In 1971, the economist Stafford Beer brought the cybernetic revolution to Chile. His key perception was that economic decisions needed not only accurate, but timely information. So he set up a computer network and data analysis systems to empower the government's ministries without overloading them with irrelevant data.

In advanced economies, it's important for companies, banks and individuals to receive such information, too.

But nearly 40 years later, the USA needs to re-learn the lesson. The Federal Reserve ceased reporting M3 money supply data in 2006; accurate assessment of inflation is complicated by "hedonic adjustment" and periodic (and tendentious?) alteration of the types of item included in price surveys; the Bureau of Labor Statistics seasonally adjusts unemployment figures so that an increase can sometimes appear to be a decrease; nobody (not even the lenders) yet knows the full figures on bad loans and "Tier 3 assets"; it is not even clear how we should assess a nation's wealth (GDP per capita seems a misleading measure).

How can you navigate without up-to-date information? Even in the nineteenth century, Mississippi river pilots had to keep track of the river's changes, or risk getting stranded on new sandbars. And as John Mauldin reports, party political manoeuvering is stymying two appointments to the Federal Reserve's Board, at a time when the Fed most needs to concentrate on resolving the unfolding complex financial crisis.

Even given the right data, decision-making has become tougher. Increasing global interconnection and wealth transfer between nations means that normal cycles may be broken by epochal linear developments, so the past is now a very unsafe guide to the future.

We need clarity, direction and vision.

Sunday, January 20, 2008

Panzner votes DE (flation)

Michael Panzner is in the DE camp, because the bubble was caused by credit creation: "The way up is the way down" (a maxim of both Taoism and Heraclitus, apparently; but then the Greeks have always been great travellers and interested in ideas).

In his excellent book (reviewed here last May), he suggests that inflation will come afterwards (actually, not just IN- but HYPER-).

In his excellent book (reviewed here last May), he suggests that inflation will come afterwards (actually, not just IN- but HYPER-).

Saturday, January 19, 2008

A small town in Germany

The TV was on, and I forget what programme we were watching. Sometimes they were Dutch - we were near the border - but more often German. I was eleven, and would watch anything. Even the adverts were fun, linked by shorts featuring little cartoon characters, the Mainzelmännchen. HB cigarettes, Allianz insurance, Bear condensed milk ("Nichts geht über Bärenmarke……Bärenmarke zum Kaffee!")

Then a newsflash cut in: the President of the USA had been shot on a visit to Dallas and had been rushed to hospital. My father went upstairs. The programme resumed.

My father came down. I still remember him buckling his belt over his uniform, as ever uncomfortable and determined to do his best, a stocky man with a straight back, now full of tension. He watched with us as another newsflash came: the President was dead.

I think the camp sent a driver with a Jeep; in any case, Dad was gone. We watched some more TV, interrupted by occasional updates and speculation. Then it was time for bed. Flannel pyjamas, cotton sheets, the heavy blankets that trapped your feet. I went to sleep.

Lights woke me, illuminating the curtains. Heavy engines, headlights passing, heading in the direction of Düsseldorf. One after another after another. Now, I know they were tank transporters, racing to position the heavy armour in readiness for the Red invasion.

And now there are no more Communists, or so it seems. We buy fuel from the Russians, hardware and toys from the Chinese. The people my father, a gentle and sensitive man, was prepared to die fighting, are our friends and trading partners. As reported by The Independent, Chinese interests even supported our Conservative leader and former Prime Minister, Edward Heath (Sir Edward protested the following week, saying the claims were "misleading and inaccurate" - but did not go so far as to say that they were untrue). Surely, we're all friends now. After all, Dad had helped the Germans start to rebuild their country; he'd worked with German civilians, learned to speak the language fluently, married a German refugee. Wars happen, and so does peace. The people of the world are vexed by their leaders, yet love for one another endures and triumphs.

But Communism is not a nation, and does not love people. Everything, even its own most ardent supporters, can be burned on the altar of abstract principle. Informed that a general nuclear war would kill a third of humankind, Mao said good, then there would be no more classes.

As gypsies and beggars used to sing:

So proud and lofty is some sort of sin

Which many take delight and pleasure in

Whose conversation God doth much dislike

And yet He shakes His sword before He strike

(The Watersons performed it on "Frost and Fire", which our English teacher played to us in the late Sixties. I associate it with cold, freshness, the musty fragrance of the Monmouthshire woods, animism, hope.)

