An essay on the basic argument for trade, at Mises. But the author does admit a problem with externalised costs that aren't taken into account.

A thought: what if we in the UK really don't have much of a comparative advantage in any area, long-term? Once the East has caught up on skills, what do we have that anyone will want to buy?

And what about the monetary distortions in the market? It's like Monopoly with some players cheating by using secret stashes of extra banknotes.

Are the economists misled by an idealised picture of economics?

Wednesday, July 16, 2008

Will the UK/US trade balance influence the dollar value of sterling?

Here's some trade stats for UK/USA. Last year, we imported $6.6 billion more from the US than we exported to them. Last night, the exchange rate for the pound rose above US$2.00. For some time, we seem to have been shadowing the dollar, but do we have an incentive to allow the dollar to fall further against the pound?

Or will we be more influenced by the desire not to devalue the amount we have loaned to the US via Treasury bonds? And then there is the possible extra unemployment that could result from UK goods becoming more expensive in dollar terms.

Any forex experts care to give a view?

UPDATE: Here's the answer, it seems:

Weak jobs data knocks pound vs dollar and euro (Reuters)

UPUPDATE: ...And here's a different answer:

Sterling up versus dollar, banks support (Reuters)

Wouldn't roulette be more honest, somehow? "Manque! Pair! Impair! Passe! Noir! Rouge! Numero 17!"

Or will we be more influenced by the desire not to devalue the amount we have loaned to the US via Treasury bonds? And then there is the possible extra unemployment that could result from UK goods becoming more expensive in dollar terms.

Any forex experts care to give a view?

UPDATE: Here's the answer, it seems:

Weak jobs data knocks pound vs dollar and euro (Reuters)

UPUPDATE: ...And here's a different answer:

Sterling up versus dollar, banks support (Reuters)

Wouldn't roulette be more honest, somehow? "Manque! Pair! Impair! Passe! Noir! Rouge! Numero 17!"

Tuesday, July 15, 2008

How far can the FTSE fall?

The FTSE hit a long-term low at 3,287 at the close of 12 March 2003. If it were to drop to 5,000 now, that would still mean about 8% p.a. compound growth.

Bank deposits are investments, and can go wrong

Karl Denninger takes us back to basics about banks and "your money" (highlighting is mine):

I want to talk about IndyMac for a bit.

The news has covered a few really, truly sad stories. People with $200,000, $300,000, $400,000 or more in there who have seen 50% of their balance over $100k disappear overnight.

Older people who literally have their life savings in these institutions. People who are relatively unsophisticated, but have been told through the years that the government will make it all ok, and who believed it.

It tugs at your heart to see a 70+ year old man pleading for them to let him have his money - money that he worked and saved a lifetime for.

If only it were that easy.

People don't think of a bank as being an investment, but it is.

You are lending your money to the bank so they can make money with it, and they pay your a coupon - interest, or the "safekeeping" in the case of a checking account that does not pay interest - in return!

I want to talk about IndyMac for a bit.

The news has covered a few really, truly sad stories. People with $200,000, $300,000, $400,000 or more in there who have seen 50% of their balance over $100k disappear overnight.

Older people who literally have their life savings in these institutions. People who are relatively unsophisticated, but have been told through the years that the government will make it all ok, and who believed it.

It tugs at your heart to see a 70+ year old man pleading for them to let him have his money - money that he worked and saved a lifetime for.

If only it were that easy.

People don't think of a bank as being an investment, but it is.

You are lending your money to the bank so they can make money with it, and they pay your a coupon - interest, or the "safekeeping" in the case of a checking account that does not pay interest - in return!

US banks: uninsured deposits stand at $2.6 trillion

Mish calculates the potential for disaster if depositors lose confidence:

"FDIC Recap

There is $6.84 Trillion in bank deposits.

$2.60 Trillion of that is uninsured.

Total cash on hand at banks is $273.7 Billion."

So 89% of uninsured deposits are not covered by available cash in the bank.

"FDIC Recap

There is $6.84 Trillion in bank deposits.

$2.60 Trillion of that is uninsured.

Total cash on hand at banks is $273.7 Billion."

So 89% of uninsured deposits are not covered by available cash in the bank.

Monday, July 14, 2008

TMS a better measure of the money supply?

What looks like an important idea and discussion of "True Money Supply" in Mish. I shall have to chew on it for a bit, but thought the finance-oriented reader might care to do the same.

