A pattern is emerging.

Jörg Guido Hülsmann, on the Mises site, says deflation does not ruin the economy as a whole, but destroys the parasites who exploit the potential of fiat money. Parasites like (alleged) Ponzi-style fraudster Madoff and his clients, who deserve what they've now got, Mish judges.

Jesse says that "financial capitalism" seeks to use the money system to develop a dictatorial New World Order, and will be defeated when the dollar fails as the world's reserve currency.

Brad Setser wonders whether the dollar has reached its zenith; which implies that it may begin heading for its nadir.

Desperately holding back the inevitable is the US Federal Reserve, says Jim from San Marcos, who (although the Fed is refusing FOI requests) suspects that its $2 trillion in emergency loans is equally divided between support for banks, credit cards and the stockmarket. (I wondered what was being used as the robust cloth on the Dow's trampoline, and covert official support may be the answer.)

As I argued yesterday, the straightest path would be to destroy fraudulent, oppressive debt and those who introduced it into the system. For so many families, the bank is the fattest kid at their kitchen table, and nobody knows who invited him.

For a long time, I've been recasting financial issues as issues of power and freedom. If Jesse is correct, we are reaching a turning point in the battle. I hope we may soon say, as Churchill said of El Alamein, "A bright gleam has caught the helmets of our soldiers and warmed and cheered all our hearts." It would be worth the blood, toil, tears and sweat.

Saturday, December 13, 2008

Friday, December 12, 2008

History repeats itself - because it's getting old

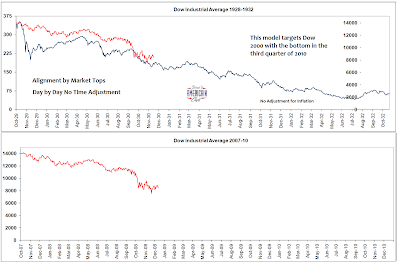

Jesse extrapolates the Dow and sees it heading for 2,000 points:

As my select and distinguished readers now know, I'm an optimist (by the standards of unfolding reality), and I say, not so. I say, maybe 4,000 - 5,000, adjusted for CPI.

The comparison I'd urge is not with 1929-32 (stockmarket deflation exacerbated by monetary strictness), but (in inflation-adjusted terms) from January 1966 to July 1982: stockmarket deflation prolonged and partially disguised by monetary inflation; I said so here and here, last month. I maintain that the bear market began in 2000 and the symptoms were masked by the terrible extra debts taken on over the last 8 years. Karl Denninger showed us yesterday that these debts account for all the US GDP growth since the New Millennium, plus $9 trillion.

The debate about inflation and deflation continues, though from a British perspective we've seen practically the whole of the rest of the world become one-third more expensive in sterling terms, in only five months. However, Einstein's theory of relativity rejects the notion of any absolute standpoint, and we shall see next year which other currencies mimic sterling's vertiginous fall.

In these shifting times, it becomes very hard to discern real value; but however hard to measure, it exists nevertheless. There is a real bill to pay for our excesses, and I think 2008 will be seen in retrospect as the year that the global balance of power underwent a sudden tectonic shift, from West to East. Yes, the East will suffer for a while, too, but it has long been acquiring the means of production and developing its local markets, and will emerge from the crisis ahead of us.

And there will also - must also - be an intergenerational shift of power, within our Western societies. As globalization continues and real income and real house prices decline, existing debt (set in fixed terms) will become proportionately greater, until the weight is too great to bear; and the worst of it falls on the people who are also struggling to raise families and save something, however inadequate, for their old age. They cannot be crucified in this way. How can savers be taxed at 20% and workers at (effectively, on margin, including National Insurance) 40%? Real wealth must flow from one to the other, just to maintain civilization. I think either savings must be taxed more (perhaps the removal of tax exemption for some savings products will be the start), or inflation must come, though I don't know how long the play will go on before the denouement.

We did have another option, and I was only half-joking: cancel mortgage debts on a massive scale (bankrupting the banks and the bankers, and serve them right). Then, with our productive populace relatively unencumbered, it would be possible to let Western wages and prices fall to much nearer Eastern levels, and we could begin to compete.

As my select and distinguished readers now know, I'm an optimist (by the standards of unfolding reality), and I say, not so. I say, maybe 4,000 - 5,000, adjusted for CPI.

