Showing posts with label deflation. Show all posts

Showing posts with label deflation. Show all posts

Sunday, November 08, 2009

Tuesday, August 25, 2009

Debt, unemployment and escape routes

Interesting observation by Steve Keen: unemployment correlates closely with the amount that debt contributes to demand in the economy.

Let me try to reason out the consequences, however inexpertly.

So, as everyone scrambles to cut spending and get out of debt, unemployment will soar. Since there is a great deal of international trade, the hit will be felt internationally.

Then government finances will come properly unravelled, especially in countries that have generous social welfare provisions. Worldwide, sovereign states will look for anyone who has real money to lend.

This should result in higher interest rates, but that would make the cost of debt, and its sustainability, extremely difficult, both for states and for corporations (and the burden on the latter will tend to result in even more unemployment and more claimants on the government). A rise in rates would also hit holders of long-term government debt, which may be one of the reasons the Chinese have been swapping that for shorter-dated Treasuries. A collapse in bonds will affect the capital value of pensions and investments, oh dear.

Another way out is default on debt. But who will be hit by that? Not just foreigners, but our pensions and managed investment funds.

A third way, which given that we have history to learn from doesn't seem likely, is the true hyperinflation approach. Germany in 1923, Hungary, Argentina, Zimbabwe... do you really see this happening here?

Then there's the downgrading of debt, with corresponding falls in the traded value of the currency. We've seen some of that - what, 20% off the pound? - so maybe there's more to come from that direction. Except other countries may follow suit. In 1922, if you were a far-sighted German, I suppose you might have sold marks and bought dollars; what currency would you buy now?

Or there's "more of the same" again - talking up the economy and pumping in cash until you spend because you daren't leave it to rot in the savings account.

Which way will it go? Where will it all end?

Let me try to reason out the consequences, however inexpertly.

So, as everyone scrambles to cut spending and get out of debt, unemployment will soar. Since there is a great deal of international trade, the hit will be felt internationally.

Then government finances will come properly unravelled, especially in countries that have generous social welfare provisions. Worldwide, sovereign states will look for anyone who has real money to lend.

This should result in higher interest rates, but that would make the cost of debt, and its sustainability, extremely difficult, both for states and for corporations (and the burden on the latter will tend to result in even more unemployment and more claimants on the government). A rise in rates would also hit holders of long-term government debt, which may be one of the reasons the Chinese have been swapping that for shorter-dated Treasuries. A collapse in bonds will affect the capital value of pensions and investments, oh dear.

Another way out is default on debt. But who will be hit by that? Not just foreigners, but our pensions and managed investment funds.

A third way, which given that we have history to learn from doesn't seem likely, is the true hyperinflation approach. Germany in 1923, Hungary, Argentina, Zimbabwe... do you really see this happening here?

Then there's the downgrading of debt, with corresponding falls in the traded value of the currency. We've seen some of that - what, 20% off the pound? - so maybe there's more to come from that direction. Except other countries may follow suit. In 1922, if you were a far-sighted German, I suppose you might have sold marks and bought dollars; what currency would you buy now?

Or there's "more of the same" again - talking up the economy and pumping in cash until you spend because you daren't leave it to rot in the savings account.

Which way will it go? Where will it all end?

Monday, August 24, 2009

Credit contraction is outpacing monetary stimulus

"... the Eurozone, the UK, Japan, and essentially every county on the planet is all attempting some sort of stimulus plan or other. This is bound to cause a major distortion at some point, as no country has anything remotely close to an exit strategy for this. What kind of distortion and when cannot be certain because we are indeed in uncharted territory, worldwide."

- Mish.

The more I read around, the more uncertain I become. All I have is my instinct, that things are out of control and we're being told fairy stories to lull us.

Mish's argument is that "The credit bubble that just popped exceeded that preceding the great depression, not just in the US but worldwide. Thus, it is unrealistic to expect the deflationary bust to be anything other than the biggest bust in history. Those looking for hyperinflation or even strong inflation in light of the above, are simply looking at the wrong model." If he's right, it's cash is king, for a long time to come.

- Mish.

The more I read around, the more uncertain I become. All I have is my instinct, that things are out of control and we're being told fairy stories to lull us.

