Monday, January 21, 2008

Danger of systemic breakdown

Doug Noland looks at the world of financial speculation, which has used loads of borrowed money to boost returns, and worries that as liquidity dries up, the market will become inefficient. This is, I think, one of the things about which Richard Bookstaber has warned. Perhaps the gunslinger day traders should assure themselves of the robustness of their counterparties when playing with futures and options.

We've just had a crash

... and Robert McHugh figures that the US stock market (as measured by the Wilshire 5000 Index) has already lost $2.6 trillion in the last three months.

He's begging for inflation now, rather than a useless stimulant later when the mule has died.

He's begging for inflation now, rather than a useless stimulant later when the mule has died.

The $1 trillion loss figure reappears

Thomas Tan thinks the addition of plausible losses in the credit default swap market to write-offs in other areas of banking, could bring the total hit on the US financial system to the $1 trillion mark.

Sunday, January 20, 2008

Economics in the dark

In 1971, the economist Stafford Beer brought the cybernetic revolution to Chile. His key perception was that economic decisions needed not only accurate, but timely information. So he set up a computer network and data analysis systems to empower the government's ministries without overloading them with irrelevant data.

In advanced economies, it's important for companies, banks and individuals to receive such information, too.

But nearly 40 years later, the USA needs to re-learn the lesson. The Federal Reserve ceased reporting M3 money supply data in 2006; accurate assessment of inflation is complicated by "hedonic adjustment" and periodic (and tendentious?) alteration of the types of item included in price surveys; the Bureau of Labor Statistics seasonally adjusts unemployment figures so that an increase can sometimes appear to be a decrease; nobody (not even the lenders) yet knows the full figures on bad loans and "Tier 3 assets"; it is not even clear how we should assess a nation's wealth (GDP per capita seems a misleading measure).

How can you navigate without up-to-date information? Even in the nineteenth century, Mississippi river pilots had to keep track of the river's changes, or risk getting stranded on new sandbars. And as John Mauldin reports, party political manoeuvering is stymying two appointments to the Federal Reserve's Board, at a time when the Fed most needs to concentrate on resolving the unfolding complex financial crisis.

Even given the right data, decision-making has become tougher. Increasing global interconnection and wealth transfer between nations means that normal cycles may be broken by epochal linear developments, so the past is now a very unsafe guide to the future.

We need clarity, direction and vision.

In advanced economies, it's important for companies, banks and individuals to receive such information, too.

But nearly 40 years later, the USA needs to re-learn the lesson. The Federal Reserve ceased reporting M3 money supply data in 2006; accurate assessment of inflation is complicated by "hedonic adjustment" and periodic (and tendentious?) alteration of the types of item included in price surveys; the Bureau of Labor Statistics seasonally adjusts unemployment figures so that an increase can sometimes appear to be a decrease; nobody (not even the lenders) yet knows the full figures on bad loans and "Tier 3 assets"; it is not even clear how we should assess a nation's wealth (GDP per capita seems a misleading measure).

How can you navigate without up-to-date information? Even in the nineteenth century, Mississippi river pilots had to keep track of the river's changes, or risk getting stranded on new sandbars. And as John Mauldin reports, party political manoeuvering is stymying two appointments to the Federal Reserve's Board, at a time when the Fed most needs to concentrate on resolving the unfolding complex financial crisis.

Even given the right data, decision-making has become tougher. Increasing global interconnection and wealth transfer between nations means that normal cycles may be broken by epochal linear developments, so the past is now a very unsafe guide to the future.

We need clarity, direction and vision.

Panzner votes DE (flation)

Michael Panzner is in the DE camp, because the bubble was caused by credit creation: "The way up is the way down" (a maxim of both Taoism and Heraclitus, apparently; but then the Greeks have always been great travellers and interested in ideas).

In his excellent book (reviewed here last May), he suggests that inflation will come afterwards (actually, not just IN- but HYPER-).

In his excellent book (reviewed here last May), he suggests that inflation will come afterwards (actually, not just IN- but HYPER-).

Saturday, January 19, 2008

A small town in Germany

The TV was on, and I forget what programme we were watching. Sometimes they were Dutch - we were near the border - but more often German. I was eleven, and would watch anything. Even the adverts were fun, linked by shorts featuring little cartoon characters, the Mainzelmännchen. HB cigarettes, Allianz insurance, Bear condensed milk ("Nichts geht über Bärenmarke……Bärenmarke zum Kaffee!")

Then a newsflash cut in: the President of the USA had been shot on a visit to Dallas and had been rushed to hospital. My father went upstairs. The programme resumed.

My father came down. I still remember him buckling his belt over his uniform, as ever uncomfortable and determined to do his best, a stocky man with a straight back, now full of tension. He watched with us as another newsflash came: the President was dead.

I think the camp sent a driver with a Jeep; in any case, Dad was gone. We watched some more TV, interrupted by occasional updates and speculation. Then it was time for bed. Flannel pyjamas, cotton sheets, the heavy blankets that trapped your feet. I went to sleep.

Lights woke me, illuminating the curtains. Heavy engines, headlights passing, heading in the direction of Düsseldorf. One after another after another. Now, I know they were tank transporters, racing to position the heavy armour in readiness for the Red invasion.

