A letter to the Spectator (unpublished), posted here on 2nd November 2008. We seem to be edging towards the "unsurprising", though the market may give a leap of denial before then:

Sir:

Your leader (“Riders On The Storm”, 1 November) suggests that current investor sentiment is “excessively negative”. That depends upon one’s historical perspective, in both directions.

A reversion to the mean (over the last generation) for UK house prices would be some 3.5 times household income, which on 2007 figures would imply average valuations around £120,000. Turning to shares, the progress of the Dow over the past 80 years (adjusted for consumer prices) indicates that a return to 6,000 points should be unsurprising, and a low of 4,000 not impossible.

But in addition to the business cycle and recurrent bubbles, there are deep linear changes at work. While maintaining the Western consumer in his fantasy of idle wealth, the East has been building up its human and physical industrial resources. We are focussing on the present recession, but not what the world will look like afterwards. When Asia has sufficiently developed its domestic demand, it will lose its enthusiasm for US Treasury debt, and the credit markets will tear at our economies with higher interest rates. Already, the search is well under way for an alternative to the US dollar as a world trading currency; and foreign investors, sovereign wealth funds and oil-rich governments are building up holdings in our bellwether businesses (e.g. Barclays Bank), thus converting imbalance into equity and exporting our future dividends.

Besides, the Dow and FTSE companies derive an increasing proportion of their income from abroad, so stock indices no longer reflect national prosperity. Real wages have stalled, and seem set to decline against a background of rising inflation and global competition; this, plus an interest rate correction, might strengthen the downward trend for house prices.

In short, successive governments have failed to repair our economic structure, and bear market rallies notwithstanding, I think we must eventually recalibrate our measures of normality.

Thursday, February 26, 2009

Darwin's Bicentennial

The 'balance of Nature' is a misleading phrase. It is not a Disney-esque harmony, but the sweaty struggle of wrestlers, with efficiency of predation competing with that of procreation. A small change in environment, or the introduction of a new disease or species can lead to rapid extinction.

If an ecological niche opens, or gains resources, there is an explosion of varieties. When resources are abundant and predators scarce, even the weaker ones can thrive for a while. This explains the fat, waddling dodo.

The Industrial Revolution, and the Agricultural one that came before it, were the product of a few minds, and the sweat of many. They drove the move to more cities, which meant larger companies and bigger government. This widened the niche for a parasitic class of people who produce nothing, but are sometimes necessary. We call them consultants, middle managers, investment specialists (sorry Sackerson!), marketing gurus, guidance and life coaches, and the like.

With no predators, and a virtually infinite supply of resources (they print the money!), this class grew like a cancer. We have now reached the point that it consumes most of what we produce, and the system is shutting down. Since the typical politician or bureaucrat is of this class, the obvious answer is to give them more. Hence the Bush stimulus package.

I could be wrong, but I think that we are simply postponing the inevitable.

If an ecological niche opens, or gains resources, there is an explosion of varieties. When resources are abundant and predators scarce, even the weaker ones can thrive for a while. This explains the fat, waddling dodo.

The Industrial Revolution, and the Agricultural one that came before it, were the product of a few minds, and the sweat of many. They drove the move to more cities, which meant larger companies and bigger government. This widened the niche for a parasitic class of people who produce nothing, but are sometimes necessary. We call them consultants, middle managers, investment specialists (sorry Sackerson!), marketing gurus, guidance and life coaches, and the like.

With no predators, and a virtually infinite supply of resources (they print the money!), this class grew like a cancer. We have now reached the point that it consumes most of what we produce, and the system is shutting down. Since the typical politician or bureaucrat is of this class, the obvious answer is to give them more. Hence the Bush stimulus package.

I could be wrong, but I think that we are simply postponing the inevitable.

Wednesday, February 25, 2009

Dow update

Adjusted for CPI inflation, the Dow is now back to where it was in December 1995.

This is still above the peak of the previous long cycle, ending in January 1966 - and still over 4 times higher than the low of July 1982. We only think of it as catastrophic because we got used to more recent, wildly inflated valuations.

I'm still hoping that the end position will be no worse than 4,000 points - a drop of 45% from today's close.

This is still above the peak of the previous long cycle, ending in January 1966 - and still over 4 times higher than the low of July 1982. We only think of it as catastrophic because we got used to more recent, wildly inflated valuations.

I'm still hoping that the end position will be no worse than 4,000 points - a drop of 45% from today's close.

