The vitally important inflation / deflation debate continues. In my last post, I relayed one view, which is that the very rich and powerful will not permit runaway inflation, because it erodes the value of money and the rich have most of the money.

As a corrective, I give below the latest video from the National Inflation Association (NIA), a US group that has warned about credit growth and inflation for a long time. Their motivation appears to be patriotic - a return to sound money as part of what makes individual prosperity and freedom possible.

The NIA argues that the rise in the price of gold is not because of mass speculation, for although a lot of gold has been bought recently, a lot has also been sold. What may be happening now is a transfer of privately-held gold from relatively poor people who need to raise money, to investors who are looking ahead to a time when cash will rapidly depreciate. Think of all those gold-buying outlets (or inlets) you now see on your High Street. As someone said a while ago, the mania will be when those shops start selling you gold instead of buying it from you.

As many have now said, trading nations around the world are devaluing their currencies to keep pace with one another, for fear that their exports will be hit if they don't. So the soaring value of precious metals can be seen as a better indication of inflation than currency exchange rates.

You may think that if currencies are depreciating, then surely prices of goods and services in general must also increase rapidly, and we don't see this yet. But we are in a recession and the threat of unemployment is keeping down wage demands; the self-employed are willing to lower their rates, perhaps especially if paid in cash; and traders in items such as cars and computers are offering discounts to clear stock and keep paying their overheads.

However, the NIA and others say there will come a time when the system begins to crack. Governments are buying their own debt, or lending money to banks to do it for them, to maintain the appearance of normality and control; this can't go on forever. The prediction is that we will get either default or hyperinflation. So the gold bugs say buy gold, silver, maybe oil and agricultural commodities etc - anything tangible that can't be multiplied at will.

I don't think (feel) that the turning point is imminent, because of recession and the attempts by some governments (such as the UK) to retrench. But I fear that these last-ditch attempts are untimately doomed to partial or complete failure. In that case, the gold bugs will probably be vindicated.

The other thing I'd say, as I've said before, is that if the system really does come under severe strain, the price of gold may not be the most important of your concerns. If you accept the inflationists' thesis, you will be quietly making preparations to cope with emergencies of different kinds.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, October 09, 2010

Wednesday, October 06, 2010

Down with the Bolligarchs!

"Governing is quite simple, really," remarked Kameronski. "It's merely a matter of knouting the krestyan and taxing the burzhuaznyĭ. Some," and he looked about him meaningfully as a dread silence enveloped the room, "fail to understand the necessity of firmness."

"Governing is quite simple, really," remarked Kameronski. "It's merely a matter of knouting the krestyan and taxing the burzhuaznyĭ. Some," and he looked about him meaningfully as a dread silence enveloped the room, "fail to understand the necessity of firmness."The figure on the right in the last image is that of the hapless Osbornski, purged with other moderates and revisionists in the ensuing Party reorganisation. His wilier successor Clarkov, known as "old Stone-Liver", survived until the latter half of the decade.

Saturday, September 25, 2010

The Thin Geek Line

I have just finished reading "The Ultimate Utility of Nonutility", by Lisa Colletta (Academe magazine, September-October 2010).

In it, she writes the following:

"A liberal mind is one which is independent and disinterested, aware of the history of thought, action, and reaction, and understanding of ambiguity. The liberal arts are not valuable because they are useful politically or vocationally. They are valuable because they are what constitutes real knowledge.

...I would claim that real knowledge of the real world is emphatically not the domain of the professional fields. The professions teach students skills, skills that may indeed be useful, but are too often uniformed by knowledge or thoughtfulness."

She is not alone in her dismissive attitude towards the sciences and engineering. I have seen similar opinions expressed by David Brooks of The Washington Post, Simon Jenkins of the UK's The Guardian, several other political commentators, and all too many university professors.

They remind me of the ancient Greek philosophers, debating the virtues of democracy, while surrounded by slaves and servants who do the actual work.

Apparently, her 'real' knowledge and grasp of the ephemeral nature of human constructs have failed to make her aware of the frailty of our whole civilization.

Were it not for the excess food and other resources provided by the Agricultural, Scientific and Industrial Revolutions, our comfortable lives would not be possible, the lofty ideals of the Enlightenment would be so much empty rhetoric, and democracy as we know it would not exist. In fact, without the relatively small number of technical experts, the best estimates are that 95% of humanity would starve to death within a few months.

Let her ponder that the next time she pontificates to her students.

In it, she writes the following:

"A liberal mind is one which is independent and disinterested, aware of the history of thought, action, and reaction, and understanding of ambiguity. The liberal arts are not valuable because they are useful politically or vocationally. They are valuable because they are what constitutes real knowledge.

...I would claim that real knowledge of the real world is emphatically not the domain of the professional fields. The professions teach students skills, skills that may indeed be useful, but are too often uniformed by knowledge or thoughtfulness."

She is not alone in her dismissive attitude towards the sciences and engineering. I have seen similar opinions expressed by David Brooks of The Washington Post, Simon Jenkins of the UK's The Guardian, several other political commentators, and all too many university professors.

They remind me of the ancient Greek philosophers, debating the virtues of democracy, while surrounded by slaves and servants who do the actual work.

Apparently, her 'real' knowledge and grasp of the ephemeral nature of human constructs have failed to make her aware of the frailty of our whole civilization.

Were it not for the excess food and other resources provided by the Agricultural, Scientific and Industrial Revolutions, our comfortable lives would not be possible, the lofty ideals of the Enlightenment would be so much empty rhetoric, and democracy as we know it would not exist. In fact, without the relatively small number of technical experts, the best estimates are that 95% of humanity would starve to death within a few months.

Let her ponder that the next time she pontificates to her students.

Tuesday, September 21, 2010

Excellent article by Charles Hugh Smith

Charles Hugh Smith explains the current mess in terms of class warfare and entrenched self-interest. In a nutshell:

US citizens have to pay US tax on their earnings anywhere in the world, but if they renounce citzizenship and have over $2 million in net assets (including income-producing assets such as pensions), there is still a one-off ransom tax to pay before they leave.

If they have less than $2 million, they may not have enough to live the idler's dream abroad.

The result is that fewer than 750 Americans chose the escape route in the last year.

But Smith's article is very useful for seeing how the parts of the machine work, and why it resists reconstruction.

- The wealthiest top 1% have influenced the tax system so that their investment income is barely touched, especially when there are loopholes and shelters they can use. They and their wealth can stay in the US.

- The bottom 60% depend partly or wholly on what they receive in benefits from the system. They have to stay in the US.

- This puts the burden on the middle-to-upper income-earners. But if the burden gets too heavy, the top half of those earners may choose to flee the country. If so, the system breaks down.

US citizens have to pay US tax on their earnings anywhere in the world, but if they renounce citzizenship and have over $2 million in net assets (including income-producing assets such as pensions), there is still a one-off ransom tax to pay before they leave.

If they have less than $2 million, they may not have enough to live the idler's dream abroad.

The result is that fewer than 750 Americans chose the escape route in the last year.

But Smith's article is very useful for seeing how the parts of the machine work, and why it resists reconstruction.

Tuesday, September 14, 2010

What inflation? "Them" won't let it happen

Inflation in food and soon, it is reported, in clothing, is owing to factors such as bad harvests, rising energy costs and government export restrictions.

But if you agree with the monetarists that inflation is caused by the expansion of money and credit, then until people and governments have paid-down (or defaulted) enough debt to feel confident about spending again, we are in a deflationary environment and whoever holds money is going to do well.

