Last Thursday, the people spoke, and what they said was this:

"We want a proper government. A strong, honest government that works for us.

"One that doesn't make stupid compromises just to keep in power. One that works for what most people want.

"A job. A better chance for our children than we had. Money to pay bills, to pay for a bit of fun, to save for when we're old. Decent education and healthcare, keep crime down, protect us from enemies domestic and foreign.

"Apart from those things, if you have a wonderful vision of the future, write a novel or make a movie. We don't want revolutionaries, Puritans of any religion or none, national separatists or the European Brotherhood of Man.

"Now, get on with it. And stop lying and fiddling the expenses."

So, why not a coalition of Conservative and Labour? Up to the 70s/80s, when the country was tearing itself into pieces because of economic crisis after Bretton-Woods collapsed, there was quite a lot of consensus between the two sides.

If Clegg can talk face to face with Brown and his back can talk to Cameron, maybe Lab and Con could discover that they have more in common with each other than they have with the LibDems. (For a start, neither of them thinks that a white flag is a robust defence in a nuclear world.)

With 424 seats, a Lab/Con government of national unity would have a majority of 198. Enough to ignore special pleading and political blackmail from Alex Salmond, Ieuan Wyn Jones and the Northern Irish factions; enough to ignore the babel of grand reformist schemes from the LibDems; and enough left over to ignore episodes of up to half a hundred backbenchers at a time temporarily crossing the floor of the House in a hissy fit about their own pet projects.

We face enough challenges to occupy a full-length Parliament, challenges that all serious politicians would wish to solve together.

So, why not? Out of 650 Members of Parliament, is is really impossible to find 326 that would cooperate for the national good?

There might even be some Liberal Democrats willing to help.

Monday, May 10, 2010

Exports and loans

The way Charles Hugh Smith explains it, it seems that Germany is the China of Europe.

Goldman Sachs - "financial terrorists"

Max Keiser claims GS quite deliberately caused last week's 1,000-point drop on the Dow, just to remind the US Government who's master.

Who is Nick Clegg?

For someone propelled into the political spotlight, Nick Clegg is an oddity. Unlike Blair, who treated attention like a sunlamp, Clegg seems oddly uncomfortable - not just with his situation, but with himself. Many photographs show his head tilted forward slightly, as though manfully resisting the urge to look down; after making key points in the pseudo-Presidential TV debates, his eyes would flick to the floor; and if you cover the top part of the face, look at the mouth - all wrong, somehow.

Like Baroness Ashton (Europe's first High Representative For Foreign Affairs), he looks like a natural loser who's won the Lottery, but is going to have it all taken away from him at some point. True, both are winners in a sense now, but the European setup that gave Clegg his first major political position as an MEP (after some years of service with the European Commission), and Ashton (I think) her last, has carefully arranged matters so that you have a big group of nonentities in a mock-Parliament, while all the real power is vested in the Council of Ministers. In short, these two are perfect stooges and the light of publicity does not flatter them.

It is, I think, significant that Clegg's postgraduate learning included a spell at the College of Europe in Bruges, an outfit whose purpose was described by postwar Euro-idealist Henri Brugmans as "to train an elite of young executives for Europe." I read that as a sort of McKinsey for pliable idiots. Other British Isles alumni include former Tory MP Nigel Forman, Neil Kinnock's sprog Stephen, LD stiff Simon Hughes, ScotNat MEP Alyn Smith (how a nationalist and a federalist? explain!), and Irish-born ex-Gen Sec of the European Commission David O'Sullivan.

Now, for a short spell, Clegg's playing with the big boys, and they're going to have his marbles and the bag they came in. Nothing will persuade any Labour or Conservative leader to agree to PR, a system that would guarantee perpetually recurring crises of governance like the present one. The Single Transferable Vote as some describe it (preference ranking within conflated groupings of constituencies) would tend to a squeeze of minor parties in favour of the largest two; tweaked versions of the Alternative Vote are obvious political fudges designed to include cosy dunroamin deadend spots for loyal, clapped-out Party hacks or political chessmen in search of a sinecure (I believe AV+ was Roy Jenkins' brainchild, if so the connection doesn't surprise).

The best that can be hoped for by LibDems is constituency-level Alternative Vote, and it's by no means certain that AV would prove greatly helpful to them. In habitually Conservative seats, many LD voters may be slightly disenchanted Tories who will return to the fold if they feel threatened by some Lib-Lab combination; in Labour seats, the same situation in reverse; and some Liberal seats could be threatened by odd tactical combinations of their enemies, questioning LD policies on e.g. nuclear disarmament, Eurointegration, immigration.

The best that can be hoped for by Nick Clegg, I think, is to do a Blair: sell out to powerful interests who will springboard him into some position less vulnerable to the people's franchise. Perhaps the reward for his long service to Europe will be a seat on the European Commission (maybe he still speaks to David O'Sullivan and friends - see above). He, and ultimately his descendants, will be accepted into that modern equivalent of the Hapsburg dynasty that is the nascent power support structure of the EU.

Or maybe he'll stand his ground, and watch his party get whittled away back down to six seats, a fate David Steel vividly remembers.

Like Baroness Ashton (Europe's first High Representative For Foreign Affairs), he looks like a natural loser who's won the Lottery, but is going to have it all taken away from him at some point. True, both are winners in a sense now, but the European setup that gave Clegg his first major political position as an MEP (after some years of service with the European Commission), and Ashton (I think) her last, has carefully arranged matters so that you have a big group of nonentities in a mock-Parliament, while all the real power is vested in the Council of Ministers. In short, these two are perfect stooges and the light of publicity does not flatter them.

