Monday, January 11, 2010

Climate change and industrial activity

Could the current cold weather be partly related to a downturn in fossil-fuel-powered manufacturing and transportation? I only ask because I seem to recall reading/hearing that big freezes also happened in the 70s, and after both World wars.

Why a turnaround in the economy is not imminent

"Mish" collates a number of emails and comments to reinforce his thesis that we are set for a long and very difficult deflation, for a variety of reasons. One of his respondents is noted Australian economist Steve Keen, one of the dozen or so (out of perhaps 20,000 professional economists worldwide) who foresaw the credit crunch; Keen thinks it would have been better to give money to debtors directly, rather than to the banks, who will simply hoard the cash as so few now wish to borrow the way they used to.

Vitaliy Katsenelson looks at history and finds: "Over the last 200 years, every long-lasting bull market (and we just had a supersized one from 1982 to 2000) was followed by a range-bound market that lasted about 15 years or so (the only exception was the Great Depression)." He expects the market to bounce up and down and "At the end of this wild ride, when the excitement subsides and the dust settles, index investors and buy-and-hold stock collectors will find themselves not far from where they started in 2000," so he recommends that we analyze individual companies and timing our purchases according to when we think their particular stocks are undervalued.

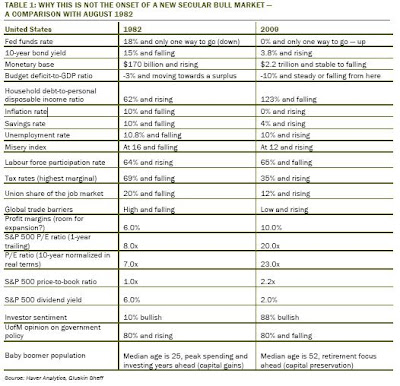

David Rosenberg tabulates lots of ways in which the present circumstances are not like those in 1982 (when the market began to turn upwards in real terms):

By the way, that last statistic about median ages startled me, so I looked elsewhere for information on general US demographics, rather than just the "baby boomers". This graph says that the median age of the US population as a whole rose from 26 years in 1929 to nearly 30 post WWII, then fell to below 28 in the late 1960s, after which there was a steady rise to over 34 years by 1994. This site estimates the median age in 2006/2008 at 36.7 years. Demographic change has had and is going to have an enormous impact on government budgets and the stockmarket.

Bill Gross (of PIMCO, which recently announced its plan to be a net seller of UK bonds) laments the corruption of government that makes him wary of trading in the US at present. He thinks that relative to more fiscally responsible governments like Germany, countries like the USA, UK and Japan will have higher interest rates and this will, of course, hit the value of their bonds and stocks.

Finally, Warren Pollock's politico-economic overview sees threats to two key stabilisers in the world economy - Saudi Arabia and China. Problems there could begin a wider unravelling of current arrangements.

So, as I have done for the last 10 years or more, I am urging caution and the making of emergency plans.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Vitaliy Katsenelson looks at history and finds: "Over the last 200 years, every long-lasting bull market (and we just had a supersized one from 1982 to 2000) was followed by a range-bound market that lasted about 15 years or so (the only exception was the Great Depression)." He expects the market to bounce up and down and "At the end of this wild ride, when the excitement subsides and the dust settles, index investors and buy-and-hold stock collectors will find themselves not far from where they started in 2000," so he recommends that we analyze individual companies and timing our purchases according to when we think their particular stocks are undervalued.

David Rosenberg tabulates lots of ways in which the present circumstances are not like those in 1982 (when the market began to turn upwards in real terms):

By the way, that last statistic about median ages startled me, so I looked elsewhere for information on general US demographics, rather than just the "baby boomers". This graph says that the median age of the US population as a whole rose from 26 years in 1929 to nearly 30 post WWII, then fell to below 28 in the late 1960s, after which there was a steady rise to over 34 years by 1994. This site estimates the median age in 2006/2008 at 36.7 years. Demographic change has had and is going to have an enormous impact on government budgets and the stockmarket.

Bill Gross (of PIMCO, which recently announced its plan to be a net seller of UK bonds) laments the corruption of government that makes him wary of trading in the US at present. He thinks that relative to more fiscally responsible governments like Germany, countries like the USA, UK and Japan will have higher interest rates and this will, of course, hit the value of their bonds and stocks.

Finally, Warren Pollock's politico-economic overview sees threats to two key stabilisers in the world economy - Saudi Arabia and China. Problems there could begin a wider unravelling of current arrangements.

