Sunday, January 04, 2009

Disaster deferred (and increased), not averted

Karl Denninger goes back to basics, explaining how the reflation is merely paying you-now from you-future's account. Knit faster, we're running out of wool.

Saturday, January 03, 2009

Murky business

Brad Setser does a very interesting bit of detective work and concludes that much of the UK's holdings of US Treasury securities, are on behalf of China. He gives us a graph demonstrating that when the UK's official holding declines sharply (usually in June), China's suddenly rises.

Setser estimates that China owns $1.425 trillion in Treasuries and Agencies, which is equivalent to about 10% of US GDP. ("Treasuries" are debts directly owed by the US Government, "agencies" are debts of the US Government's organisations, as explained in this Federal Reserve handbook from 2004.)

He ends by calling for more transparency in British accounts of these holding - that would be most welcome all round, generally. Half our problems (and, I assume, opportunities for fatcat swindlers) stem from our not knowing the real position of the world's finances.

Setser estimates that China owns $1.425 trillion in Treasuries and Agencies, which is equivalent to about 10% of US GDP. ("Treasuries" are debts directly owed by the US Government, "agencies" are debts of the US Government's organisations, as explained in this Federal Reserve handbook from 2004.)

He ends by calling for more transparency in British accounts of these holding - that would be most welcome all round, generally. Half our problems (and, I assume, opportunities for fatcat swindlers) stem from our not knowing the real position of the world's finances.

Pop

Perhaps the fall will be faster.

In this piece, Charles Biderman explains that the value of a stock is set by marginal purchases, which do not reflect what you'd get if you sold all the company's shares at the same time. He estimates that from 2003-2007 the world's equities increased in notional value by $25 trillion, on nothing more than $1.5 trillion cash, a bit of borrowing and mostly, illusion: "Market cap and money aren't necessarily related."

When the illusion goes pop, so do all the gains. First out gets the most.

htp: zgirl

In this piece, Charles Biderman explains that the value of a stock is set by marginal purchases, which do not reflect what you'd get if you sold all the company's shares at the same time. He estimates that from 2003-2007 the world's equities increased in notional value by $25 trillion, on nothing more than $1.5 trillion cash, a bit of borrowing and mostly, illusion: "Market cap and money aren't necessarily related."

When the illusion goes pop, so do all the gains. First out gets the most.

htp: zgirl

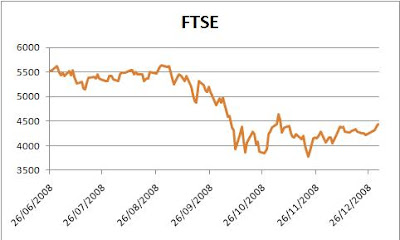

Elliot, Kondratieff, or normal service resumed?

On 26th June I looked at the progress of the FTSE since around 1984 and thought that the next low would be no worse than c. 4,500. Here's what actually happened:

The lows were certainly lower, and we have only recently learned just how close we came to a banking collapse. The question now is, are we where we "should" be - following a trend set by the last 25 years - or are there longer cycles due to make hay of the pattern of the last quarter-century? Elliot wavers and Kondratieff followers say yes.

My guess is that, after the steep stockmarket falls and the horrid crisis apparently averted, there will be a bounce in the next 1-2 years, then a decline in real (inflation-adjusted) terms for maybe another 5 years after that. Your guess?

By the way, I'd also be interested to know your views on why the bankers and brokers have been allowed to Get Away With It. To me, it seems like a big fat moral hazard and unless there is some real squealy punishment for all this bad behaviour, I'd advise any bright, conscienceless youngster to become a banker.

Currently, my preferred fantasy solution is to bust all the overextended banks, leave the shareholders with zilch, sack the senior bank managers and ban them from being company directors for at least 5 years, halve all mortgages, and give the book of business to more prudent operators including well-run building societies. In my view, this was never ever going to happen, because the FSA, the BoE and the government are also implicated. So, not so much "too big to fail", but too well-connected to fail.

But there's a price to pay, anyway: it's now clearly Us and Them. Perhaps, since they are immeasurably more powerful, we should give up trying to rectify the world and merely ape their cynicism and corruption. Moralists will demur; and so this is truly an age when we can say, "Affairs are now soul size".

The lows were certainly lower, and we have only recently learned just how close we came to a banking collapse. The question now is, are we where we "should" be - following a trend set by the last 25 years - or are there longer cycles due to make hay of the pattern of the last quarter-century? Elliot wavers and Kondratieff followers say yes.

My guess is that, after the steep stockmarket falls and the horrid crisis apparently averted, there will be a bounce in the next 1-2 years, then a decline in real (inflation-adjusted) terms for maybe another 5 years after that. Your guess?