It is, I think, significant that Clegg's postgraduate learning included a spell at the College of Europe in Bruges, an outfit whose purpose was described by postwar Euro-idealist Henri Brugmans as "to train an elite of young executives for Europe." I read that as a sort of McKinsey for pliable idiots. Other British Isles alumni include former Tory MP Nigel Forman, Neil Kinnock's sprog Stephen, LD stiff Simon Hughes, ScotNat MEP Alyn Smith (how a nationalist and a federalist? explain!), and Irish-born ex-Gen Sec of the European Commission David O'Sullivan.

Now, for a short spell, Clegg's playing with the big boys, and they're going to have his marbles and the bag they came in. Nothing will persuade any Labour or Conservative leader to agree to PR, a system that would guarantee perpetually recurring crises of governance like the present one. The Single Transferable Vote as some describe it (preference ranking within conflated groupings of constituencies) would tend to a squeeze of minor parties in favour of the largest two; tweaked versions of the Alternative Vote are obvious political fudges designed to include cosy dunroamin deadend spots for loyal, clapped-out Party hacks or political chessmen in search of a sinecure (I believe AV+ was Roy Jenkins' brainchild, if so the connection doesn't surprise).

The best that can be hoped for by LibDems is constituency-level Alternative Vote, and it's by no means certain that AV would prove greatly helpful to them. In habitually Conservative seats, many LD voters may be slightly disenchanted Tories who will return to the fold if they feel threatened by some Lib-Lab combination; in Labour seats, the same situation in reverse; and some Liberal seats could be threatened by odd tactical combinations of their enemies, questioning LD policies on e.g. nuclear disarmament, Eurointegration, immigration.

The best that can be hoped for by Nick Clegg, I think, is to do a Blair: sell out to powerful interests who will springboard him into some position less vulnerable to the people's franchise. Perhaps the reward for his long service to Europe will be a seat on the European Commission (maybe he still speaks to David O'Sullivan and friends - see above). He, and ultimately his descendants, will be accepted into that modern equivalent of the Hapsburg dynasty that is the nascent power support structure of the EU.

Or maybe he'll stand his ground, and watch his party get whittled away back down to six seats, a fate David Steel vividly remembers.

Sunday, May 09, 2010

It's the Tories who fear voting reform - and the LibDems who should fear it

Watching William Hague and Danny Alexander speak to the Press outside the Cabinet Office, it was obvious to me how shtum they were keeping about electoral reform.

There's a good reason, I think: a truly representative voting system would probably mean there would never again be a Conservative government.

Let's say that we had some form of nationwide Alternative Vote. The votes for the very small parties would likely pass on about equally between the Tories and Labour - maybe a little more Right than Left. The key would be how the LD votes would split, and I'd guess it would be not less than 80:20 in favour of a left of centre Labour party. Even now, that would mean an outright majority for Labour.

Just as American politics is basically a choice between two sides that from a British perspective seem right-wing, British politics under "fair voting" would be a choice between two left of centre parties, for to have any hope of power the Tories would have to share even more in "progressive" political values than they have done in many years. Indeed David Cameron's electoral sales pitch already reflects this, to some extent.

But if we go down this road, then we might be better off with a truly Presidential system, because the two candidates could be assessed not only on general policy direction but on character. We're mutating into a leader-driven system as it is, thanks in major part to the mass media, especially TV. At least a national direct election for the country's leadership would winnow out callow, jumped-up backroom boffins like Milliband - or so I'd hope.

It's much more difficult to judge what would happen if we retained the territorial constituency system but adopted the Alternative Vote. I don't have the time, the psephological database or the specialised computer programs and theoretical assumptions to study 650 constituencies and play out the permutations. But this is what Gordon Brown is rumoured to be offering the LibDems, and forming a coalition to get AV may be better than going for PR with the Tories and eventually ending up with a FrankenLeft party that swallows the LibDems whole.

If Clegg and co. come to a deal with the Conservatives without electoral reform, I think it'll be the end for Clegg; if they get PR, it could be the end of the third force in British politics. Yet Labour haven't enough to go on, even with the LibDems' support.

Perhaps the upshot will be another General Election, even sooner than the 12 - 18 months people are talking about. And that could fracture both Labour and the Conservatives, as Peter Hitchens has long suggested and wished.

We do live in interesting times.

There's a good reason, I think: a truly representative voting system would probably mean there would never again be a Conservative government.

Let's say that we had some form of nationwide Alternative Vote. The votes for the very small parties would likely pass on about equally between the Tories and Labour - maybe a little more Right than Left. The key would be how the LD votes would split, and I'd guess it would be not less than 80:20 in favour of a left of centre Labour party. Even now, that would mean an outright majority for Labour.

Just as American politics is basically a choice between two sides that from a British perspective seem right-wing, British politics under "fair voting" would be a choice between two left of centre parties, for to have any hope of power the Tories would have to share even more in "progressive" political values than they have done in many years. Indeed David Cameron's electoral sales pitch already reflects this, to some extent.

But if we go down this road, then we might be better off with a truly Presidential system, because the two candidates could be assessed not only on general policy direction but on character. We're mutating into a leader-driven system as it is, thanks in major part to the mass media, especially TV. At least a national direct election for the country's leadership would winnow out callow, jumped-up backroom boffins like Milliband - or so I'd hope.

It's much more difficult to judge what would happen if we retained the territorial constituency system but adopted the Alternative Vote. I don't have the time, the psephological database or the specialised computer programs and theoretical assumptions to study 650 constituencies and play out the permutations. But this is what Gordon Brown is rumoured to be offering the LibDems, and forming a coalition to get AV may be better than going for PR with the Tories and eventually ending up with a FrankenLeft party that swallows the LibDems whole.