Mish says when you look at the situation correctly, we are definitely in DEflation.

Mish says when you look at the situation correctly, we are definitely in DEflation.

Ron Paul and Tibet: is he right?

House and Senate Pass Resolutions on Chinese Crackdown of Tibet

On Wednesday, the House overwhelmingly passed a resolution calling on China to “end its crackdown on Tibet and release Tibetans imprisoned for “nonviolent” demonstrations.” The resolution passed on a vote of 413-1, with ”Rep. Ron Paul, R-Texas, who recently dropped out of the presidential race, was the lone congressman voting against it.”

(Reuters)

This entry is given prominence in Reuters' site (world news section), but is three months old, a point I didn't spot at first. Still, I think the underlying issues are enduring and (given the imminent start of the Games) topical.

The almost-complete unanimity of the vote seems rather suspicious, but although we are used to the army being out of step with Ron Paul in financial matters, is he right in this case? Some might think you cannot have a policy of "liberty in one country", any more than "socialism in one country."

Can't find much in Google News about it, but here's a bit of blog discussion, updated here.

On Wednesday, the House overwhelmingly passed a resolution calling on China to “end its crackdown on Tibet and release Tibetans imprisoned for “nonviolent” demonstrations.” The resolution passed on a vote of 413-1, with ”Rep. Ron Paul, R-Texas, who recently dropped out of the presidential race, was the lone congressman voting against it.”

(Reuters)

This entry is given prominence in Reuters' site (world news section), but is three months old, a point I didn't spot at first. Still, I think the underlying issues are enduring and (given the imminent start of the Games) topical.

The almost-complete unanimity of the vote seems rather suspicious, but although we are used to the army being out of step with Ron Paul in financial matters, is he right in this case? Some might think you cannot have a policy of "liberty in one country", any more than "socialism in one country."

Can't find much in Google News about it, but here's a bit of blog discussion, updated here.

Sunday, July 13, 2008

Bear market: Steiff comes home

Chasing lower costs, Steiff outsourced around a fifth of its production to China in 2003 but has now decided to come back because of concerns about quality and staff turnover.

Steiff is one of a small number of German firms which are swimming against the tide and leaving China, despite its cheaper workforce and a burgeoning consumer population. With fuel at record highs, some cite mounting transport costs.

Production of Steiff toys, which include a distinctive long-limbed bear with a melancholy growl, will come back to Germany and other countries in Europe by the end of 2009.

(Reuters)

That's sort of heartening, except that as it continues to develop, China will deal with quality issues. Japan listened to W. Edwards Deming in the 1950s and soon "Made in Japan" meant, not cheap, tinny and shoddy, but innovative, reliable and affordable.

In any case, this is clutching at straws. Tiny companies making high-value toys won't sustain Western Europe. We need major changes if we're going to become globally competitive. For example, health and welfare provision will have to be reassessed as the budgets shrink.

And here's a big debate to come: how much education? How much benefits the economy, how much is positional (Swiss finishing school for your daughter, etc), and how much is luxury consumption, like foreign holidays and Lagerfeld dresses?

How much education is simply an illogical, implicit pretence that the government is doing something to give all children relative advantage, particularly yours? How much is to disguise unemployment? How much is to keep potential young criminals penned-in during the daytime on weekdays? How much is to baby-mind children so that women can be driven out of their homes to do low-paid work?

As the money dries up, there will be an education debate, and it will be messy.

Steiff is one of a small number of German firms which are swimming against the tide and leaving China, despite its cheaper workforce and a burgeoning consumer population. With fuel at record highs, some cite mounting transport costs.

Production of Steiff toys, which include a distinctive long-limbed bear with a melancholy growl, will come back to Germany and other countries in Europe by the end of 2009.

(Reuters)

That's sort of heartening, except that as it continues to develop, China will deal with quality issues. Japan listened to W. Edwards Deming in the 1950s and soon "Made in Japan" meant, not cheap, tinny and shoddy, but innovative, reliable and affordable.

In any case, this is clutching at straws. Tiny companies making high-value toys won't sustain Western Europe. We need major changes if we're going to become globally competitive. For example, health and welfare provision will have to be reassessed as the budgets shrink.

And here's a big debate to come: how much education? How much benefits the economy, how much is positional (Swiss finishing school for your daughter, etc), and how much is luxury consumption, like foreign holidays and Lagerfeld dresses?

