Sunday, January 04, 2009

Disaster deferred (and increased), not averted

Karl Denninger goes back to basics, explaining how the reflation is merely paying you-now from you-future's account. Knit faster, we're running out of wool.

Saturday, January 03, 2009

Murky business

Brad Setser does a very interesting bit of detective work and concludes that much of the UK's holdings of US Treasury securities, are on behalf of China. He gives us a graph demonstrating that when the UK's official holding declines sharply (usually in June), China's suddenly rises.

Setser estimates that China owns $1.425 trillion in Treasuries and Agencies, which is equivalent to about 10% of US GDP. ("Treasuries" are debts directly owed by the US Government, "agencies" are debts of the US Government's organisations, as explained in this Federal Reserve handbook from 2004.)

He ends by calling for more transparency in British accounts of these holding - that would be most welcome all round, generally. Half our problems (and, I assume, opportunities for fatcat swindlers) stem from our not knowing the real position of the world's finances.

Setser estimates that China owns $1.425 trillion in Treasuries and Agencies, which is equivalent to about 10% of US GDP. ("Treasuries" are debts directly owed by the US Government, "agencies" are debts of the US Government's organisations, as explained in this Federal Reserve handbook from 2004.)

He ends by calling for more transparency in British accounts of these holding - that would be most welcome all round, generally. Half our problems (and, I assume, opportunities for fatcat swindlers) stem from our not knowing the real position of the world's finances.

Pop

Perhaps the fall will be faster.

In this piece, Charles Biderman explains that the value of a stock is set by marginal purchases, which do not reflect what you'd get if you sold all the company's shares at the same time. He estimates that from 2003-2007 the world's equities increased in notional value by $25 trillion, on nothing more than $1.5 trillion cash, a bit of borrowing and mostly, illusion: "Market cap and money aren't necessarily related."

When the illusion goes pop, so do all the gains. First out gets the most.

htp: zgirl

In this piece, Charles Biderman explains that the value of a stock is set by marginal purchases, which do not reflect what you'd get if you sold all the company's shares at the same time. He estimates that from 2003-2007 the world's equities increased in notional value by $25 trillion, on nothing more than $1.5 trillion cash, a bit of borrowing and mostly, illusion: "Market cap and money aren't necessarily related."

When the illusion goes pop, so do all the gains. First out gets the most.

htp: zgirl

Elliot, Kondratieff, or normal service resumed?

On 26th June I looked at the progress of the FTSE since around 1984 and thought that the next low would be no worse than c. 4,500. Here's what actually happened:

The lows were certainly lower, and we have only recently learned just how close we came to a banking collapse. The question now is, are we where we "should" be - following a trend set by the last 25 years - or are there longer cycles due to make hay of the pattern of the last quarter-century? Elliot wavers and Kondratieff followers say yes.

My guess is that, after the steep stockmarket falls and the horrid crisis apparently averted, there will be a bounce in the next 1-2 years, then a decline in real (inflation-adjusted) terms for maybe another 5 years after that. Your guess?

By the way, I'd also be interested to know your views on why the bankers and brokers have been allowed to Get Away With It. To me, it seems like a big fat moral hazard and unless there is some real squealy punishment for all this bad behaviour, I'd advise any bright, conscienceless youngster to become a banker.

Currently, my preferred fantasy solution is to bust all the overextended banks, leave the shareholders with zilch, sack the senior bank managers and ban them from being company directors for at least 5 years, halve all mortgages, and give the book of business to more prudent operators including well-run building societies. In my view, this was never ever going to happen, because the FSA, the BoE and the government are also implicated. So, not so much "too big to fail", but too well-connected to fail.

But there's a price to pay, anyway: it's now clearly Us and Them. Perhaps, since they are immeasurably more powerful, we should give up trying to rectify the world and merely ape their cynicism and corruption. Moralists will demur; and so this is truly an age when we can say, "Affairs are now soul size".

The lows were certainly lower, and we have only recently learned just how close we came to a banking collapse. The question now is, are we where we "should" be - following a trend set by the last 25 years - or are there longer cycles due to make hay of the pattern of the last quarter-century? Elliot wavers and Kondratieff followers say yes.

My guess is that, after the steep stockmarket falls and the horrid crisis apparently averted, there will be a bounce in the next 1-2 years, then a decline in real (inflation-adjusted) terms for maybe another 5 years after that. Your guess?

By the way, I'd also be interested to know your views on why the bankers and brokers have been allowed to Get Away With It. To me, it seems like a big fat moral hazard and unless there is some real squealy punishment for all this bad behaviour, I'd advise any bright, conscienceless youngster to become a banker.

Currently, my preferred fantasy solution is to bust all the overextended banks, leave the shareholders with zilch, sack the senior bank managers and ban them from being company directors for at least 5 years, halve all mortgages, and give the book of business to more prudent operators including well-run building societies. In my view, this was never ever going to happen, because the FSA, the BoE and the government are also implicated. So, not so much "too big to fail", but too well-connected to fail.