Mish's argument is that "The credit bubble that just popped exceeded that preceding the great depression, not just in the US but worldwide. Thus, it is unrealistic to expect the deflationary bust to be anything other than the biggest bust in history. Those looking for hyperinflation or even strong inflation in light of the above, are simply looking at the wrong model." If he's right, it's cash is king, for a long time to come.

Monday, August 03, 2009

The dam may break after all

Jesse reports on another big bank about to go down; Karl Denninger speculates that the FDIC is colluding in the cover-up of widespread bank insolvency, so it isn't forced to step in when there's no money left in its kitty - for the only thing after that is load more of the losses onto Uncle Sam, i.e. the taxpayers and all our descendants.

If the pressure continues, maybe we'll end up doing what some have said all along needs to be done: step back and let the losers fail, to flush all the rubbish out of the system. Well, all the rubbish that Uncle Sam hasn't already been forced to eat.

More difficult for us in the UK, though, since we don't have lots of second-tier banks ready to take over the loan books. Maybe Barclays and HSBC will profit enormously? Or how about the Bank of China, now moving into the British market?

Thursday, July 02, 2009

Dow 400?

Tim Iacono quotes the Elliott Wave people:

For the record, EWFF also shows a "grand supercycle," beginning in January 2000 and ending at 400. Yes, that was FOUR HUNDRED.

And I thought I was being Eeyorish at 2,000.

For the record, EWFF also shows a "grand supercycle," beginning in January 2000 and ending at 400. Yes, that was FOUR HUNDRED.

And I thought I was being Eeyorish at 2,000.

Tuesday, June 23, 2009

Inflation, not deflation

Jesse today, maintaining that inflation can indeed happen...

Our own view is that a serious stagflation with further devaluation of the US dollar as it is replaced as the world's reserve currency is very likely, after a period of slackening demand and high unemployment. A military conflict is also a probable outcome as countries often go to war when they fail at peace.

Tips?

From my own readings in this area, the people who tended to survive the Weimar stagflation the best were those who:

1. Owned independent supplies of essentials including food and shelter and were reasonably self-sufficient.

2. Had savings in foreign currencies that were backed by gold such as the US dollar and the Swiss Franc

3. Possessed precious metals

4. Belonged to a trade union and/or had essential skills or government position which guaranteed a wage

5. Were invested in foreign equity markets, and even in the domestic German stock market for a time

Our own view is that a serious stagflation with further devaluation of the US dollar as it is replaced as the world's reserve currency is very likely, after a period of slackening demand and high unemployment. A military conflict is also a probable outcome as countries often go to war when they fail at peace.

Tips?

From my own readings in this area, the people who tended to survive the Weimar stagflation the best were those who:

1. Owned independent supplies of essentials including food and shelter and were reasonably self-sufficient.

2. Had savings in foreign currencies that were backed by gold such as the US dollar and the Swiss Franc

3. Possessed precious metals

4. Belonged to a trade union and/or had essential skills or government position which guaranteed a wage

5. Were invested in foreign equity markets, and even in the domestic German stock market for a time

Sunday, April 19, 2009

The deflationary bust

Looking around "Financial Sense"...

Professor Antal E. Fekete revisits his deflationary theory: we have passed a crucial point in debt accumulation. From now (actually, from 2006, he says) onward, the more politicians attempt to stimulate it with debt, the faster the economy will shrink. Gold, the machine's "governor" that set limits to debt, was decoupled from the system a century ago - it got in the way of war financing.

Stephen Tetreault says if there's a rise in stocks, sell: "I do not see a positive bullish catalyst in the making as we head into the earnings sector other than a potential short squeeze, relief rally that should which should be sold into." He notes that deflation means those that can, are paying down debt, but also lenders are widening the margins between the interest they pay and the interest they charge, which gives further impetus to deflation.

Tony Allison says, sooner or later energy is going to cost more. He's thinking about the right point to speculate, the rest of us should consider the effect of higher energy costs on family budgets, and therefore on how reduced disposable income will be allocated.

Captain Hook foresees a time when "the public finally gives up the ghost on stocks in general, correspondingly they will fully embrace the likelihood of deflation, which will trigger a temporary collapse in commodity prices, led by their paper representations." He thinks this will be the time when physical gold will win; I wonder whether that is so, when most of us are so dependent on an electronic system. We're not farmers, selling corn and cattle to each other; the machine cannot be allowed to stop. That's why I think there will be, for a time, a switch to currency inflation; then perhaps a rerun of the early Eighties, as someone public-spirited in public life takes unpopular action to prevent the dive into the abyss.