By the way, I'd also be interested to know your views on why the bankers and brokers have been allowed to Get Away With It. To me, it seems like a big fat moral hazard and unless there is some real squealy punishment for all this bad behaviour, I'd advise any bright, conscienceless youngster to become a banker.

Currently, my preferred fantasy solution is to bust all the overextended banks, leave the shareholders with zilch, sack the senior bank managers and ban them from being company directors for at least 5 years, halve all mortgages, and give the book of business to more prudent operators including well-run building societies. In my view, this was never ever going to happen, because the FSA, the BoE and the government are also implicated. So, not so much "too big to fail", but too well-connected to fail.

But there's a price to pay, anyway: it's now clearly Us and Them. Perhaps, since they are immeasurably more powerful, we should give up trying to rectify the world and merely ape their cynicism and corruption. Moralists will demur; and so this is truly an age when we can say, "Affairs are now soul size".

Thursday, January 01, 2009

Am I the idiot, or are they?

For years, at least since the Reagan era, we in the US have heard the Republican Party mantra that the answer to growing the economy is to cut taxes for the richest, since they will 'invest in business'.

It never made sense to me, especially as I saw such a transfer of wealth to those same rich people, who spent their money on luxury imported goods. Incomes for the middle and lower class barely kept pace with inflation, even as industry became ever more efficient.

Today, thanks to posts here and elsewhere, I finally realized what is wrong with the claim above: buying stocks does not 'invest in a company', unless you are buying stock directly from that same company. All it does is put money in the pockets of the stockbrokers, while you have a piece of paper that must rise in value by profit plus fees, and find another sucker to buy it. The real estate market is no different.

Nonetheless, all of the experts that I have talked with over the years insisted that I simply didn't understand, implying that I was an idiot. Am I?

It never made sense to me, especially as I saw such a transfer of wealth to those same rich people, who spent their money on luxury imported goods. Incomes for the middle and lower class barely kept pace with inflation, even as industry became ever more efficient.

Today, thanks to posts here and elsewhere, I finally realized what is wrong with the claim above: buying stocks does not 'invest in a company', unless you are buying stock directly from that same company. All it does is put money in the pockets of the stockbrokers, while you have a piece of paper that must rise in value by profit plus fees, and find another sucker to buy it. The real estate market is no different.

Nonetheless, all of the experts that I have talked with over the years insisted that I simply didn't understand, implying that I was an idiot. Am I?

Tuesday, December 30, 2008

Fun with extrapolation

Since the 1990s, the stockmarket has been showing such freakish returns that many thought we were in a "new paradigm", whatever that means.

So I've looked at the Dow adjusted for CPI since late 1928, and calculated max/min lines on the basis of the highs in 1929 and 1966, and the lows in 1932 and 1982, to see just how unrepresentative the last decade has been. If we saw a return to these imaginary trends, the next Dow low could be less than half the present value. If, if, if...

Coincidentally, Jim Kunstler is predicting much the same:

By May of 2009, the stock markets will resume crashing with the ultimate destination of a Dow 4000 before the end of the year.

But I think it may take longer than that. The Elliott-wavers are looking for a final upwave first. Having said that, the last 10 years have been out of all comparison with the 70 years before.

Monday, December 29, 2008

Debt forgiveness, inflation and welching

Thus Jesse, discussing Michael Hodges' visionary "Grandfather Economic Report" and US indebtedness:

In a simple handwave estimate, one might say that the debt will have to be discounted by at least half. That includes inflation and selective defaults...

... something has got to give. The givers will most likely be all holders of US financial assets, responsible middle class savers, and a disproportionate share of foreign holders of US debt.

While the debtors hold the means of payment in dollars and the power to decide who gets paid, where do you think the most likely impact will be felt?

I give below the US Treasury's data on foreign holdings of their government securities as at October 2008, but I also reinterpret it in the light of each country's GDP, to show relative potential impact (please click on image to enlarge).

Mind you, even a complete repudiation would only take care of $3 trillion. Funny how not so long ago, $1 trillion seemed a high-end estimate of the damage, and now it's something like seven times that. And that still leaves a long haul to get to Hodges' $53 tn - equivalent to, what, one year's global GDP?

In a simple handwave estimate, one might say that the debt will have to be discounted by at least half. That includes inflation and selective defaults...

... something has got to give. The givers will most likely be all holders of US financial assets, responsible middle class savers, and a disproportionate share of foreign holders of US debt.

While the debtors hold the means of payment in dollars and the power to decide who gets paid, where do you think the most likely impact will be felt?