If Clegg and co. come to a deal with the Conservatives without electoral reform, I think it'll be the end for Clegg; if they get PR, it could be the end of the third force in British politics. Yet Labour haven't enough to go on, even with the LibDems' support.

Perhaps the upshot will be another General Election, even sooner than the 12 - 18 months people are talking about. And that could fracture both Labour and the Conservatives, as Peter Hitchens has long suggested and wished.

We do live in interesting times.

Should we fear proportional representation?

There are vested interests opposing electoral reform. One of their subtler strategies is to propose pantomime-horse variants on the Single Transferable Vote (AV+ etc) , I suspect to muddy the waters sufficiently so that people will say change isn't worth it.

The fact is, under the present system 95.5% of the seats went to the three major parties; if seats had been allocated in proportion to votes cast, the top three would still have had 88.3%. Between them, quite enough to vote down everyone else.

Yes, some of the "wrong types" (e.g. the BNP) would have got a voice in Parliament; but actually, the fourth biggest party would have been UKIP, with 20 seats - and under a different system, UKIP might have gained switch-support from those who voted BNP because of concerns about national sovereignty and the economic and social effects of relatively uncontrolled (yet disproportionately locally concentrated) immigration; leaving the race-haters fuming in an even tinier corner. Some other minorities would have even fewer seats than they have now, and we'd have some fresh voices on the benches. Is it really necessary to uphold a flawed existing arrangement merely because it gags mouths that might offend us?

Another objection is that the LibDems would be the kingmakers, the masters of the seesaw. Not necessarily: how many of those who voted LD tactically last week, would have voted directly for Labour or Conservative if they had thought their vote would count as much as anyone else's?

PR would break the link between an MP and his/her constituency, say some. Yet it seems that so much voting is simply for the rosette, and we have just seen a General Election campaign fought on presidential terms, without our having the right to elect the President.

In 26 years, I've been doorstepped twice by Parliamentary candidates - both them in the last month, because thanks to boundary changes I'm now in a marginal constituency. Before then, I had two Labour bods in succession, each obviously taking the view that they needn't make any effort because the seat was usually bombproof under First-Past-The-Post. (I have a sneaking - perhaps totally unfair - suspicion that the boundary was altered partly to shut out Respect, who were threatening to do well in this part of Birmingham.)

I'm not a fan of the party list kind of PR, because that takes away the voters' right to reject individuals they consider unsuitable - but the Single Transferable Vote (STV) would give a voice to us voiceless people, and we might be heard from time to time among the hubbub.

I give below a list of seats actually won, and another showing how brutally simple national PR would have allocated them; what it can't show is how votes would have been cast if people knew every vote counted absolutely equally, nationwide; or how the picture would change if you could express 2nd and 3rd choices in constituency-based STV voting.

The fact is, under the present system 95.5% of the seats went to the three major parties; if seats had been allocated in proportion to votes cast, the top three would still have had 88.3%. Between them, quite enough to vote down everyone else.

Yes, some of the "wrong types" (e.g. the BNP) would have got a voice in Parliament; but actually, the fourth biggest party would have been UKIP, with 20 seats - and under a different system, UKIP might have gained switch-support from those who voted BNP because of concerns about national sovereignty and the economic and social effects of relatively uncontrolled (yet disproportionately locally concentrated) immigration; leaving the race-haters fuming in an even tinier corner. Some other minorities would have even fewer seats than they have now, and we'd have some fresh voices on the benches. Is it really necessary to uphold a flawed existing arrangement merely because it gags mouths that might offend us?

Another objection is that the LibDems would be the kingmakers, the masters of the seesaw. Not necessarily: how many of those who voted LD tactically last week, would have voted directly for Labour or Conservative if they had thought their vote would count as much as anyone else's?

PR would break the link between an MP and his/her constituency, say some. Yet it seems that so much voting is simply for the rosette, and we have just seen a General Election campaign fought on presidential terms, without our having the right to elect the President.

In 26 years, I've been doorstepped twice by Parliamentary candidates - both them in the last month, because thanks to boundary changes I'm now in a marginal constituency. Before then, I had two Labour bods in succession, each obviously taking the view that they needn't make any effort because the seat was usually bombproof under First-Past-The-Post. (I have a sneaking - perhaps totally unfair - suspicion that the boundary was altered partly to shut out Respect, who were threatening to do well in this part of Birmingham.)

I'm not a fan of the party list kind of PR, because that takes away the voters' right to reject individuals they consider unsuitable - but the Single Transferable Vote (STV) would give a voice to us voiceless people, and we might be heard from time to time among the hubbub.

I give below a list of seats actually won, and another showing how brutally simple national PR would have allocated them; what it can't show is how votes would have been cast if people knew every vote counted absolutely equally, nationwide; or how the picture would change if you could express 2nd and 3rd choices in constituency-based STV voting.

Saturday, May 08, 2010

Will Cameron support the breakup of the UK?

Scotland has 59 seats in the British Parliament, of which 41 voted Labour in this week's General Election, and only one voted Conservative.

David Cameron proposes to reduce the number of MPs by 10%, i.e. 65 out of 650.

On the GE results, giving Scotland her "independence" (within the European Empire, of course) would mean the Conservatives having 305 seats out of 591, a 9-seat majority. The DUP in Northern Ireland could add the support of another 8 seats, at a price.

Or the Conservatives could drop the Unionist part of their party's title altogether, and cut Northern Ireland and Wales "free" as well. Only 9 of the 117 constituencies in the quasi-Celtic countries voted Tory. This would leave an English-only Parliament (eagerly desired by some on the interwebs) of 533 seats, 297 of them Conservative - a 30-seat majority for the Tories, even on the latest disappointing showing. Central Office could then simply relocate to Buckingham Palace to begin a thousand-year reign.