Theft by inflation has begun already

The UK Debt Management Office website shows that a UK Treasury bond offering 5% annual interest is, because of its current traded price, actually yielding 2.522793%.

But the risk of default, almost as high as Italy's government debt and far higher than even the USA's, is (as Jesse quotes) currently priced at 1.63%. (The market currently prices the risk of USA default at 1%.)

So after insuring for risk, 5-year UK sovereign debt earns you less than 0.893%.

Inflation, as measured by the Consumer Price Index*, now runs at 3%. In other words, a "safe" government bond loses you more than 2% a year.

And that's before inflation really gets going.

_____________________________________

*The Retail Price Index is a different measure of inflation, which takes into account mortgage costs. So after recent savage cuts in the bank rate, currently RPI should be negative. But wait until the private capital credit strike leads to higher interest rates, and judge.

But the risk of default, almost as high as Italy's government debt and far higher than even the USA's, is (as Jesse quotes) currently priced at 1.63%. (The market currently prices the risk of USA default at 1%.)

So after insuring for risk, 5-year UK sovereign debt earns you less than 0.893%.

Inflation, as measured by the Consumer Price Index*, now runs at 3%. In other words, a "safe" government bond loses you more than 2% a year.

And that's before inflation really gets going.

_____________________________________

*The Retail Price Index is a different measure of inflation, which takes into account mortgage costs. So after recent savage cuts in the bank rate, currently RPI should be negative. But wait until the private capital credit strike leads to higher interest rates, and judge.

How long will the bear market last?

Jesse quotes this comparison of the current bear market with three previous ones, mixing stats for the Dow and the S&P 500:

I'd suggest we should look at when the recent bubble really burst - end 1999, then desperately disguised by monetary inflation from 2002/03 onwards; if that's right, we have maybe another 6 years to go through.

I'd suggest we should look at when the recent bubble really burst - end 1999, then desperately disguised by monetary inflation from 2002/03 onwards; if that's right, we have maybe another 6 years to go through.

But taking similar periods for the Dow only, adjusting for CPI inflation, and adding the long period from 1966 to 1982, we get this:

I'd suggest we should look at when the recent bubble really burst - end 1999, then desperately disguised by monetary inflation from 2002/03 onwards; if that's right, we have maybe another 6 years to go through.

I'd suggest we should look at when the recent bubble really burst - end 1999, then desperately disguised by monetary inflation from 2002/03 onwards; if that's right, we have maybe another 6 years to go through.

The shapes of these two lines do sort of rhyme, don't they? And if so, looking at where the end of the red line is, maybe a bear market rally is now due, like the c. '75 - '76 mini-recovery.

End point in real terms this time, my guess, is the equivalent of 4,000 points today. However, there are features unique to the present situation, especially the size of debts, the loss of much of the West's manufacturing base, and the interconnectedness of modern world markets and economies.

Tuesday, February 24, 2009

Cash (equivalent) and gold - iTulip

Our primary concern at this stage is no longer our readers' portfolios but their ability to weather a US dollar crisis if one erupts. In response, we are increasing our gold allocation to 30% and moving all Treasury holdings to the very shortest maturities, to three month Treasury bills, until we see indications that conditions are stabilizing. We encourage you to engage with the community to actively discuss strategies that are appropriate for you.

The rest is here.

The rest is here.

Sunday, February 22, 2009

Good luck, right action

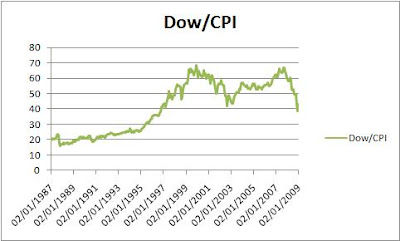

Reportedly, George Soros doesn't see the bottom of the market yet. We judge by recent experience and think ourselves hard done by, yet look at the following chart, which takes the Dow and adjusts it for inflation:

What they're really talking about is inflation. Debt, which is fixed in nominal terms, becomes cruelly heavier as the assets pledged against it become worth less and less. The pain will get so bad that the government will crack, as it always does, and debauch the currency. Holding cash just now is great, for those lucky enough to have it; but if Robin Hood can't confiscate it through taxation, he'll bleed it white by printing lots more fiat currency for himself (and the people who keep voting for him), so sucking real value out of your money. If you can't face investing, be prepared to spend like a sailor on shore leave when inflation hits town.

