Doug Noland sees the debt crisis spreading to the corporate sector; David Jensen writes a letter to the Governor of the Bank of Canada, including very telling graphs of mounting debt and the bubble in the financial markets; Michael Panzner discusses a piece from the Financial Times on the threat of a downgrade of America's historic AAA credit rating, and refers to the weakening of the USA's military pre-eminence; Sol Palha worries about the acquisition of Western assets by sovereign wealth funds ("Slowly but surely America and Europe are going to be owned by foreigners. The irony is that Congress is trying to keep immigrants out of this country but right in front of their eyes foreigners are slowly gobbling up huge chunks of this country.").

All this leads me to Jeffrey Nyquist's grim, but compelling latest piece. He despairs of the irrelevance of mainstream political discussion, especially as the polling process rattles on, and paints a far greater picture. I think you should read it all, but here are a few extracts:

What is happening in the news today, what is happening in the markets and in the banking system, has profound strategic implications... There are no invulnerable countries... If a government does not see ahead, make defensive preparations, establish a dialogue with citizens, lead the way to awareness and responsibility, then the nation stumbles into the next world war unarmed and psychologically unprepared.

Even worse, today's politics has become a politics of "divide and conquer" in which one constituency is played off against another: poor against rich, non-white against white, the secular against the religious. Before a positive outcome is possible, we must have unity and we must have reality.

It's more comfortable to ignore the crying of Cassandra, but maybe Nyquist is like Churchill in the pre-WWII political wilderness, trying to prepare us for the next conflict. We in Britain only just made it, and how we have paid for that struggle ever since.

But it was a price worth paying. History would have been very different, and very horrible I am sure, if Churchill had listened to some in his Cabinet in 1940 who advised him to make a deal with the Nazis. He said, “If this long island story of ours is to end at last, let it end only when each one of us lies choking in his own blood upon the ground.” It's a line that even now has tears pricking my eyes. The appeasers were silenced by the sound of deeply-moved men banging their fists on the Cabinet table in agreement and applause.

My worry is that I don't see men of that calibre now. As Lord Acton said in a letter to a bishop, "Power corrupts, and absolute power corrupts absolutely". Commenting on the House of Commons after the Great War, Stanley Baldwin remarked on the presence of "A lot of hard-faced men who look as if they had done very well out of the war". Today, the faces are softer, the hair expensively dressed, the manner relaxed and affable, but behind it all one senses cold-hearted, selfish betrayal. To be charitable, it may be that our leaders and ex-leaders don't fully realize the negative consequences of all their deals, compromises and consultancies.

As our reckless debt is progessively converted into ownership, we may find out how much we took our freedom for granted. It's a lot harder to get back.

The Bible has something to say on this, too (and no, I'm not a preacher, this is to show that the issues endure throughout history): Leviticus, Chapter 25 deals with debt, buying and redeeming slaves, and how the chosen people should be treated differently from the heathens - for the latter, enslavement is perpetual.

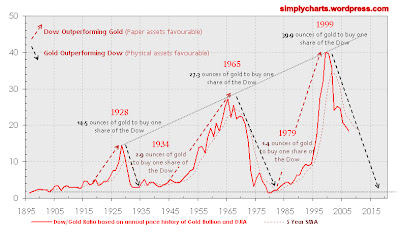

It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.

It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.