The political temptation to assist the European fragmentarian project must be immense.

And then there is the financial side. Comparing revenue and expenditure, how much do Northern Ireland, Scotland and Wales cost the British government?

David Cameron proposes to reduce the number of MPs by 10%, i.e. 65 out of 650.

On the GE results, giving Scotland her "independence" (within the European Empire, of course) would mean the Conservatives having 305 seats out of 591, a 9-seat majority. The DUP in Northern Ireland could add the support of another 8 seats, at a price.

Or the Conservatives could drop the Unionist part of their party's title altogether, and cut Northern Ireland and Wales "free" as well. Only 9 of the 117 constituencies in the quasi-Celtic countries voted Tory. This would leave an English-only Parliament (eagerly desired by some on the interwebs) of 533 seats, 297 of them Conservative - a 30-seat majority for the Tories, even on the latest disappointing showing. Central Office could then simply relocate to Buckingham Palace to begin a thousand-year reign.

The political temptation to assist the European fragmentarian project must be immense.

And then there is the financial side. Comparing revenue and expenditure, how much do Northern Ireland, Scotland and Wales cost the British government?

Stockmarkets: don't join the crooked card game

UPDATE:

It may be worse than at first we thought. The savage drop could have been (this says it was) deliberately engineered by Goldman Sachs as a shot across the bows, warning legislators not to mess with them!

_______________________________________

Nathan Martin makes the point that Thursday's 1,000-point drop on the Dow Jones Index unveiled the truth: the current high valuation of the market is because of money thrown into it by banks and hedge funds, not ordinary private investors. The drop happened when the insiders stopped trading.

The question is, how much longer can the illusion be maintained? Why are they doing it? Is it to tempt investors back into the market so that they can suffer all the financial losses when the banks pull out?

This is an age when cynicism comes easily.

It may be worse than at first we thought. The savage drop could have been (this says it was) deliberately engineered by Goldman Sachs as a shot across the bows, warning legislators not to mess with them!

_______________________________________

Nathan Martin makes the point that Thursday's 1,000-point drop on the Dow Jones Index unveiled the truth: the current high valuation of the market is because of money thrown into it by banks and hedge funds, not ordinary private investors. The drop happened when the insiders stopped trading.

The question is, how much longer can the illusion be maintained? Why are they doing it? Is it to tempt investors back into the market so that they can suffer all the financial losses when the banks pull out?

This is an age when cynicism comes easily.

Thursday, May 06, 2010

Right, it's UKIP then

When even a major political party is encouraging us to vote tactically, you know the system is cracking. Good.

It's not about Britain's economic difficulties: disaster is pretty much assured whoever gets in. But we've been poor before; so what? Liberty is harder to recover than wealth.

First we have to get the power back from Europe, then we have to get it back from our venal and treacherous domestic politicians.

There is no system that will make people good and happy; that revolution is in the heart. The bureaucratic reification of good intentions becomes the slave of its own power and protocols.

We need some freedom to act. I shall do my tiny, practically insignificant bit to clear a little space so that those who have good will can practise it.

A vote for UKIP, this "contemptible little army", may encourage those elsewhere with a better chance - perhaps in the South West - to keep pushing back, to resist the Black Hole.

UPDATE

Some discussion of the deficiencies of Proportional Representation on Hatfeld Girl's site. I've submitted the following comment:

PR no, Alternative Vote (what I used to know as the Single Transferable Vote) yes. The latter is basically the same as First Past The Post but with AV the post stands at 50% of votes cast.

I don't see how this would necessarily lead to hung Parliaments, coalitions and weirdo fringe MPs, indeed I think it would help avoid them. You'd get more of a fight for the centre ground, but you'd get an MP that was more likely to have reflected some level of your choice so you wouldn't feel disenfranchised. And I think you'd get more examination of policies to determine 2nd and 3rd choices.

Turnout this time in the national elections was reportedly 65%, less than at any time in the 75 years from 1922-1997. And that's after market panic, credit crunch, the near destruction of the banking system, general hoo-ha, fedupness with Brown (how much of the vote depends on emotional spasm?) and Sam Cam's bump.

The present system is effectively useless and corrupt, which is why it will continue. I expect David Cameron to offer a Royal Commission and then do nothing, since the current arrangement suits Tweedledum and Tweedledee.

It's not about Britain's economic difficulties: disaster is pretty much assured whoever gets in. But we've been poor before; so what? Liberty is harder to recover than wealth.

First we have to get the power back from Europe, then we have to get it back from our venal and treacherous domestic politicians.

There is no system that will make people good and happy; that revolution is in the heart. The bureaucratic reification of good intentions becomes the slave of its own power and protocols.

We need some freedom to act. I shall do my tiny, practically insignificant bit to clear a little space so that those who have good will can practise it.

A vote for UKIP, this "contemptible little army", may encourage those elsewhere with a better chance - perhaps in the South West - to keep pushing back, to resist the Black Hole.

UPDATE

Some discussion of the deficiencies of Proportional Representation on Hatfeld Girl's site. I've submitted the following comment:

PR no, Alternative Vote (what I used to know as the Single Transferable Vote) yes. The latter is basically the same as First Past The Post but with AV the post stands at 50% of votes cast.

I don't see how this would necessarily lead to hung Parliaments, coalitions and weirdo fringe MPs, indeed I think it would help avoid them. You'd get more of a fight for the centre ground, but you'd get an MP that was more likely to have reflected some level of your choice so you wouldn't feel disenfranchised. And I think you'd get more examination of policies to determine 2nd and 3rd choices.