So, as I have done for the last 10 years or more, I am urging caution and the making of emergency plans.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Sunday, January 10, 2010

NEST - compulsory pension savings for employees

In the UK, many people face an impoverished retirement. Stakeholder Pensions were introduced in 2001 as a simple and cheap form of retirement saving, but even now, nearly 12 million people have no pension plan, or a very small one. There are reasons for this - including being too poor to invest enough to make a worthwhile difference to one's retirement income.

From 2012, this will change. A compulsory scheme will be introduced in workplaces, for people that haven't already joined a scheme. It's been called by different names and has just been rebranded "NEST" - the National Employment Savings Trust. (The logo (see left) reportedly cost £363,000 to dream up - the equivalent of over 100 years' worth of maximum contributions to a NEST plan.)

There was an earlier, and in my view better, scheme mooted by one-man think tank the Rt Hon Frank Field MP, who set up the Pensions Reform Group in 1999 to address the issue. They came up with the idea of a Universal Protected Pension, which has 5 principles:

1. Together with the Basic State Pension, an extra (funded) pension should eventually lift all pensioners permanently above the poverty line, by providing a total minimum income of 25-30% of average earnings. Those who are able and willing, can pay in more to get more.

2. It should be for everybody.

3. It should operate as a redistributive scheme: everybody pays a proportion of their earnings (so higher earners pay more), but everybody will get the same benefits.

4. The layer on top of the Basic State Pension should be funded - i.e. it would become an enormous investment fund. Without this, the whole scheme would be another expensive unfunded Government undertaking and at risk of being cut or abolished when the national budget gets tight.

5. It should be kept independent of the Government, to keep the politicians' hands off it.

Like other ideas by Mr Field, this one has been well thought-out. And like some of his other ideas, it's been ignored, or badly adapted. Perhaps, in this case, it's because politicians understand the temptation of (4) too well to think that (5) would work.

Let's look at (1 - 3) as well. Without compulsion, many workers not only would not join, but might be foolish to join. This is because of the way the benefit system works. If you reach retirement with an income of less than a certain weekly amount, the State will top it up. So if you know that is going to happen, it's not worth saving up out of your earned income - you'll just get less by way of a free top-up, so it's as though your personal provision was being taxed at 100%.

To answer this objection, the State first discounts each pound of income you provided for yourself, then re-awards you a "Savings Credit" of 60p. But this is still, effectively, a "tax rate" of 40% - Higher Rate Tax for the poor. This explains Steve Bee's comment on NEST:

Now all we need is for the government guys to fix things so that the pension savings of low to moderate earners can’t be devalued by the unfortunate way pension savings currently interact with the means-tested entitlements that are provided for the elderly and we’ll be cooking on gas.

Not surprisingly, financial advisers find themselves in a quandary when advising lower-paid people about funding for retirement!

Under Frank Field's group's proposals, there would be no decision to make, since contributions would be compulsory. But also, however little you contributed, you would still attain the overall target income of 25-30% of average earnings and be above the notional poverty line, so the complicated and self-defeating system of Pension Credit and Savings Credit would be redundant.

Instead, the NEST is universal only for those who aren't already in a scheme, and you only get the results of what you and your employer have put in - no redistribution effect. Presumably the employer will take into account what he/she has to contribute to the pension, when calculating what pay rises to give you, so it's not even "free money" from the employer. In effect, we have a variant on the current unsatisfactory system, plus compulsion.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Saturday, January 09, 2010

Simon Johnson on the coming disaster

Simon Johnson comments on renewed speculative activity by the banks. He fears that the next bubble-and-pop may be in emerging markets, especially China.

For those who wish to understand more, Simon's website, The Baseline Scenario, offers a beginner's guide to the global financial crisis (GFC).

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

For those who wish to understand more, Simon's website, The Baseline Scenario, offers a beginner's guide to the global financial crisis (GFC).

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Which books should we burn?

Welsh pensioners are buying books as fuel. Discounting differences in book size, and assuming you could gather all copies of the same title, which books would you burn?

On his deathbed, the poet Virgil requested his friends to burn his "Aeneid". Does an author have the right to do this?

On his deathbed, the poet Virgil requested his friends to burn his "Aeneid". Does an author have the right to do this?

GDP: friend or foe?

I attended the British Association for the Advancement of Science Conference in Birmingham in 1977, and even then economists were asking whether GDP was a useful measure. The example I remember was eating more sweets and consequently visiting the dentist more often.

Should we be quite so concerned about goosing GDP with quantitative easing etc, or is it just a trap to make us continue misallocating resources?

Should we be quite so concerned about goosing GDP with quantitative easing etc, or is it just a trap to make us continue misallocating resources?

