly how this situation would play itself out, but it is worth thinking about it.

Worth the US$ 200 annual subscription, you may think. Especially since some of it goes towards the education of poor children in northern Thailand.

And here's an extract from Faber's monthly "Market Comment" three years ago (July 5, 2005):

... Lastly, think about the following situation. The US manufacturing sector becomes very weak. The housing market falls and consumption declines. But oil goes through the roof because the empire of eternally rising home prices has just bombed Iran (very likely, in my opinion). Now the Fed cuts interest rates and eases massively. Just think what the stock, bond, foreign exchange, and gold market will do? The initial reaction might be a flight to safety – into government bonds and gold, and out of stocks. But, thereafter, a massive sell-off in bonds could occur as inflationary pressures build from sky high energy prices and massive money printing.

I have to confess, that I am not so sure exactly how this situation would play itself out, but it is worth thinking about it.

Worth the US$ 200 annual subscription, you may think. Especially since some of it goes towards the education of poor children in northern Thailand.

Janszen says next bubble will be in energy

A "bubble cycle" instead of a business cycle... house prices to revert to trend and fall 38% from peak... a $12 trillion gap to plug with fresh securities in a different sector as the current bubble collapses... government legislation to clear the way for the speculative rush... $12 tn + an extra $8 tn = $20 tn... it's going to be... ALTERNATIVE ENERGY.

Read iTulip founder Eric Janszen's Harpers article.

"Caloriefornia or bust!" Any views from energy investment specialists (e.g. Nick Drew)?

Read iTulip founder Eric Janszen's Harpers article.

"Caloriefornia or bust!" Any views from energy investment specialists (e.g. Nick Drew)?

A defence of blogging

In early times, learning was only to be had by digging and mining; it is now the circulating medium. Men may become learned in many ways besides the means of erudite courses of instruction: that is learning which enables a writer to inform his readers of matters applicable to the purposes of either profit or pleasure, of which they were not previously aware. In this sense, many are learned who do not suspect themselves in possession of this envied distinction. A prejudice lingers, however, in favour of that description of learning gained by hard study over tall books, and under the dim light of the lamp. But this is only the theory: in practice, men appreciate the living learning only which cheers the evening of leisure, or guides the daily labour - enlightens the professions, or instructs the statesman.

From "The Spectator" magazine, inaugural issue, July 5, 1828.

Yet how swiftly do some other publications forget their humble origins, which have subsequently attained eminent status. "Private Eye" lampoons the "online community" in its column "From The Message Boards"; but in 1961, there were its founders Christopher Booker and Willie Rushton, using typewriter, Letraset, hand-drawn cartoons, scissors and glue (in Willie's mother's flat, I seem to remember) to compose their witty and scurrilous magazine; and the new technology of photo-litho offset to print it. How is this different from the homeworkers of the blogosphere, and the use of the new capabilities of the Internet? Was not Private Eye the original blogpaper?

From "The Spectator" magazine, inaugural issue, July 5, 1828.

Yet how swiftly do some other publications forget their humble origins, which have subsequently attained eminent status. "Private Eye" lampoons the "online community" in its column "From The Message Boards"; but in 1961, there were its founders Christopher Booker and Willie Rushton, using typewriter, Letraset, hand-drawn cartoons, scissors and glue (in Willie's mother's flat, I seem to remember) to compose their witty and scurrilous magazine; and the new technology of photo-litho offset to print it. How is this different from the homeworkers of the blogosphere, and the use of the new capabilities of the Internet? Was not Private Eye the original blogpaper?

Liberty Marr'd by its Champions

A gentleman writes, that Mr Andrew Marr, the news-reporter and erstwhile foe of judge-made privacy law, now desires to be kept privy not only certain information concerning himself, but also the knowledge that he has secured an injunction to that effect from the court.

If any correspondent should care to illuminate this dark matter, he shall find us all ears; though we grant, that ears cannot see.

Might it be item 35 here? As revealed by Guido in January?

UPDATE: Another gentleman writes in defence of Mr Marr's right to privacy

*** 2009 UPDATE: Alastair Campbell implies exposure of Andrew Marr

Sunday, June 29, 2008

Making money out of distressed financials

Michael Panzner has come across a real estate blogpost that includes this idea:

Several of the deal guys said that banks they contacted three months ago about buying assets are all of a sudden calling back. Three months ago they said everything was fine. The idea du jour is to buy the bank to get the bank’s real estate. Sounds screwy to me but I’ll write some more about this one tomorrow.