And now there are no more Communists, or so it seems. We buy fuel from the Russians, hardware and toys from the Chinese. The people my father, a gentle and sensitive man, was prepared to die fighting, are our friends and trading partners. As reported by The Independent, Chinese interests even supported our Conservative leader and former Prime Minister, Edward Heath (Sir Edward protested the following week, saying the claims were "misleading and inaccurate" - but did not go so far as to say that they were untrue). Surely, we're all friends now. After all, Dad had helped the Germans start to rebuild their country; he'd worked with German civilians, learned to speak the language fluently, married a German refugee. Wars happen, and so does peace. The people of the world are vexed by their leaders, yet love for one another endures and triumphs.

But Communism is not a nation, and does not love people. Everything, even its own most ardent supporters, can be burned on the altar of abstract principle. Informed that a general nuclear war would kill a third of humankind, Mao said good, then there would be no more classes.

As gypsies and beggars used to sing:

So proud and lofty is some sort of sin

Which many take delight and pleasure in

Whose conversation God doth much dislike

And yet He shakes His sword before He strike

(The Watersons performed it on "Frost and Fire", which our English teacher played to us in the late Sixties. I associate it with cold, freshness, the musty fragrance of the Monmouthshire woods, animism, hope.)

By degrees, this brings me to the current state of affairs. Our leaders wish us to believe that the history of our fathers is at an end, and now only efficient administration remains to be achieved. The revels of democracy are ended; they were fun, but their time is past.

No: as Christopher Fry said, "affairs are soul size", still. Although I do believe that sudden and total conversion is possible, as in James Shirley's now implausible-seeming play "Hyde Park" (who would have believed the Earl of Rochester's conversion? - and there are those who still doubt it, not knowing how the sinner hates sin), I doubt that all who worked with the old Soviet and Chinese Communist regimes have abandoned their principles and plans. Like the remark about the significance of the French Revolution (variously attributed to Chou En-Lai and Mao Tse-Tung), it's "too early to say".

Even if our leaders should be gullible or merely suborned, Jeffrey Nyquist reminds us again that there are still people who think differently from us, and we must be prepared. It is not all right to be weak, whether militarily or in our economies. Good fences (and good borders) make good neighbours.

Then a newsflash cut in: the President of the USA had been shot on a visit to Dallas and had been rushed to hospital. My father went upstairs. The programme resumed.

My father came down. I still remember him buckling his belt over his uniform, as ever uncomfortable and determined to do his best, a stocky man with a straight back, now full of tension. He watched with us as another newsflash came: the President was dead.

I think the camp sent a driver with a Jeep; in any case, Dad was gone. We watched some more TV, interrupted by occasional updates and speculation. Then it was time for bed. Flannel pyjamas, cotton sheets, the heavy blankets that trapped your feet. I went to sleep.

Lights woke me, illuminating the curtains. Heavy engines, headlights passing, heading in the direction of Düsseldorf. One after another after another. Now, I know they were tank transporters, racing to position the heavy armour in readiness for the Red invasion.

And now there are no more Communists, or so it seems. We buy fuel from the Russians, hardware and toys from the Chinese. The people my father, a gentle and sensitive man, was prepared to die fighting, are our friends and trading partners. As reported by The Independent, Chinese interests even supported our Conservative leader and former Prime Minister, Edward Heath (Sir Edward protested the following week, saying the claims were "misleading and inaccurate" - but did not go so far as to say that they were untrue). Surely, we're all friends now. After all, Dad had helped the Germans start to rebuild their country; he'd worked with German civilians, learned to speak the language fluently, married a German refugee. Wars happen, and so does peace. The people of the world are vexed by their leaders, yet love for one another endures and triumphs.

But Communism is not a nation, and does not love people. Everything, even its own most ardent supporters, can be burned on the altar of abstract principle. Informed that a general nuclear war would kill a third of humankind, Mao said good, then there would be no more classes.

And dictators, dressed in a little brief authority, ignore warnings. On the eve of World War II, when the conflict could yet be averted, Hitler was with guests in Berchtesgaden when the clouds over the mountains assumed an ominous red and yellow appearance. A woman told him "Das bedeutet blut, und mehr blut" ("This means blood, and more blood"); Hitler trembled, but then said if it must be so, it must be so.

As gypsies and beggars used to sing:

So proud and lofty is some sort of sin

Which many take delight and pleasure in

Whose conversation God doth much dislike

And yet He shakes His sword before He strike

(The Watersons performed it on "Frost and Fire", which our English teacher played to us in the late Sixties. I associate it with cold, freshness, the musty fragrance of the Monmouthshire woods, animism, hope.)

By degrees, this brings me to the current state of affairs. Our leaders wish us to believe that the history of our fathers is at an end, and now only efficient administration remains to be achieved. The revels of democracy are ended; they were fun, but their time is past.

No: as Christopher Fry said, "affairs are soul size", still. Although I do believe that sudden and total conversion is possible, as in James Shirley's now implausible-seeming play "Hyde Park" (who would have believed the Earl of Rochester's conversion? - and there are those who still doubt it, not knowing how the sinner hates sin), I doubt that all who worked with the old Soviet and Chinese Communist regimes have abandoned their principles and plans. Like the remark about the significance of the French Revolution (variously attributed to Chou En-Lai and Mao Tse-Tung), it's "too early to say".

Even if our leaders should be gullible or merely suborned, Jeffrey Nyquist reminds us again that there are still people who think differently from us, and we must be prepared. It is not all right to be weak, whether militarily or in our economies. Good fences (and good borders) make good neighbours.