By degrees, this brings me to the current state of affairs. Our leaders wish us to believe that the history of our fathers is at an end, and now only efficient administration remains to be achieved. The revels of democracy are ended; they were fun, but their time is past.

No: as Christopher Fry said, "affairs are soul size", still. Although I do believe that sudden and total conversion is possible, as in James Shirley's now implausible-seeming play "Hyde Park" (who would have believed the Earl of Rochester's conversion? - and there are those who still doubt it, not knowing how the sinner hates sin), I doubt that all who worked with the old Soviet and Chinese Communist regimes have abandoned their principles and plans. Like the remark about the significance of the French Revolution (variously attributed to Chou En-Lai and Mao Tse-Tung), it's "too early to say".

Even if our leaders should be gullible or merely suborned, Jeffrey Nyquist reminds us again that there are still people who think differently from us, and we must be prepared. It is not all right to be weak, whether militarily or in our economies. Good fences (and good borders) make good neighbours.

Then a newsflash cut in: the President of the USA had been shot on a visit to Dallas and had been rushed to hospital. My father went upstairs. The programme resumed.

My father came down. I still remember him buckling his belt over his uniform, as ever uncomfortable and determined to do his best, a stocky man with a straight back, now full of tension. He watched with us as another newsflash came: the President was dead.

I think the camp sent a driver with a Jeep; in any case, Dad was gone. We watched some more TV, interrupted by occasional updates and speculation. Then it was time for bed. Flannel pyjamas, cotton sheets, the heavy blankets that trapped your feet. I went to sleep.

Lights woke me, illuminating the curtains. Heavy engines, headlights passing, heading in the direction of Düsseldorf. One after another after another. Now, I know they were tank transporters, racing to position the heavy armour in readiness for the Red invasion.

And now there are no more Communists, or so it seems. We buy fuel from the Russians, hardware and toys from the Chinese. The people my father, a gentle and sensitive man, was prepared to die fighting, are our friends and trading partners. As reported by The Independent, Chinese interests even supported our Conservative leader and former Prime Minister, Edward Heath (Sir Edward protested the following week, saying the claims were "misleading and inaccurate" - but did not go so far as to say that they were untrue). Surely, we're all friends now. After all, Dad had helped the Germans start to rebuild their country; he'd worked with German civilians, learned to speak the language fluently, married a German refugee. Wars happen, and so does peace. The people of the world are vexed by their leaders, yet love for one another endures and triumphs.

But Communism is not a nation, and does not love people. Everything, even its own most ardent supporters, can be burned on the altar of abstract principle. Informed that a general nuclear war would kill a third of humankind, Mao said good, then there would be no more classes.

And dictators, dressed in a little brief authority, ignore warnings. On the eve of World War II, when the conflict could yet be averted, Hitler was with guests in Berchtesgaden when the clouds over the mountains assumed an ominous red and yellow appearance. A woman told him "Das bedeutet blut, und mehr blut" ("This means blood, and more blood"); Hitler trembled, but then said if it must be so, it must be so.

As gypsies and beggars used to sing:

So proud and lofty is some sort of sin

Which many take delight and pleasure in

Whose conversation God doth much dislike

And yet He shakes His sword before He strike

(The Watersons performed it on "Frost and Fire", which our English teacher played to us in the late Sixties. I associate it with cold, freshness, the musty fragrance of the Monmouthshire woods, animism, hope.)

By degrees, this brings me to the current state of affairs. Our leaders wish us to believe that the history of our fathers is at an end, and now only efficient administration remains to be achieved. The revels of democracy are ended; they were fun, but their time is past.

No: as Christopher Fry said, "affairs are soul size", still. Although I do believe that sudden and total conversion is possible, as in James Shirley's now implausible-seeming play "Hyde Park" (who would have believed the Earl of Rochester's conversion? - and there are those who still doubt it, not knowing how the sinner hates sin), I doubt that all who worked with the old Soviet and Chinese Communist regimes have abandoned their principles and plans. Like the remark about the significance of the French Revolution (variously attributed to Chou En-Lai and Mao Tse-Tung), it's "too early to say".

Even if our leaders should be gullible or merely suborned, Jeffrey Nyquist reminds us again that there are still people who think differently from us, and we must be prepared. It is not all right to be weak, whether militarily or in our economies. Good fences (and good borders) make good neighbours.

Punish the perp

Karl Denninger says we should make the people who caused the subprime problems pay for the consequences. Either they should burn up with their own debt (Marc Faber has said some players should be taken out of the game) or pass on the grief to their shareholders, issuing new shares to raise capital and so diluting the existing stockholders' portion.