For E. M. Forster's extraordinarily accurate vision of the future, written in 1909, please click the last link above. Telephone, TV, a populace paralysed by lethargy and wealth in its bedrooms...

Professor Antal E. Fekete revisits his deflationary theory: we have passed a crucial point in debt accumulation. From now (actually, from 2006, he says) onward, the more politicians attempt to stimulate it with debt, the faster the economy will shrink. Gold, the machine's "governor" that set limits to debt, was decoupled from the system a century ago - it got in the way of war financing.

Stephen Tetreault says if there's a rise in stocks, sell: "I do not see a positive bullish catalyst in the making as we head into the earnings sector other than a potential short squeeze, relief rally that should which should be sold into." He notes that deflation means those that can, are paying down debt, but also lenders are widening the margins between the interest they pay and the interest they charge, which gives further impetus to deflation.

Tony Allison says, sooner or later energy is going to cost more. He's thinking about the right point to speculate, the rest of us should consider the effect of higher energy costs on family budgets, and therefore on how reduced disposable income will be allocated.

Captain Hook foresees a time when "the public finally gives up the ghost on stocks in general, correspondingly they will fully embrace the likelihood of deflation, which will trigger a temporary collapse in commodity prices, led by their paper representations." He thinks this will be the time when physical gold will win; I wonder whether that is so, when most of us are so dependent on an electronic system. We're not farmers, selling corn and cattle to each other; the machine cannot be allowed to stop. That's why I think there will be, for a time, a switch to currency inflation; then perhaps a rerun of the early Eighties, as someone public-spirited in public life takes unpopular action to prevent the dive into the abyss.

For E. M. Forster's extraordinarily accurate vision of the future, written in 1909, please click the last link above. Telephone, TV, a populace paralysed by lethargy and wealth in its bedrooms...

Friday, April 10, 2009

More on bonds, and an alternative view

Antal E. Fekete is a professor of money and banking in San Francisco (such a beautiful place, too). He has a pet thesis about the bond market, which is that every time interest rates halve, effectively the capital value of (older) bonds doubles, to match the yield on new bonds.

So as long as we expect the government to try to stimulate the economy by lowering interest rates, there's a killing to be made in the bond market. Theoretically this could go on forever, even in a low-interest environment - the logic holds if rates go from 0.25% to 0.125% - provided the Treasury doesn't simply go straight to zero interest, of course.

Anyhow, his latest essay says that the monetary stimulus will simply be used to settle debts, since debt gets more and more burdensome in a deflationary depression; and settling debt instead of making and buying more stuff, continues to drive deflation. In this enviroment, few businesses will want to take on more debt (certain and fixed) in the hope of increasing their profits (far from certain, and very variable). On a national level, and following the ideas of Melchior Palyi, he now sees every extra dollar of debt as causing GDP to contract.

Therefore, valuations of most assets will continue to decline - except for bonds, which are now the focus for speculators. To this extent, he agrees with Marc Faber (cited in the previous post): we now have a bubble in government bonds.

But something will go bang. The real world shies from the inevitable conclusions of mathematical models. I think it will come as a crisis in foreigners' confidence in the dollar - there will be a reluctance to buy US Treasuries (we've already seen failed sales of government bonds in the UK recently, and when the next one succeeded, that's because it was a sale of index-linked bonds). Even now, the Chinese have switched from Agencies (debts of States and municipal organisations) to Federal debt, and within the latter, from longer-dated bonds to shorter-dated ones. If government debt was an aircraft, the Chinese would be the passenger insisting on a seat next the emergency exit near the tailplane.

To use a different analogy (one I've used before), drawn from the Lord of the Rings, the rally in the dollar and the flight to US Treasury debt seems to me like the retreat to the fortress of Helm's Deep: a last-ditch defence, doomed to be overwhelmed. Can we see a little figure about to save the day by dropping the Ring of Power into the lava in Mount Doom? We can hope; but you don't make survival plans based purely on optimism.

I therefore expect a transition from deflationary depression to inflationary depression, at some point. Perhaps a sort of 1974 stockmarket moment: an apparent turnaround, which when analysed can be shown to continue the real loss of value for some years. Only when national budgets are brought under strict control, will there be the environment for true growth. I don't see a willingness to tackle that, on either side the Atlantic, so disaster will have to be our teacher.

