Most of us know by now that the government wants to increase rates of organ donation by assuming the right to our bodies the moment we cease to breathe, unless we opt-out of their grisly clutches. Jimmy Young in the Sunday Express notes the failure of such schemes in Brazil and France, for example.

My wife points out that in England, it has always been the law that the body of the deceased belongs to the next of kin. Or has that gone by the board since the EU abolished our country's sovereign right to make its own law?

What has happened to the Common Law, Natural Justice, The Reasonable Man and the long, bloodily-won fight to assert the Englishman's rights against the overweening powers of the State?

And will these things have to be re-won by bloody resistance, one day?

Sunday, November 23, 2008

Bank crashes and the Basel Accords

I need information and understanding - please help me, somebody.

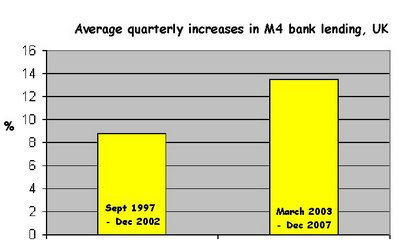

I've pointed out more than once that M4 bank lending in the UK accelerated from 2003 on, and I suspected it was something to do with reducing bank capital adequacy requirements, so the government (via its regulators) would have been implicated. In other words, I've been looking for the villain of the piece, and the smoking gun.

But do you think I can find them?

What I have found so far is references to the Basel Accords, Basel I and Basel II. Basel I became law in the G10 countries including the UK in 1992, and Basel II was published in 2004. The general drift, I understand, is to encourage a uniformity of approach to systemic financial risk, and to introduce a system of risk-weighting bank capital according to what the banks are lending against or investing in. What a success that has proved! Perhaps we should refer to the scheme as "Basel Fawlty".

But can somebody help unpack and simplify what actually happened? Is it, for example, possible that this system was perceived by the banks as a more pliable alternative to fixed minimum reserve ratios, and so they reduced the cash in their vaults to the very least that they could tweak the definitions? For example, we have read many times how mortgage-backed securities are at the heart of the subprime problem, because the packages could be represented as having much less risk than they actually contained.

So is the present crisis an unintended consequence of more elastic international regulation, dating back as far as the early 1990s?

Saturday, November 22, 2008

It's good news week

Im all the gloom, a ray of light: Kiva has just hit $50 million in micro-loans to poor entrepreneurs around the world. Join one of their teams - I have (click on logo in sidebar).

The sixfold path to Chinese hegemony

The Mogambo Guru does a (tragi-) comedy riff on a Chinese piece he's read. Here's a list of tunes that the Chinese author is calling the piper to play:

1. The US should cancel the limits on high-tech exports to China, and allow China to acquire advanced technology and high-tech companies from the US

2. The US needs to open its financial system to Chinese financial institutions, allowing all Chinese financial firms to open branches and develop business in the US

3. The US should not prevent Europe from canceling the ban against selling weapons to China

4. The US should stop selling military weapons to Taiwan

5. The US should loosen its limits on numbers of Chinese tourists and allow them to travel freely to the US

6. The US should never restrain China’s exports to the US and force RMB appreciation in the name of domestic protectionism and employment pressure

Given the relationship between government and journalism in China, I half-suspect that the article may have had input, shall we say, from official sources. Looking at the implications of these demands, we may begin to tremble.

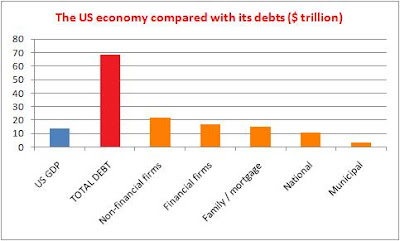

Below, I put in graph from the statistics quoted in that article. To my layman's mind, it's clear that bailouts transferring debt from other piles to the national pile, are a waste of time: it's debt cancellation that's needed.

Friday, November 21, 2008

Publish the lot

Currently there's a furore over here about the publication on the internet of the membership of the British National Party. Some of them look like scrubbed-up thugs, it's true, but I can't see them ever being anything but a cranky and resentful minority. However, if you are a policeman and hold officially-unapproved views, you will lose your job; and there are others for whom this cyber-unmasking will prove a permanent block in their careers.

But if we really want to set the cat among the pigeons, let's make public all political party membership, past and present. Then let's correlate the information with employment. For I recall reading in the 70s that it was pretty much career suicide for teachers in some London boroughs not to be members of the Labour Party, and I suspect the same issue would apply in other areas and other lines of work. And how about mapping the complex network of personal and employment-related relationships, as was done so damningly for Macmillan's government?

And who was in the International Marxist Group and other left-wing, semi-secret societies? The present Minister for "Justice", Jack Straw, has, I understand, called for and either weeded or destroyed the file on himself years ago, a luxury not afforded to many of us. And who went to those annually-advertised Marxist "summer schools" and carefully didn't join a political party, or let their membership lapse to maintain radio silence in their future missions?