How much education is simply an illogical, implicit pretence that the government is doing something to give all children relative advantage, particularly yours? How much is to disguise unemployment? How much is to keep potential young criminals penned-in during the daytime on weekdays? How much is to baby-mind children so that women can be driven out of their homes to do low-paid work?

As the money dries up, there will be an education debate, and it will be messy.

US lending market: Apocalypse Now?

Some points from Denninger's latest (summary in my words):

It's getting hot. The collapse of IndyMac may take 10% - 20% of the FDIC's balance sheet, and that's assuming a savers' panic doesn't start.

If the government underwrites Fannie Mae and Freddie Mac, the Federal public debt doubles (goes up by $5 trillion), the US' credit rating is compromised (it's starting to happen already) and all debts will cost more in interest - maybe 3% extra. KD's recommendation is that the two monster lenders be put into receivership and wound down over time; this means a steep drop in house prices so that they can be afforded on more sensible terms and conditions.

His advice to you: head for the high ground. Get out of debt, get your savings balance below the FDIC's $100k ceiling, think about buying Treasury bonds. "If the government goes down you will need steel, lead and brass, not money."

BUT...

See Jim from San Marcos on the same matter. And someone copied Denninger's piece whole into a comment at Jim's, to which the latter responded:

"There is a very peculiar situation here from a stock ownership position. These two stocks are being shorted en-mass. I kind of get the feeling that neither one is going to zero. I smell a bear trap here. You can be right but still be dead wrong."

It's getting hot. The collapse of IndyMac may take 10% - 20% of the FDIC's balance sheet, and that's assuming a savers' panic doesn't start.

If the government underwrites Fannie Mae and Freddie Mac, the Federal public debt doubles (goes up by $5 trillion), the US' credit rating is compromised (it's starting to happen already) and all debts will cost more in interest - maybe 3% extra. KD's recommendation is that the two monster lenders be put into receivership and wound down over time; this means a steep drop in house prices so that they can be afforded on more sensible terms and conditions.

His advice to you: head for the high ground. Get out of debt, get your savings balance below the FDIC's $100k ceiling, think about buying Treasury bonds. "If the government goes down you will need steel, lead and brass, not money."

BUT...

See Jim from San Marcos on the same matter. And someone copied Denninger's piece whole into a comment at Jim's, to which the latter responded:

"There is a very peculiar situation here from a stock ownership position. These two stocks are being shorted en-mass. I kind of get the feeling that neither one is going to zero. I smell a bear trap here. You can be right but still be dead wrong."

Saturday, July 12, 2008

Roubini: bailing out government mortgage lenders could downgrade the USA's national credit rating

If we fiscalize all of these losses the U.S. may fast lose its AAA sovereign debt rating and eventually end up like an insolvent banana republic.

Nouriel Roubini, quoted in Mish's.

Nouriel Roubini, quoted in Mish's.

The housing bubble: 5 - 12 years to the turn

According to iTulip, we are at Step D in a timetable (published in January 2005) that implies we have quite some years to go before a housing upturn.

Their point about real estate being an illiquid market seems valid to me, and I've suggested before now that we should expect a decline and a long stall, rather than an equity-style crash.

Their point about real estate being an illiquid market seems valid to me, and I've suggested before now that we should expect a decline and a long stall, rather than an equity-style crash.