Thursday, March 19, 2009

Hold dollars?

Karl Denninger argues that the failed stimulus will lead to accelerating deflation in the US. His prediction is that demand for the dollar will soar and other currencies will collapse instead. He thinks this will hit US exports and the economy will be crippled, so Americans need to hold in-the-hand folding money - lots of it, maybe a year or two's basic expenses! - away from the bank.

He may be on the wrong medication - the current state of the world's finances is a great impetus towards paranoia and depression; but if he's even half right, we need to start making those quiet, regular cashpoint withdrawals and (for non-Americans) visiting the bureau de change. And not living in the city.

He may be on the wrong medication - the current state of the world's finances is a great impetus towards paranoia and depression; but if he's even half right, we need to start making those quiet, regular cashpoint withdrawals and (for non-Americans) visiting the bureau de change. And not living in the city.

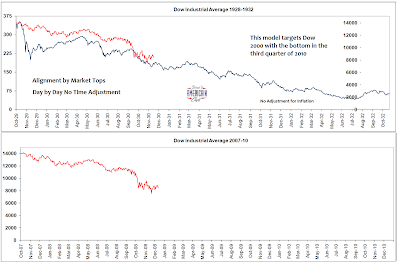

Saturday, February 28, 2009

"Bang on target!"

"Bang on target!"Wednesday, February 11, 2009

Deflation, inflation, distress

The Contrarian Investor gives a lucid explanation of the potential consequences of deflation.

In Australia (as in the UK, as I think I showed here), the nation owes more money than it has in savings, so it depends on foreign investment.

If interest rates fall, foreign capital will go away to where it can earn more. This reduces the demand for our currency and makes it cheaper. So goods we sell to foreigners get cheaper, and things they sell us get more expensive. They buy more from us, we buy less from them (or they have to cut their prices so we can afford their stuff). More money comes into our economy; all well again.

Except...

What can they take? In Australia, there are mineral deposits the Chinese will want, thinks the Contrarian Investor. Here in the UK, maybe some remaining profitable businesses and valuable technical expertise, maybe patents and secret technologies. And it's not only the Chinese that have been lending us their surpluses. We have other creditors.

Then, as the laden carts depart and the keys of the mansion are handed to the new owners, the decayed gentry become vagrants and vagabonds.

Unless we are too dangerous to dun. Perhaps America is; can we be so? And what if our creditors are not certain of our might? Uncertainty can trigger inappropriate actions. There is a Chinese saying, I believe: fear a weak enemy. Catastrophe can be avoided, but unless our leaders are tough with us now, we will learn a harder way later.

But if the master has become poor, what of his servants?

What if, like me, you're not one whose power and social status protects him from the worst effects? Do you believe that democratic societies can do the right thing? If not, this is a time for individuals to make their own quiet plans and preparations.

In Australia (as in the UK, as I think I showed here), the nation owes more money than it has in savings, so it depends on foreign investment.

If interest rates fall, foreign capital will go away to where it can earn more. This reduces the demand for our currency and makes it cheaper. So goods we sell to foreigners get cheaper, and things they sell us get more expensive. They buy more from us, we buy less from them (or they have to cut their prices so we can afford their stuff). More money comes into our economy; all well again.

Except...

- What if , thanks to decades of spending lots without earning much (and borrowing the difference), we no longer make things foreigners want?

- What if they sell us things we can't do without, and won't cut their prices?

What can they take? In Australia, there are mineral deposits the Chinese will want, thinks the Contrarian Investor. Here in the UK, maybe some remaining profitable businesses and valuable technical expertise, maybe patents and secret technologies. And it's not only the Chinese that have been lending us their surpluses. We have other creditors.

Then, as the laden carts depart and the keys of the mansion are handed to the new owners, the decayed gentry become vagrants and vagabonds.

Unless we are too dangerous to dun. Perhaps America is; can we be so? And what if our creditors are not certain of our might? Uncertainty can trigger inappropriate actions. There is a Chinese saying, I believe: fear a weak enemy. Catastrophe can be avoided, but unless our leaders are tough with us now, we will learn a harder way later.

But if the master has become poor, what of his servants?

What if, like me, you're not one whose power and social status protects him from the worst effects? Do you believe that democratic societies can do the right thing? If not, this is a time for individuals to make their own quiet plans and preparations.