Turnout this time in the national elections was reportedly 65%, less than at any time in the 75 years from 1922-1997. And that's after market panic, credit crunch, the near destruction of the banking system, general hoo-ha, fedupness with Brown (how much of the vote depends on emotional spasm?) and Sam Cam's bump.

The present system is effectively useless and corrupt, which is why it will continue. I expect David Cameron to offer a Royal Commission and then do nothing, since the current arrangement suits Tweedledum and Tweedledee.

Tuesday, May 04, 2010

It's not the ship, it's the tide that matters

The great problem for investors in today's environment is that there is no return on short-term, safe assets yet the higher risk levels on longer-term, higher return assets are too uncomfortable for most people...

John Mauldin

The only winning strategy "for the long haul" is to be fully committed to the market when it is rising and economic fundamentals support that direction, and to be entirely out at all other times.

Karl Denninger

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

The centerpiece of our own strategy [...] is understanding liquidity flows. They are the single most important force driving investment markets both up and down. Contracting liquidity caused the crash in 2008-2009 and dramatically expanding liquidity since March 2009 has triggered one of the greatest bull markets in U.S. history. The next bear market will also be driven, at some point, by a contraction in liquidity flows. However, as long as the great reflation is doing its work, that day can be postponed. [...] The music is playing again. People are back out on the dance floor. But, if the great reflation is as artificial as we believe, then this is still musical chairs. When the music stops, there won't be a chair for everyone, just like the last time.

John Mauldin

The only winning strategy "for the long haul" is to be fully committed to the market when it is rising and economic fundamentals support that direction, and to be entirely out at all other times.

Karl Denninger

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

The current investment conundrum, in a nutshell

The great problem for investors in today's environment is that there is no return on short-term, safe assets yet the higher risk levels on longer-term, higher return assets are too uncomfortable for most people...

John Mauldin

The only winning strategy "for the long haul" is to be fully committed to the market when it is rising and economic fundamentals support that direction, and to be entirely out at all other times.

Karl Denninger

The centerpiece of our own strategy [...] is understanding liquidity flows. They are the single most important force driving investment markets both up and down. Contracting liquidity caused the crash in 2008-2009 and dramatically expanding liquidity since March 2009 has triggered one of the greatest bull markets in U.S. history. The next bear market will also be driven, at some point, by a contraction in liquidity flows. However, as long as the great reflation is doing its work, that day can be postponed. [...] The music is playing again. People are back out on the dance floor. But, if the great reflation is as artificial as we believe, then this is still musical chairs. When the music stops, there won't be a chair for everyone, just like the last time.

John Mauldin

The only winning strategy "for the long haul" is to be fully committed to the market when it is rising and economic fundamentals support that direction, and to be entirely out at all other times.

Karl Denninger

Monday, May 03, 2010

Could Norway be a safe haven?

A few weeks ago, I looked at national credit ratings and Norway was the clear leader. So I wondered how strong the Norwegian Kroner might be if other currencies began to unravel.

Could the past give us a clue? No doubt those of you who have access to more sophisticated financial software and databases can do better - this is just a starting point for discussion.

Here's the 10-year history (O&A data, interbank rate, annually on 3rd May each year, rebased to 100% against the Kroner in 2000).

And in graphic form:

And in graphic form:

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Could the past give us a clue? No doubt those of you who have access to more sophisticated financial software and databases can do better - this is just a starting point for discussion.

Here's the 10-year history (O&A data, interbank rate, annually on 3rd May each year, rebased to 100% against the Kroner in 2000).

And in graphic form:

And in graphic form:

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Should we go for Norwegian cash, bonds and shares?

A few weeks ago, I looked at national credit ratings and Norway was the clear leader. So I wondered how strong the Norwegian Kroner might be if other currencies began to unravel.

Could the past give us a clue? No doubt those of you who have access to more sophisticated financial software and databases can do better - this is just a starting point for discussion.

Here's the 10-year history (O&A data, interbank rate, annually on 3rd May each year, rebased to 100% against the Kroner in 2000).

And in graphic form:

Could the past give us a clue? No doubt those of you who have access to more sophisticated financial software and databases can do better - this is just a starting point for discussion.

Here's the 10-year history (O&A data, interbank rate, annually on 3rd May each year, rebased to 100% against the Kroner in 2000).

And in graphic form:Sunday, May 02, 2010

A house is a home, not an investment

A Nationwide Building Society press release (29 April) says the average house is now worth £167,802. Prices rose by 10.5% in the past year. Perhaps we should be in a hurry to buy again.

All the previous three sentences are misleading.

First, “average” is hard to define. According to nethouseprices.com, in 2010 a semi-detached house in Sheldon, Birmingham sold for £10,000 while another in Harborne changed hands for £470,000. During the same period in London, semis sold for between £130,000 and £10 million (93 other semis went for over £1 million).

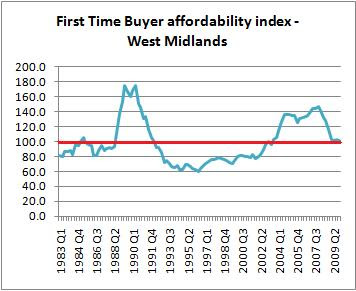

Second, as the Nationwide report admits, house prices are still 10% below the peak reached in October 2007. The good news is that they are more affordable now: using the Nationwide’s online database, here is a graph of first-time buyer mortgage costs as a proportion of average take-home pay in the West Midlands (the most typical region in the country):

Third, we face a long period of economic difficulty, with the threat of high unemployment. A falling pound could result in higher food and energy costs, and if the UK’s credit rating drops interest rates could rise. Each of these factors could easily depress property prices.

You have to live somewhere, but don’t think of it as a money-maker.

All the previous three sentences are misleading.