Punish the perp

Karl Denninger says we should make the people who caused the subprime problems pay for the consequences. Either they should burn up with their own debt (Marc Faber has said some players should be taken out of the game) or pass on the grief to their shareholders, issuing new shares to raise capital and so diluting the existing stockholders' portion.

Unfortunately, we in the UK have chickened out - for party political reasons to do with its power base in the north of England, the Labour government is currently holding the baby in the case of insolvent lender Northern Rock, even though the tax payer is on the hook for nearly $120 billion as a result. (Hey, that's nearly as much as the proposed new tax break to reflate America - and our population is one-fifth the size of yours!)

Hope you have better luck - or better leaders - over there. Buy a Lottery ticket and hope?

Unfortunately, we in the UK have chickened out - for party political reasons to do with its power base in the north of England, the Labour government is currently holding the baby in the case of insolvent lender Northern Rock, even though the tax payer is on the hook for nearly $120 billion as a result. (Hey, that's nearly as much as the proposed new tax break to reflate America - and our population is one-fifth the size of yours!)

Hope you have better luck - or better leaders - over there. Buy a Lottery ticket and hope?

Friday, January 18, 2008

Dow 9,000 update

Dow 12,082.31, gold $880.50/oz, so the Dow is now worth 13.72 ounces of gold as against Robert McHugh's prediction of 13.51.

Nearly there, and the new announcement of a $145 billion reflation may push gold that extra yard.

Nearly there, and the new announcement of a $145 billion reflation may push gold that extra yard.

Stocks may follow bond yields down

Bob Bronson gives us a striking graph of the apparent correlation (since 2000) between the stockmarket and the yield on 10-year Treasury bonds. There is now a very wide gap between the two and seemingly the implication is that stocks are overdue for a large correction.

Wednesday, January 16, 2008

Here we go

Two from Karl Denninger in the last two days:

Monday, he reasserted his belief in DE-flation; but as I've been saying for some time, maybe the real issue is the divide between haves and have-nots, and he deals with that, too. No point being rich if you daren't go out.

Yesterday, he sounded the bells for a possible crash today. Maybe this is when Robert McHugh's prediction is fulfilled.

Monday, he reasserted his belief in DE-flation; but as I've been saying for some time, maybe the real issue is the divide between haves and have-nots, and he deals with that, too. No point being rich if you daren't go out.

Yesterday, he sounded the bells for a possible crash today. Maybe this is when Robert McHugh's prediction is fulfilled.

Tuesday, January 15, 2008

Time to buy into Northern Rock?

Two hedge funds have punted heavily on the British lender that the government has supported with £55 billion.

The share price has slumped from over £12 last February to 69 pence, assisted by the gleefully gloomy 20/20 hindsight of the news media. We had voxpops today from small "windfall share" demutualisation shareholders ruefully reckoning their notional losses and admitting they can't find the (now-near worthless - ha!) certificates.

One of Sir John Templeton's maxims is "The time of maximum pessimism is the best time to buy and the time of maximum optimism is the best time to sell."

Let me offer two of mine: "Never buy what the fund managers try to sell you at financial adviser seminars", and "Remember the journalists who had their pensions in Equitable Life with-profits, because EL didn't (ugh!) pay commissions".

If I had the spare, I might speculate on NR. Hedge funds may be able to afford losing money, but they certainly don't go out of their way to do it. I wonder what will happen?

The share price has slumped from over £12 last February to 69 pence, assisted by the gleefully gloomy 20/20 hindsight of the news media. We had voxpops today from small "windfall share" demutualisation shareholders ruefully reckoning their notional losses and admitting they can't find the (now-near worthless - ha!) certificates.

One of Sir John Templeton's maxims is "The time of maximum pessimism is the best time to buy and the time of maximum optimism is the best time to sell."

Let me offer two of mine: "Never buy what the fund managers try to sell you at financial adviser seminars", and "Remember the journalists who had their pensions in Equitable Life with-profits, because EL didn't (ugh!) pay commissions".

If I had the spare, I might speculate on NR. Hedge funds may be able to afford losing money, but they certainly don't go out of their way to do it. I wonder what will happen?

Monday, January 14, 2008

Oil to crack the dollar?

Nathan Lewis reminds us how, when President Nixon cut the dollar's link to gold in 1971, OPEC protected the real value of its oil with price rises (thus earning a reputation for having caused our inflation).

Now that the gold dinar has been introduced in Malaysia, Lewis wonders whether the dirham should link to gold, too, so oil exporters can avoid being robbed by a falling dollar.

Brownouts and lines at the gas station again, perhaps.

Now that the gold dinar has been introduced in Malaysia, Lewis wonders whether the dirham should link to gold, too, so oil exporters can avoid being robbed by a falling dollar.

Brownouts and lines at the gas station again, perhaps.

USA / UK Sovereign Wealth Funds?

Shares are supposed to be the best long-term investment, better than bonds or cash. The usual concern is the time horizon of the investor. Who lives longer than a state like America or Britain?

Foreign governments with trade surpluses (based on artificially low currency exchange rates and stupid overspending by the West) are building up trillions in reserves and eyeing our companies and real estate. If our own leaders aren't willing to rebalance the world economy, the least they can do is get a piece of the action.

Why not?

Foreign governments with trade surpluses (based on artificially low currency exchange rates and stupid overspending by the West) are building up trillions in reserves and eyeing our companies and real estate. If our own leaders aren't willing to rebalance the world economy, the least they can do is get a piece of the action.