Marmite Easter Egg

According to a team of astronomers, the Milky Way is surrounded by a shell of invisible "dark matter" (Htp: Yves Smith).

But the supermassive black hole at the centre of our galaxy is gpoing to take longer to shloop us up than we thought previously.

We have a bit more time to eat that strawberry.

But the supermassive black hole at the centre of our galaxy is gpoing to take longer to shloop us up than we thought previously.

We have a bit more time to eat that strawberry.

Wednesday, January 06, 2010

Propaganda time

There's a passage in Evelyn Waugh's comic novel Scoop where gentleman nature columnist William Boot, sent on foreign assignment owing to an administrative mix-up, receives instructions from his newspaper's owner:

LORD COPPER PERSONALLY REQUIRES VICTORIES STOP ON RECEIPT OF THIS CABLE VICTORY STOP CONTINUE CABLING VICTORIES UNTIL FURTHER NOTICE STOP

I was reminded of this today when I heard (via Classic FM) the cheery news that Marks & Spencer has enjoyed an increase in like-for-like sales over the last three-month period. As far as I know, "like-for-like" just means sales turnover in monetary terms, and it's perfectly possible to achieve this if you offer deep discounts, which is what they were doing before Christmas ("3 for 2" on clothes and Christmas gifts, for example). It keeps the show on the road, but it's bound to affect profits - though you may be able to disguise that impact if you mix it up with savings from property sales (27 stores) and redundancies (1,200).

Not that we got that contextualisation on the radio, of course. We are becoming skeptical news consumers, like Russians in the days when they said "v Pravde net izvestiy, v Izvestiyakh net pravdy" (In the Truth there is no news, and in the News there is no truth). It's a shame that we can't rely on mainstream news media, because when forced to the blogosphere to find out what's going on, we discover that not everyone who approaches you in a tatty coat tied together with rope is an Old Testament prophet.

But there's also plenty of stuff from more respectable sources, too. Michael Panzner ( who provides a great scan-and-select service for the economics newsfollower) directs us to this column by Morgan Stanley expert Stephen Roach. Brief highlights:

1. Only about half of an estimated $3.4 trillion in asset losses have been officially written off so far, according to the IMF.

2. The slowdown is worldwide, so other nations are unlikely to take up the slack.

3. The American consumer is not able or willing to resume spending as before.

4. 45% of China's economic activity is in "fixed investment" (building roads, factories etc) and there is a risk that they may be creating a lot of "white elephants".

Money is still changing hands here, but Roach says this is "fueled by a temporary boost from the inventory cycle", i.e. vendors are flogging-off surplus stock at bargain prices - which is why I've cited the feelgood M&S article above. After that, I think, comes cool reality - maybe continued lower prices, but also lower wages, lower profits, higher unemployment and an increase in bankruptcies.

Roach estimates a 40% chance of a "double dip" global recession this year. He also fears that economic stimulus will not be withdrawn quickly enough when a recovery comes, so possibly yet another bubble will be created. Another risk, in his view, is that the US will seek to protect domestic industry against Chinese imports; this could threaten the financial arrangements between the two countries, weaken the dollar and raise inflation.

Is it really not possible for radio and TV news to give a rounder picture of reality?

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

LORD COPPER PERSONALLY REQUIRES VICTORIES STOP ON RECEIPT OF THIS CABLE VICTORY STOP CONTINUE CABLING VICTORIES UNTIL FURTHER NOTICE STOP

I was reminded of this today when I heard (via Classic FM) the cheery news that Marks & Spencer has enjoyed an increase in like-for-like sales over the last three-month period. As far as I know, "like-for-like" just means sales turnover in monetary terms, and it's perfectly possible to achieve this if you offer deep discounts, which is what they were doing before Christmas ("3 for 2" on clothes and Christmas gifts, for example). It keeps the show on the road, but it's bound to affect profits - though you may be able to disguise that impact if you mix it up with savings from property sales (27 stores) and redundancies (1,200).

Not that we got that contextualisation on the radio, of course. We are becoming skeptical news consumers, like Russians in the days when they said "v Pravde net izvestiy, v Izvestiyakh net pravdy" (In the Truth there is no news, and in the News there is no truth). It's a shame that we can't rely on mainstream news media, because when forced to the blogosphere to find out what's going on, we discover that not everyone who approaches you in a tatty coat tied together with rope is an Old Testament prophet.

But there's also plenty of stuff from more respectable sources, too. Michael Panzner ( who provides a great scan-and-select service for the economics newsfollower) directs us to this column by Morgan Stanley expert Stephen Roach. Brief highlights:

1. Only about half of an estimated $3.4 trillion in asset losses have been officially written off so far, according to the IMF.

