It's not just the banks that are short of money. Many US States and local authorities are also suffering financial problems, and this is affecting the trade in their bonds, i.e. their borrowings on the money market.

("What are bonds, exactly?" - see here.)

Michael Panzner reports that municipal bonds ("munis") offer a better yield than US Treasury bonds, but the difference is still not enough to pay for the extra risk. Professional investors are short-selling "munis". i.e. betting that they will fall in price. A steep fall may indicate imminent bankruptcy, and some say this is on the way for many authorities, as

Mish reported at the end of December.

So, what will happen when the US Government is seen to be buying everybody's bad debts?

People (even here in the UK, where we tend to wait patiently for our wise rulers to solve all) are beginning to worry about inflation, and are thinking about investing again. An article in

Elliott Wave International warns us not to be panicked into parting with our cash, and reminds us:

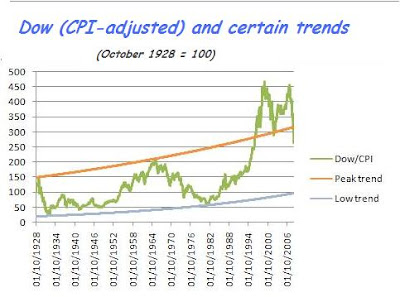

... there are periods when inflation does erode the value of cash. I mean, look at the seven years leading up to the October 2007 peak in U.S. stocks: big gains in the stock indexes, while inflation was eroding cash. No way did cash do as well as stocks during that time. Right? Wrong. Cash outperformed stocks in the seven years leading up to the 2007 stock market high. That outperformance has only increased in the time since.Since this is the view I took and communicated to clients in the 1990s, you will understand that I didn't make much money as a financial adviser. But it was certainly good advice, even if it was based on strongly-felt intuition rather than macroeconomic analysis.

Not that analysis guarantees results, in a world where the money game's rules are changed at will by politicians with a host of agendas that they don't share with us ordinary types. But my current guess is that the stockmarket will halve again in the next few years, when compared with the cost of living.

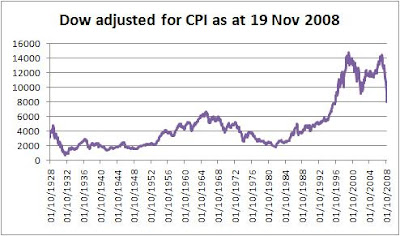

Discussing the Dow, I have previously suggested that instead of looking back to 1929, we might use the period 1966 - 1982 as a comparator. I've adjusted January 1966 and December 1999 to = 100 and oddly enough, the beginning of September 2009 sees the Dow past and present at a fairly similar point.

Discussing the Dow, I have previously suggested that instead of looking back to 1929, we might use the period 1966 - 1982 as a comparator. I've adjusted January 1966 and December 1999 to = 100 and oddly enough, the beginning of September 2009 sees the Dow past and present at a fairly similar point.

What if the banks hadn't gone for broke from 2002/2003 onward?

What if the banks hadn't gone for broke from 2002/2003 onward? iTulip's:

iTulip's:

{kind=link}