Why not?

Sunday, January 13, 2008

Dow 9,000 update

Last year, Robert McHugh predicted that the Dow would drop to 9,000, if not in nominal terms then in relation to gold. The Dow was then 13,238.73 and gold $666.30/oz, which means that it took 19.87 ounces of gold to buy the Dow. McHugh's prediction implies the Dow dropping to 13.51 gold ounces (a fall of 6.36 ounces).

The Dow is now 12,606.30 and gold $894.90, so the Dow is now worth 14.09 gold ounces. It has fallen by 5.78 ounces out of the predicted 6.36, so the prediction is 90.9% fulfilled so far.

McHugh will be fully correct if, for example, the Dow remains unchanged and gold rises to $933/oz; or if gold stalls, the Dow will need to fall to 12,090.

The Dow is now 12,606.30 and gold $894.90, so the Dow is now worth 14.09 gold ounces. It has fallen by 5.78 ounces out of the predicted 6.36, so the prediction is 90.9% fulfilled so far.

McHugh will be fully correct if, for example, the Dow remains unchanged and gold rises to $933/oz; or if gold stalls, the Dow will need to fall to 12,090.

To Gordon Brown: please remit £4bn ASAP

From Bob Hoye in Safe Haven yesterday:

"U.K. Sold 395 tonnes of gold at an average price of $274.9 per ounce. The first sale at $254 caught (or caused?) the low point in a 20-year slide in the price of gold.

The losers are us, Brown's gold sales raised around $3.49 billion.."

-- Telegraph.co.uk , January 2, 2006

That was written when the price was $627 and at today’s gold price of $895 the position would be worth $11.4 billion. And - remember the reason for selling was to improve central bank returns - what did they buy with the funds?

I make that a loss of $8 billion to date, or £4bn sterling.

We hear a lot about accountability. If only politicians could be made personally financially accountable.

Or if they could be paid to go away. In recent times, it would have saved the country a fortune if each senior politician had been given £10 million to do nothing at all.

"U.K. Sold 395 tonnes of gold at an average price of $274.9 per ounce. The first sale at $254 caught (or caused?) the low point in a 20-year slide in the price of gold.

The losers are us, Brown's gold sales raised around $3.49 billion.."

-- Telegraph.co.uk , January 2, 2006

That was written when the price was $627 and at today’s gold price of $895 the position would be worth $11.4 billion. And - remember the reason for selling was to improve central bank returns - what did they buy with the funds?

I make that a loss of $8 billion to date, or £4bn sterling.

We hear a lot about accountability. If only politicians could be made personally financially accountable.

Or if they could be paid to go away. In recent times, it would have saved the country a fortune if each senior politician had been given £10 million to do nothing at all.

Saturday, January 12, 2008

Debt and slavery

Doug Noland sees the debt crisis spreading to the corporate sector; David Jensen writes a letter to the Governor of the Bank of Canada, including very telling graphs of mounting debt and the bubble in the financial markets; Michael Panzner discusses a piece from the Financial Times on the threat of a downgrade of America's historic AAA credit rating, and refers to the weakening of the USA's military pre-eminence; Sol Palha worries about the acquisition of Western assets by sovereign wealth funds ("Slowly but surely America and Europe are going to be owned by foreigners. The irony is that Congress is trying to keep immigrants out of this country but right in front of their eyes foreigners are slowly gobbling up huge chunks of this country.").

All this leads me to Jeffrey Nyquist's grim, but compelling latest piece. He despairs of the irrelevance of mainstream political discussion, especially as the polling process rattles on, and paints a far greater picture. I think you should read it all, but here are a few extracts:

What is happening in the news today, what is happening in the markets and in the banking system, has profound strategic implications... There are no invulnerable countries... If a government does not see ahead, make defensive preparations, establish a dialogue with citizens, lead the way to awareness and responsibility, then the nation stumbles into the next world war unarmed and psychologically unprepared.

Even worse, today's politics has become a politics of "divide and conquer" in which one constituency is played off against another: poor against rich, non-white against white, the secular against the religious. Before a positive outcome is possible, we must have unity and we must have reality.

It's more comfortable to ignore the crying of Cassandra, but maybe Nyquist is like Churchill in the pre-WWII political wilderness, trying to prepare us for the next conflict. We in Britain only just made it, and how we have paid for that struggle ever since.

But it was a price worth paying. History would have been very different, and very horrible I am sure, if Churchill had listened to some in his Cabinet in 1940 who advised him to make a deal with the Nazis. He said, “If this long island story of ours is to end at last, let it end only when each one of us lies choking in his own blood upon the ground.” It's a line that even now has tears pricking my eyes. The appeasers were silenced by the sound of deeply-moved men banging their fists on the Cabinet table in agreement and applause.

My worry is that I don't see men of that calibre now. As Lord Acton said in a letter to a bishop, "Power corrupts, and absolute power corrupts absolutely". Commenting on the House of Commons after the Great War, Stanley Baldwin remarked on the presence of "A lot of hard-faced men who look as if they had done very well out of the war". Today, the faces are softer, the hair expensively dressed, the manner relaxed and affable, but behind it all one senses cold-hearted, selfish betrayal. To be charitable, it may be that our leaders and ex-leaders don't fully realize the negative consequences of all their deals, compromises and consultancies.