That said, there is a subset of monetarists who think that somehow, governments will force-feed money into the system to create inflation, or hyperinflation.

While this is technically possible, people like Mike Shedlock counter that the ruling elite will not allow this to happen, since it would destroy their wealth.

It's a rigged game, not Russian roulette. So barring some catastrophic default, we've got to sweat it out through a new Depression era.

Save money.

"Commercial real estate lags residential and residential real estate has not yet bottomed, and indeed may not bottom for years." - Mike Shedlock

"The most important indicator is “credit growth” or lack thereof. Everything else follows... There is no credit growth, and therefore, according to my long-standing theory, there can be no sustainable economic growth unless and until miraculously credit starts growing. However, given current policies in Washington, that seems unlikely at this time." - Bert Dohmen (htp: Karl Denninger)

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

But if you agree with the monetarists that inflation is caused by the expansion of money and credit, then until people and governments have paid-down (or defaulted) enough debt to feel confident about spending again, we are in a deflationary environment and whoever holds money is going to do well.

That said, there is a subset of monetarists who think that somehow, governments will force-feed money into the system to create inflation, or hyperinflation.

While this is technically possible, people like Mike Shedlock counter that the ruling elite will not allow this to happen, since it would destroy their wealth.

It's a rigged game, not Russian roulette. So barring some catastrophic default, we've got to sweat it out through a new Depression era.

Save money.

"Commercial real estate lags residential and residential real estate has not yet bottomed, and indeed may not bottom for years." - Mike Shedlock

"The most important indicator is “credit growth” or lack thereof. Everything else follows... There is no credit growth, and therefore, according to my long-standing theory, there can be no sustainable economic growth unless and until miraculously credit starts growing. However, given current policies in Washington, that seems unlikely at this time." - Bert Dohmen (htp: Karl Denninger)

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sunday, September 12, 2010

Future issues

White collar work in the West is threatened by lightspeed worldwide communication with countries where wage rates are dramatically lower; and by increasingly powerful computers and programs.

When all but manual and menial work simply and permanently isn't there anymore for very large numbers of people, the moral connexion between work and income is weakened. The issue then will be distribution of wealth: who gets given what, and with what justification?

The embers of socialism are still hot.

When all but manual and menial work simply and permanently isn't there anymore for very large numbers of people, the moral connexion between work and income is weakened. The issue then will be distribution of wealth: who gets given what, and with what justification?

The embers of socialism are still hot.

Stunt preachers

You could almost believe that Pastor Terry Jones and Imam Feisal Abdul Rauf are in cahoots over the controversial Park51/Cordoba House project.

The former is an ex-hotel manager whose sister church cut ties after allegations of his financial impropriety, and who preaches to a congregation of maybe 50 people. His I'll-burn-the-Koran stunt has made a nobody into a somebody.

The latter has allegedly "dedicated his life to building bridges between Muslims and the West and is a leader in the effort to build religious pluralism and integrate Islam into modern society", but his company Cordoba Initiative has a stake in the Park51 project and the recent publicity, athough temporarily polarizing opinion, may ultimately turn out to have been financially useful. Donald Trump reckons so - and he's looking to buy in without getting squeezed for too much extra cash.

It's enough to make a cat laugh.

The former is an ex-hotel manager whose sister church cut ties after allegations of his financial impropriety, and who preaches to a congregation of maybe 50 people. His I'll-burn-the-Koran stunt has made a nobody into a somebody.

The latter has allegedly "dedicated his life to building bridges between Muslims and the West and is a leader in the effort to build religious pluralism and integrate Islam into modern society", but his company Cordoba Initiative has a stake in the Park51 project and the recent publicity, athough temporarily polarizing opinion, may ultimately turn out to have been financially useful. Donald Trump reckons so - and he's looking to buy in without getting squeezed for too much extra cash.

It's enough to make a cat laugh.

Thursday, September 09, 2010

Goldmans Sachs "fine"

Goldman Sachs is going to pay £20 million to the FSA, says the news. That's not a fine, it's a tip.

Tuesday, September 07, 2010

Should retirees look to the stockmarket for income?

Adapted from my advice to a client this weekend:

Price inflation is not uniform or universal. Food and fuel have risen in cost recently, but State Pension benefits are linked to a cost of living index and should therefore approximately keep pace with increases in the price of basic needs.

In other areas (e.g. cars, cruises) prices have remained stable or even fallen. During what I suspect will turn out to be a long, Japan-style recession, it may be that the price of luxury goods and services will not inflate greatly, except perhaps for the luxuries of the very wealthiest.

Other than cash, what other ways could you invest?

First, one could look at deposits that link to inflation indices. Unfortunately, NS&I recently withdrew their index-linked savings certificates, the first time they have done so in 35 years. National Counties Building Society has an RPI-linked cash ISA (available until 30 September) but this is for a fixed amount (£5,100), runs for a fixed 5 year term and does not permit earlier withdrawals, so it may not fit in with your requirements.

If the government issues new index-linked gilts, these provide income and capital growth in line with RPI. The initial income may be low, however. For further details, please see the website of the Debt Management Office or a stockbroker. Generally, I would not now strongly recommend government bonds on the second-hand market, because the demand for them has become so high in these troubled times that the yield (ratio of income to traded price) is very low. If public finances unravel and interest rates rise, the effect on the capital value of bonds would be very depressing. As it is, the UK is struggling to maintain its official AAA rating and the implied credit rating on the credit default insurance market is actually rather lower already.**

Residential property appears still to be overpriced in historical terms. I think the only reason prices haven’t fallen much further is that interest rates are very low, which allows homeowners to maintain their mortgage payments on large loans. As the budget cuts begin to take effect, I think we will also see a depression in commercial real estate.

The stock market is also in a bubble, I believe. The ratio of price to earnings is still very high and the earnings may not truly reflect the forward position*. Companies are reportedly maintaining some degree of profitability by running down stocks, closing sites and laying off staff, but there is only so far they can go down this road. Many leading companies derive a significant part of their earnings overseas, but world trade is so interconnected these days that a slowdown in Western consumption will also impact on Eastern production.

The general picture appears to be deflationary, and although governments would like to stimulate further inflation in the way they have done over the past 30 years, there are respected economic and investment commentators who say we are now saturated with debt and unless we see outright defaults by sovereign nations (which could still happen), we will have to go through a long and painful process of retrenchment and paying-off debt.

Others look beyond deflation and think that it will ultimately force governments to find some way to increase the monetary base and devalue their currency. It may be significant that both Russia and China have made substantial purchases of gold in the last few months, and China has announced its intention of increasing her holding from c. 1,000 tonnes to six or ten times that amount in the next decade. But here we are in the realms of financial speculation, and the inflation speculators are already buying into agricultural commodities, precious metals, oil etc.

However, extreme or unconventional government strategies to deal with deflation don’t seem imminent and so I think that over the next couple of years, cash savings are likely to be a good way to build up funds for your envisaged discretionary expenditure***. Should there appear to be a major policy change, then we may have to look at investments that could protect against high inflation.

* Albert Edwards at SocGen expects a major reversal, the FT reports today.

** Though CMA DataVision have raised the UK from aa to aa+ in their Q2 report.

*** "There are no longer any “defensive” securities on the planet. The old asset allocation models and the diversification models don’t and won’t work any more and they haven’t for over a decade. I can’t believe that prominent asset managers are still using this approach." - Steven Bauer

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Price inflation is not uniform or universal. Food and fuel have risen in cost recently, but State Pension benefits are linked to a cost of living index and should therefore approximately keep pace with increases in the price of basic needs.

