Sunday, April 28, 2013

UK: is inflation and national ruin inevitable?

See the Broad Oak page for "The Quiet Collapse of the Pound."

The quiet collapse of the pound

The forces ranged against the British pound may be so powerful that the government is in no position to offer inflation protection to savers.

I show above what has happened over the past five years. Nominally, UK inflation has advanced by 17 or 18 per cent, depending on how you choose to measure it.

Gold has soared, and had already done so for some time before 2008, but it had been at a low point for a long time during the years of the phoney boom. I still feel that, bearing in mind the amount of extra money pumped into the economy, gold is fairly valued. But compared to other assets it's a small market and so more volatile and subject to manipulation, so for the active trader it's full of traps:

So let's return to the first graph and look at the currency market instead, to get a feeling for our relative performance and a hint about the future.

The euro has risen 8% over the period - not dramatic, but the EU has its own large problems.

The US dollar has risen 29% and although it is an ailing giant, the dollar is still the world's major reserve and trading currency, so when crisis hits there may be a flight to USD. Longer term, the US economy is out of kilter, like that of the UK and EU, so all three are in a quandary - the choices appear to be painful deflation and social unrest, monetary inflation with all that attends it, or debt defaults and forgiveness (which powerful creditors are determined to prevent).

My feeling is that the UK will pursue the first course until it's politically impossible, then the second (by which time the smart money will have got out, as happened in a different way in the Cyprus bank debacle).

The orange columns (except for Saudi Arabia) show the progress of the six currencies tipped for 2013 by the Money Morning website. I have no idea whether their recommendations are good. And again, I'm not one of these nimble traders that draw lines all over their charts and make references to the Fibonacci series, tramlines, head and shoulders etc. Like all professional gamblers, they're terrific until they get to the point where they sell their binoculars for one last punt. Good luck to them but I haven't got their nerve.

What I'm looking for - and what was available for 35 years in this country, until the Coalition took over in 2010 - is something for the humble saver. Something safe that will simply hold its value in spending terms, after inflation and taxation. In short, something that makes saving worthwhile, instead of a form of slow financial suicide. I don't see why the cautious, prudent saver has to choose between losing to the pickpocket of inflation, or alternatively to the croupiers in the marble-halled casino of stocks and bonds.

But we may have gone beyond the point of finding the right bank for our safe haven; we could be at the stage of backing the right country. There's a stealthy run on the banks going on now - not only in Cyprus, but capital flight from the Euro area; soon enough, I fear, there'll be a sort of run on countries.

In which case, I'd be looking for one that is politically stable, balances its budget, is strong enough to defend itself (and isn't near a psycho state like North Korea), doesn't feel obliged to join in competitive devaluation to maintain its exports, doesn't have porous borders or an over-generous welfare system, and has what other countries will still want once the international disaster is over.

Australia, with its industry-relevant natural resources? The USA, with its high arable land-to-population ratio?

Wish I knew. Perhaps I should back all the best horses in the race. But one thing seems clear to me: the UK is not one of them.

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Fighting the Government for savers and against inflation (2)

This series is a report on my attempts to get questions raised in Parliament about the Government's failure to protect small savers against inflation, taxes and theft by banks. Part 1 is here.

The latest news that should (ought to) turn up the gas under this issue is Matt Taibbi's article for next month's edition of Rollling Stone magazine (htp: Jesse) detailing another gigantic price-fixing swindle by banks who have previously been exposed in the Libor scandal. As Taibbi reports, not only has the door opened to reveal that virtually all markets are rigged (against us, the ordinary people), but - astoundingly - an American court has accepted defendants' argument that nobody expected the interest rate market not to be fixed.

All the more reason why you might look at the Move Your Money website.

Here are some of the newer email exchanges between myself, my MP and his researcher:

MP to me - March 3, 2013:

I am happy if you wish to work with my researcher on written parliamentary questions on this issue.

(N.B. note the "written")

Researcher to me - March 12, 2013:

Me to researcher - April 21, 2013:

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

The latest news that should (ought to) turn up the gas under this issue is Matt Taibbi's article for next month's edition of Rollling Stone magazine (htp: Jesse) detailing another gigantic price-fixing swindle by banks who have previously been exposed in the Libor scandal. As Taibbi reports, not only has the door opened to reveal that virtually all markets are rigged (against us, the ordinary people), but - astoundingly - an American court has accepted defendants' argument that nobody expected the interest rate market not to be fixed.

All the more reason why you might look at the Move Your Money website.

Here are some of the newer email exchanges between myself, my MP and his researcher:

MP to me - March 3, 2013:

I am happy if you wish to work with my researcher on written parliamentary questions on this issue.

(N.B. note the "written")

Researcher to me - March 12, 2013:

[...] I understand you wish to ask ministers about maintaining the value of savings vis a vis inflation and purchasing power parity of the pound against other currencies – it would help if you could give me an indication of exactly what you would like to ask or if you could draft a question I could amend?

For instance, I’m not sure if you would like to simply ask a question along the lines of ‘ To ask the Chancellor of the exchequer what steps he has taken or plans to undertake to maintain the value of savings against increased inflation and devaluations of the pound’ -- or alternatively you might want to ask the Treasury if you have a particular scheme or strategy you would like them to adopt?

Don’t worry about phrasing, I can amend a question so that it will be accepted by the table office.

We can table a written parliamentary question to any department with ease and departmental oral questions in the house occur every few weeks, I am sure we could arrange for John to ask an oral question if his diary allows – Questions to the Prime Minister during PMQs on a Wednesday are more tricky – you can put in written Questions for oral response or try to catch the eye of the speaker if you are a member, but demand is, obviously, high and this would require John to both be in the chamber and willing to use what is an infrequent opportunity to gain significant publicity for a cause, on this issue. That’s not saying he would be unwilling to do so but I don’t know if he has an issue he does want to raise at PMQs and it might take a few months before that opportunity presents itself.

A written or oral question to the Treasury would be most feasible with a reasonable turnaround on a response.

For instance, I’m not sure if you would like to simply ask a question along the lines of ‘ To ask the Chancellor of the exchequer what steps he has taken or plans to undertake to maintain the value of savings against increased inflation and devaluations of the pound’ -- or alternatively you might want to ask the Treasury if you have a particular scheme or strategy you would like them to adopt?

Don’t worry about phrasing, I can amend a question so that it will be accepted by the table office.

We can table a written parliamentary question to any department with ease and departmental oral questions in the house occur every few weeks, I am sure we could arrange for John to ask an oral question if his diary allows – Questions to the Prime Minister during PMQs on a Wednesday are more tricky – you can put in written Questions for oral response or try to catch the eye of the speaker if you are a member, but demand is, obviously, high and this would require John to both be in the chamber and willing to use what is an infrequent opportunity to gain significant publicity for a cause, on this issue. That’s not saying he would be unwilling to do so but I don’t know if he has an issue he does want to raise at PMQs and it might take a few months before that opportunity presents itself.