First, “average” is hard to define. According to nethouseprices.com, in 2010 a semi-detached house in Sheldon, Birmingham sold for £10,000 while another in Harborne changed hands for £470,000. During the same period in London, semis sold for between £130,000 and £10 million (93 other semis went for over £1 million).

Second, as the Nationwide report admits, house prices are still 10% below the peak reached in October 2007. The good news is that they are more affordable now: using the Nationwide’s online database, here is a graph of first-time buyer mortgage costs as a proportion of average take-home pay in the West Midlands (the most typical region in the country):

The bad news is, the graph is affected by record low interest rates; the actual amount borrowed is much higher than it used to be. As late as 1998, new mortgages averaged £60,000; now, according to thisismoney.co.uk (25 February), the average new loan is £140,000 – 5 ½ times the median wage, far above the long-term trend (3 ½ times earnings).

Third, we face a long period of economic difficulty, with the threat of high unemployment. A falling pound could result in higher food and energy costs, and if the UK’s credit rating drops interest rates could rise. Each of these factors could easily depress property prices.

You have to live somewhere, but don’t think of it as a money-maker.

Friday, April 30, 2010

More on houses

A Nationwide Building Society press release (29 April) says the average house is now worth £167,802. Prices rose by 10.5% in the past year. Perhaps we should be in a hurry to buy again.

All the previous three sentences are misleading.

First, “average” is hard to define. According to nethouseprices.com, in 2010 a semi-detached house in Sheldon, Birmingham sold for £10,000 while another in Harborne changed hands for £470,000. During the same period in London, semis sold for between £130,000 and £10 million (93 other semis went for over £1 million).

Second, as the Nationwide report admits, house prices are still 10% below the peak reached in October 2007. The good news is that they are more affordable now: using the Nationwide’s online database, here is a graph of first-time buyer mortgage costs as a proportion of average take-home pay in the West Midlands (the most typical region in the country):

Third, we face a long period of economic difficulty, with the threat of high unemployment. A falling pound could result in higher food and energy costs, and if the UK’s credit rating drops interest rates could rise. Each of these factors could easily depress property prices.

You have to live somewhere, but don’t think of it as a money-maker.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

All the previous three sentences are misleading.

First, “average” is hard to define. According to nethouseprices.com, in 2010 a semi-detached house in Sheldon, Birmingham sold for £10,000 while another in Harborne changed hands for £470,000. During the same period in London, semis sold for between £130,000 and £10 million (93 other semis went for over £1 million).

Second, as the Nationwide report admits, house prices are still 10% below the peak reached in October 2007. The good news is that they are more affordable now: using the Nationwide’s online database, here is a graph of first-time buyer mortgage costs as a proportion of average take-home pay in the West Midlands (the most typical region in the country):

The bad news is, the graph is affected by record low interest rates; the actual amount borrowed is much higher than it used to be. As late as 1998, new mortgages averaged £60,000; now, according to thisismoney.co.uk (25 February), the average new loan is £140,000 – 5 ½ times the median wage, far above the long-term trend (3 ½ times earnings).

Third, we face a long period of economic difficulty, with the threat of high unemployment. A falling pound could result in higher food and energy costs, and if the UK’s credit rating drops interest rates could rise. Each of these factors could easily depress property prices.

You have to live somewhere, but don’t think of it as a money-maker.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Tuesday, April 27, 2010

Heads down

May I draw your attention to an interview with Dr Marc Faber on CNBC on 21st April (see videos on sidebar in Broad Oak Blog)?

Dr Faber is a highly respected commentator and his predictions of economic disaster, though cheerily delivered, are perfectly serious (he has a European way of giving bad news with an ironic smile).

He believes - and has done for a long time - that governments will try to inflate their way out of the long-developing overspending mess, and that eventually all "fiat" money (currencies not backed by anything that restricts the growth of the money supply) will become worthless. Then there will be a crash of epochal proportions, and the social consequences will be very painful (which is why his website is called GloomBoomDoom.com).

As he says in this interview, his view is that gold and silver are not to be considered as commodities like oil and corn, but as a form of money that governments cannot multiply as they do with their sovereign currencies. He advises (please remember that I cannot advise you here on this blog) investors to build up their holdings of physical gold and silver - "physical" because there is much speculation in this market and many times more in contracts than can be actually delivered. After that, maybe some investment in precious metal exploration companies.

Given Dr Faber's view of the real practical consequences of economic collapse, I think it is not irrelevant that he lives in Chiang Mai, northern Thailand, an area that can provide the needs of life locally and that is close to several international borders.

We may still have time - Dr Faber thinks that with continued monetary inflation, we could still see markets go up for quite a period; but from all that he says, and all that I have thought (and said) for years now, we appear to be facing a prolonged period of high volatility and the danger of sudden and savage reverses in valuations. Until inflation takes off, it can be good to hold cash; but if Dr Faber is correct, ultimately cash will be the worst possible investment.

I would also say that before considering your investment portfolio, there may be other issues to resolve - where you should live, what work you should do, what skills you should acquire, security precautions you should take, emergency provisions you should stock up with. Even if disaster does not strike with full force, big rises in fuel costs would transform the conditions of our daily life.

It is curious that we are now expected to be exercised by climate change issues, yet the media have yet to come to grips with our economic climate. It is still not generally known that the good old days (as remembered) of the Conservative boom in the 1980s (and mid-90s) was because of excessive bank lending, which caused both housing and the stockmarket to become heavily overvalued. This process of inflating the economy until it pops (as it must, one day, but who knows exactly when), has being going on for decades.

I've tried to get the message across to the public; perhaps I should spend my time quietly advising my clients, instead. Anyhow, I've told you, now.