Unfortunately, we in the UK have chickened out - for party political reasons to do with its power base in the north of England, the Labour government is currently holding the baby in the case of insolvent lender Northern Rock, even though the tax payer is on the hook for nearly $120 billion as a result. (Hey, that's nearly as much as the proposed new tax break to reflate America - and our population is one-fifth the size of yours!)

Hope you have better luck - or better leaders - over there. Buy a Lottery ticket and hope?

Unfortunately, we in the UK have chickened out - for party political reasons to do with its power base in the north of England, the Labour government is currently holding the baby in the case of insolvent lender Northern Rock, even though the tax payer is on the hook for nearly $120 billion as a result. (Hey, that's nearly as much as the proposed new tax break to reflate America - and our population is one-fifth the size of yours!)

Hope you have better luck - or better leaders - over there. Buy a Lottery ticket and hope?

Friday, January 18, 2008

Dow 9,000 update

Dow 12,082.31, gold $880.50/oz, so the Dow is now worth 13.72 ounces of gold as against Robert McHugh's prediction of 13.51.

Nearly there, and the new announcement of a $145 billion reflation may push gold that extra yard.

Nearly there, and the new announcement of a $145 billion reflation may push gold that extra yard.

Stocks may follow bond yields down

Bob Bronson gives us a striking graph of the apparent correlation (since 2000) between the stockmarket and the yield on 10-year Treasury bonds. There is now a very wide gap between the two and seemingly the implication is that stocks are overdue for a large correction.

Wednesday, January 16, 2008

Here we go

Two from Karl Denninger in the last two days:

Monday, he reasserted his belief in DE-flation; but as I've been saying for some time, maybe the real issue is the divide between haves and have-nots, and he deals with that, too. No point being rich if you daren't go out.

Yesterday, he sounded the bells for a possible crash today. Maybe this is when Robert McHugh's prediction is fulfilled.

Monday, he reasserted his belief in DE-flation; but as I've been saying for some time, maybe the real issue is the divide between haves and have-nots, and he deals with that, too. No point being rich if you daren't go out.

Yesterday, he sounded the bells for a possible crash today. Maybe this is when Robert McHugh's prediction is fulfilled.

Tuesday, January 15, 2008

Time to buy into Northern Rock?

Two hedge funds have punted heavily on the British lender that the government has supported with £55 billion.

The share price has slumped from over £12 last February to 69 pence, assisted by the gleefully gloomy 20/20 hindsight of the news media. We had voxpops today from small "windfall share" demutualisation shareholders ruefully reckoning their notional losses and admitting they can't find the (now-near worthless - ha!) certificates.

One of Sir John Templeton's maxims is "The time of maximum pessimism is the best time to buy and the time of maximum optimism is the best time to sell."

Let me offer two of mine: "Never buy what the fund managers try to sell you at financial adviser seminars", and "Remember the journalists who had their pensions in Equitable Life with-profits, because EL didn't (ugh!) pay commissions".

If I had the spare, I might speculate on NR. Hedge funds may be able to afford losing money, but they certainly don't go out of their way to do it. I wonder what will happen?

The share price has slumped from over £12 last February to 69 pence, assisted by the gleefully gloomy 20/20 hindsight of the news media. We had voxpops today from small "windfall share" demutualisation shareholders ruefully reckoning their notional losses and admitting they can't find the (now-near worthless - ha!) certificates.

One of Sir John Templeton's maxims is "The time of maximum pessimism is the best time to buy and the time of maximum optimism is the best time to sell."

Let me offer two of mine: "Never buy what the fund managers try to sell you at financial adviser seminars", and "Remember the journalists who had their pensions in Equitable Life with-profits, because EL didn't (ugh!) pay commissions".

If I had the spare, I might speculate on NR. Hedge funds may be able to afford losing money, but they certainly don't go out of their way to do it. I wonder what will happen?

Monday, January 14, 2008

Oil to crack the dollar?

Nathan Lewis reminds us how, when President Nixon cut the dollar's link to gold in 1971, OPEC protected the real value of its oil with price rises (thus earning a reputation for having caused our inflation).

Now that the gold dinar has been introduced in Malaysia, Lewis wonders whether the dirham should link to gold, too, so oil exporters can avoid being robbed by a falling dollar.

Brownouts and lines at the gas station again, perhaps.

Now that the gold dinar has been introduced in Malaysia, Lewis wonders whether the dirham should link to gold, too, so oil exporters can avoid being robbed by a falling dollar.