A written or oral question to the Treasury would be most feasible with a reasonable turnaround on a response.

Me to researcher - March 12, 2013:

[...] I have some ammo to use in framing questions, the idea being to get govt to accept that there is a moral case for protecting the value of savers' money and in fact there's a couple of passages in Hansard that strigly [sic; intended "strongly"] indicate that acceptance in the year that NS&I Index-Linked Savings Certificates were first introduced.

It may well be true that the financial situation is serious, as your boss says - in fact I've been blogging about it since 2007 and warned of the banking crash both there and in the letters pages of the Spectator - but there is absolutely no justification for making the prudent pay the cost, or for forcing them to gamble with their money just in order to try to avoid losing it to inflation.

I wd very much like your help in framing Qs that will make the ministers, Chancellor and PM bloody well squirm.

It may well be true that the financial situation is serious, as your boss says - in fact I've been blogging about it since 2007 and warned of the banking crash both there and in the letters pages of the Spectator - but there is absolutely no justification for making the prudent pay the cost, or for forcing them to gamble with their money just in order to try to avoid losing it to inflation.

I wd very much like your help in framing Qs that will make the ministers, Chancellor and PM bloody well squirm.

Researcher to me - April 18, 2013

I’ve still got this on my list of things to do – You suggested you would be back in touch, but I do not seem to have a follow up email from you since the one below

Could you confirm if you have a question in mind, or if the more general one I suggested below would suffice? [The question was omitted from his email]

Could you confirm if you have a question in mind, or if the more general one I suggested below would suffice? [The question was omitted from his email]

Me to researcher - April 21, 2013:

Sorry, been away a few days.

I don't see the general question you refer to, but since Cyprus I have two serious worries - which should apply to many of my ex-clients and people generally:

1. How to set aside money and preserve its spending value, without being eroded by inflation and taxes and without being forced to accept any kind of investment risk;

2. How to be sure that no portion of savings below the deposit insurance ceiling will not be seized in some form of bank bail-in or pseudo-tax, but be payable in the form and to the schedule expected by the saver.

I understand that Tam Dalyell was feared as a Parliamentary questioner because his questions were short, to the point and allowed no room for irrelevant waffle in reply. Do you think you could frame questions on that model?

Also, should they not be asked as PMQs rather than handed off to get some dusty reply from the Treasury? My experience of the latter pretty much destroyed my confidence in getting anything other than fluff and party political twaddle.

I don't see the general question you refer to, but since Cyprus I have two serious worries - which should apply to many of my ex-clients and people generally:

1. How to set aside money and preserve its spending value, without being eroded by inflation and taxes and without being forced to accept any kind of investment risk;

2. How to be sure that no portion of savings below the deposit insurance ceiling will not be seized in some form of bank bail-in or pseudo-tax, but be payable in the form and to the schedule expected by the saver.

I understand that Tam Dalyell was feared as a Parliamentary questioner because his questions were short, to the point and allowed no room for irrelevant waffle in reply. Do you think you could frame questions on that model?

Also, should they not be asked as PMQs rather than handed off to get some dusty reply from the Treasury? My experience of the latter pretty much destroyed my confidence in getting anything other than fluff and party political twaddle.

No reply received before my next email to him - April 27, 2013:

Further to my last email of 6 days ago, perhaps you could spare the time to look at the latest article by Matt Taibbi in Rolling Stone. It may give you some idea of why I now (as a former IFA of 23 years' experience in the financial industry) regard the whole bank and trading shebang as irredeemably systemically corrupt. Any government that wishes to retain its claim to authority needs to protect the life savings of the little people.

http://www.rollingstone.com/

Do please let me know how you are getting on with framing appropriate questions as previously discussed.

Best wishes

http://www.rollingstone.com/

Do please let me know how you are getting on with framing appropriate questions as previously discussed.

Best wishes

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Fighting the Government for savers and against inflation (2)

This series is a report on my attempts to get questions raised in Parliament about the Government's failure to protect small savers against inflation, taxes and theft by banks. Part 1 is here.

The latest news that should (ought to) turn up the gas under this issue is Matt Taibbi's article for next month's edition of Rollling Stone magazine (htp: Jesse) detailing another gigantic price-fixing swindle by banks who have previously been exposed in the Libor scandal. As Taibbi reports, not only has the door opened to reveal that virtually all markets are rigged (against us, the ordinary people), but - astoundingly - an American court has accepted defendants' argument that nobody expected the interest rate market not to be fixed.

All the more reason why you might look at the Move Your Money website.

Here are some of the newer email exchanges between myself, my MP and his researcher:

MP to me - March 3, 2013:

I am happy if you wish to work with my researcher on written parliamentary questions on this issue.

(N.B. note the "written")

Researcher to me - March 12, 2013:

Me to researcher - April 21, 2013:

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

The latest news that should (ought to) turn up the gas under this issue is Matt Taibbi's article for next month's edition of Rollling Stone magazine (htp: Jesse) detailing another gigantic price-fixing swindle by banks who have previously been exposed in the Libor scandal. As Taibbi reports, not only has the door opened to reveal that virtually all markets are rigged (against us, the ordinary people), but - astoundingly - an American court has accepted defendants' argument that nobody expected the interest rate market not to be fixed.

All the more reason why you might look at the Move Your Money website.

Here are some of the newer email exchanges between myself, my MP and his researcher:

MP to me - March 3, 2013:

I am happy if you wish to work with my researcher on written parliamentary questions on this issue.

(N.B. note the "written")

Researcher to me - March 12, 2013:

[...] I understand you wish to ask ministers about maintaining the value of savings vis a vis inflation and purchasing power parity of the pound against other currencies – it would help if you could give me an indication of exactly what you would like to ask or if you could draft a question I could amend?

For instance, I’m not sure if you would like to simply ask a question along the lines of ‘ To ask the Chancellor of the exchequer what steps he has taken or plans to undertake to maintain the value of savings against increased inflation and devaluations of the pound’ -- or alternatively you might want to ask the Treasury if you have a particular scheme or strategy you would like them to adopt?

Don’t worry about phrasing, I can amend a question so that it will be accepted by the table office.

We can table a written parliamentary question to any department with ease and departmental oral questions in the house occur every few weeks, I am sure we could arrange for John to ask an oral question if his diary allows – Questions to the Prime Minister during PMQs on a Wednesday are more tricky – you can put in written Questions for oral response or try to catch the eye of the speaker if you are a member, but demand is, obviously, high and this would require John to both be in the chamber and willing to use what is an infrequent opportunity to gain significant publicity for a cause, on this issue. That’s not saying he would be unwilling to do so but I don’t know if he has an issue he does want to raise at PMQs and it might take a few months before that opportunity presents itself.

A written or oral question to the Treasury would be most feasible with a reasonable turnaround on a response.

For instance, I’m not sure if you would like to simply ask a question along the lines of ‘ To ask the Chancellor of the exchequer what steps he has taken or plans to undertake to maintain the value of savings against increased inflation and devaluations of the pound’ -- or alternatively you might want to ask the Treasury if you have a particular scheme or strategy you would like them to adopt?