In other areas (e.g. cars, cruises) prices have remained stable or even fallen. During what I suspect will turn out to be a long, Japan-style recession, it may be that the price of luxury goods and services will not inflate greatly, except perhaps for the luxuries of the very wealthiest.

Other than cash, what other ways could you invest?

First, one could look at deposits that link to inflation indices. Unfortunately, NS&I recently withdrew their index-linked savings certificates, the first time they have done so in 35 years. National Counties Building Society has an RPI-linked cash ISA (available until 30 September) but this is for a fixed amount (£5,100), runs for a fixed 5 year term and does not permit earlier withdrawals, so it may not fit in with your requirements.

If the government issues new index-linked gilts, these provide income and capital growth in line with RPI. The initial income may be low, however. For further details, please see the website of the Debt Management Office or a stockbroker. Generally, I would not now strongly recommend government bonds on the second-hand market, because the demand for them has become so high in these troubled times that the yield (ratio of income to traded price) is very low. If public finances unravel and interest rates rise, the effect on the capital value of bonds would be very depressing. As it is, the UK is struggling to maintain its official AAA rating and the implied credit rating on the credit default insurance market is actually rather lower already.**

Residential property appears still to be overpriced in historical terms. I think the only reason prices haven’t fallen much further is that interest rates are very low, which allows homeowners to maintain their mortgage payments on large loans. As the budget cuts begin to take effect, I think we will also see a depression in commercial real estate.

The stock market is also in a bubble, I believe. The ratio of price to earnings is still very high and the earnings may not truly reflect the forward position*. Companies are reportedly maintaining some degree of profitability by running down stocks, closing sites and laying off staff, but there is only so far they can go down this road. Many leading companies derive a significant part of their earnings overseas, but world trade is so interconnected these days that a slowdown in Western consumption will also impact on Eastern production.

The general picture appears to be deflationary, and although governments would like to stimulate further inflation in the way they have done over the past 30 years, there are respected economic and investment commentators who say we are now saturated with debt and unless we see outright defaults by sovereign nations (which could still happen), we will have to go through a long and painful process of retrenchment and paying-off debt.

Others look beyond deflation and think that it will ultimately force governments to find some way to increase the monetary base and devalue their currency. It may be significant that both Russia and China have made substantial purchases of gold in the last few months, and China has announced its intention of increasing her holding from c. 1,000 tonnes to six or ten times that amount in the next decade. But here we are in the realms of financial speculation, and the inflation speculators are already buying into agricultural commodities, precious metals, oil etc.

However, extreme or unconventional government strategies to deal with deflation don’t seem imminent and so I think that over the next couple of years, cash savings are likely to be a good way to build up funds for your envisaged discretionary expenditure***. Should there appear to be a major policy change, then we may have to look at investments that could protect against high inflation.

* Albert Edwards at SocGen expects a major reversal, the FT reports today.

** Though CMA DataVision have raised the UK from aa to aa+ in their Q2 report.

*** "There are no longer any “defensive” securities on the planet. The old asset allocation models and the diversification models don’t and won’t work any more and they haven’t for over a decade. I can’t believe that prominent asset managers are still using this approach." - Steven Bauer

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Kitten climbs Matterhorn

From the Times of London, 60 years ago today:

Mice? Here? Or do they mean (as I hope) that he got back to the hotel in Zermatt?*

* Now (and maybe even then) known as the Hotel Bella Vista, I think. I thought the Times was authoritative?

Simplify and survive

Kunstler:

Let me tell you exactly what is going on "out there." The so-called developed world is watching two giant forces race each other to put an end to business-as-usual for industrial civilization. These two forces are the catastrophe of debt and predicament of oil supplies. They had been running neck-and-neck for a few years, but now the catastrophe of debt is pulling slightly ahead. But even this is an illusion because these two forces are actually hitched in tandem, with the rickety cart of civilization bouncing perilously behind them, and whatever one of these forces does will affect the other. Bad debt will eventually cripple the global oil industry's ability to perform, and the failures of the oil industry will only amplify the killing force of debt. It's that simple.

And the simple moral of the story is that the only sane thing America can do is simplify itself, de-complexify its dangerously hyper-complex organs of daily life. I've stated them before but, briefly, this means simplifying the way we do farming, commerce, transportation, inhabiting the landscape, schooling, medicine, and banking. Everything we do to add additional layers of complexity to these already tottering systems will guarantee an eventual orgy of blood and material destruction to this land. Everything we do to prop up the unsustainable instead of reconstructing the armatures of everyday life will make American life a nightmare in a very few years ahead.

Wish he'd explain the how behind "Bad debt will eventually cripple the global oil industry's ability to perform" (inebriated by the exuberance of his own verbosity, as Disraeli said of Gladstone?) but he's trying to see into the heart of the matter.

Let me tell you exactly what is going on "out there." The so-called developed world is watching two giant forces race each other to put an end to business-as-usual for industrial civilization. These two forces are the catastrophe of debt and predicament of oil supplies. They had been running neck-and-neck for a few years, but now the catastrophe of debt is pulling slightly ahead. But even this is an illusion because these two forces are actually hitched in tandem, with the rickety cart of civilization bouncing perilously behind them, and whatever one of these forces does will affect the other. Bad debt will eventually cripple the global oil industry's ability to perform, and the failures of the oil industry will only amplify the killing force of debt. It's that simple.

And the simple moral of the story is that the only sane thing America can do is simplify itself, de-complexify its dangerously hyper-complex organs of daily life. I've stated them before but, briefly, this means simplifying the way we do farming, commerce, transportation, inhabiting the landscape, schooling, medicine, and banking. Everything we do to add additional layers of complexity to these already tottering systems will guarantee an eventual orgy of blood and material destruction to this land. Everything we do to prop up the unsustainable instead of reconstructing the armatures of everyday life will make American life a nightmare in a very few years ahead.

Wish he'd explain the how behind "Bad debt will eventually cripple the global oil industry's ability to perform" (inebriated by the exuberance of his own verbosity, as Disraeli said of Gladstone?) but he's trying to see into the heart of the matter.

Monday, September 06, 2010

The Hitchhiker's Guide to... British politics

We've had ten years of Zaphod Beeblebrox, followed by three years of Marvin the Paranoid Android. Now we're controlled by the two ruthless, multidimensional white mice.

Don't panic.

Don't panic.

Tuesday, August 31, 2010

What James Bond can teach us about sex and money

When gender testing first came to the Olympics in 1966, Ukrainian track and field stars Tamara and Irina Press disappeared from the sports scene. Yet the methodology is still disputed.

I'd like to suggest a quicker and easier test: identifying movie preferences.

Generally speaking, women love films about loss and self-sacrifice (Love Story, Casablanca) whereas men prefer stories of conflict and victory, especially where the hero easily destroys hosts of enemies (James Bond, Arnold Schwarzenegger). For women, tear-jerkers; for men, jerk-tearers.

But don't look down your noses at 007, ladies: Bond has much to teach us about the world. Last night I watched the remake of "Casino Royale", starring Daniel Craig. In this yarn, the superspy ruins his arch-enemy in a high-stakes poker game with a pot of $150 million. When the spoils are stolen, he recovers them in a shootout in Venice that involves sinking a whole building into the marshes.

It's prescient: a movie from 2006 about financial speculation ending in a housing collapse.