Brownouts and lines at the gas station again, perhaps.

USA / UK Sovereign Wealth Funds?

Shares are supposed to be the best long-term investment, better than bonds or cash. The usual concern is the time horizon of the investor. Who lives longer than a state like America or Britain?

Foreign governments with trade surpluses (based on artificially low currency exchange rates and stupid overspending by the West) are building up trillions in reserves and eyeing our companies and real estate. If our own leaders aren't willing to rebalance the world economy, the least they can do is get a piece of the action.

Why not?

Foreign governments with trade surpluses (based on artificially low currency exchange rates and stupid overspending by the West) are building up trillions in reserves and eyeing our companies and real estate. If our own leaders aren't willing to rebalance the world economy, the least they can do is get a piece of the action.

Why not?

Sunday, January 13, 2008

Dow 9,000 update

Last year, Robert McHugh predicted that the Dow would drop to 9,000, if not in nominal terms then in relation to gold. The Dow was then 13,238.73 and gold $666.30/oz, which means that it took 19.87 ounces of gold to buy the Dow. McHugh's prediction implies the Dow dropping to 13.51 gold ounces (a fall of 6.36 ounces).

The Dow is now 12,606.30 and gold $894.90, so the Dow is now worth 14.09 gold ounces. It has fallen by 5.78 ounces out of the predicted 6.36, so the prediction is 90.9% fulfilled so far.

McHugh will be fully correct if, for example, the Dow remains unchanged and gold rises to $933/oz; or if gold stalls, the Dow will need to fall to 12,090.

The Dow is now 12,606.30 and gold $894.90, so the Dow is now worth 14.09 gold ounces. It has fallen by 5.78 ounces out of the predicted 6.36, so the prediction is 90.9% fulfilled so far.

McHugh will be fully correct if, for example, the Dow remains unchanged and gold rises to $933/oz; or if gold stalls, the Dow will need to fall to 12,090.

To Gordon Brown: please remit £4bn ASAP

From Bob Hoye in Safe Haven yesterday:

"U.K. Sold 395 tonnes of gold at an average price of $274.9 per ounce. The first sale at $254 caught (or caused?) the low point in a 20-year slide in the price of gold.

The losers are us, Brown's gold sales raised around $3.49 billion.."

-- Telegraph.co.uk , January 2, 2006

That was written when the price was $627 and at today’s gold price of $895 the position would be worth $11.4 billion. And - remember the reason for selling was to improve central bank returns - what did they buy with the funds?

I make that a loss of $8 billion to date, or £4bn sterling.

We hear a lot about accountability. If only politicians could be made personally financially accountable.

Or if they could be paid to go away. In recent times, it would have saved the country a fortune if each senior politician had been given £10 million to do nothing at all.

"U.K. Sold 395 tonnes of gold at an average price of $274.9 per ounce. The first sale at $254 caught (or caused?) the low point in a 20-year slide in the price of gold.

The losers are us, Brown's gold sales raised around $3.49 billion.."

-- Telegraph.co.uk , January 2, 2006

That was written when the price was $627 and at today’s gold price of $895 the position would be worth $11.4 billion. And - remember the reason for selling was to improve central bank returns - what did they buy with the funds?

I make that a loss of $8 billion to date, or £4bn sterling.

We hear a lot about accountability. If only politicians could be made personally financially accountable.

Or if they could be paid to go away. In recent times, it would have saved the country a fortune if each senior politician had been given £10 million to do nothing at all.

Saturday, January 12, 2008

Debt and slavery

Doug Noland sees the debt crisis spreading to the corporate sector; David Jensen writes a letter to the Governor of the Bank of Canada, including very telling graphs of mounting debt and the bubble in the financial markets; Michael Panzner discusses a piece from the Financial Times on the threat of a downgrade of America's historic AAA credit rating, and refers to the weakening of the USA's military pre-eminence; Sol Palha worries about the acquisition of Western assets by sovereign wealth funds ("Slowly but surely America and Europe are going to be owned by foreigners. The irony is that Congress is trying to keep immigrants out of this country but right in front of their eyes foreigners are slowly gobbling up huge chunks of this country.").

All this leads me to Jeffrey Nyquist's grim, but compelling latest piece. He despairs of the irrelevance of mainstream political discussion, especially as the polling process rattles on, and paints a far greater picture. I think you should read it all, but here are a few extracts:

What is happening in the news today, what is happening in the markets and in the banking system, has profound strategic implications... There are no invulnerable countries... If a government does not see ahead, make defensive preparations, establish a dialogue with citizens, lead the way to awareness and responsibility, then the nation stumbles into the next world war unarmed and psychologically unprepared.