Don’t worry about phrasing, I can amend a question so that it will be accepted by the table office.

We can table a written parliamentary question to any department with ease and departmental oral questions in the house occur every few weeks, I am sure we could arrange for John to ask an oral question if his diary allows – Questions to the Prime Minister during PMQs on a Wednesday are more tricky – you can put in written Questions for oral response or try to catch the eye of the speaker if you are a member, but demand is, obviously, high and this would require John to both be in the chamber and willing to use what is an infrequent opportunity to gain significant publicity for a cause, on this issue. That’s not saying he would be unwilling to do so but I don’t know if he has an issue he does want to raise at PMQs and it might take a few months before that opportunity presents itself.

A written or oral question to the Treasury would be most feasible with a reasonable turnaround on a response.

Me to researcher - March 12, 2013:

[...] I have some ammo to use in framing questions, the idea being to get govt to accept that there is a moral case for protecting the value of savers' money and in fact there's a couple of passages in Hansard that strigly [sic; intended "strongly"] indicate that acceptance in the year that NS&I Index-Linked Savings Certificates were first introduced.

It may well be true that the financial situation is serious, as your boss says - in fact I've been blogging about it since 2007 and warned of the banking crash both there and in the letters pages of the Spectator - but there is absolutely no justification for making the prudent pay the cost, or for forcing them to gamble with their money just in order to try to avoid losing it to inflation.

I wd very much like your help in framing Qs that will make the ministers, Chancellor and PM bloody well squirm.

It may well be true that the financial situation is serious, as your boss says - in fact I've been blogging about it since 2007 and warned of the banking crash both there and in the letters pages of the Spectator - but there is absolutely no justification for making the prudent pay the cost, or for forcing them to gamble with their money just in order to try to avoid losing it to inflation.

I wd very much like your help in framing Qs that will make the ministers, Chancellor and PM bloody well squirm.

Researcher to me - April 18, 2013

I’ve still got this on my list of things to do – You suggested you would be back in touch, but I do not seem to have a follow up email from you since the one below

Could you confirm if you have a question in mind, or if the more general one I suggested below would suffice? [The question was omitted from his email]

Could you confirm if you have a question in mind, or if the more general one I suggested below would suffice? [The question was omitted from his email]

Me to researcher - April 21, 2013:

Sorry, been away a few days.

I don't see the general question you refer to, but since Cyprus I have two serious worries - which should apply to many of my ex-clients and people generally:

1. How to set aside money and preserve its spending value, without being eroded by inflation and taxes and without being forced to accept any kind of investment risk;

2. How to be sure that no portion of savings below the deposit insurance ceiling will not be seized in some form of bank bail-in or pseudo-tax, but be payable in the form and to the schedule expected by the saver.

I understand that Tam Dalyell was feared as a Parliamentary questioner because his questions were short, to the point and allowed no room for irrelevant waffle in reply. Do you think you could frame questions on that model?

Also, should they not be asked as PMQs rather than handed off to get some dusty reply from the Treasury? My experience of the latter pretty much destroyed my confidence in getting anything other than fluff and party political twaddle.

I don't see the general question you refer to, but since Cyprus I have two serious worries - which should apply to many of my ex-clients and people generally:

1. How to set aside money and preserve its spending value, without being eroded by inflation and taxes and without being forced to accept any kind of investment risk;

2. How to be sure that no portion of savings below the deposit insurance ceiling will not be seized in some form of bank bail-in or pseudo-tax, but be payable in the form and to the schedule expected by the saver.

I understand that Tam Dalyell was feared as a Parliamentary questioner because his questions were short, to the point and allowed no room for irrelevant waffle in reply. Do you think you could frame questions on that model?

Also, should they not be asked as PMQs rather than handed off to get some dusty reply from the Treasury? My experience of the latter pretty much destroyed my confidence in getting anything other than fluff and party political twaddle.

No reply received before my next email to him - April 27, 2013:

Further to my last email of 6 days ago, perhaps you could spare the time to look at the latest article by Matt Taibbi in Rolling Stone. It may give you some idea of why I now (as a former IFA of 23 years' experience in the financial industry) regard the whole bank and trading shebang as irredeemably systemically corrupt. Any government that wishes to retain its claim to authority needs to protect the life savings of the little people.

http://www.rollingstone.com/

Do please let me know how you are getting on with framing appropriate questions as previously discussed.

Best wishes

http://www.rollingstone.com/

Do please let me know how you are getting on with framing appropriate questions as previously discussed.

Best wishes

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Sunday, April 14, 2013

Australia: Alternative Economics

I was born in Manchester England in 1950. My mother a housewife, my father a salesman in an engineering company but steadily rose to high management. He was quite conservative but could entertain any idea and judge its merits, and he liked to debate. He was quite willing to be devil's advocate and would make a spirited defense of ideas he didn't adhere to. That was when I began to question just about everything and started my career as a rebel.

I failed the 11+, a single test at age 11 which purported to determine if a child has academic potential. Somehow, in my last couple of years at school, I got sent to an age-old part-boarding grammar school. It was super conservative and the teachers still wore gowns and mortar boards. It reeked of tradition, privilege and snobbery. This was where I honed my and hardened my rebellious streak. I was in the headmaster's office at least once a week. At university (mech eng), I toyed with joining the Socialist Society which was the most radical group, but they said and did such silly things, so I joined the Peace Society and got to do demonstrations (peaceful of course) and started to pick up some flower-power, hippie ideals of sharing and caring, love and peace man! I began to see how unfairly money is distributed in a country and around the world. It still is, worse perhaps.

I managed to do enough work to graduate with honours, but did not want to get my nose to the grindstone of a career, so worked a couple of months in a warehouse stacking boxes and headed off on the overland hippie trail to the the antipodes. A couple of years and many adventures later I found myself in Australia. I was now an expert on living on a shoestring and out of a backpack. Suddenly, due to a genocidal maniac called Ida Amin in Uganda, the Commonwealth changed all the immigration rules. By immense good luck, I was entitled to be a permanent resident of Australia, just by being in the right place at the right time. It has been very difficult to come to Australia since that time.

I then put in the longest period of work by far in my life. Two whole years! Doing exploration work in central Western Australia. With one other guy, or sometimes on my own, I did 4-6 week projects in some of the most open and deserted landscape on the planet. The job paid labourer's wages, but food and swagroll was provided, and there was nowhere to spend money. Great way to save. I spend the money to buy an empty block of land at the other end of the country. From flat, desiccated, blistering desert to hilly lush rainforest in far north Queensland. 156 acres of cloud-forest on top of the great dividing range. Now to really become a self-sufficient hippie recluse, maybe even start a commune! No money left, no knowledge of how to build, grow anything, live etc, no road in, no tools ........ no problem. I invested my last few dollars in a machete so at least I could get to the place. I worked a couple of months out in the bush to buy a 1962, 3 geared Toyota landcruiser for $750. The exhaust valves were blown and many other things wrong but got it going again. I got stereoscopic aerial photos centered on my block and used skills I had acquired doing exploration to see the land around in 3D so I could spot a possible route in. 4kms long and totally unmade, it went mostly through a neighbouring farm.