There's a further lesson. When you have won all the chips on the table, you don't give them back to your competitors; you stand up and walk away. So it is with investment: now that a tiny elite has cornered most of the income and capital, why on earth would they re-enter the market?

I'd like to suggest a quicker and easier test: identifying movie preferences.

Generally speaking, women love films about loss and self-sacrifice (Love Story, Casablanca) whereas men prefer stories of conflict and victory, especially where the hero easily destroys hosts of enemies (James Bond, Arnold Schwarzenegger). For women, tear-jerkers; for men, jerk-tearers.

But don't look down your noses at 007, ladies: Bond has much to teach us about the world. Last night I watched the remake of "Casino Royale", starring Daniel Craig. In this yarn, the superspy ruins his arch-enemy in a high-stakes poker game with a pot of $150 million. When the spoils are stolen, he recovers them in a shootout in Venice that involves sinking a whole building into the marshes.

It's prescient: a movie from 2006 about financial speculation ending in a housing collapse.

There's a further lesson. When you have won all the chips on the table, you don't give them back to your competitors; you stand up and walk away. So it is with investment: now that a tiny elite has cornered most of the income and capital, why on earth would they re-enter the market?

Monday, August 30, 2010

Killer facts about Prohibition in the USA (1919 - 1933)

The 18th Amendment to the US Constitution allowed you to continue using alcohol, and also to make it for your own consumption. What was prohibited was its commercial manufacture and distribution.

As a result, cirrhosis death rates for men dropped by two-thirds. Admissions to state mental hospitals for alcoholic psychosis halved. The homicide rate, which had soared between 1900 and 1910, did not increase significantly during Prohibition.

Prohibition was ended in order to raise taxes for the Federal Government. It was supported by labor unions and wealthy industrialists.

The 21st Amendment, which repealed the 18th Amendment, made unregulated imports of alcohol illegal.

During Prohibition, national alcohol consumption decreased by an estimated 30 - 50%. After repeal, it increased. In 1989, alcohol was implicated in over 50% of homicides (and drugs in 10 - 20% of them). Alcohol was then also believed to be the cause of over 23,000 motor vehicle deaths - more than twice the number of drink-related homicides.

Iceland banned beer for 73 years (1915 - 1988). But for the first thirty years of its existence, Pakistan allowed the free sale and consumption of alcohol; restrictions were only introduced in 1977.

As a result, cirrhosis death rates for men dropped by two-thirds. Admissions to state mental hospitals for alcoholic psychosis halved. The homicide rate, which had soared between 1900 and 1910, did not increase significantly during Prohibition.

Prohibition was ended in order to raise taxes for the Federal Government. It was supported by labor unions and wealthy industrialists.

The 21st Amendment, which repealed the 18th Amendment, made unregulated imports of alcohol illegal.

During Prohibition, national alcohol consumption decreased by an estimated 30 - 50%. After repeal, it increased. In 1989, alcohol was implicated in over 50% of homicides (and drugs in 10 - 20% of them). Alcohol was then also believed to be the cause of over 23,000 motor vehicle deaths - more than twice the number of drink-related homicides.

Iceland banned beer for 73 years (1915 - 1988). But for the first thirty years of its existence, Pakistan allowed the free sale and consumption of alcohol; restrictions were only introduced in 1977.

Saturday, August 28, 2010

Hands off the raggle-taggle gypsies

I was, I don't know, six. The teacher asked brightly what we knew about gypsies. Ever eager to show off my knowledge, I stood up and said they stole children. I don't know what story I'd got that from.

Half a century later and we're still giving them prejudice. Dirty thieves etc. France is moving them on; in Istanbul, they're knocking down and rebuilding houses as "transformation projects" and offering the romanies the chance to buy the new houses (which they can't afford) or fresh rentals 40 kilometres away. These people, ironically, had been among the first to abandon their ancient nomadic life.

Here's a couple of gypsy blogs: Pesha's blog and Clearwater Gypsies.

And for those who missed it, here's the recent Channel 4 programme "My Big Fat Gypsy Wedding". A community where even the tough guys fear God and the girls are chaste until they marry.

I've never been happier than when leaving somewhere.

Half a century later and we're still giving them prejudice. Dirty thieves etc. France is moving them on; in Istanbul, they're knocking down and rebuilding houses as "transformation projects" and offering the romanies the chance to buy the new houses (which they can't afford) or fresh rentals 40 kilometres away. These people, ironically, had been among the first to abandon their ancient nomadic life.

Here's a couple of gypsy blogs: Pesha's blog and Clearwater Gypsies.

And for those who missed it, here's the recent Channel 4 programme "My Big Fat Gypsy Wedding". A community where even the tough guys fear God and the girls are chaste until they marry.

I've never been happier than when leaving somewhere.

Great music

Several Bloghounds members have been offering musical selections. Try listening to the Al Andaluz Project - seven of their tracks are available to click on. I heard something by them on R3's "World Routes" a fortnight ago.

From the same programme I heard Marko Markovitch's tremendously vibrant jazz band. You can't get it on iPlayer but here's a site with samples, and here's "Romany wedding" which would make even the lame dance.

BOBAN MARKOVIC-RROMANO BIJAV-LA BELLEVILLOISE

Uploaded by aceituna11. - Watch more music videos, in HD!

From the same programme I heard Marko Markovitch's tremendously vibrant jazz band. You can't get it on iPlayer but here's a site with samples, and here's "Romany wedding" which would make even the lame dance.

BOBAN MARKOVIC-RROMANO BIJAV-LA BELLEVILLOISE

Uploaded by aceituna11. - Watch more music videos, in HD!

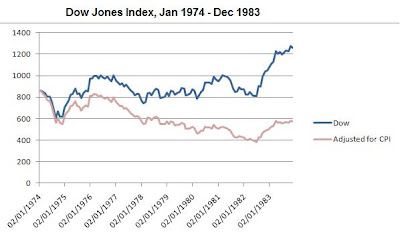

A response to "Capitalists@Work"

"City Unslicker" has posted a feelgood piece and entitled it "Bearwatch". If this is intended as a tease, looking sideways at my first blog which started three years ago and forewarned of the credit crunch*, banking collapse etc, then it's worked. Not that I claim any wisdom, but a strong gut feeling got me looking around for sources of information other than the useless Press.

Perhaps I should feel flattered that anyone from stockbroking or banking pays me any attention; or maybe it's just a naming coincidence. Nevertheless, here is my reply: you experts can be both right and wrong at the same time.

I'd like to have made a graph for the FTSE over the period I think we should be looking at, but that index only started in 1984. Besides, ours is a mixed economy, doing the hokey-cokey between privatisation and nationalisation, so it's very difficult to discern the reality underlying all the fudge.

So instead, here's the history of the US stockmarket "boom" of 1974. The blue line is the nominal index, and then I reinterpret the figures in the light of the Consumer Price Index. We start at the beginning of 1974 and continue for 10 years.

*"a systemic risk that could have really serious consequences is the possibility of a major failure in the mortgage and credit markets, which could then roll on to the banking sector." - 31 July 2007

*"a systemic risk that could have really serious consequences is the possibility of a major failure in the mortgage and credit markets, which could then roll on to the banking sector." - 31 July 2007

Perhaps I should feel flattered that anyone from stockbroking or banking pays me any attention; or maybe it's just a naming coincidence. Nevertheless, here is my reply: you experts can be both right and wrong at the same time.