Sunday, February 08, 2009

Denninger: deflation

Belatedly, I refer you to Karl Denninger's end-year review and forecast. He sees continuing deflation, and makes a number of other plausible and worrisome predictions - scroll to the end of his post for the horrid gallery of prognostications.

In short:

...rallies are to be sold, cash is to be raised and prudence is to be practiced in your own personal financial affairs. Don't get creative in all things finance, get stingy and prudent. Your personal financial survival could well depend on it.

So instead of staring at the low interest on your cash balance, think of the real capital appreciation of your money as measured by what big-ticket items it will buy. And for once, the government can't easily tax your capital gain.

You may also want to hold more cash away from a bank ("Round #2 of severe bank instability gets served up on us in the second half of 2009").

And maybe diversify your currency holdings:

The Dollar will not collapse. This is not because we're in great shape or will truly recover, it is because the rest of the world is in worse shape than we are... The rest of the world is literally on the precipice of a full-on collapse. European banks are more-levered and less-transparent than our banks as just one example... I see the potential for the pound and euro to both reach par with the dollar.

I think Denninger on the one hand, and Faber/Janszen on the other, may both be correct. It's a matter of timing - deflation now, debasement of the currency later. Because nominal debt gets relatively bigger as assets and incomes decline in value, something will have to give.

In short:

...rallies are to be sold, cash is to be raised and prudence is to be practiced in your own personal financial affairs. Don't get creative in all things finance, get stingy and prudent. Your personal financial survival could well depend on it.

So instead of staring at the low interest on your cash balance, think of the real capital appreciation of your money as measured by what big-ticket items it will buy. And for once, the government can't easily tax your capital gain.

You may also want to hold more cash away from a bank ("Round #2 of severe bank instability gets served up on us in the second half of 2009").

And maybe diversify your currency holdings:

The Dollar will not collapse. This is not because we're in great shape or will truly recover, it is because the rest of the world is in worse shape than we are... The rest of the world is literally on the precipice of a full-on collapse. European banks are more-levered and less-transparent than our banks as just one example... I see the potential for the pound and euro to both reach par with the dollar.

I think Denninger on the one hand, and Faber/Janszen on the other, may both be correct. It's a matter of timing - deflation now, debasement of the currency later. Because nominal debt gets relatively bigger as assets and incomes decline in value, something will have to give.

Monday, February 02, 2009

IN- vs. DE- and an upcoming opportunity

Jesse echoes my hunch: deflation now, inflation soon-ish, with high interest rates for a bit. At that latter point, get your annuity and /or bonds, and benefits as rates subside. A guess, but it's comforting to see wise owls coming to the same conclusion.

You now have our investment gameplan for what is likely to be the rest of Jesse's life.

No, no "Jesse"; live long and prosper.

You now have our investment gameplan for what is likely to be the rest of Jesse's life.

No, no "Jesse"; live long and prosper.

Wednesday, January 21, 2009

Newsflash

All is well: the Dow has just sailed (well, snailed) back through the 8,000 barrier. But what's this? Brad Setser doesn't know what to think about China's role in US debt financing.

Here he thinks that a downturn in China's production will be panic their already-prudent populace into saving even more money, and

they'll also import less, which will screw our deflation down even tighter:

Bottom line: A big fall in activity in China will tend to drive China’s trade surplus up. It thus would tend to increase — not reduce — China’s (net) purchases of foreign assets. Someone in China will still buying foreign assets — and likely providing indirect support for the Treasury market — even if it is not China’s central bank. A big fall in activity also means less Chinese demand for the world’s products — as well as less Chinese demand for China’s products, which frees up capacity to export. That adds to the deflationary forces in the world economy.

... and here he worries about the switch from long-term purchases of Treasuries, to ones with short maturity dates:

At the same time, it is risky to finance a large external deficit with short-term debt. Even for the US. If the US deficit starts to head back up again — as, for example, the effect of the recent fall in oil prices wears off and a large fiscal stimulus in the US stimulates the world economy — without a shift in the composition of inflows, there would be cause for concern.

It's said that Charles Colson, an aide to President Nixon, had this motto framed in his office: "When you've got them by the balls, their hearts and minds will follow." Funny, until you're on the receiving end.