I started building a house with very little money, no idea how, no plans, not even a sketch on the back of an envelope, no power and of course no council permission because it didn't even occur to me. I used a considerable amount of discarded scraps from local saw mills, bush poles for free, secondhand doors and windows, scrap fencing from the tip to reinforce the concrete stumps, discarded 1 inch thick boards from 3 inches wide to 20 inches. They were used in two layers for the outside cladding and cost $10 per ton on average. A local planing mill sold reject packs of planed wood such as floorboards at a fraction of the retail price. So I built myself a house of 90 sq m for $1400 complete with plumbing, wood stove etc etc. A third of the cost was the tin on the roof. 35 years later it is not only still standing but has not required any maintenance beyond a bit of paint. You can check it out if you like at www.possumvalley.com.au . It is now called Blackbean Cottage.

I built a hydro-electric system utilising a 20m high waterfall and knowledge I acquired at university. I built a water system to provide water to the house utilising a smaller waterfall and a ram pump to deliver what most take for granted:- water coming out of taps. I built sewerage systems to deal with the stuff most don't even want to think about. I enjoyed all my successes at the most menial things. I love getting things to work.

I got married, have 2 daughters, started doing wood craft and carving to sell at local markets, and whenever I required money, dug spuds for the local farmers. Hard work I can tell you. Anytime the farmer looks round and sees anyone on the digger with any time to spare, he finds another gear until everybody is flat out. Tractors have a lot of gears. When I started digging, spud bags had a nominal weight of 70 kgs. They mostly weighed 75 kgs as they were packed by volume and hand sewn with twine and a 6 inch needle. It was quite a skill as they mustn't leak spuds in all the handling on the way to market. On average they were filled, compacted, sewn and stacked in 11 seconds. I liked it though. It was satisfying. There is no product more important than a potato. There are products of equal value like an avocado or a cup of rice, but the humble spud is my personal favourite.

So at last, I get round to the subject in the title. Alternative economics. At 63 years of age, I can now analyze my chosen path in life for its economic and social benefit. I have worked for wages perhaps a total of 4-5 years. I have paid tax in only two years when I did exploration. I have also worked as a builder's labourer, a carpenter building a school in Darwin (which got flattened 6 months later by cyclone Tracy), and perhaps the best was as a ski lift operator in New Zealand. Great.... the spell-check has never even heard of New Zealand. I still don't earn enough to pay tax. I now use two houses to earn a living at B&B. It is to my great personal satisfaction that people mostly have a wild and real experience at my rainforest retreat.

I have mostly worked directly for myself, building things I need without the overheads of tax on what you earn, other taxes, fees, insurance, travel, profit and other costs which multiply when you employ someone to build your house etc. And of course interest on the mortgage you require to get started. So my strategy has been not to go into debt. If you haven't got the money, don't do it. I have always valued my freedom and debt is the antithesis of freedom. I have maintained my financial freedom throughout my life by being debt free which enabled me to pursue many opportunities. Of course having children is a lifetime commitment with no remission, and which I undertake gladly. So I am not free of obligation or responsibility. Please, if you escape the rat-race don't think you will have freedom. It will just morph your responsibilities onto a different landscape. Perhaps a better landscape, where your concerns are family and friends rather than money and debt.

My income for the last twenty years has come from 2 fully self-contained cottages. I don't provide meals so the work is servicing, maintenance and washing linen and towels. I work perhaps a few hours in the day. It is a small non-taxable income but I have no debts and few non-business payments. I have few expenses, generate my own electricity, and the biggest bill every year is the rates. So I have a small income but nearly all of it is disposable at my whim.

_____________________________________________

Paul's Possum Valley blog and website are here.

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy.

Saturday, April 13, 2013

Anuta

Anuta tempts the philosopher and moralist. Its 300 Polynesian people live on the smallest inhabited island in the South Pacific and sustain themselves by carefully harvesting their natural resources. Fragile, precious, beautiful life in utter isolation - a metaphor for planet Earth in a universe where we may still turn out to be alone.

The BBC sent ex-Royal Marine Bruce Parry there in 2007; he said afterwards, "If I had to pick one tribe to go back and live with permanently — and I hate doing this, it’s not a contest — it would be the people of Anuta [...] It’s got white beaches, blue seas, good food and gentle, friendly people who have a wonderful philosophy of sharing." The communal ethic is calleed "aropa" in their language.

In 2009 the BBC returned to include the story in their stunningly-shot series "South Pacific", contrasting Anuta with Easter Island, where the tribes' competition and reckless exploitation of their ecology led to catastrophe. (The Easter Islanders are the starting point for Belgrano whistleblower Clive Ponting's 1991 book, "A Green History of the World: The Environment and the Collapse of Great Civilizations", reissued in 2007.)

BBC reporter Huw Cordey was part of the 2009 visit and made a radio programme for the Nature series, called "Anuta - An Island Governed By Love". He found that even in Anuta there are discontents, like anywhere else.

Yet we're still haunted by the myth of the happy land. As the poet Elizabeth Jennings says, "Sickness for Eden was so strong."

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy.

Friday, April 12, 2013

Gold market crashes!

Chart: The Real Asset Co

All original material is copyright of its author. Fair use permitted. Contact via comment. Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog; or for unintentional error and inaccuracy. The blog author may have, or intend to change, a personal position in any stock or other kind of investment mentioned.

Tuesday, April 09, 2013

Mrs Thatcher and inflation: a letter to the Spectator

Republished from the Broad Oak Blog - original post dated 16 January 2010 (N.B. BoE M4 data from 1963 - 1981 has recently been redacted, without explanation):

Sir;

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

Sir;

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

Mrs Thatcher and inflation: a letter to the Spectator

Republished from 16 January 2010 (N.B. BoE M4 data from 1963 - 1981 has recently been redacted, without explanation):

Sir;

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

Sir;

Sir Peregrine Worsthorne (Letters, 16 January) may have been right to support Mrs Thatcher for confronting the unions, but I believe he is wholly mistaken when he says she tackled inflation. Thanks to the opening up of global markets, consumer prices have been lowered by cheap foreign labour, indirectly by the importation of goods, and directly by the deliberately uncontrolled immigration of low-paid workers. However, behind the scenes there has been massive long-term monetary inflation, the woeful consequences of which we are now merely beginning to suffer. Economics may seem rather dry, but its implications are correspondingly fiery and so I hope your magazine will allow room for explanation.

Comparing GDP with (M4) bank lending figures from the Bank of England’s website, which gives data from 1963 on, we see that annual increases in lending almost always outstrip increases in GDP, but sometimes far more so than others. The worst was in 1972, when M4 increased by 35% (GDP grew by only 12%); the fear of monetary inflation and its potential effect on exchange rates may have been a major factor in OPEC’s decision to hike oil prices in 1973, which triggered years of high price inflation in the UK and the humiliating IMF rescue in 1976. Lending increases dropped below GDP between 1974 and 1977, then resumed ascendancy, though not in time to rescue James Callaghan’s premiership.

