Today, I started my 27th year of teaching at a State-supported US university. Compared with 1984, we have the same number of students, fewer full-time teaching faculty, and twice as many administrators. In the past 8 years alone, the non-academic budget has grown from 44% to 60% of the budget.

This week, we start discussions on increasing teaching loads (which will, of course, require more administrators to 'organize' things).

I see this trend in business, government, medicine and the military. Is it just the human condition that the non-productive take over everything?

I recall that, when the Mongols took over a city, they killed the bureaucrats, and took the scholars home with them. The Allies did much the same in Germany in 1945.

Perhaps they had the right idea?

Tuesday, January 12, 2010

Monday, January 11, 2010

Climate change and industrial activity

Could the current cold weather be partly related to a downturn in fossil-fuel-powered manufacturing and transportation? I only ask because I seem to recall reading/hearing that big freezes also happened in the 70s, and after both World wars.

Why a turnaround in the economy is not imminent

"Mish" collates a number of emails and comments to reinforce his thesis that we are set for a long and very difficult deflation, for a variety of reasons. One of his respondents is noted Australian economist Steve Keen, one of the dozen or so (out of perhaps 20,000 professional economists worldwide) who foresaw the credit crunch; Keen thinks it would have been better to give money to debtors directly, rather than to the banks, who will simply hoard the cash as so few now wish to borrow the way they used to.

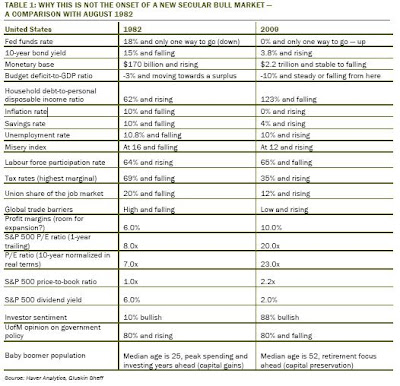

Vitaliy Katsenelson looks at history and finds: "Over the last 200 years, every long-lasting bull market (and we just had a supersized one from 1982 to 2000) was followed by a range-bound market that lasted about 15 years or so (the only exception was the Great Depression)." He expects the market to bounce up and down and "At the end of this wild ride, when the excitement subsides and the dust settles, index investors and buy-and-hold stock collectors will find themselves not far from where they started in 2000," so he recommends that we analyze individual companies and timing our purchases according to when we think their particular stocks are undervalued.

David Rosenberg tabulates lots of ways in which the present circumstances are not like those in 1982 (when the market began to turn upwards in real terms):

By the way, that last statistic about median ages startled me, so I looked elsewhere for information on general US demographics, rather than just the "baby boomers". This graph says that the median age of the US population as a whole rose from 26 years in 1929 to nearly 30 post WWII, then fell to below 28 in the late 1960s, after which there was a steady rise to over 34 years by 1994. This site estimates the median age in 2006/2008 at 36.7 years. Demographic change has had and is going to have an enormous impact on government budgets and the stockmarket.

Bill Gross (of PIMCO, which recently announced its plan to be a net seller of UK bonds) laments the corruption of government that makes him wary of trading in the US at present. He thinks that relative to more fiscally responsible governments like Germany, countries like the USA, UK and Japan will have higher interest rates and this will, of course, hit the value of their bonds and stocks.

Finally, Warren Pollock's politico-economic overview sees threats to two key stabilisers in the world economy - Saudi Arabia and China. Problems there could begin a wider unravelling of current arrangements.

So, as I have done for the last 10 years or more, I am urging caution and the making of emergency plans.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Vitaliy Katsenelson looks at history and finds: "Over the last 200 years, every long-lasting bull market (and we just had a supersized one from 1982 to 2000) was followed by a range-bound market that lasted about 15 years or so (the only exception was the Great Depression)." He expects the market to bounce up and down and "At the end of this wild ride, when the excitement subsides and the dust settles, index investors and buy-and-hold stock collectors will find themselves not far from where they started in 2000," so he recommends that we analyze individual companies and timing our purchases according to when we think their particular stocks are undervalued.

David Rosenberg tabulates lots of ways in which the present circumstances are not like those in 1982 (when the market began to turn upwards in real terms):

By the way, that last statistic about median ages startled me, so I looked elsewhere for information on general US demographics, rather than just the "baby boomers". This graph says that the median age of the US population as a whole rose from 26 years in 1929 to nearly 30 post WWII, then fell to below 28 in the late 1960s, after which there was a steady rise to over 34 years by 1994. This site estimates the median age in 2006/2008 at 36.7 years. Demographic change has had and is going to have an enormous impact on government budgets and the stockmarket.

Bill Gross (of PIMCO, which recently announced its plan to be a net seller of UK bonds) laments the corruption of government that makes him wary of trading in the US at present. He thinks that relative to more fiscally responsible governments like Germany, countries like the USA, UK and Japan will have higher interest rates and this will, of course, hit the value of their bonds and stocks.