2. The slowdown is worldwide, so other nations are unlikely to take up the slack.

3. The American consumer is not able or willing to resume spending as before.

4. 45% of China's economic activity is in "fixed investment" (building roads, factories etc) and there is a risk that they may be creating a lot of "white elephants".

Money is still changing hands here, but Roach says this is "fueled by a temporary boost from the inventory cycle", i.e. vendors are flogging-off surplus stock at bargain prices - which is why I've cited the feelgood M&S article above. After that, I think, comes cool reality - maybe continued lower prices, but also lower wages, lower profits, higher unemployment and an increase in bankruptcies.

Roach estimates a 40% chance of a "double dip" global recession this year. He also fears that economic stimulus will not be withdrawn quickly enough when a recovery comes, so possibly yet another bubble will be created. Another risk, in his view, is that the US will seek to protect domestic industry against Chinese imports; this could threaten the financial arrangements between the two countries, weaken the dollar and raise inflation.

Is it really not possible for radio and TV news to give a rounder picture of reality?

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Tuesday, January 05, 2010

Money fund or mattress?

When I first started in financial services, Albany Life (now Canada Life) had a reassuringly-named "Guaranteed Money Fund"; some time ago, this was quietly rebranded "Money Fund" (see page 19 of this brochure).

It's a sign of the times. Money market funds are supposed to be rock-solid - only one ever failed to return 100 cents in the dollar between 1971 and late 2008. But when Lehman Brothers collapsed in September 2008, it caused losses to a large and venerable US money market fund called The Reserve Primary Fund, which owned some Lehman debt. Initially, the loss was not great - Lehman debt represented only 1% of Reserve Primary's total assets - but there was a one-hour window in which investors could get their cash out at 100 cents on the dollar. Naturally, big investment companies, watching their computer screens, were in the best position to know what was going on and act accordingly. So they jumped out of Reserve Primary, in such volume that the Lehman debt was now worth 3% of the remaining (much shrunken) assets.

For the safety-conscious, there is hardly anything more disturbing than discovering that something you trust in completely is not entirely reliable. So a panic started, with investors exiting money funds generally, until the United States government said it would guarantee such funds. At least, it would guarantee those funds that agreed to pay an insurance premium to the government; and only investments made on or before 19th September 2008.

Now the rules on money funds are to be reviewed and understandably, it raises deep suspicions. In this recent post, Tyler Durden looks at a proposal to suspend your right to realize your money market investment, in a time of exceptional turbulence. Of course, that is exactly the time that you would wish to get out, and given the experience of September 2008 it would not be surprising to find that the institutional investors had already moved out before the suspension came into force.

It is important, because according to Durden's article about a third of all mutual funds' (the US equivalent of the UK's unit trusts) assets are in money market funds, and according to this Wikipedia article one-third of all money market funds are held by private investors. So the fear is that Joe Public would be left holding the baby if there should be a run on money market funds.

I think the fear is overdone. The measures discussed by Durden (see the paragraphs re "Recommendation 3") are clearly intended to make mutual fund investment into the money market safer, and less exciting in terms of gains; those funds that try to achieve better returns with higher risk are to be clearly identified and segregated, with tighter regulation plus provisions for emergency backing from central bankers. And removing promises re withdrawal on demand lessens the chances of a panic, by moderating expectations - it's like those commercial property funds that warn the investor that there could be a delay of up to 6 months if he/she wants to cash out.

Besides, even 97 cents in the dollar is a good return, when stocks have, at some points, lost as much as 50% of their value (e.g. between the end of 1999 and the summer of 2003).

A wider issue is the preferential treatment given to one class of investor over another. If The Reserve Primary Fund had cut its realizable value to 99 cents on the dollar immediately and for everybody, it might have prevented the panic, which was at least partly due to not wishing to be the last one left holding the worthless asset.

Nevertheless, there is always the question of what happens if you need money in a hurry. Argentine citizens were caught out in the "corralito" of December 2001, when banks froze accounts for initially a 90-day period (with the right to draw small amounts for day-to-day expenditure). The Argentine peso had previously been pegged to the US dollar, and after de-linking lost almost three-quarters of its exchange value by June the following year.

The real story, then, is the need for (a) emergency cash, in a form you can get at when you do really need it; and (b) for investors, a watchful eye on exchange rates, particularly in the light of economic problems because of out-of-control debt.