But inflation did wonders for Mrs Thatcher. The average annual excess of M4 growth over GDP in 1964-79 was 2%; from 1979-1990, the “Thatcher years”, it averaged 8% (and about 4% p.a. thereafter). The results have included overspending on luxuries; the loss of jobs and industrial skills; the export of machinery and tools; and a huge exaggeration of property and stock valuations. Worse, we now have a large class of economic dependants, both home-grown and recently imported, whose support costs cannot be externalised as easily as our manufacturing capacity.

Sir Peregrine may not divine in Mr Cameron the architect of our rescue, but I fear the situation may now have developed well beyond any man’s power to amend without reform on a scale that may not be entirely possible in a democratic society.

UK: Money-movers play catch-me-if-you-can

The global financial crisis is also a local issue for the UK, dubbed the 'global capital of money-laundering' in a Private Eye magazine investigation by Richard Brooks (August 2012).

The role of the financial sector in Britain ballooned in the years before the breakdown: this 2011 report by the Bank of England (pdf) shows that its annual growth was 6%, twice that of the economy as a whole.

That's why we need it. But why does the rest of the world need it to be in London?

In part the answer is that, as David Malone explains below, our system is particularly good at handling money without asking too many awkward questions. Shell companies make it hard to track down who is running businesses.

Moreover, unless money is definitely proved to have come from illegal activities, the authorities are unable to treat money transfers as criminal "money-laundering". Malone's only censored post to date, from which he quotes sections here, was a detailed investigation for Reuters into alleged money-laundering in Cyprus; but his original piece fell foul of that (perfectly logical, of course) lack-of-predicate-crime rule.

In this context it's worth remembering that the UK is also known as the "libel capital of the world", with potentially big payouts for plaintiffs if the defendant cannot prove his allegations (up to three years ago, it could get much worse than a civil court case: there was such a thing as criminal libel, punishable by imprisonment - this was what caused Private Eye's then editor Richard Ingrams to throw in the sponge when Sir James Goldsmith pursued him in July 1976).

And now, following the Leveson inquiry into abuses by mainstream journalists, bloggers may find themselves at risk of high financial penalties, without having the legal and financial resources of the conventional Press to help defend themselves.

I also reproduce here a piece by France-based blogger John Ward, reporting on the vast quantities of cash held in offshore banks that might (if captured onshore) otherwise contribute up to a trillion pounds to the UK economy.

In a digitised world, capital can zip around the globe far faster than leaden-footed regulators and tax authorities. Cyber-money is also very useful for dodging attempts by local banks to grab it to shore up their reserves, as we are seeing in Cyprus - and this article on Charles Hugh Smith's site goes further, implying that EU banks may have influenced a delay in the European Central Bank's enforcement action against the island, to allow them time to extract most of their cash before the shutters went down.

Finally, delay can help bosses as well as the banks they run: there is much noise being made at the moment about "examining powers to take legal action" against three directors of HBOS who were on watch when billions were lost by their company; but the Financial Services Authority has a strict time limit of three years to take disciplinary action against individuals, and that deadline has come and gone. A cynic might wonder why exactly the FSA missed it, but the fact remains that we have to obey the law as it stands, so I don't expect any retrospective ruling against these people, who are far from the only ones to have (allegedly) overseen significant losses in the banking sector.

My sincere thanks to David Malone and John Ward for permission to reproduce their posts.

________________________________________________

Making the Truth Illegal – revisited

“Making the Truth Illegal” is the title of the only post I have ever removed from this blog.

I removed it because I was threatened with legal consequences if I did not. (Plus, I would like to add, some of the way I had written the blog post was stupid and could have hurt someone who had helped me.)

The post concerned an article I had written for Reuters which they decided they could not/would not publish. Reuters pulled the article because they and I had been threatened, by a major European Bank, with legal consequences if they did not. The title of the article was “Cyprus, Magnitsky and the truth about Money Laundering.”

Although I cannot publish the article I can show you how it began and tell you how it is, that the truth it contained was made illegal.

The article began:

Money laundering is the life blood of organized crime. Without it crime would simply not pay. But who does the laundering? The easy and obvious answer is criminals. But that is completely wrong and is at the root of our inability to stop it.

Criminals are the people who need money laundering. They are the clients. But they do not, themselves, know how to launder money. The only people who do know, and who are in positions to do it, are those whose day jobs are the many professional services which make up laundering: the accountants, lawyers, company registration and management agents, account managers in banks and company directors in companies that have no reason to be, other than to pass hot money through an endless spin cycle. In organized crime, criminals provide the crime but professionals provide the organization.

Of course we could get jesuitical about it and say, but those professionals who launder are criminals. Which would be fine, except that we do not treat them as criminals. Criminals break laws. Professionals do not, they have ‘failures of compliance’. One is considered an active, purposeful ‘doing’ of something, for which punishment is de rigeur. The other is excused as an unfortunate and unintentional ‘not doing’; an oversight, omisssion or failure to do, for which one and one’s employer get admonished to ‘do’ better. And as long as you promise you will, all is considered fine and finished. There may be a small fine but nothing to lose your bonus over. No one senior ever goes to gaol.As you can see the purpose of the article was not simply to prove, what everyone already knew, that Cyprus had indeed been laundering dirty Russian money, but to say something about WHO actually does the laundering. The point was to finger the launderers themselves not their clients. Of course that meant naming companies, lawyers, company directors, company registration agents, and last but not least, the banks and individuals in them. These are, of course, people who are not used to the idea that they can be named, take grave exception to being named and who have the power, I discovered, to make sure they are not.

Criminals are investigated – by police. Professionals are ‘regulated’ – usually, and rather conveniently, by themselves or colleagues. People who rob banks have legal problems. People in banks, who rob people, or help others to rob them by laundering their money for them, they have regulatory issues. One is serious the other is a joke. How many bankers actually went to prison from Wachovia or Citi or HSBC?

All this might seem rather sweeping. But it is not. It is just that usually we do not get to hear about the people and businesses who do the actual laundering nor what happens to them afterwards. When money laundering is reported it is usually the lurid details of the clients of the money laundering, the drug cartels and terrorist organization, who get all the headlines. Hardly ever do we hear of the launderers themselves. And that is because, as already noted, they are never ‘guilty’ of having ‘done’ anything. But events in Cyprus have recently given us a rare opportunity to lift the sewer’s cover, peer inside and see at least some of the people who failed to act; who by omission, oversight, laziness or complicity, intentionally or otherwise, ‘helped’ to launder money.

As the philosopher Edmund Burke famously noted, “All that is necessary for the triumph of evil is that good men do nothing”.