Even worse, today's politics has become a politics of "divide and conquer" in which one constituency is played off against another: poor against rich, non-white against white, the secular against the religious. Before a positive outcome is possible, we must have unity and we must have reality.

It's more comfortable to ignore the crying of Cassandra, but maybe Nyquist is like Churchill in the pre-WWII political wilderness, trying to prepare us for the next conflict. We in Britain only just made it, and how we have paid for that struggle ever since.

But it was a price worth paying. History would have been very different, and very horrible I am sure, if Churchill had listened to some in his Cabinet in 1940 who advised him to make a deal with the Nazis. He said, “If this long island story of ours is to end at last, let it end only when each one of us lies choking in his own blood upon the ground.” It's a line that even now has tears pricking my eyes. The appeasers were silenced by the sound of deeply-moved men banging their fists on the Cabinet table in agreement and applause.

My worry is that I don't see men of that calibre now. As Lord Acton said in a letter to a bishop, "Power corrupts, and absolute power corrupts absolutely". Commenting on the House of Commons after the Great War, Stanley Baldwin remarked on the presence of "A lot of hard-faced men who look as if they had done very well out of the war". Today, the faces are softer, the hair expensively dressed, the manner relaxed and affable, but behind it all one senses cold-hearted, selfish betrayal. To be charitable, it may be that our leaders and ex-leaders don't fully realize the negative consequences of all their deals, compromises and consultancies.

As our reckless debt is progessively converted into ownership, we may find out how much we took our freedom for granted. It's a lot harder to get back.

The Bible has something to say on this, too (and no, I'm not a preacher, this is to show that the issues endure throughout history): Leviticus, Chapter 25 deals with debt, buying and redeeming slaves, and how the chosen people should be treated differently from the heathens - for the latter, enslavement is perpetual.

Friday, January 11, 2008

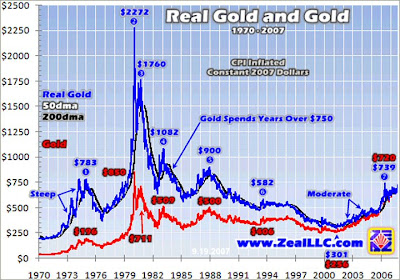

Gold, the dollar and the Dow

Gold supporters seem to be waiting for a reprise of the heady days of 1980. I think this is another case where you need to decide whether you are a speculator or a long-term investor.

Here's a relatively recent graph of the price of gold, adjusted for inflation (admittedly, inflation can be defined in many ways):

Here's a relatively recent graph of the price of gold, adjusted for inflation (admittedly, inflation can be defined in many ways):

On this chart, it looks as though gold's median price would be around $600/oz, so currently it's above trend and presumably the elevated value factors-in some economic concern.

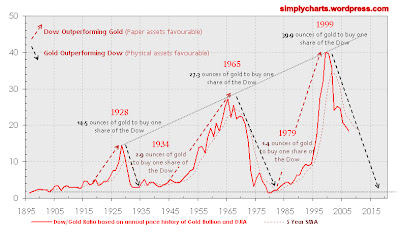

Now, here's a chart correlating the Dow and gold: It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.

It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.

So a purchase of gold now looks like a speculation, rather than a bargain.

Waves and tides

A most apposite article by the Contrarian Investor, in which he considers how all this economic information leaves us confused as to the future direction of the economy. It's like getting millimetre-accurate radar images of all the waves in the harbour, without knowing about the effect of the moon on the tides. Not that the information itself is accurate, anyway.

Thursday, January 10, 2008

Stuffed

Michael Panzner hands on a piece from Naked Capitalism: expert, inside opinion is that the banks are so gorged with bad debt that America will mimic the "melancholy, long withdrawing roar" of Japan's ebb tide.

Wednesday, January 09, 2008

Something's gotta give

Interest on official debt in the USA runs at $430 billion for 2007, and rising steeply, according to the Treasury's own figures (htp Michael Panzner, quoting Mish's Global Economic Trend Analysis); total government debt is now c. $9.2 trillion.

It's more serious than that, of course: James Turk quotes the Comptroller General, David M Walker's estimate that total liabilities, including commitments to future social security benefits, are around $53 trillion. The government's annual revenues are only around 5% of this figure, so the credit card looks like it's pretty much fully-loaded.