I give below the US Treasury's data on foreign holdings of their government securities as at October 2008, but I also reinterpret it in the light of each country's GDP, to show relative potential impact (please click on image to enlarge).

Mind you, even a complete repudiation would only take care of $3 trillion. Funny how not so long ago, $1 trillion seemed a high-end estimate of the damage, and now it's something like seven times that. And that still leaves a long haul to get to Hodges' $53 tn - equivalent to, what, one year's global GDP?

Sunday, December 28, 2008

Saturday, December 27, 2008

Is gold a hedge against inflation?

There are problems with using gold as an insurance against inflation.

(N.B. gold prices to the end of 1967 are annual averages, then monthly averages to the end of 1974, then the price is as on the first trading day of the month; all gold price figures from Kitco).

1. Governments interfere with it - from making it the legal base of their currency, as in the US Constitution, to making it illegal to have any, as in the US in 1933; from guaranteeing the exchange rate of gold against the dollar (post WWII) to the Nixon Shock of 1971, when the gold window was closed.

2. Central banks claim to hold it, then (it is widely suspected) lend or sell it surreptitiously.

3. There is so little of it, that speculators can have a significant effect on the price, especially if (as appears to have happened in recent years), the speculation has been powered by vast amounts of borrowed money.

Below, I give three graphs, all comparing the price of gold per ounce in US dollars with inflation as measured by the Consumer Price Index (and that's another can of worms). It's clear that gold has a very volatile relationship with inflation and can spend a very long time above or below trend.

In the fourth graph I divide the Dow by the price of gold. It seems obvious that gold is a contrarian position for equity investors, rather than a simple hedge against inflation.

Currently, the Dow has come back to something like a normal ratio to gold, but past history suggests there will be an overshoot. And gold itself seems above trend over all three periods chosen; which suggests that both still have a way to fall in nominal terms, but the Dow more so.

(N.B. gold prices to the end of 1967 are annual averages, then monthly averages to the end of 1974, then the price is as on the first trading day of the month; all gold price figures from Kitco).

Friday, December 26, 2008

Nominal and real

Marc Faber's latest interviews on Bloomberg and CNBC show him estimating the recession to last "2, 5, 10 years". He also says that Asia is better placed to recover, because after the panic of 1998 they deleveraged, i.e. reduced borrowings.

So it's time for me to review my guesses about when the recovery will come for us. A key consideration is inflation, which Faber says is being stoked up for the long term by all the "stimulus" currently put in by panicky Western governments.

I've suggested that we might compare the present, not to the 1929-32 collapse, but the period 1966-1982, when inflation sometimes growled and sometimes roared. The result was that the nominal and inflation-adjusted low points are very far apart: the start-of-month level for the Dow hit bottom in September 1974, but adjusted for CPI, the real bottom was in July 1982.

So when the upturn comes, depends on your definition. I am still guessing that there will be a nominal recovery in 2010, but inflation will erode gains over time and the real turning point may not come until, say, 2016.

Wednesday, December 24, 2008

"Efficiency" vs. survival

"...we have to build back into the system Resiliency. This means that each region has to work to become largely energy, food and financially self sustaining and that each region needs to network into the others. In effect we shift from an efficient machine to a resilient network."

Robert Paterson, as quoted by London Banker.

Like I keep saying, it's about diversity, dispersion and disconnection - please click on the label below for my posts on this subject.

Robert Paterson, as quoted by London Banker.

Like I keep saying, it's about diversity, dispersion and disconnection - please click on the label below for my posts on this subject.

It's not about dinosaurs

Would you rather explain away the following, or share in it?

1. The death of William Blake, 12 August 1827:

“Just before he died His Countenance became fair. His eyes Brighten'd and he burst out Singing of the things he saw in Heaven”

2. The experience of St Thomas Aquinas, 6 December 1273:

LXXIX: The witness went on to recall that while brother Thomas was saying his Mass one morning, in the chapel of St. Nicholas at Naples, something happened which profoundly affected and altered him. After Mass he refused to write or dictate; indeed he put away his writing materials. He was in the third part of the Summa, at the questions on Penance. And brother Reginald, seeing that he was not writing, said to him: 'Father, are you going to give up this great work, undertaken for the glory of God and to enlighten the world?' But Thomas replied: 'Reginald, I cannot go on.' Then Reginald, who began to fear that much study might have affected his master's brain, urged and insisted that he should continue his writing; but Thomas only answered in the same way: 'Reginald, I cannot - because all that I have written seems to me so much straw.' Then Reginald, astonished that ... brother Thomas should go to see his sister, the countess of San Severino, whom he loved in all charity; and hastening there with great difficulty, when he arrived and the countess came out to meet him, he could scarcely speak. The countess, very much alarmed, said to Reginald: 'What has happened to brother Thomas? He seems quite dazed and hardly spoke to me!' And Reginald answered: 'He has been like this since about the feast of St. Nicholas - since when he has written nothing at all.' Then again brother Reginald began to beseech Thomas to tell him why he refused to write and why he was so stupefied; and after much of this urgent questioning and insisting, Thomas at last said to Reginald: 'Promise me, by the living God almighty and by your loyalty to our Order and by the love you bear to me, that you will never reveal, as long as I live, what I shall tell you.' Then he added: 'All that I have written seems to me like straw compared with what has now been revealed to me.'