The article also did one further thing. When you added it all together and told the whole tale in all its detail, with all the names, dates, places and amounts, one further conclusion jumped out. The lawyers, accountants, company directors and bankers, who did the laundering, are also the people who the anti money-laundering system relies upon to police the system and stop the laundering. The inescapable conclusion is that the anti-money laundering system not only does not work, but seems expressly fashioned to make sure it does not work.

It is possible – it happened in the Magnitsky case – for a criminal to buy a bank and be granted a bank license. Yet the law says it is the directors of such a bank who will be relied upon to contact the authorities about suspicious transactions. Criminals don’t often turn themselves in, yet in every country this is the non-system our leaders and financial experts maintain. In the UK the law is set up so that a company can be set up without any due diligence at all being done to determine the character let alone the actual identity of the owner. Because of this ‘loophole’ as the authorities coyly refer to it, the UK is home to tens of thousands of shell companies set up by criminals and used for criminal purposes. This may sound like a fantastic charge and one I cannot possibly substantiate. Yet almost every major case of fraud or money laundering will involve UK shell companies. Follow the Magnitsky money and you will see it pass thorough UK shell companies. The same goes for the $64 billion of state money stolen from Kyrgyzstan much of it then passed through UK shell companies. Or the on-going case of money laundered out of Ukraine by means of a fake oil rig purchase. That money too passed through UK companies.

I could give you plenty of other examples but the important point is that NO ONE in authority can offer a shred of evidence to show that I am wrong no matter how many criminal companies I claim there are likely to be, for one simple reason. THEY HAVE NO IDEA WHO OWNS THE COMPANIES. The system is set up so no one knows. Companies register owners but they can be other companies in other jurisdictions. And it is easy to set up a company in such a way so that no one checks on the owner at all, ever. That is the system we maintain.

Every minister who has ever had the power to change this state of affairs has been aware of this but they have all chosen to leave it that way.

In short we have a system which is conveniently designed so it does not stop money laundering but does make sure no one will be prosecuted. It serves to shield the guilty not stop them.

I realize these are statements that can still be dismissed as ‘conspiracy’. Without the 8000 words of detail the article contained, without the references to over a hundred pages of bank transfers and company records, I am left with just what I know to be the case without being able to show you what convinced me.

All I can do, as promised, is show you the final ‘shell’ which surrounds everything else and which allows the rest of the corrupt system to exist and do its job. The last shell is a legal one and I had not understood its importance, nor its power, until it did its job and stopped me publishing.

This is how it works.

First a few facts. In the Magnitsky case $230 million was stolen from the Russian state. That money was then laundered in a scheme that involved five deaths, a lorry load of bank records that exploded, eight banks, numerous shell companies and complete, abject and total regulatory failure. It is called the Magnitsky case after Sergei Magnitsky who was found dead, handcuffed on the floor of a cell in a Russian prison. His body, photographed at the time, was covered in bruises.

Mr Magnitsky had been arrested and then held without charge or trial in the custody of the Russian Interior Ministry for nearly a year. He had been detained shortly after he had named in official testimony Interior Ministry officials and certain tax officials as the criminals behind the theft. The men he named were the ones who arranged his detention.

BUT, the Interior Ministry held its own investigation. What it found was that although the money had indeed ‘gone missing’, none of the officials Mr Magnitsky had named were, according to their official investigation, guilty of anything other than being ‘tricked’ by person or persons unknown. The Ministry did try to suggest several culprits but two of them died mysteriously of heart attacks a thousand kilometres from their homes before they could testify, while another had, rather embarrassingly, died before the crime he was accused of had even been committed. The Ministry looked silly even by Russian standards and no case was brought.

Eventually the Russian officials accused the deceased Mr Magnitsky of being the mastermind behind the crime he had been investigating. At one point the Russian state said it was going to put him on trial posthumously. So far it has not. And thus the case rests with the conclusion that there was no crime, only a ‘trick’ with no one found guilty.

It was also decided in Mr Magnitsky’s absence that despite the photographic evidence of his beaten body, he had died of natural causes and no crime had been committed there either. Case closed. And that ‘Case closed’ is what it is all about.

In the end it doesn’t matter what actually happened nor what evidence is to hand. As long as some official body does its own ‘investigation’ from which it concludes nothing happened, then nothing did, and the case can be closed. Not only that but if anyone should try to look for themselves at the evidence they cannot refer to anyone or any bank as being involved in criminal behaviour of any kind. Because there wasn’t any.

If no money was stolen – and none was because the Russian said so – then no one could have laundered any. How can you launder money that was not stolen?

The Russian decision meant, in legal parlance, that there was no ‘predicate’ crime – no crime from which other crimes followed. Which means, if one authority says there was no crime, every other authority in every other country, should it want to, can point to this judgment and say, ‘why should we investigate anything if there was no crime in the first place?’

This meant when an official complaint was sent to the Cypriot authorities in 2008 alerting them to the Magnitsky affair, right at its beginning, they could ignore it. And they did. The Cypriot police were sent an official complaint in 2008, and to this day they have never replied to it nor even questioned the people, even Cypriot people, named in it.

In fact even when the Cypriot Authorities were sent another much more detailed complaint in 2012, which gave them dozens of leads and lines of enquiry they wrote back saying,

“…it is important that we firstly obtain information from the Russian authorities about the predicate offence or offences committed in Russia.And of course there was no predicate crime. Not officially. Even though companies were stolen and hundreds of millions did ‘go missing’.

Thus we plan to contact the Russian authorities in order to obtain information…”

Similarly, in 2010 another complaint was sent about the Magnitsky affair, this time to the Austrian authorities. The complaint alleged that the very large and powerful Austrian bank Raiffeisen, had handled much of the money that had ‘gone missing’. The Austrian authorities opened an investigation which concluded Raiffeisen had done nothing wrong at all. Case closed.

The Russians found no crime had been committed on their patch. The Austrians found nothing on their patch either.

This is despite the fact that Raiffeisen did handle the money. But you see handling is NOT laundering. Laundering requires the money be illicit AND that Raiffeisen knew, or reasonably could have known, the money was illicit. And the Austrian regulator concluded that Raiffeisen could not have known there was anything wrong with either the money it was handling, nor the bank from which it came nor the owner of that bank. The owner we are talking about here is the criminal – a convicted criminal who owned his own bank – mentioned earlier. According to Raiffeisen and the Austrian regulator the criminal past of the owner of the bank Raiffeisen was doing business with, could not have been known till a later date.

Now I find this judgement to be difficult to understand since the man in question had been convicted in Russian court in 2006. There are court transcripts of his admission of guilt which I have read. Yet Raiffeisen was handling the money in question in 2008.

BUT it doesn’t matter if I or you find this odd. The only FACT that is important, is that the Austrian regulator looked and found Raiffeisen NOT guilty of any crime. And so they are innocent. Case closed.

This is how you can end up, as I did, compiling facts and dates, evidence of bank transfers subpoenaed in court, which lead you to a conclusion that you are nevertheless not allowed to make public. You can present all the evidence but you must contrive to do it without ever mentioning the name of a crime, nor suggesting any illegal activity in the piece. And of course you certainly cannot conclude in writing what the evidence suggests. If you try to , as I found, you are threatened with the law.