As our reckless debt is progessively converted into ownership, we may find out how much we took our freedom for granted. It's a lot harder to get back.

The Bible has something to say on this, too (and no, I'm not a preacher, this is to show that the issues endure throughout history): Leviticus, Chapter 25 deals with debt, buying and redeeming slaves, and how the chosen people should be treated differently from the heathens - for the latter, enslavement is perpetual.

Friday, January 11, 2008

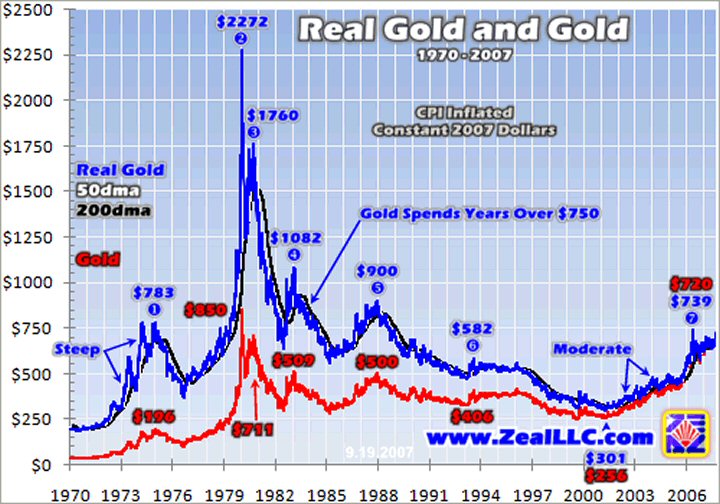

Gold, the dollar and the Dow

Gold supporters seem to be waiting for a reprise of the heady days of 1980. I think this is another case where you need to decide whether you are a speculator or a long-term investor.

Here's a relatively recent graph of the price of gold, adjusted for inflation (admittedly, inflation can be defined in many ways):

Here's a relatively recent graph of the price of gold, adjusted for inflation (admittedly, inflation can be defined in many ways):

On this chart, it looks as though gold's median price would be around $600/oz, so currently it's above trend and presumably the elevated value factors-in some economic concern.

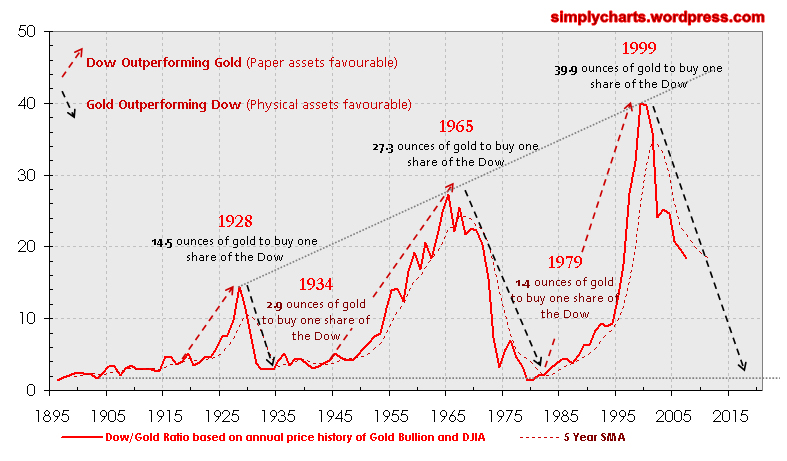

Now, here's a chart correlating the Dow and gold: It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.

It seems harder to spot an average here, since each peak is much higher than the one before. But taking the Dow as it is now (12,606.30) and the current price of gold ($894.90), the present ratio of 14.08 ounces would be in the middle range of the variation since the mid-1920s.

So a purchase of gold now looks like a speculation, rather than a bargain.

Waves and tides

A most apposite article by the Contrarian Investor, in which he considers how all this economic information leaves us confused as to the future direction of the economy. It's like getting millimetre-accurate radar images of all the waves in the harbour, without knowing about the effect of the moon on the tides. Not that the information itself is accurate, anyway.

Thursday, January 10, 2008

Stuffed

Michael Panzner hands on a piece from Naked Capitalism: expert, inside opinion is that the banks are so gorged with bad debt that America will mimic the "melancholy, long withdrawing roar" of Japan's ebb tide.

Wednesday, January 09, 2008

Something's gotta give

Interest on official debt in the USA runs at $430 billion for 2007, and rising steeply, according to the Treasury's own figures (htp Michael Panzner, quoting Mish's Global Economic Trend Analysis); total government debt is now c. $9.2 trillion.

It's more serious than that, of course: James Turk quotes the Comptroller General, David M Walker's estimate that total liabilities, including commitments to future social security benefits, are around $53 trillion. The government's annual revenues are only around 5% of this figure, so the credit card looks like it's pretty much fully-loaded.

However it happens, it seems something must give way under the strain. Frank Barbera reckons the Dow has plenty further to fall (and possible interim correction or not, he thinks gold looks good). Prieur du Plessis concurs, quoting Nouriel Roubini's comment that "... a lousy stock market in 2007 will look good compared to an awful stock market in 2008."

Bob Bronson thinks the downturn will be long as well as hard. He in turn quotes the chairman of the National Bureau of Economic Research: this one “could be deeper and longer than the recessions of the past.”

Boris Sobolev also looks to gold, but prefers the smaller companies because of all the money that's piled into the majors.