I'd like to have made a graph for the FTSE over the period I think we should be looking at, but that index only started in 1984. Besides, ours is a mixed economy, doing the hokey-cokey between privatisation and nationalisation, so it's very difficult to discern the reality underlying all the fudge.

So instead, here's the history of the US stockmarket "boom" of 1974. The blue line is the nominal index, and then I reinterpret the figures in the light of the Consumer Price Index. We start at the beginning of 1974 and continue for 10 years.

*"a systemic risk that could have really serious consequences is the possibility of a major failure in the mortgage and credit markets, which could then roll on to the banking sector." - 31 July 2007

*"a systemic risk that could have really serious consequences is the possibility of a major failure in the mortgage and credit markets, which could then roll on to the banking sector." - 31 July 2007DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Friday, August 27, 2010

A green query

Are designer eco-homes more environmentally friendly than not building them?

As Scott Adams says:

The greenest home is the one you don't build. If you really want to save the Earth, move in with another family and share a house that's already built. Better yet, live in the forest and eat whatever the squirrels don't want. Don't brag to me about riding your bicycle to work; a lot of energy went into building that bicycle. Stop being a hypocrite like me.

I prefer a more pragmatic definition of green. I think of it as living the life you want, with as much Earth-wise efficiency as your time and budget reasonably allow.

Is the well-heeled greenie not unlike Marie Antoinette, tending her washed (and "heavily perfumed") sheep in a sylvan fantasy?

I'm only jealous, of course. I can't wait to join the middle-class lotus eaters, as soon as my Lotto ticket pays out the Big One.

As Scott Adams says:

The greenest home is the one you don't build. If you really want to save the Earth, move in with another family and share a house that's already built. Better yet, live in the forest and eat whatever the squirrels don't want. Don't brag to me about riding your bicycle to work; a lot of energy went into building that bicycle. Stop being a hypocrite like me.

I prefer a more pragmatic definition of green. I think of it as living the life you want, with as much Earth-wise efficiency as your time and budget reasonably allow.

Is the well-heeled greenie not unlike Marie Antoinette, tending her washed (and "heavily perfumed") sheep in a sylvan fantasy?

I'm only jealous, of course. I can't wait to join the middle-class lotus eaters, as soon as my Lotto ticket pays out the Big One.

Underneath the headlines, debt continues to increase

There's much argument on the wires about the issue of inflation vs deflation. As James Quinn points out, the mainstream media aren't helping much because if they comment at all, they may still misunderstand what they're reporting. The official figures appear to show that debt in the US is reducing, but this needs to be reinterpreted in the light of write-offs:

If consumer debt was $13.8 trillion at the end of 2008 and the banks have since written off 5.66% of that debt, total write-offs were $800 billion. If total consumer debt now sits at $13.5 trillion, then consumers have actually taken on $500 billion of additional debt since the end of 2008. The consumer hasn’t cut back at all. They are still spending and borrowing. It is beyond my comprehension that no one on CNBC or in the other mainstream media can do simple math to figure out that the deleveraging story is just a Big Lie.

Reading around, it seems that a lot of credit card debt has been written-off, but better-risk customers may be increasing their usage, especially business owners (perhaps finding a way around the dearth in other forms of bank lending):

Credit cards are now the most common source of financing for America’s small-business owners. (Source: National Small Business Association survey, 2008)

44 percent of small-business owners identified credit cards as a source of financing that their company had used in the previous 12 months —- more than any other source of financing, including business earnings. In 1993, only 16 percent of small-businesses owners identified credit cards as a source of funding they had used in the preceding 12 months. (Source: National Small Business Association survey, 2008)

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

If consumer debt was $13.8 trillion at the end of 2008 and the banks have since written off 5.66% of that debt, total write-offs were $800 billion. If total consumer debt now sits at $13.5 trillion, then consumers have actually taken on $500 billion of additional debt since the end of 2008. The consumer hasn’t cut back at all. They are still spending and borrowing. It is beyond my comprehension that no one on CNBC or in the other mainstream media can do simple math to figure out that the deleveraging story is just a Big Lie.

Reading around, it seems that a lot of credit card debt has been written-off, but better-risk customers may be increasing their usage, especially business owners (perhaps finding a way around the dearth in other forms of bank lending):

Credit cards are now the most common source of financing for America’s small-business owners. (Source: National Small Business Association survey, 2008)

44 percent of small-business owners identified credit cards as a source of financing that their company had used in the previous 12 months —- more than any other source of financing, including business earnings. In 1993, only 16 percent of small-businesses owners identified credit cards as a source of funding they had used in the preceding 12 months. (Source: National Small Business Association survey, 2008)

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Gold up, shares down?

Hot on the heels of China, which has recently increased its gold hoard to over 1,000 tonnes and intends to accumulate far more, comes Russia, which has acquired an extra 10% in the last seven months.

This is at a time when the wealthy are turning pessimistic about the economy again. As I said two years ago, generally I now see newspapers as useless, except for tidbits like that: "Other than weather forecasts, the last usable information I can remember is from the summer of 1987, when I learned that Sir James Goldsmith had sold all his shares on the Paris Bourse, which confirmed my feelings about the way the market was going - but that item came from Private Eye magazine." The current pessimism is reflected not only in last night's close on the Dow (now below 10,000 again), but also in a surge in demand for safe government bonds, as "Jesse" reports.

I said a few days ago that the price of gold was well above its inflation-adjusted trend, but the interest of foreign countries, bearish millionaires and speculative funds boosted by cheaply borrowed money may keep the market buoyant for some time yet.

And I'm sure we'll all be watching the stockmarket with some interest this autumn.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

This is at a time when the wealthy are turning pessimistic about the economy again. As I said two years ago, generally I now see newspapers as useless, except for tidbits like that: "Other than weather forecasts, the last usable information I can remember is from the summer of 1987, when I learned that Sir James Goldsmith had sold all his shares on the Paris Bourse, which confirmed my feelings about the way the market was going - but that item came from Private Eye magazine." The current pessimism is reflected not only in last night's close on the Dow (now below 10,000 again), but also in a surge in demand for safe government bonds, as "Jesse" reports.

I said a few days ago that the price of gold was well above its inflation-adjusted trend, but the interest of foreign countries, bearish millionaires and speculative funds boosted by cheaply borrowed money may keep the market buoyant for some time yet.

And I'm sure we'll all be watching the stockmarket with some interest this autumn.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Gold up, shares down?

Hot on the heels of China, which has recently increased its gold hoard to over 1,000 tonnes and intends to accumulate far more, comes Russia, which has acquired an extra 10% in the last seven months.

This is at a time when the wealthy are turning pessimistic about the economy again. As I said two years ago, generally I now see newspapers as useless, except for tidbits like that: "Other than weather forecasts, the last usable information I can remember is from the summer of 1987, when I learned that Sir James Goldsmith had sold all his shares on the Paris Bourse, which confirmed my feelings about the way the market was going - but that item came from Private Eye magazine." The current pessimism is reflected not only in last night's close on the Dow (now below 10,000 again), but also in a surge in demand for safe government bonds, as "Jesse" reports.

I said a few days ago that the price of gold was well above its inflation-adjusted trend, but the interest of foreign countries, bearish millionaires and speculative funds boosted by cheaply borrowed money may keep the market buoyant for some time yet.