Here he thinks that a downturn in China's production will be panic their already-prudent populace into saving even more money, and

they'll also import less, which will screw our deflation down even tighter:

Bottom line: A big fall in activity in China will tend to drive China’s trade surplus up. It thus would tend to increase — not reduce — China’s (net) purchases of foreign assets. Someone in China will still buying foreign assets — and likely providing indirect support for the Treasury market — even if it is not China’s central bank. A big fall in activity also means less Chinese demand for the world’s products — as well as less Chinese demand for China’s products, which frees up capacity to export. That adds to the deflationary forces in the world economy.

... and here he worries about the switch from long-term purchases of Treasuries, to ones with short maturity dates:

At the same time, it is risky to finance a large external deficit with short-term debt. Even for the US. If the US deficit starts to head back up again — as, for example, the effect of the recent fall in oil prices wears off and a large fiscal stimulus in the US stimulates the world economy — without a shift in the composition of inflows, there would be cause for concern.

It's said that Charles Colson, an aide to President Nixon, had this motto framed in his office: "When you've got them by the balls, their hearts and minds will follow." Funny, until you're on the receiving end.

Friday, January 16, 2009

Taxation is inflationary, not deflationary

I've often wondered whether that's the case - now the Mogambo Guru says so. If taxes cut our take-home income, we insist on more income to make up for it.

Thursday, January 15, 2009

Under the floorboards

The Contrarian Investor reports that the Chinese will have difficulty stimulating demand within their own country, if the Western buying spree stalls. Poverty, compulsive saving by those who can, and stacks of cash hidden under corrupt officials' floors mean that helicopters filled with banknotes won't tempt the population to get out and blow their wads.

Saturday, January 10, 2009

The next wave of bailouts

It's not just the banks that are short of money. Many US States and local authorities are also suffering financial problems, and this is affecting the trade in their bonds, i.e. their borrowings on the money market. ("What are bonds, exactly?" - see here.)

Michael Panzner reports that municipal bonds ("munis") offer a better yield than US Treasury bonds, but the difference is still not enough to pay for the extra risk. Professional investors are short-selling "munis". i.e. betting that they will fall in price. A steep fall may indicate imminent bankruptcy, and some say this is on the way for many authorities, as Mish reported at the end of December.

So, what will happen when the US Government is seen to be buying everybody's bad debts?

People (even here in the UK, where we tend to wait patiently for our wise rulers to solve all) are beginning to worry about inflation, and are thinking about investing again. An article in Elliott Wave International warns us not to be panicked into parting with our cash, and reminds us:

... there are periods when inflation does erode the value of cash. I mean, look at the seven years leading up to the October 2007 peak in U.S. stocks: big gains in the stock indexes, while inflation was eroding cash. No way did cash do as well as stocks during that time.

Right?

Wrong. Cash outperformed stocks in the seven years leading up to the 2007 stock market high. That outperformance has only increased in the time since.

Since this is the view I took and communicated to clients in the 1990s, you will understand that I didn't make much money as a financial adviser. But it was certainly good advice, even if it was based on strongly-felt intuition rather than macroeconomic analysis.

Not that analysis guarantees results, in a world where the money game's rules are changed at will by politicians with a host of agendas that they don't share with us ordinary types. But my current guess is that the stockmarket will halve again in the next few years, when compared with the cost of living.

Michael Panzner reports that municipal bonds ("munis") offer a better yield than US Treasury bonds, but the difference is still not enough to pay for the extra risk. Professional investors are short-selling "munis". i.e. betting that they will fall in price. A steep fall may indicate imminent bankruptcy, and some say this is on the way for many authorities, as Mish reported at the end of December.

So, what will happen when the US Government is seen to be buying everybody's bad debts?

People (even here in the UK, where we tend to wait patiently for our wise rulers to solve all) are beginning to worry about inflation, and are thinking about investing again. An article in Elliott Wave International warns us not to be panicked into parting with our cash, and reminds us:

... there are periods when inflation does erode the value of cash. I mean, look at the seven years leading up to the October 2007 peak in U.S. stocks: big gains in the stock indexes, while inflation was eroding cash. No way did cash do as well as stocks during that time.

Right?

Wrong. Cash outperformed stocks in the seven years leading up to the 2007 stock market high. That outperformance has only increased in the time since.

Since this is the view I took and communicated to clients in the 1990s, you will understand that I didn't make much money as a financial adviser. But it was certainly good advice, even if it was based on strongly-felt intuition rather than macroeconomic analysis.