In case we in the UK should be tempted by schadenfreude, Ashraf Laidi predicts that sterling will accompany the US dollar's fall against other currencies. From what I read in connection with the USA, a weakening currency may provide a temporary boost to exports, but also inflate the cost of imports; so I don't suppose that our following the dollar will do us much long-term good, either.

Of course, it's possible to dismiss all this as group-think wall-of-worry stuff, but maybe that would be double-bluffing ourselves. Sometimes, things are exactly what they seem. Banks have consistently turned a profit for centuries, on the inexorability of debt.

It's more serious than that, of course: James Turk quotes the Comptroller General, David M Walker's estimate that total liabilities, including commitments to future social security benefits, are around $53 trillion. The government's annual revenues are only around 5% of this figure, so the credit card looks like it's pretty much fully-loaded.

However it happens, it seems something must give way under the strain. Frank Barbera reckons the Dow has plenty further to fall (and possible interim correction or not, he thinks gold looks good). Prieur du Plessis concurs, quoting Nouriel Roubini's comment that "... a lousy stock market in 2007 will look good compared to an awful stock market in 2008."

Bob Bronson thinks the downturn will be long as well as hard. He in turn quotes the chairman of the National Bureau of Economic Research: this one “could be deeper and longer than the recessions of the past.”

Boris Sobolev also looks to gold, but prefers the smaller companies because of all the money that's piled into the majors.

In case we in the UK should be tempted by schadenfreude, Ashraf Laidi predicts that sterling will accompany the US dollar's fall against other currencies. From what I read in connection with the USA, a weakening currency may provide a temporary boost to exports, but also inflate the cost of imports; so I don't suppose that our following the dollar will do us much long-term good, either.

Of course, it's possible to dismiss all this as group-think wall-of-worry stuff, but maybe that would be double-bluffing ourselves. Sometimes, things are exactly what they seem. Banks have consistently turned a profit for centuries, on the inexorability of debt.

Oil splat

"Oil crunch" doesn't sound right, although it might be appropriate to shale oil: Jeffrey Brown outlines what looks like a compelling thesis on growing domestic energy consumption by major oil exporters. He thinks that the top five producers will be using all their own supplies by around 2030, and concludes that the USA must rapidly reshape its transportation system:

In simplest terms, we are concerned that the very lifeblood of the world industrial economy—net oil export capacity—is draining away in front of our very eyes, and we believe that it is imperative that major oil importing countries like the United States launch an emergency Electrification of Transportation program--electric light rail and streetcars--combined with a crash wind power program.

That is just the tip of the iceberg, surely: residential and office heating/lighting, mechanised farming, supermarket shopping, centralised medical facilities - so much will have to be reviewed and planned.

In simplest terms, we are concerned that the very lifeblood of the world industrial economy—net oil export capacity—is draining away in front of our very eyes, and we believe that it is imperative that major oil importing countries like the United States launch an emergency Electrification of Transportation program--electric light rail and streetcars--combined with a crash wind power program.

That is just the tip of the iceberg, surely: residential and office heating/lighting, mechanised farming, supermarket shopping, centralised medical facilities - so much will have to be reviewed and planned.

Tuesday, January 08, 2008

Twang money, encore

The Contrarian Investor is also struck by the elasticity of fiat money, and how this vitiates attempts to make fair comparisons and store wealth. Gold for the long term, he thinks.

In the short term, we have this contest between credit contraction and currency expansion. I'm getting the feeling it'll be the first followed by the second, which is what Michael Panzner predicts in "Financial Armageddon".

In the short term, we have this contest between credit contraction and currency expansion. I'm getting the feeling it'll be the first followed by the second, which is what Michael Panzner predicts in "Financial Armageddon".

Grab your pension now, inflation-proof it?

Tony Allison looks at the threats to your prosperity in retirement. A bird in the hand?

Monday, January 07, 2008

Killer greens

Stuart Staniford takes a point I've read recently in Vernon Coleman's "Oil Apocalypse", about biofuels threatening food supplies for the world's poor, and extrapolates frighteningly:

... both oil and cereals are global commodity markets. If it's profitable to make food into fuel in the US, even without a subsidy, then it's profitable elsewhere also - possibly more so given lower labor costs. So the basic growth dynamics are the same. The infection just hasn't got as strong a grip on the whole globe yet, but it's growing at similar rates.

... I expect oil prices to increase in the medium term, though certainly they could go down in the short-term if the credit crunch affects the global economy enough.

... When we have a bidding war between the gas tanks of the roughly one billion middle class people on the planet, and the dinner tables of the poor, where does that reach equilibrium?

... We noted earlier that according to the UN about 800 million people are unable to meet minimal dietary energy requirements. That is 12% of the world population. [...] we can estimate that a doubling in food prices over 2000 levels might bring 30% or so of the global population below the level of minimal dietary energy requirements, and a quadrupling of food prices over 2000 levels might bring 60% or so of the global population into that situation.

... both oil and cereals are global commodity markets. If it's profitable to make food into fuel in the US, even without a subsidy, then it's profitable elsewhere also - possibly more so given lower labor costs. So the basic growth dynamics are the same. The infection just hasn't got as strong a grip on the whole globe yet, but it's growing at similar rates.

... I expect oil prices to increase in the medium term, though certainly they could go down in the short-term if the credit crunch affects the global economy enough.

... When we have a bidding war between the gas tanks of the roughly one billion middle class people on the planet, and the dinner tables of the poor, where does that reach equilibrium?

