After his prescient book "Financial Armageddon", in which Michael Panzner identified four major threats to our economic security, he wrote another called "When Giants Fall", which I have been planning to review for a year now.

The latter is more complex and harder to summarise, but as I see it, essentially it views America's loss of power and prestige as leading to a sort of Balkanization of the world, just as after the death of Tito, Yugoslavia and other Eastern European countries fractured and fought. I once visited a pet shop where there was a large rabbit sitting among the guinea pigs; when I asked why, they told me that guinea pigs will fight to the death for dominance, but one look at the rabbit told them they had no chance and so they decided to get along peaceably.

This global fracture is now under way, with major nations like China and Russia playing a 21st century version of The Great Game, and we see it in little ways as well as the more obvious ones. Mark Steyn, a sharply witty Canadian journalist, comments on the curious case of a South Pacific islet (Nauru) taking it on itself to recognise the nationhood of Abkhazia, currently a province of the Caucasian republic of Georgia (Stalin's birthplace). Naturally, it's for a consideration, in this case money from President Putin, who wants to reabsorb Georgia.

Should we take it seriously? Aren't both these little nations a bit like the Duchy of Grand Fenwick in the film comedy "The Mouse That Roared"?

A single match can start a forest fire. When some Serbs decided to break off from Croatia in the 1990s, they may have started as a rather small, contemptibly scruffy and ill-equipped band, but other players and suppliers got involved and things fell apart very nastily. When there are powerful interests at stake, nothing is insignificant: Russia quibbles about the definition of its continental shelf to lay claim (in 2001) to fossil fuels near the North Pole; China goes back to the 13th century to justify its claim to Tibet, and by extension the (currently) Indian province of Arunachal Pradesh - both containing valuable natural resources that the Chinese need. Relatively small amounts of money and support can recruit votes that matter in international politics and law.

Panzner's book examines all sorts of potential consequences of the weakening of the "world's policeman", and no-one knows how matters will progress. The situation is so complex that chaos theory could be relevant - the flutter of the butterfly's wings triggering a hurricane thousands of miles away.

So what can we do about it? I think all we can do, is to become generally more cautious and store resources to cope with emergencies. Like Boy Scouts, we must "be prepared"; as our grandparents would say, "don't put all your eggs in one basket".

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sunday, January 17, 2010

Saturday, January 16, 2010

Mrs Thatcher and inflation: a letter to the Spectator

Sir;

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Wednesday, January 13, 2010

Debt, the financial sector and economic growth

Someone who occasionally reads and comments on my older blog has a formulation of real growth: increase in GDP less increase in debt. I've finally taken the bait and invested time to look at this, for the UK, and it's intriguing.

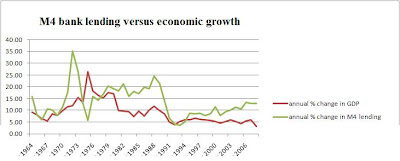

First, I've taken figures for M4 bank lending, from the Bank of England's website. This gives the quarterly increase as a percentage, re-expressed as an annual equivalent figure. I've used Excel to average the four quarters for each calendar year. Since the information is only available from partway through 1963, I use the estimated annual percentage increase from 1964 onwards.

For GDP, I use the Measuring Worth site and the "UK nominal GDP" figures (i.e. x million pounds, not adjusted for inflation), and again give the percentage increase year-on-year (the last available year here is 2008).

Here's the resulting graph for increases in M4 and GDP (click on graph to enlarge):

What is obvious is that apart from a short time in the early 1990s, lending has risen far more than GDP for the last 30 years. That extra money went somewhere, and it seems that all it did was inflate asset prices, in the stockmarket and in housing, at the same time that global trade has kept down wages and consumer prices.

What is obvious is that apart from a short time in the early 1990s, lending has risen far more than GDP for the last 30 years. That extra money went somewhere, and it seems that all it did was inflate asset prices, in the stockmarket and in housing, at the same time that global trade has kept down wages and consumer prices.

Between 1964 and 1981, GDP increased by an average 12.69% and M4 by 15.16% - a difference of 2.48% per year. But from 1982 to 2008, GDP increased annually on average by 6.63% and M4 by 12.32% - a difference of 5.69% p.a. Compounded up over the past quarter century, that extra difference may explain how financiers have become so large and powerful. In the USA, according to Robert Creamer , the financial sector accounted for 8% of national GDP over the last 10 years, but made 41% of the profits.

I can't say when it will end, but equally I can't see this going on forever. This is why I am inclined to listen to the Jeremiahs who warn us of further economic setbacks, despite strong recent rises in the stockmarkets.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

First, I've taken figures for M4 bank lending, from the Bank of England's website. This gives the quarterly increase as a percentage, re-expressed as an annual equivalent figure. I've used Excel to average the four quarters for each calendar year. Since the information is only available from partway through 1963, I use the estimated annual percentage increase from 1964 onwards.

For GDP, I use the Measuring Worth site and the "UK nominal GDP" figures (i.e. x million pounds, not adjusted for inflation), and again give the percentage increase year-on-year (the last available year here is 2008).