Dr Faber is a highly respected commentator and his predictions of economic disaster, though cheerily delivered, are perfectly serious (he has a European way of giving bad news with an ironic smile).

He believes - and has done for a long time - that governments will try to inflate their way out of the long-developing overspending mess, and that eventually all "fiat" money (currencies not backed by anything that restricts the growth of the money supply) will become worthless. Then there will be a crash of epochal proportions, and the social consequences will be very painful (which is why his website is called GloomBoomDoom.com).

As he says in this interview, his view is that gold and silver are not to be considered as commodities like oil and corn, but as a form of money that governments cannot multiply as they do with their sovereign currencies. He advises (please remember that I cannot advise you here on this blog) investors to build up their holdings of physical gold and silver - "physical" because there is much speculation in this market and many times more in contracts than can be actually delivered. After that, maybe some investment in precious metal exploration companies.

Given Dr Faber's view of the real practical consequences of economic collapse, I think it is not irrelevant that he lives in Chiang Mai, northern Thailand, an area that can provide the needs of life locally and that is close to several international borders.

We may still have time - Dr Faber thinks that with continued monetary inflation, we could still see markets go up for quite a period; but from all that he says, and all that I have thought (and said) for years now, we appear to be facing a prolonged period of high volatility and the danger of sudden and savage reverses in valuations. Until inflation takes off, it can be good to hold cash; but if Dr Faber is correct, ultimately cash will be the worst possible investment.

I would also say that before considering your investment portfolio, there may be other issues to resolve - where you should live, what work you should do, what skills you should acquire, security precautions you should take, emergency provisions you should stock up with. Even if disaster does not strike with full force, big rises in fuel costs would transform the conditions of our daily life.

It is curious that we are now expected to be exercised by climate change issues, yet the media have yet to come to grips with our economic climate. It is still not generally known that the good old days (as remembered) of the Conservative boom in the 1980s (and mid-90s) was because of excessive bank lending, which caused both housing and the stockmarket to become heavily overvalued. This process of inflating the economy until it pops (as it must, one day, but who knows exactly when), has being going on for decades.

I've tried to get the message across to the public; perhaps I should spend my time quietly advising my clients, instead. Anyhow, I've told you, now.

Very uncertain times

May I draw your attention to an interview with Dr Marc Faber on CNBC on 21st April (see videos on sidebar)?

Dr Faber is a highly respected commentator and his predictions of economic disaster, though cheerily delivered, are perfectly serious (he has a European way of giving bad news with an ironic smile).

He believes - and has done for a long time - that governments will try to inflate their way out of the long-developing overspending mess, and that eventually all "fiat" money (currencies not backed by anything that restricts the growth of the money supply) will become worthless. Then there will be a crash of epochal proportions, and the social consequences will be very painful (which is why his website is called GloomBoomDoom.com).

As he says in this interview, his view is that gold and silver are not to be considered as commodities like oil and corn, but as a form of money that governments cannot multiply as they do with their sovereign currencies. He advises (please remember that I cannot advise you here on this blog) investors to build up their holdings of physical gold and silver - "physical" because there is much speculation in this market and many times more in contracts than can be actually delivered. After that, maybe some investment in precious metal exploration companies.

Given Dr Faber's view of the real practical consequences of economic collapse, I think it is not irrelevant that he lives in Chiang Mai, northern Thailand, an area that can provide the needs of life locally and that is close to several international borders.

We may still have time - Dr Faber thinks that with continued monetary inflation, we could still see markets go up for quite a period; but from all that he says, and all that I have thought (and said) for years now, we appear to be facing a prolonged period of high volatility and the danger of sudden and savage reverses in valuations. Until inflation takes off, it can be good to hold cash; but if Dr Faber is correct, ultimately cash will be the worst possible investment.

I would also say that before considering your investment portfolio, there may be other issues to resolve - where you should live, what work you should do, what skills you should acquire, security precautions you should take, emergency provisions you should stock up with. Even if disaster does not strike with full force, big rises in fuel costs would transform the conditions of our daily life.

It is curious that we are now expected to be exercised by climate change issues, yet the media have yet to come to grips with our economic climate. It is still not generally known that the good old days (as remembered) of the Conservative boom in the 1980s (and mid-90s) was because of excessive bank lending, which caused both housing and the stockmarket to become heavily overvalued. This process of inflating the economy until it pops (as it must, one day, but who knows exactly when), has being going on for decades.

I've tried to get the message across to the public; perhaps I should spend my time quietly advising my clients, instead. Anyhow, I've told you, now.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Dr Faber is a highly respected commentator and his predictions of economic disaster, though cheerily delivered, are perfectly serious (he has a European way of giving bad news with an ironic smile).

He believes - and has done for a long time - that governments will try to inflate their way out of the long-developing overspending mess, and that eventually all "fiat" money (currencies not backed by anything that restricts the growth of the money supply) will become worthless. Then there will be a crash of epochal proportions, and the social consequences will be very painful (which is why his website is called GloomBoomDoom.com).

As he says in this interview, his view is that gold and silver are not to be considered as commodities like oil and corn, but as a form of money that governments cannot multiply as they do with their sovereign currencies. He advises (please remember that I cannot advise you here on this blog) investors to build up their holdings of physical gold and silver - "physical" because there is much speculation in this market and many times more in contracts than can be actually delivered. After that, maybe some investment in precious metal exploration companies.

Given Dr Faber's view of the real practical consequences of economic collapse, I think it is not irrelevant that he lives in Chiang Mai, northern Thailand, an area that can provide the needs of life locally and that is close to several international borders.