... We noted earlier that according to the UN about 800 million people are unable to meet minimal dietary energy requirements. That is 12% of the world population. [...] we can estimate that a doubling in food prices over 2000 levels might bring 30% or so of the global population below the level of minimal dietary energy requirements, and a quadrupling of food prices over 2000 levels might bring 60% or so of the global population into that situation.

Zero sum for the lower echelons

Martin Hutchinson (07 January) makes my case, with particular reference to Tata and Jaguar-cum-Land Rover :

... it seems likely that the most skilled Westerners will continue to give their countries a comparative advantage against emerging markets. However, there is no guarantee that these research-intensive sectors are likely to support the entire Western population, far from it. They are highly cyclical, benefiting hugely from an active stock market and venture capital market. Further there is no evidence that innovation itself, as distinct from the fruits of recent past innovations, is significantly expanding as a percentage of output -- indeed, research expenditure has if anything declined.

... Since the majority of location-dependent jobs in Western countries are low-skill it therefore follows that if governments wish to protect local living standards, they need to discourage low-skill immigration. Except in Japan, they have not been doing so; both in the EU and the United States low-skill immigration, frequently illegal immigration, has got completely out of control and is immiserating the working classes.

... the economic histories of a high proportion of the Western population under 30, except the very highly skilled, will involve repeated bouts of unemployment, with job changes involving not a move to higher living standards but an angry acceptance of lower ones. By 2030, it is possible that the median real income in the United States and Western Europe may be no more than 50-60% of its level today.

This will expose the democratic divide between those who vote and influence the system in their favour, and the rest. The class division could sharpen as "I'm all right Jack" is replaced by "One can't complain, Piers".

Sackerson awards a Prose Prize for Hutchinson's use of the term "immiserating".

P.S.

... and presumably this will have an obvious effect on residential property prices. Who's for selling up and buying a caravan?

... it seems likely that the most skilled Westerners will continue to give their countries a comparative advantage against emerging markets. However, there is no guarantee that these research-intensive sectors are likely to support the entire Western population, far from it. They are highly cyclical, benefiting hugely from an active stock market and venture capital market. Further there is no evidence that innovation itself, as distinct from the fruits of recent past innovations, is significantly expanding as a percentage of output -- indeed, research expenditure has if anything declined.

... Since the majority of location-dependent jobs in Western countries are low-skill it therefore follows that if governments wish to protect local living standards, they need to discourage low-skill immigration. Except in Japan, they have not been doing so; both in the EU and the United States low-skill immigration, frequently illegal immigration, has got completely out of control and is immiserating the working classes.

... the economic histories of a high proportion of the Western population under 30, except the very highly skilled, will involve repeated bouts of unemployment, with job changes involving not a move to higher living standards but an angry acceptance of lower ones. By 2030, it is possible that the median real income in the United States and Western Europe may be no more than 50-60% of its level today.

This will expose the democratic divide between those who vote and influence the system in their favour, and the rest. The class division could sharpen as "I'm all right Jack" is replaced by "One can't complain, Piers".

Sackerson awards a Prose Prize for Hutchinson's use of the term "immiserating".

P.S.

... and presumably this will have an obvious effect on residential property prices. Who's for selling up and buying a caravan?

Gold boom, gold bust

Brady Willett offers his predictions for 2008, including (at some stage) a major correction in the gold price, and Chinese equities.

I've reported expert comment before, about the vulnerability of gold to market manipulation and speculation. I think I'll keep on sitting out this dance.

I've reported expert comment before, about the vulnerability of gold to market manipulation and speculation. I think I'll keep on sitting out this dance.

Inflation or deflation: an expert writes

So it's not just me, even chart analysts like Captain Hook can't decide about IN vs. DE.

Also heartening to see my suggestion re insider jiggery-pokery echoed here:

As an aside, I still don't know what to make of the triangle / diamond in Goldman's chart (see Figure 4) other than they plan to squeeze stocks higher under the cover of low volumes over Christmas holidays in justifying their bonuses.

Also heartening to see my suggestion re insider jiggery-pokery echoed here:

As an aside, I still don't know what to make of the triangle / diamond in Goldman's chart (see Figure 4) other than they plan to squeeze stocks higher under the cover of low volumes over Christmas holidays in justifying their bonuses.

Sunday, January 06, 2008

A winning combination

The Daily Mail alleges a new craze called "celebrity maths", where you combine two famous faces to make a third. Who might be the third here?

The Daily Mail alleges a new craze called "celebrity maths", where you combine two famous faces to make a third. Who might be the third here?And what other political combinations would you like to see?

Gold and liberty

Fear, and the resentment of the oppressed, are more dangerous than bullish aggression.

I watched a programme last night about how we very nearly had the Third World War in 1983. This was a time when Russia was especially paranoid about the West's military intentions - spies were even ordered to report how many lights were on in late evening at the Ministry of Defence in London, apparently not knowing that the offices were lit so the cleaners could do their work.

Then in September, a Soviet spy satellite, fooled by sunlight reflecting off high-level cloud, reported not one, but five missile launches from America. The Russian monitor on duty ignored the klaxon and flashing screen, backed his judgment and told his superiors it was a false alarm, for which he was ultimately discharged from the Army. Wikipedia says his name is Stanislav Petrov. He's certainly worth more than the $1,000 the Association of World Citizens could afford to award him. We may owe him our lives.