Zimbabwe: racism and international meddling

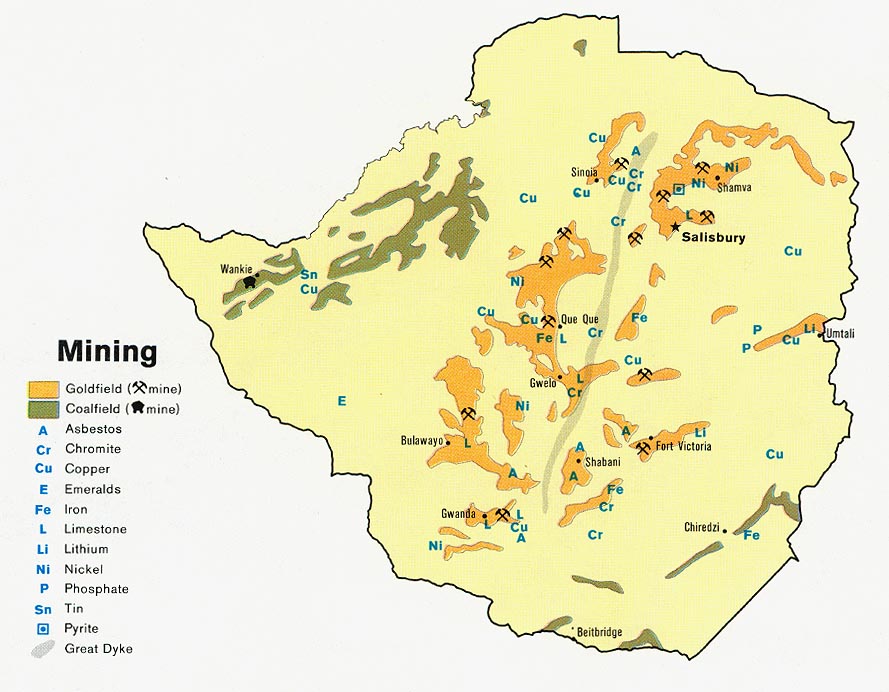

Mines in Zimbabwe

Mines in ZimbabweZimbabwe on Saturday welcomed the failure of a Western-backed U.N. Security Council resolution to impose sanctions over its violent presidential elections, calling it a victory over racism and meddling in its affairs. (Reuters)

Racist...

Robert Mugabe is a member of the Shona tribe (as is opposition leader Morgan Tsvangirai), which comprises 70% of the population of Zimbabwe, occupying the centre and north of the country.

The Matabele (Ndebele) tribe, who tend to live in the southern part, make up half of the remaining minority, and (not surprisingly, in view of their post-Independence massacres by Mugabe's troops) are supporters of the MDC (Movement for Democratic Change). ''The denial of food to opposition strongholds has replaced overt violence as the government's principal tool of repression,'' the ICG wrote in August 2002.

Meddling...

Zimbabwe's natural resources include "coal, chromium ore [10% of the world's reserves], asbestos, gold, nickel, copper, iron ore, vanadium, lithium, tin, platinum group metals" (CIA World Factbook), and there are 10 or so foreign-owned mining companies operating there. The Zimbabwean kleptocracy has turned from seizing farms (which they either don't know how to run, or can't be bothered to), to grabbing controlling interests in foreign-owned firms, and a 25% no-compensation stake in mining companies. Presumably, in the latter case, they'll leave the operational side to the experts.

In 2005, the Chinese government and Chinese businesses supplied T-shirts for ZANU-PF supporters, jets and trucks for the Army, and the architectural plans and blue tiles for Mugabe's new 25-bedroom mansion. The recent attempt (April 2008) to ship a load of arms in, so that Mr Mugabe could deal with his little local difficulty, was described by the Chinese as "normal military trade". Annual trade between these two countries was expected to reach $500 million this year.

Zimbabwe is touting Russia for trade and business deals, including tourism (uniformed hunting trips in Matabeleland?)

Perhaps the reason 84-year-old Mugabe is hanging on, is that he and his entourage have a tiger by the tail. How could they get out of their land-locked country alive?

UPDATE

But why Russia? The New York Times fishes for an explanation as to why Russia indicates some willingness to consider sanctions, and then reneged, dragging China with her. The NYT is baffled, limply quoting the US Ambassador to the UN: “Something happened in Moscow.”

Could it be that Zimbabwe in itself has little interest for Russia, but this veto is a dog-whistle to other African nations where the Ivans may develop more serious business links?

Or could it be, as this blogger hypothesises, part of the Great Game between Russia and the US, particularly reflecting missile defence technology?

How skilfully does Robert Mugabe, the Dom Mintoff of East Africa, play off great nations against one another! If only his skills benefitted his country, also.

Stephen Glover, in today's Grumbler:

The English libel laws used to be much loved by the rich and famous, and to a large degree London remains the libel capital of the world to which freebooters of all nationalities, including our own, flock in order to pick up some usually undeserved loot.

Now these and other folk have fastened on to Article Eight of the Human Rights Act. Of course, their and everyone else's privacy must be respected, but so must the right of a free Press to write about the private misbehaviour - more often financial rather than sexual - of the rich and powerful.

Does Mr Glover think this should apply to celeb journalists, also? It seems to me that some members of the Fourth Estate are rich and powerful, when compared to the rest of us.

