This information is a year out of date - more, in the case of credit unions. I wonder where we are now? Ambrose Evans-Pritchard reports that US housing has dropped 29% from peak. Is the system, as some say, basically bust?

This information is a year out of date - more, in the case of credit unions. I wonder where we are now? Ambrose Evans-Pritchard reports that US housing has dropped 29% from peak. Is the system, as some say, basically bust?

Sunday, April 19, 2009

How much is left in the banking system?

Mark Wadsworth refers us to this US banking information, from which I extract and interpret the following:

This information is a year out of date - more, in the case of credit unions. I wonder where we are now? Ambrose Evans-Pritchard reports that US housing has dropped 29% from peak. Is the system, as some say, basically bust?

This information is a year out of date - more, in the case of credit unions. I wonder where we are now? Ambrose Evans-Pritchard reports that US housing has dropped 29% from peak. Is the system, as some say, basically bust?

Kill the old

Not my idea; but I saw it as a graffito on the back of a bus seat on the upper deck, where the schoolchildren gravitate - more than 20 years ago.

Now the FT comments on how longevity (plus the old's passion for killing the unborn and preventing conception) is going to ruin us. We think the young are selfish, and don't dare glance at their elders, who imagine they can quit their jobs in the prime of life and live like kings on the backs of their progeny and remoter descendants - or such few of them as the old permit to survive.

As Mark Steyn puts it:

“Over the next decade,” Frau Merkel pointed out, “we will undergo a massive demographic change, and, therefore, borrowing is a greater burden for the future than in a country with a much more continuously growing population, as in the United States of America.”

Translation: America can rack up multi-trillion-dollar deficits and stick it to its kids and grandkids. But in Europe there are no kids and grandkids to stick it to—just upside- down family trees: in Germany, Spain and Italy, four grandparents have two children have one grandchild. The Financial Times noted last week that the demographic death spiral is a far greater threat to fiscal solvency than the present economic downturn. And yet, despite Germany, Japan and Russia already being in net population decline, the G20 had not a word to say about it.

That bill's going to come in, and Herod himself can't prevent it. In fact, he caused it.

Now the FT comments on how longevity (plus the old's passion for killing the unborn and preventing conception) is going to ruin us. We think the young are selfish, and don't dare glance at their elders, who imagine they can quit their jobs in the prime of life and live like kings on the backs of their progeny and remoter descendants - or such few of them as the old permit to survive.

As Mark Steyn puts it:

“Over the next decade,” Frau Merkel pointed out, “we will undergo a massive demographic change, and, therefore, borrowing is a greater burden for the future than in a country with a much more continuously growing population, as in the United States of America.”

Translation: America can rack up multi-trillion-dollar deficits and stick it to its kids and grandkids. But in Europe there are no kids and grandkids to stick it to—just upside- down family trees: in Germany, Spain and Italy, four grandparents have two children have one grandchild. The Financial Times noted last week that the demographic death spiral is a far greater threat to fiscal solvency than the present economic downturn. And yet, despite Germany, Japan and Russia already being in net population decline, the G20 had not a word to say about it.

That bill's going to come in, and Herod himself can't prevent it. In fact, he caused it.

The market is going to tank

How do I know? I don't.

But I read this piece in the Grumbler.

Picture it. You are a rich broker - floated your company in May 2007 (how's that for timing?). Predicting good times ahead, you... sell £47m of your shares.

You say it's for "private projects", and throw the Mail journalist a tidbit about your beloved foopball club. The Mail journalist writing down your copy at least thinks to ask you how much of this cash will go towards the new stadium. You "decline to say".

Meanwhile, Charles Hugh Smith describes (April 18) the thinking that has led him to punt on a financial bear fund.

Straws in the wind, I'm thinking.

But I read this piece in the Grumbler.

Picture it. You are a rich broker - floated your company in May 2007 (how's that for timing?). Predicting good times ahead, you... sell £47m of your shares.

You say it's for "private projects", and throw the Mail journalist a tidbit about your beloved foopball club. The Mail journalist writing down your copy at least thinks to ask you how much of this cash will go towards the new stadium. You "decline to say".