Maybe we'll see where the real danger lies.

But if we really want to set the cat among the pigeons, let's make public all political party membership, past and present. Then let's correlate the information with employment. For I recall reading in the 70s that it was pretty much career suicide for teachers in some London boroughs not to be members of the Labour Party, and I suspect the same issue would apply in other areas and other lines of work. And how about mapping the complex network of personal and employment-related relationships, as was done so damningly for Macmillan's government?

And who was in the International Marxist Group and other left-wing, semi-secret societies? The present Minister for "Justice", Jack Straw, has, I understand, called for and either weeded or destroyed the file on himself years ago, a luxury not afforded to many of us. And who went to those annually-advertised Marxist "summer schools" and carefully didn't join a political party, or let their membership lapse to maintain radio silence in their future missions?

Maybe we'll see where the real danger lies.

Moral hazard and white-collar crime

I've said several times that I think a benchmark punishment for those financiers who have very nearly destroyed us with, if not criminal intent, then culpable ignorance, should be the repayment of their last 5 years' bonuses.

Harsh, one may think; unreasonable. Surely this would bankrupt many and leave them homeless.

Well, what is happening now to thousands of the victims of their greedy schemes across America and Britain? Men seeing the disappointment and cooling affection in their women's eyes, feeling the ardour of embraces replaced by demoralising reassurance, knowing that after the comfort comes recrimination; women worrying about their men's fidelity and sobriety, about their own security and the safety of their children; education disrupted, futures blighted.

A long-running motif in public affairs here and presumably across the Atlantic has been "getting away with it". You will all have your own list of those who have been rewarded for misbehaviour. Without fitting retribution, society will continue to crumble. This is not about vengeance, but about making whole.

Harsh, one may think; unreasonable. Surely this would bankrupt many and leave them homeless.

Well, what is happening now to thousands of the victims of their greedy schemes across America and Britain? Men seeing the disappointment and cooling affection in their women's eyes, feeling the ardour of embraces replaced by demoralising reassurance, knowing that after the comfort comes recrimination; women worrying about their men's fidelity and sobriety, about their own security and the safety of their children; education disrupted, futures blighted.

A long-running motif in public affairs here and presumably across the Atlantic has been "getting away with it". You will all have your own list of those who have been rewarded for misbehaviour. Without fitting retribution, society will continue to crumble. This is not about vengeance, but about making whole.

Thursday, November 20, 2008

The reality goggles are smeared

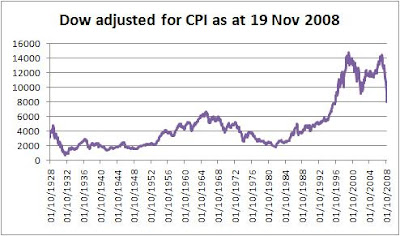

This project of mine is echoed by Eric Janszen of iTulip. His graph and red line suggests what I've been saying recently, that the Dow's trend (if it has one) could be to 6,000 points, with an overshoot to 4,000.

My independently-researched version:

iTulip's:

iTulip's:

My independently-researched version:

iTulip's: It's really hard to see the past in our own terms. I'm trying to do it using the Consumer Price Index, which opens another can of worms about the composition and weighting of that index, especially since (I understand) it affects government statistics and benefits. However, you have to start somewhere.

The first thing to note is how freakish recent years have been. If you connect previous start-of-month highs (August 1929, January 1966) and extended the line, you'd expect the recent Dow highs of 1999 and 2007 to be no more than 10,000 points.

And as for the lows: the drop from 1929 to 1932 was 86% "in real terms"; from 1966 to 1982, 73%; and so far since 1999, 46% - but this last from an amazing historical high. And the 350%-plus American debt-to-GDP ratio is quite unprecedented.

So the history of the last 80 years offers no clear guide as to what could happen next. If proportionately as severe as 1932, the Dow could dive to about 2,100 points; if like 1982, just below 4,000. BUT the second of these great waves crashed rather less than the first, so maybe the third will be even more merciful, perhaps a top-to-bottom fall of only 60%, i.e. end up at c. 5,900.

I note that the Dow has closed tonight at 7,552.29. What a fast fall we've seen - will it spring back sharply and then recommence its decline, as in previous cycles, or is it popping like a balloon?

Methodology

I've noted the Dow as it stood on the first trading day each month, starting October 1928 and ending November 2008 (plus where it stood yesterday - 7.997.28 - since we've seen a further steep fall). Then I've noted the historical CPI as at the end of the previous month in each case. Then, looking at the latest Dow figure, I've adjusted historical Dow figures accordingly (i.e. Dow then/CPI then, times CPI now).

Sources: Dow: Yahoo! Finance; CPI: InflationData.com

UPDATE

iTulip today also reproduces its graph on holdings at the Federal Reserve bank, underscoring the point that the current crisis has features that we can scarcely compare to anything in the last 80 years. Except that it's unlikely to be good news.

Subscribe to:

Posts (Atom)