The English libel laws used to be much loved by the rich and famous, and to a large degree London remains the libel capital of the world to which freebooters of all nationalities, including our own, flock in order to pick up some usually undeserved loot.

Now these and other folk have fastened on to Article Eight of the Human Rights Act. Of course, their and everyone else's privacy must be respected, but so must the right of a free Press to write about the private misbehaviour - more often financial rather than sexual - of the rich and powerful.

Does Mr Glover think this should apply to celeb journalists, also? It seems to me that some members of the Fourth Estate are rich and powerful, when compared to the rest of us.

Signs of the times

A BBC Radio 4 topical news comedy programme says that you can't make a movie featuring recession. I beg to differ. I think that we get reflections of how things are now, and inklings of things to come, from contemporary culture - think of Stravinsky's Rites of Spring and how the world changed shortly afterwards. Look out for films that echo these:

And I read long ago that some professional investors look for all sorts of straws in the wind, for example, the length of women's skirts (shorter = more confident, boomtime).

Any similar?

UK economy: between a rock and a hard place

CU has asked me to comment on his latest post on the UK's economic crisis. I'm flattered that someone thinks my opinion is worth anything, but here's my effort:

There's often a kind of self-destructive excitement as a crisis develops, as at the gathering of forces for a war. But the Rupert Brookes will be succeeded by the Wilfred Owens.

I have believed for about 9 years that we are in for an unpleasant time, and that is why I returned to the public sector pro tem at the end of 1999: I really did (and do) think that everybody should prepare for a storm. I have also been encouraging my clients to become/stay cautious, for the last 10 years. I thought we'd returned to sanity in 2003, when the FTSE had halved from its start-2000 peak, but off we went again. From my amateur perspective (and who exactly is an expert on the world economy?), the delay in facing economic reality has allowed the patient's condition to worsen.

Mark Wadsworth's opening comment here was "Sell to rent. Cash is King." Yes, I agree, at this stage. I was talking to my wife last year about selling the house (and, I think, the year before that) but personal circumstances and priorities often trump the cold financial calculations, don't they?

However, I don't think cash will be king for a long period. I can't see the government rapidly shrinking the public sector, and at the same time we shall see reduced earnings, more insolvencies and increasing unemployment in the private sector. The financial sector, which has helped our nation's books to nearly balance, is being hit in banking and investment now, and will (I think) be hit worse in future; that cow will yield far less milk to the Treasury, and so the budget will be even more unbalanced than it is today.

Europe seems keen to enforce a discipline on the Chancellor of the Exchequer, that it has been unwilling to emulate with respect to its own accounts for many years; if the EU continues to take such a rigid line, maybe there will be a tear in the EU fabric, along the line of the English Channel.

Meanwhile, I think Gordon Brown's reputation as a money manager is ruined. As has been said, he failed to fix the roof when the weather was fine. A playboy can seem a financial wizard as long as he keeps partying on his yacht, but the adoring guests will disembark when the holes below the waterline make themselves felt.

(I wonder what would have happened if the Conservatives had won again in 1997? Can we be confident that the consequences would have been better?)

To right the ship of State will take money, or (since we hardly know what faith to place in money any more) perhaps it would be apter to say, wealth. This, I think, is where the "cash is king" slogan will wear thin. At the moment, we see a devaluation/destocking in houses, cars, computers and other big-ticket items. It's a good time for Loadsamoney to go shopping, even if the price of his dried pasta is up 40%.

But when the stocks have been run down to match shrunken demand levels, and Loadsamoney's firm is on the skids, the game will probably change. RPI is on the up, but now the causes are more external than internal: we have forgotten the lessons of WWII and have become very dependent on imports of food and fuel, which are major components of those inflation indices that aim to reflect the circumstances of the ordinary person. So interest rate rises are unlikely to reduce the cost of such necessities, except indirectly insofar as they may help strengthen sterling; yet a weakening in sterling is the hope for our trade in manufactures (the pound has dropped 15% or so against the Euro, in the last year). Indeed, we seem to have a policy of shadowing the plummeting US dollar, as once we shadowed the Deutschmark; perhaps, perceiving this strategy, George Soros will stage another coup, to our country's cost, again.