The comparison I'd urge is not with 1929-32 (stockmarket deflation exacerbated by monetary strictness), but (in inflation-adjusted terms) from January 1966 to July 1982: stockmarket deflation prolonged and partially disguised by monetary inflation; I said so here and here, last month. I maintain that the bear market began in 2000 and the symptoms were masked by the terrible extra debts taken on over the last 8 years. Karl Denninger showed us yesterday that these debts account for all the US GDP growth since the New Millennium, plus $9 trillion.

The debate about inflation and deflation continues, though from a British perspective we've seen practically the whole of the rest of the world become one-third more expensive in sterling terms, in only five months. However, Einstein's theory of relativity rejects the notion of any absolute standpoint, and we shall see next year which other currencies mimic sterling's vertiginous fall.

In these shifting times, it becomes very hard to discern real value; but however hard to measure, it exists nevertheless. There is a real bill to pay for our excesses, and I think 2008 will be seen in retrospect as the year that the global balance of power underwent a sudden tectonic shift, from West to East. Yes, the East will suffer for a while, too, but it has long been acquiring the means of production and developing its local markets, and will emerge from the crisis ahead of us.

And there will also - must also - be an intergenerational shift of power, within our Western societies. As globalization continues and real income and real house prices decline, existing debt (set in fixed terms) will become proportionately greater, until the weight is too great to bear; and the worst of it falls on the people who are also struggling to raise families and save something, however inadequate, for their old age. They cannot be crucified in this way. How can savers be taxed at 20% and workers at (effectively, on margin, including National Insurance) 40%? Real wealth must flow from one to the other, just to maintain civilization. I think either savings must be taxed more (perhaps the removal of tax exemption for some savings products will be the start), or inflation must come, though I don't know how long the play will go on before the denouement.

We did have another option, and I was only half-joking: cancel mortgage debts on a massive scale (bankrupting the banks and the bankers, and serve them right). Then, with our productive populace relatively unencumbered, it would be possible to let Western wages and prices fall to much nearer Eastern levels, and we could begin to compete.

I prefer Alexander's handling of the Gordian knot, to Gordon Brown's. For me, debt forgiveness is the way; but that's too radical, it seems. Instead, inflation will have to diminish the real value of debt, but jerkily, as the debt-holders periodically jack up interest rates in a fighting retreat. All to hide from reality. "Oh, what a tangled web we weave..."

The US economy in a nutshell

"Wages are sticky downward": American car workers are still trying to fight gravity, i.e. globalization's effect on wage rates. Denninger think that if it's anything more than a bargaining ploy, it will finish most of the US car industry.

And after them? Who else could have their work outsourced? White-collar workers should not look on unconcerned. Save money while you can, while wages are still ahead of minimum spending requirements.

Meanwhile, up in the clouds, a hedge fund manager has (allegedly) admitted his business was a fraud, losing $50 billion; more than three times the car-makers' bailout fund currently under discussion.

And after them? Who else could have their work outsourced? White-collar workers should not look on unconcerned. Save money while you can, while wages are still ahead of minimum spending requirements.

Meanwhile, up in the clouds, a hedge fund manager has (allegedly) admitted his business was a fraud, losing $50 billion; more than three times the car-makers' bailout fund currently under discussion.

How we got here? [by Paddington]

In my opinion, the boom and bust cycles of the past 30 years or so reflect the deep denial of the real world from our leaders in business, government and education.

Much of that is due to the dearth of quantitative and scientific influence on decision-making. President Bush even down-graded the science advisor from the Cabinet.

For decades, students in the US and UK have avoided mathematics, science and engineering. Becoming a teacher meant getting an education degree, rather than knowledge of any particular discipline, as if the skills of teaching were at some mystical higher level than mere content. In business schools, students shunned accounting and finance, and flocked to management and marketing, as the former required too much mathematics and computer knowledge.

This meant a whole generation of managers unable to make decisions based on facts.

Managers in business are brothers under the skin with bureaucrats in government, and the administrators in education, all of whom make wild assertions and demands of subordinates that are completely at odds with reality.

Much of that is due to the dearth of quantitative and scientific influence on decision-making. President Bush even down-graded the science advisor from the Cabinet.

For decades, students in the US and UK have avoided mathematics, science and engineering. Becoming a teacher meant getting an education degree, rather than knowledge of any particular discipline, as if the skills of teaching were at some mystical higher level than mere content. In business schools, students shunned accounting and finance, and flocked to management and marketing, as the former required too much mathematics and computer knowledge.