Finally, Warren Pollock's politico-economic overview sees threats to two key stabilisers in the world economy - Saudi Arabia and China. Problems there could begin a wider unravelling of current arrangements.

So, as I have done for the last 10 years or more, I am urging caution and the making of emergency plans.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sunday, January 10, 2010

NEST - compulsory pension savings for employees

In the UK, many people face an impoverished retirement. Stakeholder Pensions were introduced in 2001 as a simple and cheap form of retirement saving, but even now, nearly 12 million people have no pension plan, or a very small one. There are reasons for this - including being too poor to invest enough to make a worthwhile difference to one's retirement income.

From 2012, this will change. A compulsory scheme will be introduced in workplaces, for people that haven't already joined a scheme. It's been called by different names and has just been rebranded "NEST" - the National Employment Savings Trust. (The logo (see left) reportedly cost £363,000 to dream up - the equivalent of over 100 years' worth of maximum contributions to a NEST plan.)

There was an earlier, and in my view better, scheme mooted by one-man think tank the Rt Hon Frank Field MP, who set up the Pensions Reform Group in 1999 to address the issue. They came up with the idea of a Universal Protected Pension, which has 5 principles:

1. Together with the Basic State Pension, an extra (funded) pension should eventually lift all pensioners permanently above the poverty line, by providing a total minimum income of 25-30% of average earnings. Those who are able and willing, can pay in more to get more.

2. It should be for everybody.

3. It should operate as a redistributive scheme: everybody pays a proportion of their earnings (so higher earners pay more), but everybody will get the same benefits.

4. The layer on top of the Basic State Pension should be funded - i.e. it would become an enormous investment fund. Without this, the whole scheme would be another expensive unfunded Government undertaking and at risk of being cut or abolished when the national budget gets tight.

5. It should be kept independent of the Government, to keep the politicians' hands off it.

Like other ideas by Mr Field, this one has been well thought-out. And like some of his other ideas, it's been ignored, or badly adapted. Perhaps, in this case, it's because politicians understand the temptation of (4) too well to think that (5) would work.

Let's look at (1 - 3) as well. Without compulsion, many workers not only would not join, but might be foolish to join. This is because of the way the benefit system works. If you reach retirement with an income of less than a certain weekly amount, the State will top it up. So if you know that is going to happen, it's not worth saving up out of your earned income - you'll just get less by way of a free top-up, so it's as though your personal provision was being taxed at 100%.

To answer this objection, the State first discounts each pound of income you provided for yourself, then re-awards you a "Savings Credit" of 60p. But this is still, effectively, a "tax rate" of 40% - Higher Rate Tax for the poor. This explains Steve Bee's comment on NEST:

Now all we need is for the government guys to fix things so that the pension savings of low to moderate earners can’t be devalued by the unfortunate way pension savings currently interact with the means-tested entitlements that are provided for the elderly and we’ll be cooking on gas.

Not surprisingly, financial advisers find themselves in a quandary when advising lower-paid people about funding for retirement!

Under Frank Field's group's proposals, there would be no decision to make, since contributions would be compulsory. But also, however little you contributed, you would still attain the overall target income of 25-30% of average earnings and be above the notional poverty line, so the complicated and self-defeating system of Pension Credit and Savings Credit would be redundant.

Instead, the NEST is universal only for those who aren't already in a scheme, and you only get the results of what you and your employer have put in - no redistribution effect. Presumably the employer will take into account what he/she has to contribute to the pension, when calculating what pay rises to give you, so it's not even "free money" from the employer. In effect, we have a variant on the current unsatisfactory system, plus compulsion.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, January 09, 2010

Simon Johnson on the coming disaster

Simon Johnson comments on renewed speculative activity by the banks. He fears that the next bubble-and-pop may be in emerging markets, especially China.

For those who wish to understand more, Simon's website, The Baseline Scenario, offers a beginner's guide to the global financial crisis (GFC).

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

For those who wish to understand more, Simon's website, The Baseline Scenario, offers a beginner's guide to the global financial crisis (GFC).

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Which books should we burn?

Welsh pensioners are buying books as fuel. Discounting differences in book size, and assuming you could gather all copies of the same title, which books would you burn?

On his deathbed, the poet Virgil requested his friends to burn his "Aeneid". Does an author have the right to do this?

On his deathbed, the poet Virgil requested his friends to burn his "Aeneid". Does an author have the right to do this?

GDP: friend or foe?

I attended the British Association for the Advancement of Science Conference in Birmingham in 1977, and even then economists were asking whether GDP was a useful measure. The example I remember was eating more sweets and consequently visiting the dentist more often.

Should we be quite so concerned about goosing GDP with quantitative easing etc, or is it just a trap to make us continue misallocating resources?

Should we be quite so concerned about goosing GDP with quantitative easing etc, or is it just a trap to make us continue misallocating resources?

Subscribe to:

Posts (Atom)