If revenues are down because of recession (or the D-word), where else will the Chancellor find wealth to repair the yacht? More sale of assets to sovereign wealth funds (there goes the family silver)? More bonds sold to trade-surplus foreigners (but will they have the cash, at a time when their own economies may be slumping together with Western consumer demand)? (Perhaps they will, if the US insists on handing the Chinese mortgage bail-out money - see Mish!)

Left high and dry in public view as the tide of wealth recedes, will be the billions in cash held by the crafty, the nervous and the cautious old. And the subtlest way to steal it is by inflation.

I do not know what will be the best store of wealth when major inflation strikes. All the world's gold currently above ground could be made into a cube that would fit comfortably under the arches of the Eiffel Tower (and historically, a fair bit of it could have been found not far away from the Tour Eiffel, stashed away in French ceiling-bowl lights). The gold market is small enough to be a prey to manipulation both ways.

Perhaps a safer store of value would be NS&I index-linked savings certificates. If inflation gets too bad, the easy way out for the government will be not to launch new issues, and the old ones have a maximum term of 5 years. There could theoretically be a problem for investors, in the effect of inflation between the date of maturity and the date the money is cleared in the investor's bank account, but we must hope that the government will never permit a hyperinflation.

And I note that landowners such as the Duke of Westminster have rarely sold their land because of temporary monetary inflation. Even if house prices do decline towards 3 times earnings, they will always have a value, and if rented out, will create an income. Perhaps Mark's comment would then be reversed: buy to rent, not sell to rent. Even now, as many try to get out from under the mortgage trap, there are signs that renting out property is a promising sector, since (I understand) demand is increasing faster than supply.

I'd be interested to hear other ideas.

There's often a kind of self-destructive excitement as a crisis develops, as at the gathering of forces for a war. But the Rupert Brookes will be succeeded by the Wilfred Owens.

I have believed for about 9 years that we are in for an unpleasant time, and that is why I returned to the public sector pro tem at the end of 1999: I really did (and do) think that everybody should prepare for a storm. I have also been encouraging my clients to become/stay cautious, for the last 10 years. I thought we'd returned to sanity in 2003, when the FTSE had halved from its start-2000 peak, but off we went again. From my amateur perspective (and who exactly is an expert on the world economy?), the delay in facing economic reality has allowed the patient's condition to worsen.

Mark Wadsworth's opening comment here was "Sell to rent. Cash is King." Yes, I agree, at this stage. I was talking to my wife last year about selling the house (and, I think, the year before that) but personal circumstances and priorities often trump the cold financial calculations, don't they?

However, I don't think cash will be king for a long period. I can't see the government rapidly shrinking the public sector, and at the same time we shall see reduced earnings, more insolvencies and increasing unemployment in the private sector. The financial sector, which has helped our nation's books to nearly balance, is being hit in banking and investment now, and will (I think) be hit worse in future; that cow will yield far less milk to the Treasury, and so the budget will be even more unbalanced than it is today.

Europe seems keen to enforce a discipline on the Chancellor of the Exchequer, that it has been unwilling to emulate with respect to its own accounts for many years; if the EU continues to take such a rigid line, maybe there will be a tear in the EU fabric, along the line of the English Channel.

Meanwhile, I think Gordon Brown's reputation as a money manager is ruined. As has been said, he failed to fix the roof when the weather was fine. A playboy can seem a financial wizard as long as he keeps partying on his yacht, but the adoring guests will disembark when the holes below the waterline make themselves felt.

(I wonder what would have happened if the Conservatives had won again in 1997? Can we be confident that the consequences would have been better?)

To right the ship of State will take money, or (since we hardly know what faith to place in money any more) perhaps it would be apter to say, wealth. This, I think, is where the "cash is king" slogan will wear thin. At the moment, we see a devaluation/destocking in houses, cars, computers and other big-ticket items. It's a good time for Loadsamoney to go shopping, even if the price of his dried pasta is up 40%.

But when the stocks have been run down to match shrunken demand levels, and Loadsamoney's firm is on the skids, the game will probably change. RPI is on the up, but now the causes are more external than internal: we have forgotten the lessons of WWII and have become very dependent on imports of food and fuel, which are major components of those inflation indices that aim to reflect the circumstances of the ordinary person. So interest rate rises are unlikely to reduce the cost of such necessities, except indirectly insofar as they may help strengthen sterling; yet a weakening in sterling is the hope for our trade in manufactures (the pound has dropped 15% or so against the Euro, in the last year). Indeed, we seem to have a policy of shadowing the plummeting US dollar, as once we shadowed the Deutschmark; perhaps, perceiving this strategy, George Soros will stage another coup, to our country's cost, again.