This meant a whole generation of managers unable to make decisions based on facts.

Managers in business are brothers under the skin with bureaucrats in government, and the administrators in education, all of whom make wild assertions and demands of subordinates that are completely at odds with reality.

Thursday, December 11, 2008

Toll me back from thee to my sole Self

Just caught a minute of BBC1's Question Time, chaired by the garrulous and self-regarding David Dimbleby. Self-regarding literally, this time, as he watched Will Self lay into the career-crazy fascists of New Labour, who now propose to persecute the unemployed after a decade of encouraging them to remain on benefit. As he says, they had the time, the money and the ideology to sort it out, and they didn't do it; and in some damningly characteristic way, they're slapping people who are down already. Lethal. I may have to start liking the white-nosed sleazebag, after all.

His target is the type who may not have realized that they were driving David Kelly to suicide, but probably don't much care that they did, so long as the trail was brushed. My only concern is that the public generally may be starting to feel as I do, in which case we are entering dangerous territory.

His target is the type who may not have realized that they were driving David Kelly to suicide, but probably don't much care that they did, so long as the trail was brushed. My only concern is that the public generally may be starting to feel as I do, in which case we are entering dangerous territory.

Bookends: deflation and inflation

On one side, the redoubtable Mish scorns those who think inflation is a clear and present danger:

On one side, the redoubtable Mish scorns those who think inflation is a clear and present danger:...Those who think inflation is about prices alone were busy shorting treasuries, and looking the wrong direction for over a year. Only after the stock market fell 50% and gasoline prices crashed did the media start picking up on "deflation". Only those who knew what a destruction in credit would do to jobs, to lending, to retail sales, to the stock market, to corporate bond yields and to treasury yields got it right...

Those who stick to a monetary definition of inflation pointing at M3, MZM, base money supply, or even Money AMS, are selecting a definition that makes absolutely no practical sense. Worse yet they do it screaming about bond-bubbles at yields of 5% or higher, all because they refuse to see or admit the destruction of credit is happening far faster than the Fed is printing...

The trick now is to figure out how long deflation will last, not whether we are in it. Humpty Dumpty is of no use, he cannot even see where we are.

On the other end, Jesse recalls Moscow in 1997, before the currency popped:

...They were desperate times, and you could see that there was a climactic crisis coming. It is easy to talk about this sort of thing, a thousand to one devaluation of your home currency, but harder to understand the impact. Imagine that you have $500,000 in savings for your retirement. Now imagine that within two years it is effectively reduced to $5,000 or less, and you will understand how disconcerting a currency crisis can be.

If you don't think a financial panic is possible here in the US, just take a look at the negative returns on short term T bills, and you will get a taste of the leading edge.

One of the best descriptions of the Weimar experience I have ever read was by Adam Fergusson titled "When Money Dies: The Nightmare of the Weimar Collapse." It is notoriously difficult to obtain, but it does the best job in describing how a currency collapse can come on like a lightning strike, although in retrospect everyone could have seen it coming. Denial is a strong narcotic. People believe in their institutions and ignore history until they are staring on the edge of the abyss.

I was right, but I didn't know why

Karl Denninger crunches the numbers: in the last 8 years, US GDP has increased by $14 trillion, but debts by $23 trillion, so effectively accounting for all the GDP growth in that time and still leaving a deficit of $9 trillion...

... we haven't had an expansion in GDP over the last eight years. Congress and its organs of reporting economic "facts" have lied. We have in fact actually seen about a 10% contraction in real GDP from 2000 levels; all of the so-called "expansion" of the Bush Administration has been a lie intended to prevent recognition and working through of the recession that should have happened in 2000.

Now, I sensed this during the last 8 years and felt it coming before then, and have recently said so several times. I'm only grateful that technical whizzes like Karl have managed to spell it out. If only we had taken our lumps after the technology bust of 2000.

... we haven't had an expansion in GDP over the last eight years. Congress and its organs of reporting economic "facts" have lied. We have in fact actually seen about a 10% contraction in real GDP from 2000 levels; all of the so-called "expansion" of the Bush Administration has been a lie intended to prevent recognition and working through of the recession that should have happened in 2000.

Now, I sensed this during the last 8 years and felt it coming before then, and have recently said so several times. I'm only grateful that technical whizzes like Karl have managed to spell it out. If only we had taken our lumps after the technology bust of 2000.

Subscribe to:

Posts (Atom)