And I'm sure we'll all be watching the stockmarket with some interest this autumn.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

This is at a time when the wealthy are turning pessimistic about the economy again. As I said two years ago, generally I now see newspapers as useless, except for tidbits like that: "Other than weather forecasts, the last usable information I can remember is from the summer of 1987, when I learned that Sir James Goldsmith had sold all his shares on the Paris Bourse, which confirmed my feelings about the way the market was going - but that item came from Private Eye magazine." The current pessimism is reflected not only in last night's close on the Dow (now below 10,000 again), but also in a surge in demand for safe government bonds, as "Jesse" reports.

I said a few days ago that the price of gold was well above its inflation-adjusted trend, but the interest of foreign countries, bearish millionaires and speculative funds boosted by cheaply borrowed money may keep the market buoyant for some time yet.

And I'm sure we'll all be watching the stockmarket with some interest this autumn.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Thursday, August 26, 2010

Don't look at the FTSE, all is NOT well here

Gary Dorsch points out that the UK bond market is a better indicator of local economic conditions than the UK stockmarket:

FTSE-100 companies equal about 85% of the market capitalization of the London Stock Exchange, and nearly half the companies are headquartered outside the UK. Roughly one-third of the FTSE is concentrated in the natural resource sector. Thus, the Footsie is viewed as a global bellwether rather than a reflection of the state of the British economy.

Right now the sharp downward trajectory of UK gilt yields is flashing warning signals of a sharp downturn in the British economy, which could trigger deflation in wages and UK home prices.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

FTSE-100 companies equal about 85% of the market capitalization of the London Stock Exchange, and nearly half the companies are headquartered outside the UK. Roughly one-third of the FTSE is concentrated in the natural resource sector. Thus, the Footsie is viewed as a global bellwether rather than a reflection of the state of the British economy.

Right now the sharp downward trajectory of UK gilt yields is flashing warning signals of a sharp downturn in the British economy, which could trigger deflation in wages and UK home prices.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Wednesday, August 25, 2010

Time to invest in helium?

One for the commodity punters: the Daily Mail reports on the potential price boom in helium:

The world's biggest store of helium - the most commonly used inert gas - lies in a disused airfield in Amarillo, Texas, and is being sold off far too cheaply.

But in 1996, the US government passed a law which states that the facility - the US National Helium Reserve - must be completely sold off by 2015 to recoup the price of installing it.

This means that the helium, a non-renewable gas, is being quickly sold off at increasingly cheap prices, making it uneconomical to recycle [...] The US stores around 80 per cent of the world's helium and so its decision to let it go at an extremely low price has a massive knock-on effect on its market. [...] The only way to obtain more helium would be to capture it from the decay of tritium - a radioactive hydrogen isotope, which the U.S. stopped making in 1988.

The article says that because of the too-low price, it's being used very much faster than it can be replaced and reserves will be used up in 25 years. Professor Robert Richardson of Cornell University is arguing for a return to the free market in this commodity.

According to this site, major companies supplying helium in the US are Air Products (NYSE: APD) and Praxair (NYSE:PX).

Too exciting for me as an investor, and besides I don't know when in the next 25 years the market surge might start, if at all. But it's another story in the saga of finite world resources.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

The world's biggest store of helium - the most commonly used inert gas - lies in a disused airfield in Amarillo, Texas, and is being sold off far too cheaply.

But in 1996, the US government passed a law which states that the facility - the US National Helium Reserve - must be completely sold off by 2015 to recoup the price of installing it.

This means that the helium, a non-renewable gas, is being quickly sold off at increasingly cheap prices, making it uneconomical to recycle [...] The US stores around 80 per cent of the world's helium and so its decision to let it go at an extremely low price has a massive knock-on effect on its market. [...] The only way to obtain more helium would be to capture it from the decay of tritium - a radioactive hydrogen isotope, which the U.S. stopped making in 1988.

The article says that because of the too-low price, it's being used very much faster than it can be replaced and reserves will be used up in 25 years. Professor Robert Richardson of Cornell University is arguing for a return to the free market in this commodity.

According to this site, major companies supplying helium in the US are Air Products (NYSE: APD) and Praxair (NYSE:PX).

Too exciting for me as an investor, and besides I don't know when in the next 25 years the market surge might start, if at all. But it's another story in the saga of finite world resources.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sunday, August 22, 2010

When will the bear market end? How bad will it get?

Tim W. Wood at Financial Sense reckons the last bull market ran from 1974 to 2007 (extended by government interference or support, depending on your point of view). His research tells him that bear markets last one-third as long as the preceding bull market, so he sees the present stockmarket rally as a "dead cat bounce".

That's my gut feeling, too, though I'm aware of the dangers of confirmation bias.

Below, I give two charts showing the course of the Dow from August 1929 (close to its pre-Crash peak) to August 2010, 82 years later. The first shows the raw index, which as you see only breached the 2,000 mark in the late 80s, making the last 20 years look freakish.

The second adjusts the Dow for inflation as measured by the CPI, so we can see where we are "in real terms" in comparison to the great speculative bull market of the late 1920s. Note that the recent low point (March 2009) is above the high point of the bull run that ended in January 1966, whereas the low of June 1982 was less than 40% of the 1929 peak.

If the eventual market bottom this time has the same relationship to the 1966 peak, as 1982 had to 1929, the Dow should go below 5,200 points (adjusted for inflation between now and the future low point).

So much has changed over the last 3 generations that the attempt to turn historical data into predictable cycles may be fruitless. On the one hand, debt is now an even greater burden than in 1929; on the other, big companies are multinational and the fortunes of Wall Street are less bound up with those of Main Street.

Yet global trade means that the fortunes of sovereign nations are increasingly interconnected, and while China is set to overtake Japan in size of economy, it is also (apparently) heading for a Western-style banking bust; should China choose to raid its overseas investments to tackle such a crisis, then the American markets (where China holds over $1 trillion of assets) are in trouble.

I still feel that a major breakdown is on the way, I just don't know exactly when. It's like waiting for the Big One in California: every day it's "not today", yet it's never "never".

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

That's my gut feeling, too, though I'm aware of the dangers of confirmation bias.

Below, I give two charts showing the course of the Dow from August 1929 (close to its pre-Crash peak) to August 2010, 82 years later. The first shows the raw index, which as you see only breached the 2,000 mark in the late 80s, making the last 20 years look freakish.

The second adjusts the Dow for inflation as measured by the CPI, so we can see where we are "in real terms" in comparison to the great speculative bull market of the late 1920s. Note that the recent low point (March 2009) is above the high point of the bull run that ended in January 1966, whereas the low of June 1982 was less than 40% of the 1929 peak.

If the eventual market bottom this time has the same relationship to the 1966 peak, as 1982 had to 1929, the Dow should go below 5,200 points (adjusted for inflation between now and the future low point).

So much has changed over the last 3 generations that the attempt to turn historical data into predictable cycles may be fruitless. On the one hand, debt is now an even greater burden than in 1929; on the other, big companies are multinational and the fortunes of Wall Street are less bound up with those of Main Street.

Yet global trade means that the fortunes of sovereign nations are increasingly interconnected, and while China is set to overtake Japan in size of economy, it is also (apparently) heading for a Western-style banking bust; should China choose to raid its overseas investments to tackle such a crisis, then the American markets (where China holds over $1 trillion of assets) are in trouble.

I still feel that a major breakdown is on the way, I just don't know exactly when. It's like waiting for the Big One in California: every day it's "not today", yet it's never "never".

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, August 21, 2010

Killer facts about the British standard of living

Average income in the UK is lower than in the Falkland Islands.

Iceland's per capita income is 14 rungs higher than ours.