If revenues are down because of recession (or the D-word), where else will the Chancellor find wealth to repair the yacht? More sale of assets to sovereign wealth funds (there goes the family silver)? More bonds sold to trade-surplus foreigners (but will they have the cash, at a time when their own economies may be slumping together with Western consumer demand)? (Perhaps they will, if the US insists on handing the Chinese mortgage bail-out money - see Mish!)

Left high and dry in public view as the tide of wealth recedes, will be the billions in cash held by the crafty, the nervous and the cautious old. And the subtlest way to steal it is by inflation.

I do not know what will be the best store of wealth when major inflation strikes. All the world's gold currently above ground could be made into a cube that would fit comfortably under the arches of the Eiffel Tower (and historically, a fair bit of it could have been found not far away from the Tour Eiffel, stashed away in French ceiling-bowl lights). The gold market is small enough to be a prey to manipulation both ways.

Perhaps a safer store of value would be NS&I index-linked savings certificates. If inflation gets too bad, the easy way out for the government will be not to launch new issues, and the old ones have a maximum term of 5 years. There could theoretically be a problem for investors, in the effect of inflation between the date of maturity and the date the money is cleared in the investor's bank account, but we must hope that the government will never permit a hyperinflation.

And I note that landowners such as the Duke of Westminster have rarely sold their land because of temporary monetary inflation. Even if house prices do decline towards 3 times earnings, they will always have a value, and if rented out, will create an income. Perhaps Mark's comment would then be reversed: buy to rent, not sell to rent. Even now, as many try to get out from under the mortgage trap, there are signs that renting out property is a promising sector, since (I understand) demand is increasing faster than supply.

I'd be interested to hear other ideas.

Zimbabwe: racism and international meddling

Zimbabwe on Saturday welcomed the failure of a Western-backed U.N. Security Council resolution to impose sanctions over its violent presidential elections, calling it a victory over racism and meddling in its affairs. (Reuters)

Racist...

Robert Mugabe is a member of the Shona tribe (as is opposition leader Morgan Tsvangirai), which comprises 70% of the population of Zimbabwe, occupying the centre and north of the country.

The Matabele (Ndebele) tribe, who tend to live in the southern part, make up half of the remaining minority, and (not surprisingly, in view of their post-Independence massacres by Mugabe's troops) are supporters of the MDC (Movement for Democratic Change). ''The denial of food to opposition strongholds has replaced overt violence as the government's principal tool of repression,'' the ICG wrote in August 2002.

Meddling...

Zimbabwe's natural resources include "coal, chromium ore [10% of the world's reserves], asbestos, gold, nickel, copper, iron ore, vanadium, lithium, tin, platinum group metals" (CIA World Factbook), and there are 10 or so foreign-owned mining companies operating there. The Zimbabwean kleptocracy has turned from seizing farms (which they either don't know how to run, or can't be bothered to), to grabbing controlling interests in foreign-owned firms, and a 25% no-compensation stake in mining companies. Presumably, in the latter case, they'll leave the operational side to the experts.

In 2005, the Chinese government and Chinese businesses supplied T-shirts for ZANU-PF supporters, jets and trucks for the Army, and the architectural plans and blue tiles for Mugabe's new 25-bedroom mansion. The recent attempt (April 2008) to ship a load of arms in, so that Mr Mugabe could deal with his little local difficulty, was described by the Chinese as "normal military trade". Annual trade between these two countries was expected to reach $500 million this year.

Zimbabwe is touting Russia for trade and business deals, including tourism (uniformed hunting trips in Matabeleland?)

Perhaps the reason 84-year-old Mugabe is hanging on, is that he and his entourage have a tiger by the tail. How could they get out of their land-locked country alive?

UPDATE

But why Russia? The New York Times fishes for an explanation as to why Russia indicates some willingness to consider sanctions, and then reneged, dragging China with her. The NYT is baffled, limply quoting the US Ambassador to the UN: “Something happened in Moscow.”

Could it be that Zimbabwe in itself has little interest for Russia, but this veto is a dog-whistle to other African nations where the Ivans may develop more serious business links?

