The UK government is very fond of claiming that its decarbonisation policy is being delivered at least cost to UK citizens. Irrespective of whether one supports the policy goal, one would at least like to believe them on the cost.

Sadly, their claim is a blatant falsehood; and we can see why this is by utilizing the government's own methodologies.

A very standard way of presenting the cost-effectiveness of measures that can reduce CO2 emissions is the

Marginal Abatement Cost Curve (MACC) and we will look at some examples below. The basic concept is simple: for each measure, calculate the cost per unit of CO2 emissions reduced, and rank them from cheapest to most expensive on a bar-chart. If we pick (e.g.) a particular market segment, we can additionally plot the total absolute potential for CO2 abatement each measure can deliver in that sector (e.g. in tonnes), by making the width of each bar correspond to the amount.

Having ranked them thus, for a given target amount of reductions we can directly read off the cost of the most expensive measure required to achieve the target. And why would anyone institute measures that cost more than absolutely necessary ? Surely, they would exhaust the potential of the cheapest measures first, before proceeding to the more expensive.

Before looking at UK examples, it is interesting to note that in every MACC example one ever sees, the cheapest abatement measures are in fact

profitable - that is, they pay for themselves - in some cases, handsomely so: their 'cost' is not just cheap, it is negative. (We will consider what this means in policy terms another time.) Our first example shows this aspect clearly: it comes from DECC and is the MACC of the total potential abatement identified in the UK 'non-traded' sector (the part of the economy not subject to the EU Emissions Trading Scheme), for the period 2023–27.

|

| Source: DECC |

As can be seen, at the left-hand side there is around 90 MtCO2e abatement potential that pays for itself. We should only need to start paying for abatement if the target was in excess of that amount. The weighted average of the cost (by a complex calculation) is £43 per tonne, which coincides with an abatement potential of around 130 Mt - well over half the total. Even the most expensive measures plotted come in at under £250 per tonne.

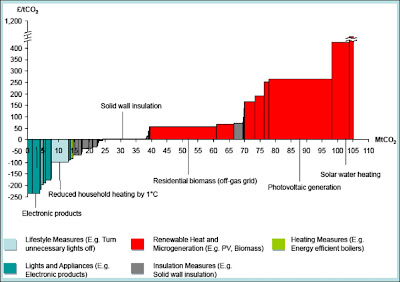

This, then, is a baseline of sorts, and certainly gives some background perspective for considering the next chart, which is the detailed MACC for abatement potential in the UK residential sector through to 2020.

|

| Source: Committee on Climate Change |

Note that solar power (PV generation) is well to the right of the curve, with a cost that towers over most of the measures available. (Solar water-heating is even worse.) Secondly, at £265 per tonne it is more expensive than any of the measures from the previous MACC.

A very obvious conclusion must surely be that solar power should not be receiving public money (via whatever mechanism) until the vastly greater potential that is available at very much less cost has been comprehensively exploited. Needless to say, the opposite is the case: residential solar power installations are heavily subsidized via our electricity bills, while huge amounts of cheaper - much cheaper - abatement potential lies dormant.

No end of sophistry is offered to defend this state of affairs.

Costs of PV are falling all the time; many jobs have been created (mostly in China, of course);

we need to create a level playing-field for all technologies (whatever that means). And there are all manner of nuances relating to the interpretation of MACCs - as DECC is keen to tell us (Box B5

here).

No amount of ratiocination, however, can deflect the accusation that subsidizing solar PV in the UK is indefensible from a cost perspective. And in straightened times, costs matter.

* * * * *

Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.