But there's a price to pay, anyway: it's now clearly Us and Them. Perhaps, since they are immeasurably more powerful, we should give up trying to rectify the world and merely ape their cynicism and corruption. Moralists will demur; and so this is truly an age when we can say, "Affairs are now soul size".

Thursday, January 01, 2009

Am I the idiot, or are they?

For years, at least since the Reagan era, we in the US have heard the Republican Party mantra that the answer to growing the economy is to cut taxes for the richest, since they will 'invest in business'.

It never made sense to me, especially as I saw such a transfer of wealth to those same rich people, who spent their money on luxury imported goods. Incomes for the middle and lower class barely kept pace with inflation, even as industry became ever more efficient.

Today, thanks to posts here and elsewhere, I finally realized what is wrong with the claim above: buying stocks does not 'invest in a company', unless you are buying stock directly from that same company. All it does is put money in the pockets of the stockbrokers, while you have a piece of paper that must rise in value by profit plus fees, and find another sucker to buy it. The real estate market is no different.

Nonetheless, all of the experts that I have talked with over the years insisted that I simply didn't understand, implying that I was an idiot. Am I?

It never made sense to me, especially as I saw such a transfer of wealth to those same rich people, who spent their money on luxury imported goods. Incomes for the middle and lower class barely kept pace with inflation, even as industry became ever more efficient.

Today, thanks to posts here and elsewhere, I finally realized what is wrong with the claim above: buying stocks does not 'invest in a company', unless you are buying stock directly from that same company. All it does is put money in the pockets of the stockbrokers, while you have a piece of paper that must rise in value by profit plus fees, and find another sucker to buy it. The real estate market is no different.

Nonetheless, all of the experts that I have talked with over the years insisted that I simply didn't understand, implying that I was an idiot. Am I?

Tuesday, December 30, 2008

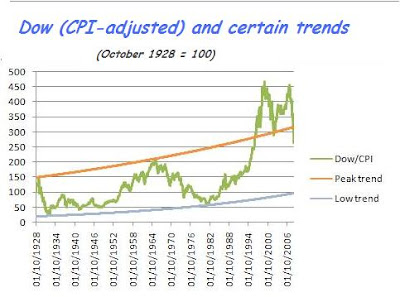

Fun with extrapolation

Since the 1990s, the stockmarket has been showing such freakish returns that many thought we were in a "new paradigm", whatever that means.

So I've looked at the Dow adjusted for CPI since late 1928, and calculated max/min lines on the basis of the highs in 1929 and 1966, and the lows in 1932 and 1982, to see just how unrepresentative the last decade has been. If we saw a return to these imaginary trends, the next Dow low could be less than half the present value. If, if, if...

Coincidentally, Jim Kunstler is predicting much the same:

By May of 2009, the stock markets will resume crashing with the ultimate destination of a Dow 4000 before the end of the year.

But I think it may take longer than that. The Elliott-wavers are looking for a final upwave first. Having said that, the last 10 years have been out of all comparison with the 70 years before.

Monday, December 29, 2008

Debt forgiveness, inflation and welching

Thus Jesse, discussing Michael Hodges' visionary "Grandfather Economic Report" and US indebtedness:

In a simple handwave estimate, one might say that the debt will have to be discounted by at least half. That includes inflation and selective defaults...

... something has got to give. The givers will most likely be all holders of US financial assets, responsible middle class savers, and a disproportionate share of foreign holders of US debt.

While the debtors hold the means of payment in dollars and the power to decide who gets paid, where do you think the most likely impact will be felt?

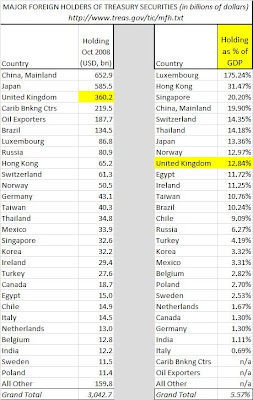

I give below the US Treasury's data on foreign holdings of their government securities as at October 2008, but I also reinterpret it in the light of each country's GDP, to show relative potential impact (please click on image to enlarge).

Mind you, even a complete repudiation would only take care of $3 trillion. Funny how not so long ago, $1 trillion seemed a high-end estimate of the damage, and now it's something like seven times that. And that still leaves a long haul to get to Hodges' $53 tn - equivalent to, what, one year's global GDP?

In a simple handwave estimate, one might say that the debt will have to be discounted by at least half. That includes inflation and selective defaults...

... something has got to give. The givers will most likely be all holders of US financial assets, responsible middle class savers, and a disproportionate share of foreign holders of US debt.

While the debtors hold the means of payment in dollars and the power to decide who gets paid, where do you think the most likely impact will be felt?

I give below the US Treasury's data on foreign holdings of their government securities as at October 2008, but I also reinterpret it in the light of each country's GDP, to show relative potential impact (please click on image to enlarge).

Mind you, even a complete repudiation would only take care of $3 trillion. Funny how not so long ago, $1 trillion seemed a high-end estimate of the damage, and now it's something like seven times that. And that still leaves a long haul to get to Hodges' $53 tn - equivalent to, what, one year's global GDP?

Subscribe to:

Posts (Atom)