Not that analysis guarantees results, in a world where the money game's rules are changed at will by politicians with a host of agendas that they don't share with us ordinary types. But my current guess is that the stockmarket will halve again in the next few years, when compared with the cost of living.

Monday, January 05, 2009

Deflation, low interest rates and the poor old saver

The British Government claims it wants to do more for the saver. Actually, it's already done a lot: the Daily Telegraph reports that the Halifax estimates house prices fell by 16.2% in 2008. Putting it another way, someone holding cash in a shoebox has made 19.33% tax-free, measured in house price terms; or 32.22% gross for a 40% taxpayer.

And that's a point: the government doesn't tax you on the gains of deflation. But I'm sure they're keen to rectify that: normal inflation will be resumed as soon as possible.

{kind=link}

And that's a point: the government doesn't tax you on the gains of deflation. But I'm sure they're keen to rectify that: normal inflation will be resumed as soon as possible.

Saturday, December 13, 2008

Two cheers for deflation

A pattern is emerging.

Jörg Guido Hülsmann, on the Mises site, says deflation does not ruin the economy as a whole, but destroys the parasites who exploit the potential of fiat money. Parasites like (alleged) Ponzi-style fraudster Madoff and his clients, who deserve what they've now got, Mish judges.

Jesse says that "financial capitalism" seeks to use the money system to develop a dictatorial New World Order, and will be defeated when the dollar fails as the world's reserve currency.

Brad Setser wonders whether the dollar has reached its zenith; which implies that it may begin heading for its nadir.

Desperately holding back the inevitable is the US Federal Reserve, says Jim from San Marcos, who (although the Fed is refusing FOI requests) suspects that its $2 trillion in emergency loans is equally divided between support for banks, credit cards and the stockmarket. (I wondered what was being used as the robust cloth on the Dow's trampoline, and covert official support may be the answer.)

As I argued yesterday, the straightest path would be to destroy fraudulent, oppressive debt and those who introduced it into the system. For so many families, the bank is the fattest kid at their kitchen table, and nobody knows who invited him.

For a long time, I've been recasting financial issues as issues of power and freedom. If Jesse is correct, we are reaching a turning point in the battle. I hope we may soon say, as Churchill said of El Alamein, "A bright gleam has caught the helmets of our soldiers and warmed and cheered all our hearts." It would be worth the blood, toil, tears and sweat.

Jörg Guido Hülsmann, on the Mises site, says deflation does not ruin the economy as a whole, but destroys the parasites who exploit the potential of fiat money. Parasites like (alleged) Ponzi-style fraudster Madoff and his clients, who deserve what they've now got, Mish judges.

Jesse says that "financial capitalism" seeks to use the money system to develop a dictatorial New World Order, and will be defeated when the dollar fails as the world's reserve currency.

Brad Setser wonders whether the dollar has reached its zenith; which implies that it may begin heading for its nadir.

Desperately holding back the inevitable is the US Federal Reserve, says Jim from San Marcos, who (although the Fed is refusing FOI requests) suspects that its $2 trillion in emergency loans is equally divided between support for banks, credit cards and the stockmarket. (I wondered what was being used as the robust cloth on the Dow's trampoline, and covert official support may be the answer.)

As I argued yesterday, the straightest path would be to destroy fraudulent, oppressive debt and those who introduced it into the system. For so many families, the bank is the fattest kid at their kitchen table, and nobody knows who invited him.

For a long time, I've been recasting financial issues as issues of power and freedom. If Jesse is correct, we are reaching a turning point in the battle. I hope we may soon say, as Churchill said of El Alamein, "A bright gleam has caught the helmets of our soldiers and warmed and cheered all our hearts." It would be worth the blood, toil, tears and sweat.

Friday, December 12, 2008

History repeats itself - because it's getting old

Jesse extrapolates the Dow and sees it heading for 2,000 points:

As my select and distinguished readers now know, I'm an optimist (by the standards of unfolding reality), and I say, not so. I say, maybe 4,000 - 5,000, adjusted for CPI.

The comparison I'd urge is not with 1929-32 (stockmarket deflation exacerbated by monetary strictness), but (in inflation-adjusted terms) from January 1966 to July 1982: stockmarket deflation prolonged and partially disguised by monetary inflation; I said so here and here, last month. I maintain that the bear market began in 2000 and the symptoms were masked by the terrible extra debts taken on over the last 8 years. Karl Denninger showed us yesterday that these debts account for all the US GDP growth since the New Millennium, plus $9 trillion.