However it happens, it seems something must give way under the strain. Frank Barbera reckons the Dow has plenty further to fall (and possible interim correction or not, he thinks gold looks good). Prieur du Plessis concurs, quoting Nouriel Roubini's comment that "... a lousy stock market in 2007 will look good compared to an awful stock market in 2008."

Bob Bronson thinks the downturn will be long as well as hard. He in turn quotes the chairman of the National Bureau of Economic Research: this one “could be deeper and longer than the recessions of the past.”

Boris Sobolev also looks to gold, but prefers the smaller companies because of all the money that's piled into the majors.

In case we in the UK should be tempted by schadenfreude, Ashraf Laidi predicts that sterling will accompany the US dollar's fall against other currencies. From what I read in connection with the USA, a weakening currency may provide a temporary boost to exports, but also inflate the cost of imports; so I don't suppose that our following the dollar will do us much long-term good, either.

Of course, it's possible to dismiss all this as group-think wall-of-worry stuff, but maybe that would be double-bluffing ourselves. Sometimes, things are exactly what they seem. Banks have consistently turned a profit for centuries, on the inexorability of debt.

It's more serious than that, of course: James Turk quotes the Comptroller General, David M Walker's estimate that total liabilities, including commitments to future social security benefits, are around $53 trillion. The government's annual revenues are only around 5% of this figure, so the credit card looks like it's pretty much fully-loaded.

However it happens, it seems something must give way under the strain. Frank Barbera reckons the Dow has plenty further to fall (and possible interim correction or not, he thinks gold looks good). Prieur du Plessis concurs, quoting Nouriel Roubini's comment that "... a lousy stock market in 2007 will look good compared to an awful stock market in 2008."

Bob Bronson thinks the downturn will be long as well as hard. He in turn quotes the chairman of the National Bureau of Economic Research: this one “could be deeper and longer than the recessions of the past.”

Boris Sobolev also looks to gold, but prefers the smaller companies because of all the money that's piled into the majors.

In case we in the UK should be tempted by schadenfreude, Ashraf Laidi predicts that sterling will accompany the US dollar's fall against other currencies. From what I read in connection with the USA, a weakening currency may provide a temporary boost to exports, but also inflate the cost of imports; so I don't suppose that our following the dollar will do us much long-term good, either.

Of course, it's possible to dismiss all this as group-think wall-of-worry stuff, but maybe that would be double-bluffing ourselves. Sometimes, things are exactly what they seem. Banks have consistently turned a profit for centuries, on the inexorability of debt.

Oil splat

"Oil crunch" doesn't sound right, although it might be appropriate to shale oil: Jeffrey Brown outlines what looks like a compelling thesis on growing domestic energy consumption by major oil exporters. He thinks that the top five producers will be using all their own supplies by around 2030, and concludes that the USA must rapidly reshape its transportation system:

In simplest terms, we are concerned that the very lifeblood of the world industrial economy—net oil export capacity—is draining away in front of our very eyes, and we believe that it is imperative that major oil importing countries like the United States launch an emergency Electrification of Transportation program--electric light rail and streetcars--combined with a crash wind power program.

That is just the tip of the iceberg, surely: residential and office heating/lighting, mechanised farming, supermarket shopping, centralised medical facilities - so much will have to be reviewed and planned.

In simplest terms, we are concerned that the very lifeblood of the world industrial economy—net oil export capacity—is draining away in front of our very eyes, and we believe that it is imperative that major oil importing countries like the United States launch an emergency Electrification of Transportation program--electric light rail and streetcars--combined with a crash wind power program.

That is just the tip of the iceberg, surely: residential and office heating/lighting, mechanised farming, supermarket shopping, centralised medical facilities - so much will have to be reviewed and planned.

Tuesday, January 08, 2008

Twang money, encore

The Contrarian Investor is also struck by the elasticity of fiat money, and how this vitiates attempts to make fair comparisons and store wealth. Gold for the long term, he thinks.

In the short term, we have this contest between credit contraction and currency expansion. I'm getting the feeling it'll be the first followed by the second, which is what Michael Panzner predicts in "Financial Armageddon".

In the short term, we have this contest between credit contraction and currency expansion. I'm getting the feeling it'll be the first followed by the second, which is what Michael Panzner predicts in "Financial Armageddon".

Grab your pension now, inflation-proof it?

Tony Allison looks at the threats to your prosperity in retirement. A bird in the hand?

Subscribe to:

Posts (Atom)