And that is how you make the truth illegal.

If this was just one case it would be horrible but isolated. But it is not. This use of official and legal judgements to squash the truth is exactly what happened in the case of Jonathan Sugarman and UniCredit. He found evidence that UniCredit was very seriously breaking the law. He got an outside company to check and they agreed. The Irish regultor however, said, ‘There’s nothing to see here move along’. And Jonathan was threatened with leagal action if he did not go quietly away and hide.

What does all this mean for money laundering?

Here is how I concluded the article I cannot publish.

People love to talk about the ‘risks to banks and companies’ from money laundering. What risks? Think of the notorious cases of money laundering before Magnitsky: Citi., Wachovia, HSBC. No one was gaoled. No one senior even lost their job. Fines are a joke. Wachovia, for example handled or laundered over $370 billion of dirty or suspect money out of Mexico. They were fined one two thousandth of that amount, just $160 million. As a percentage of the direct financial benefits accrued to Wachovia, from having the dirty money flowing through their books, fines for money laundering are vanishingly small and better thought of as a tip pressed into the palm of a compliant doorman.________________________________________________

In reality, simply looking at the facts of what it has cost the banks in gaol time, fines or even something as intangible as their standing with their regulators and governments, it is very much worth it to launder. As for ‘standing’ or reputation – being guilty of huge money laundering did no harm to Citi when it came to bailing them out. Nothing untoward has happened to Wachovia or HSBC. In short – on a cost benefit analysis I would say it is of huge benefit and virtually no risk, for any bank large enough to be able to launder money, to do so.

And what of all the many companies and professionals, the company agents, lawyers and accountants, who do the jobs which make up the bulk of the work of laundering? Are there any real risks for them? I would say there are few because our system simply does not investigate what they choose to do. Instead it is very careful to only ask them to fill out forms, to self regulate and to ‘comply’.

I think the questions we need to ask ourselves and our politicians is why is it that the financial world is ‘regulated ‘ while we, ordinary citizens, are policed? Why do they have regulations to observe, while we have laws to obey? Why are they asked to merely assess themselves while we are investigated by officers of the law? Who profits from this careful double standard?

When you boil it all down, anti-money laundering is about asking criminals and the law abiding, both, to write reports about themselves. Needless to say the criminals lie. But we pretend not to notice, and so in every country all the paperwork says there is no money laundering going on. Yet hundreds of billions is laundered every year.

Now, John Ward's post:

THE EVADERS: British banks control enough tax evasion to almost pay off our National Debt at a stroke

A story goes global, and damns the self-styled elite

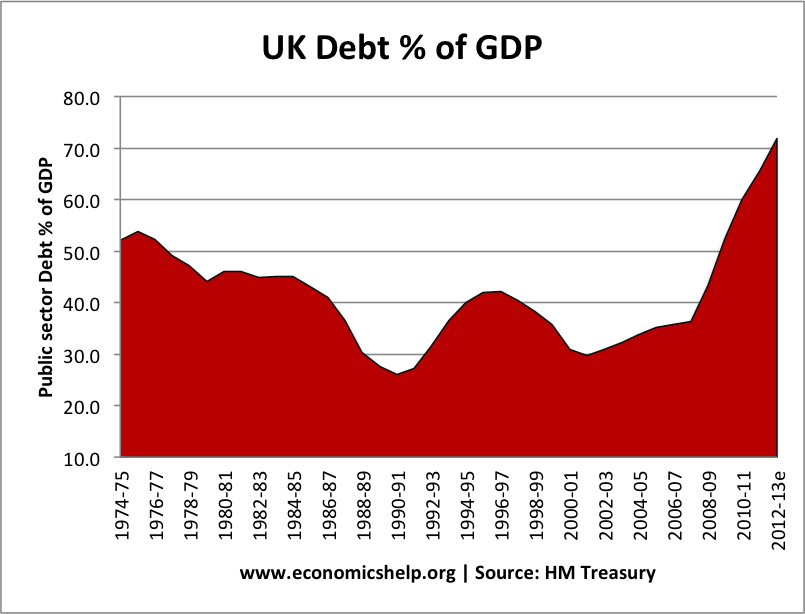

UK debt versus GDP…would be transformed if tax evaders paid their way

Last Friday, every French newspaper’s front-page from the Rightist Le Figaro to the Leftist Liberation led with the series of offshore tax haven scandals now threatening to overwhelm President Francois Hollande. In the UK, the Virgin Islands name-and-blame game has put David Cameron very seriously on the back foot. And the obvious connection between Tory newspaper The Daily Telegraph’s ownership and the Sark tax-evasion scandals there has shaken many from their torpor of bland acceptance. Throughout Europe’s citizenry this morning, there is a growing feeling that – far from being a tiny minority – rich-businessman tax evasion is the norm.

The Irish Times last Saturday threw up a staggering statistic: over 30,000 Irish firms have directors registered in offshore jurisdictions. Furthermore, in Sark specifically – population 600 – there are more than 11,000 bank accounts of directors registered to Irish firms – 18 for every island resident. There are roughly 560,000 business enterprises in the Irish Republic, of which no more than 240,000 could be described as turning over enough to make directors’ offshore holdings worthwhile. Thus an incredible 1 in 8 of the country’s business élite is stealing from the taxman.

This isn’t going down well among Ireland’s poorer classes – not least because Enterprise Ireland’s own data showed that over a thousand of its business members received government funding in 2010, with a total of 86 receiving commitments for financial support in excess of €100,000 for significant R&D projects. Life is a thing of give and take, but for Ireland’s top earners it seems to be all take and no give.

Coming in the wake of similar behaviour over the last five years from the West’s bankers and the Greek econo-political class, there is something about offshore – and the Virgin Islands story in particular – that seems to have completed a synapse connection….thus allowing the penny to drop at last: the ordinary folks are being gang-raped by greed on all sides.

As many of us always suspected, the insouciant wealth-accumulation obsession of frontal-lobe afflicted bankers is what joins them at the hip with the top earners in business – regardless of which country or culture one surveys. The ever-unpleasant HSBC’s Guernsey operation was last November shown to be shielding £699m in 4,388 accounts in Jersey – with one investor holding £6million. The average balance is £337,000. Equally, the true extent of American and German fat cat tax-evasion has been unearthed by the German Federal Intelligence Service. It is conducting a widespread investigation into Lichtenstein banking – and that of Luxembourg – where tens of thousands of US and Bundesrepublik tax evaders are hiding massive amounts of cash.

A 2012 study of 60 large US companies found that they deposited $166 billion in offshore accounts during 2012, sheltering over 40% of their profits from U.S. taxes. Yet Wolfgang Schäuble has invested a great deal of spin-time trying to suggest that Cyprus shielding the wealth of crooked Russians was atypically evil enough to warrant Berlin’s snaffling of the island’s potential energy economy. This is now shown to have been bollocks not just as a rationale, but also in its alleged uniqueness. And some of Wolfie’s mates appear to be up their eyes in similar operations around the world.

