htp: Karl Denninger

The result:

At least $125bn is to go to nine of America's largest banks, including Citigroup, JPMorgan Chase and Bank of America, in exchange for capital under the rescue plan.

The power:

(9) TROUBLED ASSETS-

The term `troubled assets' means--

(A) residential or commercial mortgages and any securities, obligations, or other instruments that are based on or related to such mortgages, that in each case was originated or issued on or before March 14, 2008, the purchase of which the Secretary determines promotes financial market stability; and

(B) any other financial instrument that the Secretary, after consultation with the Chairman of the Board of Governors of the Federal Reserve System, determines the purchase of which is necessary to promote financial market stability, but only upon transmittal of such determination, in writing, to the appropriate committees of Congress.

...not "prior approval", you'll note. For those that think they understand law, here is the full text of the genetically-modified bill as enacted on 3rd October 2008.

And here's an intriguing clause in Section 119:

(2) LIMITATIONS ON EQUITABLE RELIEF.—

(A) INJUNCTION.—No injunction or other form of equitable relief shall be issued against the Secretary for actions pursuant to section 101, 102, 106, and 109, other than to remedy a violation of the Constitution.

Excuse my ignorance, but is this a watered-down version of the infamous "non-reviewable" Paulosn proposal ("Decisions by the Secretary pursuant to the authority of this Act are non-reviewable and committed to agency discretion, and may not be reviewed by any court of law or any administrative agency.")?

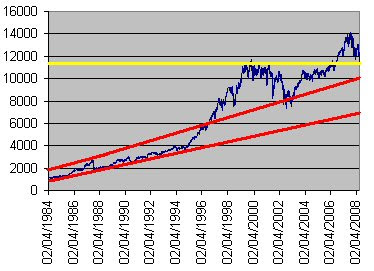

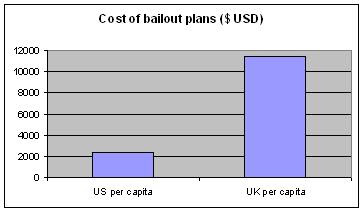

Marc Faber recently said that the US needed $5 trillion to resolve the crisis, i.e. 7 times more than the amount approved by Congress. Britain's bailout fund is proportionately 7 times greater, and so, crippling cost to the taxpayer aside, maybe it could work.

Marc Faber recently said that the US needed $5 trillion to resolve the crisis, i.e. 7 times more than the amount approved by Congress. Britain's bailout fund is proportionately 7 times greater, and so, crippling cost to the taxpayer aside, maybe it could work.

In other words, if America had no such debts, she would have $1.45 trillion more per year to spend on other things.

In other words, if America had no such debts, she would have $1.45 trillion more per year to spend on other things.

Somebody please put me right and/or direct me to authorities and information sources.

Somebody please put me right and/or direct me to authorities and information sources.