My clients generally aren't traders. In the same interview cited above, Faber said:

Recently I bought some U.S. stocks for the first time in a long time. If you buy Intel , Cisco , Yahoo! , Oracle and Microsoft , you will do much better in the next 10 years than you would with Treasuries. These stocks will double and even triple -- before going to zero.

That's not for my clients - they like the idea of the double and triple (who doesn't?), but not enough to risk the "going to zero".

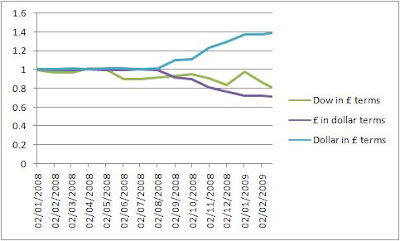

That said, investment - including in commodities - is going to be part of their fight back against the attempt to take away everything they've saved. Inflationary periods do sap the real value of shares, they hit cash even worse. Look at the position of the man who invested in the (dollar-denominated) Dow from the start of 2008 up till last Friday's seeming debacle, compared with the poor chap who "played safe" and held good old British pounds:

All that has happened is that the illusory gains of the last 12 years, more than accounted for by extra debt taken on in that time, have now unwound. Yet we're still nowhere near where we were in 1987, which (if you were around then) we thought of as an exciting time for investment. To get back to that peaklet in real terms, the Dow would have to drop below 5,000 points.

But to return to the low point of the recession that preceded it - around July 1982 - the Dow would have to break down below 1,800. Even then, that miserable score is a big advance on the low of 50 years before that (July 1932: CPI-adjusted Dow would equate to c. 833 points).

Karl Denninger has said recently that he sees 2,000 points as a possibility; I've suggested a low of c. 4,000, because in these 40-year cycles, each peak and each low has been higher than in the previous cycle.

However, seeing how unbelievably high the Dow went in recent years (way above anything that could have been extrapolated from the highs of 1929 and 1965!), maybe a correspondingly low low is not out of the question.

So why am I planning to set up a new brokerage on my own? Why don't I send a copy of this blog to all my clients, together with news of my retirement from the industry and a valedictory "Good luck, because you're going to need it"? (Actually, I have repeatedly advertised this blog to clients; I only wish the viewing stats could show me that they all read it.)

The Mogambo Guru has taken to signing off his rants with a sarcastic "Wheee! This investing stuff is easy!" - he recommends gold, silver and oil. Over on Financial Sense a couple of days ago, Martin Goldberg opines, "The important question for most investors is whether to be in cash or gold" (cash for now, he thinks). Marc Faber has long been saying that we are entering a long bull market in commodities, and has just said he thinks an ounce of gold will one day be worth more than the Dow.What they're really talking about is inflation. Debt, which is fixed in nominal terms, becomes cruelly heavier as the assets pledged against it become worth less and less. The pain will get so bad that the government will crack, as it always does, and debauch the currency. Holding cash just now is great, for those lucky enough to have it; but if Robin Hood can't confiscate it through taxation, he'll bleed it white by printing lots more fiat currency for himself (and the people who keep voting for him), so sucking real value out of your money. If you can't face investing, be prepared to spend like a sailor on shore leave when inflation hits town.

My clients generally aren't traders. In the same interview cited above, Faber said:

Recently I bought some U.S. stocks for the first time in a long time. If you buy Intel , Cisco , Yahoo! , Oracle and Microsoft , you will do much better in the next 10 years than you would with Treasuries. These stocks will double and even triple -- before going to zero.

That's not for my clients - they like the idea of the double and triple (who doesn't?), but not enough to risk the "going to zero".

That said, investment - including in commodities - is going to be part of their fight back against the attempt to take away everything they've saved. Inflationary periods do sap the real value of shares, they hit cash even worse. Look at the position of the man who invested in the (dollar-denominated) Dow from the start of 2008 up till last Friday's seeming debacle, compared with the poor chap who "played safe" and held good old British pounds:

The picture will change when the dollar dives, of course; though maybe the pound will dive along with it. To hold what you have, you'll have to keep on your feet, balancing the relative merits of currencies and asset classes. For me and most of my clients, it won't be about getting rich; it'll be about not getting robbed.

I'd have been happier with a world where money kept its value, and I'm not alone. The blogosphere is now crowded with people who have their own schemes for a fair and just economic world. But none of these ideal arrangements will enter into reality. There's too much to be made out of destroying it, by a handful of traders, and the politicians - and the bankers who will eventually employ the politicians when they leave office. We must take, not the right action, but the appropriate action.

Good luck, because you're going to need it.

Subscribe to:

Posts (Atom)