But the burgeoning scandal is more embarrassing for David ‘Legup’ Cameron than any other leader because, as the Guardian for once reported accurately at the weekend, ‘one nation in particular has ties to offshore havens everywhere. It’s a veritable nexus of offshore influence, related to havens in the Caribbean, and much closer to home. That nation is, of course, the United Kingdom.’

As so often happens today, without the leaking of more than 2m offshore files to the International Consortium of Investigative Journalists (ICIJ), the extent of this three-faced hypocrisy would be unknown to us still. So while George Osborne talks a good game about “all being in this together” – and Cameron witters on about “not wanting to associate with” tax evaders – the reality is their administration and bankrolling ranks are crammed with some of the worst offenders and facilitators. Lord Green ran HSBC for years, Jeremy Hunt is an aggressive tax-avoider, the Barclay Brothers run Sark, Boris Johnson is a particular favourite of the Sarkist-Banking fraternity, and numerous large Tory donors are among the wealthy ripping off Sovereign revenue offices: more than 175,000 UK companies have directors in offshore jurisdictions.

The ICIJ’s project uncovered a network of empty holding companies and names essentially rented out to fill out boards of non-existent corporations, including a British couple listed as active in more than 2,000 entities. This is a mirror image of the tiny survey conducted by The Slog last week into the identity of those who were early departees from the Cyprus depositor haircut.

For me, however, it is a calculation of the totals involved globally that change these revelations from being just another “it’s the rich what gets the sorrow” yarn into something that just might – we live and hope – finally get Middle England off its sofa and angry enough to demand justice.

A 2012 report from the Tax Justice Network (a UK company) estimated that between $21 trillion and $32 trillion is sheltered from taxes in unreported tax havens worldwide. Tax havens have 1.2% of the world’s population and hold 26% of the world’s wealth – including 31% of the net profits of United States multinationals. We are indeed talking about ‘a tiny minority’ here – the usual suspects – but also a colossal percentage of the money that should have been paid in Sovereign taxes. Financial opinion leaders I asked last week for an estimate of the percentage of offshore monies administered by British banking thought the number to be between 40 and 60%.

Being kind to the perpetrators and assuming (a) the lower end of those estimates and (b) lowest assessments of global market size and (c) a net tax rate of 15% being evaded, the Government of the United Kingdom knowingly loses almost exactly a trillion pounds in tax revenue thanks to the havenism endemic in the banking system it is supposed to regulate.

That is six NHS budgets, twenty defence budgets, eighteen welfare budgets, and five UK State pension budgets planned for the UK’s 2014 fiscal year. The evasion total is the same size as the entire public sector pension fund (itself a disgrace of illegal embezzlement) and only slightly smaller than Britain’s total national debt.

It is a mind-boggling 70% of United Kingdom GDP.

But here’s the final brass-necked irony: stand by for an attempt by the Global Looters to use this tax evasion reality as the excuse for stealing the savings of everyone with over £100,000 in a bank account that isn’t offshore….and represents the life-savings of a law-abiding taxpayer.

Principal articles reproduced / referenced above:

- http://www.golemxiv.co.uk/2013/04/making-the-truth-illegal-revisited/

- http://hat4uk.wordpress.com/2013/04/08/the-evaders-british-banks-control-enough-tax-evasion-to-almost-pay-off-our-national-debt-at-a-stroke/

- http://charleshughsmith.blogspot.co.uk/2013/04/the-real-cyprus-template-one-youre-not.html

UK: Money-movers play catch-me-if-you-can

The global financial crisis is also a local issue for the UK, dubbed the 'global capital of money-laundering' in a Private Eye magazine investigation by Richard Brooks (August 2012).

The role of the financial sector in Britain ballooned in the years before the breakdown: this 2011 report by the Bank of England (pdf) shows that its annual growth was 6%, twice that of the economy as a whole.

That's why we need it. But why does the rest of the world need it to be in London?

In part the answer is that, as David Malone explains below, our system is particularly good at handling money without asking too many awkward questions. Shell companies make it hard to track down who is running businesses.

Moreover, unless money is definitely proved to have come from illegal activities, the authorities are unable to treat money transfers as criminal "money-laundering". Malone's only censored post to date, from which he quotes sections here, was a detailed investigation for Reuters into alleged money-laundering in Cyprus; but his original piece fell foul of that (perfectly logical, of course) lack-of-predicate-crime rule.

In this context it's worth remembering that the UK is also known as the "libel capital of the world", with potentially big payouts for plaintiffs if the defendant cannot prove his allegations (up to three years ago, it could get much worse than a civil court case: there was such a thing as criminal libel, punishable by imprisonment - this was what caused Private Eye's then editor Richard Ingrams to throw in the sponge when Sir James Goldsmith pursued him in July 1976).

And now, following the Leveson inquiry into abuses by mainstream journalists, bloggers may find themselves at risk of high financial penalties, without having the legal and financial resources of the conventional Press to help defend themselves.

I also reproduce here a piece by France-based blogger John Ward, reporting on the vast quantities of cash held in offshore banks that might (if captured onshore) otherwise contribute up to a trillion pounds to the UK economy.

In a digitised world, capital can zip around the globe far faster than leaden-footed regulators and tax authorities. Cyber-money is also very useful for dodging attempts by local banks to grab it to shore up their reserves, as we are seeing in Cyprus - and this article on Charles Hugh Smith's site goes further, implying that EU banks may have influenced a delay in the European Central Bank's enforcement action against the island, to allow them time to extract most of their cash before the shutters went down.

Finally, delay can help bosses as well as the banks they run: there is much noise being made at the moment about "examining powers to take legal action" against three directors of HBOS who were on watch when billions were lost by their company; but the Financial Services Authority has a strict time limit of three years to take disciplinary action against individuals, and that deadline has come and gone. A cynic might wonder why exactly the FSA missed it, but the fact remains that we have to obey the law as it stands, so I don't expect any retrospective ruling against these people, who are far from the only ones to have (allegedly) overseen significant losses in the banking sector.

My sincere thanks to David Malone and John Ward for permission to reproduce their posts.

________________________________________________

Making the Truth Illegal – revisited

“Making the Truth Illegal” is the title of the only post I have ever removed from this blog.

I removed it because I was threatened with legal consequences if I did not. (Plus, I would like to add, some of the way I had written the blog post was stupid and could have hurt someone who had helped me.)

The post concerned an article I had written for Reuters which they decided they could not/would not publish. Reuters pulled the article because they and I had been threatened, by a major European Bank, with legal consequences if they did not. The title of the article was “Cyprus, Magnitsky and the truth about Money Laundering.”

Although I cannot publish the article I can show you how it began and tell you how it is, that the truth it contained was made illegal.

The article began:

Money laundering is the life blood of organized crime. Without it crime would simply not pay. But who does the laundering? The easy and obvious answer is criminals. But that is completely wrong and is at the root of our inability to stop it.