Meanwhile, Charles Hugh Smith describes (April 18) the thinking that has led him to punt on a financial bear fund.

Straws in the wind, I'm thinking.

Wednesday, April 15, 2009

Will we ever learn?

With Sackerson away, Paddington will post some (possibly) off-topic comments.

The technology that enables 7 billion of us to survive, and provides creature comforts to those in the industrialized world, is due to a tiny percentage of talented and creative scientists, together with a core of engineers who adapted and refined the results, and a larger number who actually produce the products that we use.

Despite that, I am hard-pressed to find a society anywhere that gives those people the level of respect or adulation awarded to sports figures and entertainment personalities. The monetary rewards are far less than for the average investment or insurance agent, lawyer, accountant, or medical doctor.

In the extremist Muslim world, much of science is decried as 'anti-Islam'. Evolution, physics, and geology are under attack in at least 37 US states by creationists. Much of science is also discounted by the New Age thinkers, who don't like facts to get in the way of their own comfortable beliefs.

Yet our leaders believe that the answer to our economic meltdown is to throw money at the people who caused the crisis, and who produce nothing at all. Even at universities, where some rational thinking should be expected, the sciences are de-emphasized, since they are 'hard' and unpopular, while we build programs in psychology and business management.

Without a cultural change in these attitudes, I am fearful that we may see the end of technological civilization within a few generations.

The technology that enables 7 billion of us to survive, and provides creature comforts to those in the industrialized world, is due to a tiny percentage of talented and creative scientists, together with a core of engineers who adapted and refined the results, and a larger number who actually produce the products that we use.

Despite that, I am hard-pressed to find a society anywhere that gives those people the level of respect or adulation awarded to sports figures and entertainment personalities. The monetary rewards are far less than for the average investment or insurance agent, lawyer, accountant, or medical doctor.

In the extremist Muslim world, much of science is decried as 'anti-Islam'. Evolution, physics, and geology are under attack in at least 37 US states by creationists. Much of science is also discounted by the New Age thinkers, who don't like facts to get in the way of their own comfortable beliefs.

Yet our leaders believe that the answer to our economic meltdown is to throw money at the people who caused the crisis, and who produce nothing at all. Even at universities, where some rational thinking should be expected, the sciences are de-emphasized, since they are 'hard' and unpopular, while we build programs in psychology and business management.

Without a cultural change in these attitudes, I am fearful that we may see the end of technological civilization within a few generations.

Monday, April 13, 2009

Protecting against inflation

Before we start, please read my disclaimer above!

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5: True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).

Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.

Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

How do we protect our little wealth against inflation? The gold bugs still enthuse, and it's true that if you'd sold the Dow and bought gold at the start of 2000, and bought back into the Dow now, you'd have multiplied your investment by 5:

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

But looking at the historical relationship between the Dow and gold, it seems the Dow is already below par.

When Nixon closed the "gold window" (15 August 1971), gold ceased to be a currency backing and became just another thing you could choose to invest in, so let's compare these assets from a little before that turning-point, onwards:

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

The gold-priced Dow is now well below average. So what are we to make of (I think) Marc Faber's recently-expressed view that an ounce of gold will buy the Dow?

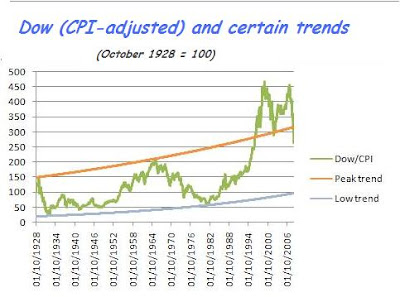

That depends on whether you read this as a statement about gold, or about the Dow. I looked at the Dow in inflation (CPI) terms a while back (December 2008):

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

If we are in a downwave, then the Dow's bottom is still a lot lower than where it stands now. Extrapolation is always risky, but my curve indicates maybe 4,000 points as its destination. Having said that, the highs of the years 2000 and 2007 are so much higher than might have been extrapolated, that maybe the low will be correspondingly lower. A real pessimist might argue that, adjusted for inflation, the Dow might test 1,000 or 2,000 points sometime in the next few years.