1. The death of William Blake, 12 August 1827:

“Just before he died His Countenance became fair. His eyes Brighten'd and he burst out Singing of the things he saw in Heaven”

2. The experience of St Thomas Aquinas, 6 December 1273:

LXXIX: The witness went on to recall that while brother Thomas was saying his Mass one morning, in the chapel of St. Nicholas at Naples, something happened which profoundly affected and altered him. After Mass he refused to write or dictate; indeed he put away his writing materials. He was in the third part of the Summa, at the questions on Penance. And brother Reginald, seeing that he was not writing, said to him: 'Father, are you going to give up this great work, undertaken for the glory of God and to enlighten the world?' But Thomas replied: 'Reginald, I cannot go on.' Then Reginald, who began to fear that much study might have affected his master's brain, urged and insisted that he should continue his writing; but Thomas only answered in the same way: 'Reginald, I cannot - because all that I have written seems to me so much straw.' Then Reginald, astonished that ... brother Thomas should go to see his sister, the countess of San Severino, whom he loved in all charity; and hastening there with great difficulty, when he arrived and the countess came out to meet him, he could scarcely speak. The countess, very much alarmed, said to Reginald: 'What has happened to brother Thomas? He seems quite dazed and hardly spoke to me!' And Reginald answered: 'He has been like this since about the feast of St. Nicholas - since when he has written nothing at all.' Then again brother Reginald began to beseech Thomas to tell him why he refused to write and why he was so stupefied; and after much of this urgent questioning and insisting, Thomas at last said to Reginald: 'Promise me, by the living God almighty and by your loyalty to our Order and by the love you bear to me, that you will never reveal, as long as I live, what I shall tell you.' Then he added: 'All that I have written seems to me like straw compared with what has now been revealed to me.'

Relativism

It's hard to measure what's going on, because currencies have turned out to be rulers made out of very stretchy elastic - especially for us Brits, recently.

In this article, Kurt Kasun reproduces a chart from Marc Faber's latest newsletter, showing an estimated drop of c. 50% on the world's stockmarkets - a loss of some $30 trillion.

So I've looked at the Dow and the FTSE, as priced in Euros, since the Euro appears to be more stable than either the dollar or the pound sterling (until we discover the supermassive black hole at the centre of the European financial galaxy, no doubt).

Fasten your seatbelts

I've relayed rumours of these things here earlier: a dollar crash and US bond default. Now a respected Japanese ratings agency is preparing us for the reality. (htp: Karl Denninger)

Tuesday, December 23, 2008

Democratic deficit

How come I can vote several times a week at Waitrose, but only once every five years or so in national elections (and with a result that's a foregone conclusion)?

Vengeance is mine

Following comments on the last post, I see the feeling that scores should be settled is spreading - see Denninger and a threatening post to which he's linked.

UPDATE

And Jim Kunstler, too.

UPDATE

And Jim Kunstler, too.

Every little thing's gonna be all right

From what I read, some people are becoming survivalist: storing food, water, medicines, cash, even weapons.

Perhaps it's no coincidence that BBC is currently screening a remake of Terry Nation's gripping 1975 post-catastrophe series, "Survivors". But that series assumes that most people have died suddenly because of a virus, so the ecosystem has not been destroyed by desparate, starving victims. I don't think Survivors is the model we should use. If we are to survive, it'll be together, in our populous societies, because if society breaks down, you and I are unlikely to emerge as the last people standing. Lone heroes don't win; this is a fantasy.

I think spare supplies are a good idea, because there could be some disruption, which could affect the very young and elderly; so we need ways to keep warm, eat and have clean water in an emergency. And it's important to make your home secure against a rise in burglary, which is associated with economic downturns; and not to go out after dark without at least one or two companions. Weapons are another matter: "guns in the home are far more likely to be used against members of the household than against intruders."