Here's the resulting graph for increases in M4 and GDP (click on graph to enlarge):

What is obvious is that apart from a short time in the early 1990s, lending has risen far more than GDP for the last 30 years. That extra money went somewhere, and it seems that all it did was inflate asset prices, in the stockmarket and in housing, at the same time that global trade has kept down wages and consumer prices.

What is obvious is that apart from a short time in the early 1990s, lending has risen far more than GDP for the last 30 years. That extra money went somewhere, and it seems that all it did was inflate asset prices, in the stockmarket and in housing, at the same time that global trade has kept down wages and consumer prices.Between 1964 and 1981, GDP increased by an average 12.69% and M4 by 15.16% - a difference of 2.48% per year. But from 1982 to 2008, GDP increased annually on average by 6.63% and M4 by 12.32% - a difference of 5.69% p.a. Compounded up over the past quarter century, that extra difference may explain how financiers have become so large and powerful. In the USA, according to Robert Creamer , the financial sector accounted for 8% of national GDP over the last 10 years, but made 41% of the profits.

I can't say when it will end, but equally I can't see this going on forever. This is why I am inclined to listen to the Jeremiahs who warn us of further economic setbacks, despite strong recent rises in the stockmarkets.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Tuesday, January 12, 2010

Interactive long-term house price graphs

Via Australian economist Steve Keen, here is a tool from The Economist magazine to help you see how house prices have changed over time. This may help you guess whether current prices are too high, too low or Goldilocks!

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Preparing for the worst is not for loners

Charles Hugh Smith offers some sensible general principles for making it through what he sees as likely very difficult, disrupted times ahead. Key recommendations include broadening your skills, and developing social networks. I think he's right - Robinson Crusoe is not the model for how to survive in our populous countries.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

More warning signs

Update: see "Jesse" on speculation about recent curious purchases of US Treasury bonds.

__________________________________________

"Mish" looks at two countries experiencing trouble - Argentina and Venezuela - and point out that European banks are exposed to risk in that area.

"George Washington" thinks the recent rise in the stockmarket has been because of activity by "hedgies, pension funds, banks and other institutional investors", including possibly even clandestine intervention by the government itself (I've seen this allegation before). However, in the US 80% of stocks are owned by individuals, not these corporate entities, so the suspicion is that the rally has been engineered to encourage the private investor to return to the market.

It doesn't seem to be working - much of the money withdrawn from stocks has gone into bonds (I think the unfortunate private investor may lose again if - as I fear - interest rates rise and bond values plummet).

I also suspect that if the individual re-entered the market because of what appears to be leveraged (boosted with borrowed money) speculation by the institutions, the latter would then cash-in and leave the individual holding the baby. This pattern is known as a "sucker rally".

But if the private investor is not "suckered" back into the market, then institutions will race to get out again (suckering each other, faute de mieux) and we could see a sharp fall in stocks. This, I assume would confirm the private investor's worst suspicions and lead him/her to pull even more out of the market.

Some, including myself, have suggested that the real bottom (at some point, goodness knows when) in the stockmarket may be somewhere around 4,000 on the Dow and 2,000 on the FTSE (adjusted for inflation, if that takes off). It may never happen, but Google "Dow 4000" and see some quite respectable commentators bandying around that idea.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

__________________________________________

"Mish" looks at two countries experiencing trouble - Argentina and Venezuela - and point out that European banks are exposed to risk in that area.

"George Washington" thinks the recent rise in the stockmarket has been because of activity by "hedgies, pension funds, banks and other institutional investors", including possibly even clandestine intervention by the government itself (I've seen this allegation before). However, in the US 80% of stocks are owned by individuals, not these corporate entities, so the suspicion is that the rally has been engineered to encourage the private investor to return to the market.

It doesn't seem to be working - much of the money withdrawn from stocks has gone into bonds (I think the unfortunate private investor may lose again if - as I fear - interest rates rise and bond values plummet).

I also suspect that if the individual re-entered the market because of what appears to be leveraged (boosted with borrowed money) speculation by the institutions, the latter would then cash-in and leave the individual holding the baby. This pattern is known as a "sucker rally".

But if the private investor is not "suckered" back into the market, then institutions will race to get out again (suckering each other, faute de mieux) and we could see a sharp fall in stocks. This, I assume would confirm the private investor's worst suspicions and lead him/her to pull even more out of the market.

Some, including myself, have suggested that the real bottom (at some point, goodness knows when) in the stockmarket may be somewhere around 4,000 on the Dow and 2,000 on the FTSE (adjusted for inflation, if that takes off). It may never happen, but Google "Dow 4000" and see some quite respectable commentators bandying around that idea.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Measure your pessimism

Hat-tip to Credit Writedowns. I'm relieved to see that I'm still at the Teddy/Cub stage!

Hat-tip to Credit Writedowns. I'm relieved to see that I'm still at the Teddy/Cub stage! DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Subscribe to:

Posts (Atom)