This reminds me of something I read many years ago in "Adam Smith" (George Goodman) and wrote about here almost exactly a year ago - buying bankrupt (or nearly so) stock that includes the rights to tangible assets.

I don't have the cash or sophistication for this one, but maybe one of you out there knows how to work out whether a bank's shares are selling at a discount to the value of its underlying assets.

There's always an angle, isn't there?

Several of the deal guys said that banks they contacted three months ago about buying assets are all of a sudden calling back. Three months ago they said everything was fine. The idea du jour is to buy the bank to get the bank’s real estate. Sounds screwy to me but I’ll write some more about this one tomorrow.

This reminds me of something I read many years ago in "Adam Smith" (George Goodman) and wrote about here almost exactly a year ago - buying bankrupt (or nearly so) stock that includes the rights to tangible assets.

I don't have the cash or sophistication for this one, but maybe one of you out there knows how to work out whether a bank's shares are selling at a discount to the value of its underlying assets.

There's always an angle, isn't there?

Inflation not purely a monetary phenomenon

I'm puzzled. Milton Friedman said, "Inflation is always and everywhere a monetary phenomenon," yet when I apply this to the UK it doesn't work.

I looked at the Bank of England's figures for M4 from end 1963 to end 2007, and by my calculation the monetary base has increased by a factor of about 240; yet prices have increased only 15 times in the same period. (*)

Currently (and time permitting) I'm also working through David Hackett Fischer's "The Great Wave". In his concluding chapter, he lists seven different causal explanations of inflation, and none of them quite fits the observed facts, not even monetarism. For example, in the sixteenth century, European prices began to rise some time before the imports of gold and silver from the New World could have made a difference.

His idea is that inflation-waves are "autogenous" (don't academics love this kind of label?), by which he means that people make decisions based on current circumstances and their personal predictions for the future, and that helps shape the next set of circumstances. It's like watching a football game unfold, each player adjusting his movements according to his perception of the others.

Fischer thinks that one important factor in the price-wave of the Middle Ages was a trend towards marrying earlier and having more children, which put pressure on natural resources at the same time as altering the ratio of working adults to dependant children. Perhaps this has modern echoes in the growing longevity and reducing mortality rate in the developing world, plus the increasing numbers of dependant elderly in most places.

At any rate, inflation in the West is likely to become less susceptible to control by adjusting the interest rate. What will the Monetary Policy Committee do then?

Perhaps it might help if we established some control over the actual amounts pumped into the economy by the banks (and other creditors). I can dimly remember the news in the 60s, about limits on how much you could borrow to buy fridges, washing machines etc - apparently a minimum deposit was a requirement of the Hire Purchase Act 1964.

However (it seems), Japanese manufacturers found ways to get round this and offer (in effect) 100% loans, and then came the pandemic of credit cards, starting with "your flexible friend" Access (1972). Telegram Sam the drug dealer is always friendly, at first.

________________

(*) Unless, of course, the discrepancy is accounted for by (a) the need for the monetary base to expand each year to cover interest on loans already made, and (b) much extra money being locked-up in real estate - an awful lot of building and rebuilding took place as the postwar economy recovered.

I looked at the Bank of England's figures for M4 from end 1963 to end 2007, and by my calculation the monetary base has increased by a factor of about 240; yet prices have increased only 15 times in the same period. (*)

Currently (and time permitting) I'm also working through David Hackett Fischer's "The Great Wave". In his concluding chapter, he lists seven different causal explanations of inflation, and none of them quite fits the observed facts, not even monetarism. For example, in the sixteenth century, European prices began to rise some time before the imports of gold and silver from the New World could have made a difference.

His idea is that inflation-waves are "autogenous" (don't academics love this kind of label?), by which he means that people make decisions based on current circumstances and their personal predictions for the future, and that helps shape the next set of circumstances. It's like watching a football game unfold, each player adjusting his movements according to his perception of the others.

Fischer thinks that one important factor in the price-wave of the Middle Ages was a trend towards marrying earlier and having more children, which put pressure on natural resources at the same time as altering the ratio of working adults to dependant children. Perhaps this has modern echoes in the growing longevity and reducing mortality rate in the developing world, plus the increasing numbers of dependant elderly in most places.

At any rate, inflation in the West is likely to become less susceptible to control by adjusting the interest rate. What will the Monetary Policy Committee do then?

Perhaps it might help if we established some control over the actual amounts pumped into the economy by the banks (and other creditors). I can dimly remember the news in the 60s, about limits on how much you could borrow to buy fridges, washing machines etc - apparently a minimum deposit was a requirement of the Hire Purchase Act 1964.