Norwegians earn 2/3rds more than we do.

https://www.cia.gov/library/publications/the-world-factbook/rankorder/2004rank.html?countryName=Iceland&countryCode=ic®ionCode=eu&rank=20#ic

Iceland's per capita income is 14 rungs higher than ours.

Norwegians earn 2/3rds more than we do.

https://www.cia.gov/library/publications/the-world-factbook/rankorder/2004rank.html?countryName=Iceland&countryCode=ic®ionCode=eu&rank=20#ic

Gold, inflation and the Dow Jones Industrial Index

Republished from the Broad Oak Blog:

I give below two charts that look at how gold has fared since President Nixon de-linked it from the dollar in 1971. In inflation terms (as measured by the US CPI-U), gold now worth is almost twice as much as its long-term average; but in turn, the Dow is still running very high against gold.

I give below two charts that look at how gold has fared since President Nixon de-linked it from the dollar in 1971. In inflation terms (as measured by the US CPI-U), gold now worth is almost twice as much as its long-term average; but in turn, the Dow is still running very high against gold.

It may or may not be the case that gold is overpriced (perhaps we should be looking at inflation as measured by average earned income, or GDP, or something else) but either way, the Dow is still extraordinarily high. It does indeed look as though there was a "new paradigm" from the early 1990s; but perhaps a dangerously misleading one. Will gold double? Will the Dow halve?

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Gold, inflation and the Dow Jones Industrial Index

I give below two charts that look at how gold has fared since President Nixon de-linked it from the dollar in 1971. In inflation terms (as measured by the US CPI-U), gold now worth is almost twice as much as its long-term average; but in turn, the Dow is still running very high against gold.

It may or may not be the case that gold is overpriced (perhaps we should be looking at inflation as measured by average earned income, or GDP, or something else) but either way, the Dow is still extraordinarily high. It does indeed look as though there was a "new paradigm" from the early 1990s; but perhaps a dangerously misleading one. Will gold double? Will the Dow halve?

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Friday, August 20, 2010

Gold and Goldman Sachs

Republished from the Broad Oak Blog:

It appears that Goldman Sachs will simultaneously predict a rise in the value of gold, and a fall, depending on how valuable a client you are. Mind you, that could reflect the difference between the advice one gives to active traders as opposed to buy-and-holders, so it's not enough evidence to convict, I think.

I looked at gold's longer-term price history in February of last year, starting in 1971 when President Nixon finally severed the official link between the US dollar and the precious metal on which it used to be based. Since then, and adjusted for the American Consumer Price Index, gold has averaged 2.8 or 2.9 times its September 1971 price. I reproduce the graph below:

It appears that Goldman Sachs will simultaneously predict a rise in the value of gold, and a fall, depending on how valuable a client you are. Mind you, that could reflect the difference between the advice one gives to active traders as opposed to buy-and-holders, so it's not enough evidence to convict, I think.

I looked at gold's longer-term price history in February of last year, starting in 1971 when President Nixon finally severed the official link between the US dollar and the precious metal on which it used to be based. Since then, and adjusted for the American Consumer Price Index, gold has averaged 2.8 or 2.9 times its September 1971 price. I reproduce the graph below:

In September 1971, gold was trading at $42.02 per ounce, when the CPI index was at 40.8 . As I write, the New York spot price is $1,232.40 and July 2010's CPI figure is 218.011. So "in real terms" gold is now worth 5.49 times as much as in the autumn of 1971, i.e. nearly twice its long-term, inflation-adjusted trend.

In September 1971, gold was trading at $42.02 per ounce, when the CPI index was at 40.8 . As I write, the New York spot price is $1,232.40 and July 2010's CPI figure is 218.011. So "in real terms" gold is now worth 5.49 times as much as in the autumn of 1971, i.e. nearly twice its long-term, inflation-adjusted trend.

As I've said before, we're now not looking at gold as a "good buy" because it's undervalued, which it isn't (it was, 10 years ago). Instead, it's assuming its role as a form of insurance against economic breakdown. I've noted recently, as doubtless you have too, how shops and internet sites have been springing up, offering to buy your gold. There must be a reason - though remember that these purchasers often don't give you the full melt-down value of your jewelry, so there's a profit margin for them already.

It may be a sign of the times, but that also means that it's a temporary phenomenon. Unless you're willing to keep a sharp eye out for price movements and can sell fairly quickly when you have made a gain, perhaps you should keep out of this speculative market.

Unless you believe the future is rather more catastrophic. In that case, as some are now advising, you may wish to build up your personal holding of the imperishable element. But consider the ancient buried hoards that have been discovered over the last few years by people with metal detectors: presumably those ancients thought they'd come back for their goods, but were overtaken by events. If you really have the disaster-movie outlook, maybe there are other, more useful things you should be doing to ensure that you survive and thrive.

Gold and Goldman Sachs

It appears that Goldman Sachs will simultaneously predict a rise in the value of gold, and a fall, depending on how valuable a client you are. Mind you, that could reflect the difference between the advice one gives to active traders as opposed to buy-and-holders, so it's not enough evidence to convict, I think.

I looked at gold's longer-term price history in February of last year, starting in 1971 when President Nixon finally severed the official link between the US dollar and the precious metal on which it used to be based. Since then, and adjusted for the American Consumer Price Index, gold has averaged 2.8 or 2.9 times its September 1971 price. I reproduce the graph below:

I looked at gold's longer-term price history in February of last year, starting in 1971 when President Nixon finally severed the official link between the US dollar and the precious metal on which it used to be based. Since then, and adjusted for the American Consumer Price Index, gold has averaged 2.8 or 2.9 times its September 1971 price. I reproduce the graph below:

In September 1971, gold was trading at $42.02 per ounce, when the CPI index was at 40.8 . As I write, the New York spot price is $1,232.40 and July 2010's CPI figure is 218.011. So "in real terms" gold is now worth 5.49 times as much as in the autumn of 1971, i.e. nearly twice its long-term, inflation-adjusted trend.

As I've said before, we're now not looking at gold as a "good buy" because it's undervalued, which it isn't (it was, 10 years ago). Instead, it's assuming its role as a form of insurance against economic breakdown. I've noted recently, as doubtless you have too, how shops and internet sites have been springing up, offering to buy your gold. There must be a reason - though remember that these purchasers often don't give you the full melt-down value of your jewelry, so there's a profit margin for them already.

It may be a sign of the times, but that also means that it's a temporary phenomenon. Unless you're willing to keep a sharp eye out for price movements and can sell fairly quickly when you have made a gain, perhaps you should keep out of this speculative market.

Unless you believe the future is rather more catastrophic. In that case, as some are now advising, you may wish to build up your personal holding of the imperishable element. But consider the ancient buried hoards that have been discovered over the last few years by people with metal detectors: presumably those ancients thought they'd come back for their goods, but were overtaken by events. If you really have the disaster-movie outlook, maybe there are other, more useful things you should be doing to ensure that you survive and thrive.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Thursday, August 19, 2010

Beating inflation safely

Republished from the Broad Oak Blog:

UK investors who are concerned about the threat of inflation have recently (19 July) lost access to an ideal solution, the NS&I Index-Linked Savings Certificate. Now a building society is offering something to fill that gap in the market.

National Counties are marketing an index-linked cash ISA. This is not quite the same as NS&I's product, because the investment is for a fixed amount (the maximum cash ISA allowance, i.e. £5,100) and no withdrawals are permitted within the 5-year term of the plan. As with NS&I, the return is linked to the Retail Price Index (RPI), plus 1% p.a. For further comment by Citywire, see here.

