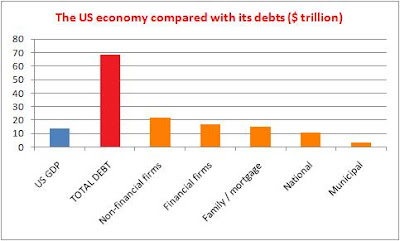

Interesting observation by

Steve Keen: unemployment correlates closely with the amount that debt contributes to demand in the economy.

Let me try to reason out the consequences, however inexpertly.

So, as everyone scrambles to cut spending and get out of debt, unemployment will soar. Since there is a great deal of international trade, the hit will be felt internationally.

Then government finances will come properly unravelled, especially in countries that have generous social welfare provisions. Worldwide, sovereign states will look for anyone who has real money to lend.

This

should result in higher interest rates, but that would make the cost of debt, and its sustainability, extremely difficult, both for states and for corporations (and the burden on the latter will tend to result in even more unemployment and more claimants on the government). A rise in rates would also hit holders of long-term government debt, which may be one of the reasons the Chinese have been swapping that for shorter-dated Treasuries. A collapse in bonds will affect the capital value of pensions and investments, oh dear.

Another way out is default on debt. But who will be hit by that? Not just foreigners, but our pensions and managed investment funds.

A third way, which given that we have history to learn from doesn't seem likely, is the true hyperinflation approach. Germany in 1923, Hungary, Argentina, Zimbabwe... do you really see this happening here?

Then there's the downgrading of debt, with corresponding falls in the traded value of the currency. We've seen some of that - what, 20% off the pound? - so maybe there's more to come from that direction. Except other countries may follow suit. In 1922, if you were a far-sighted German, I suppose you might have sold marks and bought dollars; what currency would you buy now?

Or there's "more of the same" again - talking up the economy and pumping in cash until you spend because you daren't leave it to rot in the savings account.

Which way will it go? Where will it all end?