Back to gold-pricing: it's also notable that the Dow is currently still worth some 8 ounces of gold, but in previous lows (Feb. 1933, March 1980) fell below 2 ounces: So should we still pile into gold, as a hedge against the further collapse of the Dow?

So should we still pile into gold, as a hedge against the further collapse of the Dow?

I think not. Firstly, the Dow may well have a rally, since it's fallen so sharply in such a short time. And secondly, this is missing the point, which is that we are looking to protect wealth against inflation, not against the Dow.

So another question is, how does gold hold its value during periods of price inflation? A period some readers may have lived through, is that after the oil price hike of October 1973. Here is what happened in the 5 years from 1974 to 1978:

True, the Dow merely held its value over that time (though it also made some sharp gains and losses) - but gold disappointed. I think this may be because, when prices are roaring up, people start looking for a yield, which of course the inert metal cannot provide.But let's wind the clock back just a little - let's go back to that closing of the gold window again, and see what happened between August 1971 and the end of 1978:

The massive rise in the price of gold anticipated the inflation of post-1974, and those who got in at the right moment were very well protected. It's also interesting to see what happened to the Dow in the '71 - '74 period - a fall, from which the Dow did not recover (in inflation terms).Before we start blaming the "G-dd-mn A-rabs" for inflation, let's remember the inadequately-reported fact that monetary inflation was roaring for several years beforehand. The OPEC price rise was a reaction intended to protect the Saudis' (and others') main asset - and you'd have done the same. Yes, it happened suddenly, but like an earthquake, it merely released long-pent-up stresses. Instead, let's blame a goverment that failed to control its finances generally, and spent far too much on war - a retro theme back in vogue today, it seems.

Looking at it from an investor's point of view, once the preceding monetary trend was identifiable, going overweight in gold in the early 70s would have been a sensible precaution.

So I suggest that gold's value as an inflation hedge is for those who anticipate well in advance. And this may be the lesson to draw in relation to the present time:

The inflation protection has already been built-in, for those who bought gold at the right time. The rest of us should note that gold is now above the long-term post-1971 trend:There may indeed be a spike, as in 1980 - but that's for speculators. For the average person, who wants a "fire-and-forget" longer-term investment, I can't say gold looks like a bargain now.Nor would I be that keen to get into the stockmarket, unless you're a day-trader. Some may make a killing in the present turbulence, but many will get killed. I'm still looking for that Dow-4,000 moment, and as I explained above, even then it's possible I may lose 50% - 75% in the short-to-medium term.

What else?

Houses? Still too pricey, in relation to average income. Yes, some houses are now selling - it's a thriving auction business at the moment, I understand. But again, housing is above trend.

Bonds? No, indeed. Municipal bonds in the US are offering high yields, for a very good reason; and even national bonds are a worry. The debt has not been squeezed out of the system, since our cowardly politicians have absorbed it into the public finances instead.

Here in the UK, we have National Savings & Investments Index-Linked Savings Certificates (3- and 5-year terms). Between them, a couple could get £60,000 into that haven, and not many of us have that much. I'm not sure about the rules and limits for US equivalent (TIPS), but the general argument applies. Yes, there is the question of how the government will choose to define inflation, but I don't suppose the definition will get too Mickey-Mouse.

Besides, doubtless you'll keep some cash for emergencies (including sudden bank closures), and for bargains (e.g. looking for distressed sales).

And if you've got lots more cash than the rest of us, congratulations, since the rich will get substantially richer. There's no being wealthy like being wealthy in a poor country, or one that's getting poorer. Watch that Gini Index rise.

Sunday, April 12, 2009

Conspiracy Theory

How about this as a scenario? Alistair Campbell arranges for the McBride/Draper emails to be leaked to Guido, in order not only to mortally wound both M & D (and neutralise Charlie Whelan for some time to come), but mainly to destabilise Gordon Brown ("how could he not know", "it came from Number 10's system", etc) so that a fresh leader can be installed in preparation for the 2010 General Election. "A cleansing of the Augean stables - New Labour has put its house in order - renewed commitment to our core programs - it was always about policies, not personalities - our narrative was temporarily hijacked by psychologically flawed mavericks" and so on.

Has Guido been used?

Has Guido been used?

Subscribe to:

Posts (Atom)