We may still have time - Dr Faber thinks that with continued monetary inflation, we could still see markets go up for quite a period; but from all that he says, and all that I have thought (and said) for years now, we appear to be facing a prolonged period of high volatility and the danger of sudden and savage reverses in valuations. Until inflation takes off, it can be good to hold cash; but if Dr Faber is correct, ultimately cash will be the worst possible investment.

I would also say that before considering your investment portfolio, there may be other issues to resolve - where you should live, what work you should do, what skills you should acquire, security precautions you should take, emergency provisions you should stock up with. Even if disaster does not strike with full force, big rises in fuel costs would transform the conditions of our daily life.

It is curious that we are now expected to be exercised by climate change issues, yet the media have yet to come to grips with our economic climate. It is still not generally known that the good old days (as remembered) of the Conservative boom in the 1980s (and mid-90s) was because of excessive bank lending, which caused both housing and the stockmarket to become heavily overvalued. This process of inflating the economy until it pops (as it must, one day, but who knows exactly when), has being going on for decades.

I've tried to get the message across to the public; perhaps I should spend my time quietly advising my clients, instead. Anyhow, I've told you, now.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Very uncertain times

May I draw your attention to an interview with Dr Marc Faber on CNBC on 21st April (see videos on sidebar)?

Dr Faber is a highly respected commentator and his predictions of economic disaster, though cheerily delivered, are perfectly serious (he has a European way of giving bad news with an ironic smile).

He believes - and has done for a long time - that governments will try to inflate their way out of the long-developing overspending mess, and that eventually all "fiat" money (currencies not backed by anything that restricts the growth of the money supply) will become worthless. Then there will be a crash of epochal proportions, and the social consequences will be very painful (which is why his website is called GloomBoomDoom.com).

As he says in this interview, his view is that gold and silver are not to be considered as commodities like oil and corn, but as a form of money that governments cannot multiply as they do with their sovereign currencies. He advises (please remember that I cannot advise you here on this blog) investors to build up their holdings of physical gold and silver - "physical" because there is much speculation in this market and many times more in contracts than can be actually delivered. After that, maybe some investment in precious metal exploration companies.

Given Dr Faber's view of the real practical consequences of economic collapse, I think it is not irrelevant that he lives in Chiang Mai, northern Thailand, an area that can provide the needs of life locally and that is close to several international borders.

We may still have time - Dr Faber thinks that with continued monetary inflation, we could still see markets go up for quite a period; but from all that he says, and all that I have thought (and said) for years now, we appear to be facing a prolonged period of high volatility and the danger of sudden and savage reverses in valuations. Until inflation takes off, it can be good to hold cash; but if Dr Faber is correct, ultimately cash will be the worst possible investment.

I would also say that before considering your investment portfolio, there may be other issues to resolve - where you should live, what work you should do, what skills you should acquire, security precautions you should take, emergency provisions you should stock up with. Even if disaster does not strike with full force, big rises in fuel costs would transform the conditions of our daily life.

It is curious that we are now expected to be exercised by climate change issues, yet the media have yet to come to grips with our economic climate. It is still not generally known that the good old days (as remembered) of the Conservative boom in the 1980s (and mid-90s) was because of excessive bank lending, which caused both housing and the stockmarket to become heavily overvalued. This process of inflating the economy until it pops (as it must, one day, but who knows exactly when), has being going on for decades.

I've tried to get the message across to the public; perhaps I should spend my time quietly advising my clients, instead. Anyhow, I've told you, now.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Dr Faber is a highly respected commentator and his predictions of economic disaster, though cheerily delivered, are perfectly serious (he has a European way of giving bad news with an ironic smile).

He believes - and has done for a long time - that governments will try to inflate their way out of the long-developing overspending mess, and that eventually all "fiat" money (currencies not backed by anything that restricts the growth of the money supply) will become worthless. Then there will be a crash of epochal proportions, and the social consequences will be very painful (which is why his website is called GloomBoomDoom.com).

As he says in this interview, his view is that gold and silver are not to be considered as commodities like oil and corn, but as a form of money that governments cannot multiply as they do with their sovereign currencies. He advises (please remember that I cannot advise you here on this blog) investors to build up their holdings of physical gold and silver - "physical" because there is much speculation in this market and many times more in contracts than can be actually delivered. After that, maybe some investment in precious metal exploration companies.

Given Dr Faber's view of the real practical consequences of economic collapse, I think it is not irrelevant that he lives in Chiang Mai, northern Thailand, an area that can provide the needs of life locally and that is close to several international borders.

We may still have time - Dr Faber thinks that with continued monetary inflation, we could still see markets go up for quite a period; but from all that he says, and all that I have thought (and said) for years now, we appear to be facing a prolonged period of high volatility and the danger of sudden and savage reverses in valuations. Until inflation takes off, it can be good to hold cash; but if Dr Faber is correct, ultimately cash will be the worst possible investment.

I would also say that before considering your investment portfolio, there may be other issues to resolve - where you should live, what work you should do, what skills you should acquire, security precautions you should take, emergency provisions you should stock up with. Even if disaster does not strike with full force, big rises in fuel costs would transform the conditions of our daily life.

It is curious that we are now expected to be exercised by climate change issues, yet the media have yet to come to grips with our economic climate. It is still not generally known that the good old days (as remembered) of the Conservative boom in the 1980s (and mid-90s) was because of excessive bank lending, which caused both housing and the stockmarket to become heavily overvalued. This process of inflating the economy until it pops (as it must, one day, but who knows exactly when), has being going on for decades.

I've tried to get the message across to the public; perhaps I should spend my time quietly advising my clients, instead. Anyhow, I've told you, now.

DISCLAIMER: Nothing here should be taken as personal advice, financial or otherwise. No liability is accepted for third-party content, whether incorporated in or linked to this blog.

Subscribe to:

Posts (Atom)