Or could it be, as this blogger hypothesises, part of the Great Game between Russia and the US, particularly reflecting missile defence technology?

How skilfully does Robert Mugabe, the Dom Mintoff of East Africa, play off great nations against one another! If only his skills benefitted his country, also.

How skilfully does Robert Mugabe, the Dom Mintoff of East Africa, play off great nations against one another! If only his skills benefitted his country, also.

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Friday, July 11, 2008

UK the financial "black sheep"

The UK now has the worst fiscal profile of any developed country in the North Atlantic sphere.

Daily Telegraph (htp: Mish)

Daily Telegraph (htp: Mish)

Are oil speculators to blame?

Russell Roberts at Cafe Hayek discusses a spam email from United Airlines, which blames speculation for much of the high price of oil. Naturally, he puts on his quizzical econ spectacles and says it's like blaming a thermometer for hot weather; but maybe that's just a bit too sideways.

For isn't it interesting that in 20 years, the proportion of oil contracts purchased by middlemen who don't deliver, has risen from 21% to 66%?

And isn't there a big Space Hopper of excess liquidity squmphing around the world's markets and destabilising them, as Dr Marc Faber claims? Indeed, Faber has spent years making money from predicting the future movement of this excess. In an interview on "Financial Sense" on January 12, Faber said:

... we had during the excessive consumption period 1998-2006, a current account deficit in the US that increased from 2% of GDP to over 7% of GDP, and at the end was supplying the world with $800 billion annually. And this river flows into the world through the American current account deficits, and essentially provided the world with the so-called excess liquidity and created booms in everything from art prices to commodities, stocks, bonds, real estate, what not.

I suggest that now that the Space Hopper has been punctured, the speculators riding it have been squmphing around even faster, trying to visit as many markets as they can before their toy goes totally flat.

For isn't it interesting that in 20 years, the proportion of oil contracts purchased by middlemen who don't deliver, has risen from 21% to 66%?

And isn't there a big Space Hopper of excess liquidity squmphing around the world's markets and destabilising them, as Dr Marc Faber claims? Indeed, Faber has spent years making money from predicting the future movement of this excess. In an interview on "Financial Sense" on January 12, Faber said:

... we had during the excessive consumption period 1998-2006, a current account deficit in the US that increased from 2% of GDP to over 7% of GDP, and at the end was supplying the world with $800 billion annually. And this river flows into the world through the American current account deficits, and essentially provided the world with the so-called excess liquidity and created booms in everything from art prices to commodities, stocks, bonds, real estate, what not.

I suggest that now that the Space Hopper has been punctured, the speculators riding it have been squmphing around even faster, trying to visit as many markets as they can before their toy goes totally flat.

Thursday, July 10, 2008

Time for some bankers to pack their bags

Karl Denninger continues his holy-roller rant against banks, supervisory authorities etc and reiterates the need for all the financial horror to be made plain. This is what ought to happen, but I'd have thought it's obvious that the results are likely to be so painful that delaying tactics will continue for as long as possible.

One of the outcomes, he thinks, will be major lawsuits:

We haven't even gotten to litigation risk yet, but you can bet we will. I envision racketeering suits coming in the next year or so as its rather apparent to me that this was not some "rogue deal" but rather a systematic approach to intentional understatement of risk.

I wonder how many banking and rating agency executives are even now quietly liquidating their assets and checking which countries do not have extradition agreements with the USA.

Brunei, Kuwait, the Maldives, the Philippines, Qatar, Tunisia and the UAE could be bearable; some might even allow you to buy a drink. Samoa?

Vietnam's on the rise, even if the dong is under pressure at the moment. Dr Marc Faber has an interest there, and he is no fool.

One of the outcomes, he thinks, will be major lawsuits:

We haven't even gotten to litigation risk yet, but you can bet we will. I envision racketeering suits coming in the next year or so as its rather apparent to me that this was not some "rogue deal" but rather a systematic approach to intentional understatement of risk.

I wonder how many banking and rating agency executives are even now quietly liquidating their assets and checking which countries do not have extradition agreements with the USA.

Brunei, Kuwait, the Maldives, the Philippines, Qatar, Tunisia and the UAE could be bearable; some might even allow you to buy a drink. Samoa?

Vietnam's on the rise, even if the dong is under pressure at the moment. Dr Marc Faber has an interest there, and he is no fool.

Subscribe to:

Posts (Atom)