The debate about inflation and deflation continues, though from a British perspective we've seen practically the whole of the rest of the world become one-third more expensive in sterling terms, in only five months. However, Einstein's theory of relativity rejects the notion of any absolute standpoint, and we shall see next year which other currencies mimic sterling's vertiginous fall.

In these shifting times, it becomes very hard to discern real value; but however hard to measure, it exists nevertheless. There is a real bill to pay for our excesses, and I think 2008 will be seen in retrospect as the year that the global balance of power underwent a sudden tectonic shift, from West to East. Yes, the East will suffer for a while, too, but it has long been acquiring the means of production and developing its local markets, and will emerge from the crisis ahead of us.

And there will also - must also - be an intergenerational shift of power, within our Western societies. As globalization continues and real income and real house prices decline, existing debt (set in fixed terms) will become proportionately greater, until the weight is too great to bear; and the worst of it falls on the people who are also struggling to raise families and save something, however inadequate, for their old age. They cannot be crucified in this way. How can savers be taxed at 20% and workers at (effectively, on margin, including National Insurance) 40%? Real wealth must flow from one to the other, just to maintain civilization. I think either savings must be taxed more (perhaps the removal of tax exemption for some savings products will be the start), or inflation must come, though I don't know how long the play will go on before the denouement.

We did have another option, and I was only half-joking: cancel mortgage debts on a massive scale (bankrupting the banks and the bankers, and serve them right). Then, with our productive populace relatively unencumbered, it would be possible to let Western wages and prices fall to much nearer Eastern levels, and we could begin to compete.

As my select and distinguished readers now know, I'm an optimist (by the standards of unfolding reality), and I say, not so. I say, maybe 4,000 - 5,000, adjusted for CPI.

The comparison I'd urge is not with 1929-32 (stockmarket deflation exacerbated by monetary strictness), but (in inflation-adjusted terms) from January 1966 to July 1982: stockmarket deflation prolonged and partially disguised by monetary inflation; I said so here and here, last month. I maintain that the bear market began in 2000 and the symptoms were masked by the terrible extra debts taken on over the last 8 years. Karl Denninger showed us yesterday that these debts account for all the US GDP growth since the New Millennium, plus $9 trillion.

The debate about inflation and deflation continues, though from a British perspective we've seen practically the whole of the rest of the world become one-third more expensive in sterling terms, in only five months. However, Einstein's theory of relativity rejects the notion of any absolute standpoint, and we shall see next year which other currencies mimic sterling's vertiginous fall.

In these shifting times, it becomes very hard to discern real value; but however hard to measure, it exists nevertheless. There is a real bill to pay for our excesses, and I think 2008 will be seen in retrospect as the year that the global balance of power underwent a sudden tectonic shift, from West to East. Yes, the East will suffer for a while, too, but it has long been acquiring the means of production and developing its local markets, and will emerge from the crisis ahead of us.

And there will also - must also - be an intergenerational shift of power, within our Western societies. As globalization continues and real income and real house prices decline, existing debt (set in fixed terms) will become proportionately greater, until the weight is too great to bear; and the worst of it falls on the people who are also struggling to raise families and save something, however inadequate, for their old age. They cannot be crucified in this way. How can savers be taxed at 20% and workers at (effectively, on margin, including National Insurance) 40%? Real wealth must flow from one to the other, just to maintain civilization. I think either savings must be taxed more (perhaps the removal of tax exemption for some savings products will be the start), or inflation must come, though I don't know how long the play will go on before the denouement.

We did have another option, and I was only half-joking: cancel mortgage debts on a massive scale (bankrupting the banks and the bankers, and serve them right). Then, with our productive populace relatively unencumbered, it would be possible to let Western wages and prices fall to much nearer Eastern levels, and we could begin to compete.

I prefer Alexander's handling of the Gordian knot, to Gordon Brown's. For me, debt forgiveness is the way; but that's too radical, it seems. Instead, inflation will have to diminish the real value of debt, but jerkily, as the debt-holders periodically jack up interest rates in a fighting retreat. All to hide from reality. "Oh, what a tangled web we weave..."

Subscribe to:

Posts (Atom)