On the latter point, it's worth noting that the rot has already set in: the British pound has lost about 25% against the Euro in the last 3 years alone (and about 17% against the dollar, in the same period). A professional investor I read, called Warren Pollock, recently opined that the pound should eventually trade at around US $1.38, which means a further fall of 14%. Both currencies have lost against the Euro; but quite a few members of the European Monetary Union now have severe economic problems and it is not impossible that the dollar may enjoy a (relative) resurgence, not so much because of America's strength as because of others' weaknesses becoming better understood.

Currency speculation is for the high-rollers; but some ready money is a good thing to have, especially if inflation is not burning up its value. Maybe not under the mattress, though; as the Times reported in October 2008, sales of safes in the UK have soared in the crisis - as they did when Japan entered its long recession, years earlier.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

It's a sign of the times. Money market funds are supposed to be rock-solid - only one ever failed to return 100 cents in the dollar between 1971 and late 2008. But when Lehman Brothers collapsed in September 2008, it caused losses to a large and venerable US money market fund called The Reserve Primary Fund, which owned some Lehman debt. Initially, the loss was not great - Lehman debt represented only 1% of Reserve Primary's total assets - but there was a one-hour window in which investors could get their cash out at 100 cents on the dollar. Naturally, big investment companies, watching their computer screens, were in the best position to know what was going on and act accordingly. So they jumped out of Reserve Primary, in such volume that the Lehman debt was now worth 3% of the remaining (much shrunken) assets.

For the safety-conscious, there is hardly anything more disturbing than discovering that something you trust in completely is not entirely reliable. So a panic started, with investors exiting money funds generally, until the United States government said it would guarantee such funds. At least, it would guarantee those funds that agreed to pay an insurance premium to the government; and only investments made on or before 19th September 2008.

Now the rules on money funds are to be reviewed and understandably, it raises deep suspicions. In this recent post, Tyler Durden looks at a proposal to suspend your right to realize your money market investment, in a time of exceptional turbulence. Of course, that is exactly the time that you would wish to get out, and given the experience of September 2008 it would not be surprising to find that the institutional investors had already moved out before the suspension came into force.

It is important, because according to Durden's article about a third of all mutual funds' (the US equivalent of the UK's unit trusts) assets are in money market funds, and according to this Wikipedia article one-third of all money market funds are held by private investors. So the fear is that Joe Public would be left holding the baby if there should be a run on money market funds.

I think the fear is overdone. The measures discussed by Durden (see the paragraphs re "Recommendation 3") are clearly intended to make mutual fund investment into the money market safer, and less exciting in terms of gains; those funds that try to achieve better returns with higher risk are to be clearly identified and segregated, with tighter regulation plus provisions for emergency backing from central bankers. And removing promises re withdrawal on demand lessens the chances of a panic, by moderating expectations - it's like those commercial property funds that warn the investor that there could be a delay of up to 6 months if he/she wants to cash out.

Besides, even 97 cents in the dollar is a good return, when stocks have, at some points, lost as much as 50% of their value (e.g. between the end of 1999 and the summer of 2003).

A wider issue is the preferential treatment given to one class of investor over another. If The Reserve Primary Fund had cut its realizable value to 99 cents on the dollar immediately and for everybody, it might have prevented the panic, which was at least partly due to not wishing to be the last one left holding the worthless asset.

Nevertheless, there is always the question of what happens if you need money in a hurry. Argentine citizens were caught out in the "corralito" of December 2001, when banks froze accounts for initially a 90-day period (with the right to draw small amounts for day-to-day expenditure). The Argentine peso had previously been pegged to the US dollar, and after de-linking lost almost three-quarters of its exchange value by June the following year.

The real story, then, is the need for (a) emergency cash, in a form you can get at when you do really need it; and (b) for investors, a watchful eye on exchange rates, particularly in the light of economic problems because of out-of-control debt.

On the latter point, it's worth noting that the rot has already set in: the British pound has lost about 25% against the Euro in the last 3 years alone (and about 17% against the dollar, in the same period). A professional investor I read, called Warren Pollock, recently opined that the pound should eventually trade at around US $1.38, which means a further fall of 14%. Both currencies have lost against the Euro; but quite a few members of the European Monetary Union now have severe economic problems and it is not impossible that the dollar may enjoy a (relative) resurgence, not so much because of America's strength as because of others' weaknesses becoming better understood.

Currency speculation is for the high-rollers; but some ready money is a good thing to have, especially if inflation is not burning up its value. Maybe not under the mattress, though; as the Times reported in October 2008, sales of safes in the UK have soared in the crisis - as they did when Japan entered its long recession, years earlier.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Subscribe to:

Posts (Atom)