However (it seems), Japanese manufacturers found ways to get round this and offer (in effect) 100% loans, and then came the pandemic of credit cards, starting with "your flexible friend" Access (1972). Telegram Sam the drug dealer is always friendly, at first.

________________

(*) Unless, of course, the discrepancy is accounted for by (a) the need for the monetary base to expand each year to cover interest on loans already made, and (b) much extra money being locked-up in real estate - an awful lot of building and rebuilding took place as the postwar economy recovered.

Investment, inflation and market collapses

We have had no fewer than three major financial institutions (outside the US) call for an utter collapse of the equity markets in the last two weeks.

If you're an active investor, you may start thinking about opportunities. Look at the red zones. Draw a line from a deep points to a high one, and feel the greed; but draw lines from a temporary rally to another low, and feel the disappointment. You do need to get your timing right.

If you're an active investor, you may start thinking about opportunities. Look at the red zones. Draw a line from a deep points to a high one, and feel the greed; but draw lines from a temporary rally to another low, and feel the disappointment. You do need to get your timing right.

... says Karl Denninger. Seems like the pros are sitting around waiting for someone else to panic first. Then it'll be time to get in, right?

I recently looked at what happened to shares when a period of inflation begins. You might think that since inflation will also balloon the underlying tangible assets of companies, shares would do okay. But here's the results:

If you're an active investor, you may start thinking about opportunities. Look at the red zones. Draw a line from a deep points to a high one, and feel the greed; but draw lines from a temporary rally to another low, and feel the disappointment. You do need to get your timing right.But inflation heavily penalises the passive investor, too. His boat settles onto the harbour mud; while the unlucky speculator dives headfirst off the retaining wall, deep into the goo. Inflation raises the risks for all.

Crime and punishment

Henry Wallis: "The Stone Breaker" (1857)

Henry Wallis: "The Stone Breaker" (1857)(I've brightened Wallis' painting above, but the foreground in the original is very dark, making a contrast with the gleaming, unreachable beauty of the twilit sky and its reflection on the lake.)

In a country with proper justice, nobody would dare intimidate a witness.

In such a country, wrongdoers are afraid of the law. They'd know that such a crime would certainly be prosecuted and that they'd end up doing at least 15 years breaking rocks.

... says Peter Hitchens in today's Sunday Grumbler.

"Pitee renneth sone in gentil herte," said Chaucer, sometimes ironically. The worthy compassion shown to unfortunates by the Victorians has, gone too far, some argue.

But there are now different reasons to pity. Prisons do not punish the wrongdoer in the old-fashioned ways, but the incarcerated man is no longer protected against bullying, beating, buggery and theft. In how many movies do we hear the police threaten a criminal with what his fellows will do to him in prison? Judge Mental does not put on his black cap and say, "You will be taken from here to a place of detention where you will have your arm forced up your back and..."

Then there's life outside, for the neglected underclass. "Theodore Dalrymple", a doctor who has dealt with many prisoners in Birmingham (UK), used to note in the Spectator magazine that prisoners' health improved considerably in prison, because of no (or reduced) access to drugs. Read the good doctor here on how the liberal approach to mind-altering substances is pretty much a sentence of death (prolonged and degrading). Here's an extract on alcohol:

I once worked as a doctor on a British government aid project to Africa. We were building a road through remote African bush. The contract stipulated that the construction company could import, free of all taxes, alcoholic drinks from the United Kingdom...

Of course, the necessity to go to work somewhat limited the workers’ consumption of alcohol. Nevertheless, drunkenness among them far outstripped anything I have ever seen, before or since. I discovered that, when alcohol is effectively free of charge, a fifth of British construction workers will regularly go to bed so drunk that they are incontinent both of urine and feces. I remember one man who very rarely got as far as his bed at night: he fell asleep in the lavatory, where he was usually found the next morning. Half the men shook in the mornings and resorted to the hair of the dog to steady their hands before they drove their bulldozers and other heavy machines (which they frequently wrecked, at enormous expense to the British taxpayer); hangovers were universal. The men were either drunk or hung over for months on end.

Our soft-handedness on crime and drugs, is really an extreme hard-heartedness.

Saturday, June 28, 2008

The economy is like a rainforest

The news always speaks of "the economy" as though it was one homogeneous whole. In fact, it's a host of micro-economies, financial equivalents of ecological niches.

In the rainforest, there are places that are light or dark, hot or cool, high or low, wet or dry. In the economy, there are savers, borrowers, amateur and professional investors, crooks, marks, young bold, cautious old, workers, shirkers and berserkers.