Pace the doomsters, the UK and the USA will feed itself. We may end up eating more veg and less meat; and we may be using public transport instead of cars; personally, that would simply take me back to the 70s, when I was slimmer and fitter. Globally and locally, there is enough to feed the world, although not enough to overfeed it or encourage unproductive men to sire children.

Two aspects of the current crisis worry me:

1. The present method of organising resources may be replaced, not by one dreamed of by well-fed Western socialists, but by a cruel, remote, commanding elite as in North Korea or East Germany, who far from minimising scarcity will use it to get and maintain power.

2. The transition from this system to whatever replaces it, may be disorderly and involve suffering for many people.

This is why I think the underlying issue for us is to preserve and strengthen democracy, to increase the chances that both the journey and the journey's end are acceptable.

Perhaps it's no coincidence that BBC is currently screening a remake of Terry Nation's gripping 1975 post-catastrophe series, "Survivors". But that series assumes that most people have died suddenly because of a virus, so the ecosystem has not been destroyed by desparate, starving victims. I don't think Survivors is the model we should use. If we are to survive, it'll be together, in our populous societies, because if society breaks down, you and I are unlikely to emerge as the last people standing. Lone heroes don't win; this is a fantasy.

I think spare supplies are a good idea, because there could be some disruption, which could affect the very young and elderly; so we need ways to keep warm, eat and have clean water in an emergency. And it's important to make your home secure against a rise in burglary, which is associated with economic downturns; and not to go out after dark without at least one or two companions. Weapons are another matter: "guns in the home are far more likely to be used against members of the household than against intruders."

Pace the doomsters, the UK and the USA will feed itself. We may end up eating more veg and less meat; and we may be using public transport instead of cars; personally, that would simply take me back to the 70s, when I was slimmer and fitter. Globally and locally, there is enough to feed the world, although not enough to overfeed it or encourage unproductive men to sire children.

Two aspects of the current crisis worry me:

1. The present method of organising resources may be replaced, not by one dreamed of by well-fed Western socialists, but by a cruel, remote, commanding elite as in North Korea or East Germany, who far from minimising scarcity will use it to get and maintain power.

2. The transition from this system to whatever replaces it, may be disorderly and involve suffering for many people.

This is why I think the underlying issue for us is to preserve and strengthen democracy, to increase the chances that both the journey and the journey's end are acceptable.

Monday, December 22, 2008

Why banks?

Banks require re-capitalisation. The capital is required to cover losses. Capital is also needed for assets returning onto their balance sheet (as the vehicles of the “shadow banking system” are unwound). This capital is required to restore bank balance sheets. Additional capital will be needed to support future growth. Availability of capital, high cost of new capital and dilution of earnings will impinge upon future performance.

Satyajit Das (htp: Jesse)

Nope. Banks need destroying, as does all this bank-created debt. The mistake is to try to keep things as they are. How did we come to buy houses "on tick", then cars, and now our clothes and groceries? Why is there any lending for consumption, seeing how it only means reduced future consumption? Why should banks be kept going, requiring a significant proportion of our earnings, so that wages have to be high for us to live on what's left, making us uncompetitive with the developing world?

I am reminded of the pitiless response of the Comte d'Argenson to the satirist, Desfontaines:

Desfontaines: I must live.

D'Argenson : I do not see the necessity.

Satyajit Das (htp: Jesse)

Nope. Banks need destroying, as does all this bank-created debt. The mistake is to try to keep things as they are. How did we come to buy houses "on tick", then cars, and now our clothes and groceries? Why is there any lending for consumption, seeing how it only means reduced future consumption? Why should banks be kept going, requiring a significant proportion of our earnings, so that wages have to be high for us to live on what's left, making us uncompetitive with the developing world?

I am reminded of the pitiless response of the Comte d'Argenson to the satirist, Desfontaines:

Desfontaines: I must live.

D'Argenson : I do not see the necessity.

Sunday, December 21, 2008

The lesser of two weevils

In an apocalyptic - but carefully-reasoned - post, Karl Denninger says that when the deficit expansion stops, US government spending will have to be cut by 50 - 60%, unless there is to be a "general default" on debts.

I have no idea what a general default would look like, but in a closely-interwoven and distant-from-nature modern industrial society I can only fear it might prove utterly destructive. So we're back to contemplating the lesser, but still vast disaster.

I also have no idea how much worse it might be in the UK.

Someone else please read this unberobed OT prophet and tell me where he's wrong.

PS

While the Obama Administration cannot take a 'weak dollar' policy it is the only practical way to correct the imbalances brought about by the last 20 years of systemic manipulation. It is either that, or the selective default on sovereign debt, most likely through conflict, a hot or cold war.

Subscribe to:

Posts (Atom)