A lot depends on what you think may happen in terms of inflation, which brings us to the great inflation-deflation debate. Some commentators are saying that Western economies are so indebted that we have reached a turning point and people will spend less and save more (or pay down debt, which amounts to the same thing). Governments are going to have to follow suit, and the UK government is currently busy trying to demonstrate its commitment to do so, fearing that bond markets may lose confidence in our financial management and will then charge higher interest, which would really put us in a pickle.

So demand is reducing. We see this in the recent bankruptcies of UK holiday companies and the pages of cut-price cruise adverts in the middle-class press. If this is the pattern generally, then holders of cash will benefit as prices reduce - the pound in your pocket will grow more valuable, quite safely. Even better, this type of deflationary gain is not taxed, at least not until the government nerves itself up to simply confiscate your savings.

But that's not the whole picture. While demand for luxuries is lessening, there are other things that we still have to buy, especially food and energy. Here, prices are rising. And if interest rates do rise, that will also increase RPI, which unlike the Consumer Price Index (CPI) includes housing costs. So it is quite possible that inflation as measured by RPI could be high, even as the economy slows down. It's worth noting that the government has recently changed rules on private sector occupational pensions so that their benefits will increase in line with CPI instead of RPI, which suggests that our rulers believe that one way or another, RPI will rise faster than CPI in years to come.

The BBC appears to have bought the official line that we should ignore food and energy costs, referring to CPI as "core" inflation and noting that it's now a mere 3.1%, as opposed to RPI which is running at 4.8%. However, unlike the mandarins at Broadcasting House, the rest of us need to eat and keep warm; or, to be a little fairer, food and energy is a more significant part of most people's budgets than it is for the upper echelon of the mediaocrities.

An RPI-linked cash product is a good each-way bet: if prices do reduce, then your money becomes more valuable; if prices increase, the value of your savings is preserved; and either way, you benefit from that extra 1% p.a. sweetener.

Reasons not to? You may find you need access to cash within the 5 year term; and if you're a gambler, you may be looking at investments that could outpace inflation (think of the current fever for commodities such as gold, silver, oil and agricultural products). But you shouldn't put all your eggs in one basket, and most ordinary people aren't gamblers when it comes to their nest-eggs, so this product is worth a look.

UK investors who are concerned about the threat of inflation have recently (19 July) lost access to an ideal solution, the NS&I Index-Linked Savings Certificate. Now a building society is offering something to fill that gap in the market.

National Counties are marketing an index-linked cash ISA. This is not quite the same as NS&I's product, because the investment is for a fixed amount (the maximum cash ISA allowance, i.e. £5,100) and no withdrawals are permitted within the 5-year term of the plan. As with NS&I, the return is linked to the Retail Price Index (RPI), plus 1% p.a. For further comment by Citywire, see here.

A lot depends on what you think may happen in terms of inflation, which brings us to the great inflation-deflation debate. Some commentators are saying that Western economies are so indebted that we have reached a turning point and people will spend less and save more (or pay down debt, which amounts to the same thing). Governments are going to have to follow suit, and the UK government is currently busy trying to demonstrate its commitment to do so, fearing that bond markets may lose confidence in our financial management and will then charge higher interest, which would really put us in a pickle.

So demand is reducing. We see this in the recent bankruptcies of UK holiday companies and the pages of cut-price cruise adverts in the middle-class press. If this is the pattern generally, then holders of cash will benefit as prices reduce - the pound in your pocket will grow more valuable, quite safely. Even better, this type of deflationary gain is not taxed, at least not until the government nerves itself up to simply confiscate your savings.

But that's not the whole picture. While demand for luxuries is lessening, there are other things that we still have to buy, especially food and energy. Here, prices are rising. And if interest rates do rise, that will also increase RPI, which unlike the Consumer Price Index (CPI) includes housing costs. So it is quite possible that inflation as measured by RPI could be high, even as the economy slows down. It's worth noting that the government has recently changed rules on private sector occupational pensions so that their benefits will increase in line with CPI instead of RPI, which suggests that our rulers believe that one way or another, RPI will rise faster than CPI in years to come.

The BBC appears to have bought the official line that we should ignore food and energy costs, referring to CPI as "core" inflation and noting that it's now a mere 3.1%, as opposed to RPI which is running at 4.8%. However, unlike the mandarins at Broadcasting House, the rest of us need to eat and keep warm; or, to be a little fairer, food and energy is a more significant part of most people's budgets than it is for the upper echelon of the mediaocrities.

An RPI-linked cash product is a good each-way bet: if prices do reduce, then your money becomes more valuable; if prices increase, the value of your savings is preserved; and either way, you benefit from that extra 1% p.a. sweetener.

Reasons not to? You may find you need access to cash within the 5 year term; and if you're a gambler, you may be looking at investments that could outpace inflation (think of the current fever for commodities such as gold, silver, oil and agricultural products). But you shouldn't put all your eggs in one basket, and most ordinary people aren't gamblers when it comes to their nest-eggs, so this product is worth a look.

Beating inflation safely

UK investors who are concerned about the threat of inflation have recently (19 July) lost access to an ideal solution, the NS&I Index-Linked Savings Certificate. Now a building society is offering something to fill that gap in the market.

National Counties are marketing an index-linked cash ISA. This is not quite the same as NS&I's product, because the investment is for a fixed amount (the maximum cash ISA allowance, i.e. £5,100) and no withdrawals are permitted within the 5-year term of the plan. As with NS&I, the return is linked to the Retail Price Index (RPI), plus 1% p.a. For further comment by Citywire, see here.

A lot depends on what you think may happen in terms of inflation, which brings us to the great inflation-deflation debate. Some commentators are saying that Western economies are so indebted that we have reached a turning point and people will spend less and save more (or pay down debt, which amounts to the same thing). Governments are going to have to follow suit, and the UK government is currently busy trying to demonstrate its commitment to do so, fearing that bond markets may lose confidence in our financial management and will then charge higher interest, which would really put us in a pickle.

So demand is reducing. We see this in the recent bankruptcies of UK holiday companies and the pages of cut-price cruise adverts in the middle-class press. If this is the pattern generally, then holders of cash will benefit as prices reduce - the pound in your pocket will grow more valuable, quite safely. Even better, this type of deflationary gain is not taxed, at least not until the government nerves itself up to simply confiscate your savings.

But that's not the whole picture. While demand for luxuries is lessening, there are other things that we still have to buy, especially food and energy. Here, prices are rising. And if interest rates do rise, that will also increase RPI, which unlike the Consumer Price Index (CPI) includes housing costs. So it is quite possible that inflation as measured by RPI could be high, even as the economy slows down. It's worth noting that the government has recently changed rules on private sector occupational pensions so that their benefits will increase in line with CPI instead of RPI, which suggests that our rulers believe that one way or another, RPI will rise faster than CPI in years to come.

The BBC appears to have bought the official line that we should ignore food and energy costs, referring to CPI as "core" inflation and noting that it's now a mere 3.1%, as opposed to RPI which is running at 4.8%. However, unlike the mandarins at Broadcasting House, the rest of us need to eat and keep warm; or, to be a little fairer, food and energy is a more significant part of most people's budgets than it is for the upper echelon of the mediaocrities.

An RPI-linked cash product is a good each-way bet: if prices do reduce, then your money becomes more valuable; if prices increase, the value of your savings is preserved; and either way, you benefit from that extra 1% p.a. sweetener.