Looking for updates on the gold dinar, I came across this blog by a Pakistani, in which he looks to the Islamic dinar as a way of breaking the enslavement of the world by a fiat-currency banking cartel. Irrespective of whether he's justified in his analysis of the situation, or reasonable in his hopes for such a currency, we should note the victim-perception. I seem to recall a maxim (from Sun Tzu?) that you should fear a weak enemy.

Which brings us back to the economic vulnerability of the UK and USA. Weakness can invite aggression, but also makes the weak fear an attack even when it isn't coming. Worryingly for a potential aggressor, weakness may be feigned:

22. If your opponent is of choleric temper, seek to irritate him. Pretend to be weak, that he may grow arrogant. ("Laying Plans")

I don't think you can truly be free until you are strong and independent. We need to get our houses in order, so we can deal with others from a secure base - which is safer for all involved.

I watched a programme last night about how we very nearly had the Third World War in 1983. This was a time when Russia was especially paranoid about the West's military intentions - spies were even ordered to report how many lights were on in late evening at the Ministry of Defence in London, apparently not knowing that the offices were lit so the cleaners could do their work.

Then in September, a Soviet spy satellite, fooled by sunlight reflecting off high-level cloud, reported not one, but five missile launches from America. The Russian monitor on duty ignored the klaxon and flashing screen, backed his judgment and told his superiors it was a false alarm, for which he was ultimately discharged from the Army. Wikipedia says his name is Stanislav Petrov. He's certainly worth more than the $1,000 the Association of World Citizens could afford to award him. We may owe him our lives.

Looking for updates on the gold dinar, I came across this blog by a Pakistani, in which he looks to the Islamic dinar as a way of breaking the enslavement of the world by a fiat-currency banking cartel. Irrespective of whether he's justified in his analysis of the situation, or reasonable in his hopes for such a currency, we should note the victim-perception. I seem to recall a maxim (from Sun Tzu?) that you should fear a weak enemy.

Which brings us back to the economic vulnerability of the UK and USA. Weakness can invite aggression, but also makes the weak fear an attack even when it isn't coming. Worryingly for a potential aggressor, weakness may be feigned:

22. If your opponent is of choleric temper, seek to irritate him. Pretend to be weak, that he may grow arrogant. ("Laying Plans")

I don't think you can truly be free until you are strong and independent. We need to get our houses in order, so we can deal with others from a secure base - which is safer for all involved.

Iraq may have the last laugh

A company called Sebastian River Holdings is substantially increasing its investment in Iraq:

... prior to the war with Iraq the Dinar was $3.00+ per US Dollar.

...Today the country is almost debt free; Iraq is one of the leaders in oil, natural gas and holds a huge amount of gold in its country.

... The Company believes in the near future there will be a revalue of the Iraq Currency, it is the Company's opinion after doing its due diligence and public statements from Iraq's government officials, that the revalue could come in at between .82 and 1.00 per US Dollar.

... prior to the war with Iraq the Dinar was $3.00+ per US Dollar.

...Today the country is almost debt free; Iraq is one of the leaders in oil, natural gas and holds a huge amount of gold in its country.

... The Company believes in the near future there will be a revalue of the Iraq Currency, it is the Company's opinion after doing its due diligence and public statements from Iraq's government officials, that the revalue could come in at between .82 and 1.00 per US Dollar.

Twang

Jim in San Marcos borrows and discusses a chart showing homeowners' equity. As residential property prices drop, more borrowers move into negative equity. He says bank-owned properties (REOs) are already pricing-in a fall of 30%+.

"Examine the disappearing equity. It came from no where and is going back to no where."

That's what happens when credit becomes a form of currency, as the bullion moralists keep reminding us.

Why are banks allowed to create so much "fiduciary money"? Who does own the Fed?

"Examine the disappearing equity. It came from no where and is going back to no where."

That's what happens when credit becomes a form of currency, as the bullion moralists keep reminding us.

Why are banks allowed to create so much "fiduciary money"? Who does own the Fed?

Saturday, January 05, 2008

Bitter medicine

The Levy Economics Institute runs a range of figures through its economic model and decides that it is pessimistic for the short-to-medium term, but guardedly hopeful for the state of the US economy afterwards:

... the present crisis is already more serious than any that has occurred before in modern times.

... Our projections, taken literally, imply three successive quarters of negative real GDP growth in 2008. Spending in excess of income returns to negative territory, reaching -1.6 percent of GDP in the last quarter of 2012—a value that is very close to its “prebubble” historical average.

... while the rate of growth in GDP may recover to something like its long-term average, all our simulations show that the level of GDP in the next two years or more remains well below that of

productive capacity.

... We conclude that at some stage there will have to be a relaxation of fiscal policy large enough to add perhaps 2 percent of GDP to the budget deficit.Moreover, should the slowdown in the economy over the next two to three years come to seem intolerable, we would support a relaxation having the same scale, and perhaps duration, as that which occurred around 2001.

Our projections suggest the exciting, if still rather remote, possibility that, once the forthcoming financial turmoil has been worked through, the United States could be set on a path of balanced growth combined with full employment.

... the present crisis is already more serious than any that has occurred before in modern times.

... Our projections, taken literally, imply three successive quarters of negative real GDP growth in 2008. Spending in excess of income returns to negative territory, reaching -1.6 percent of GDP in the last quarter of 2012—a value that is very close to its “prebubble” historical average.

... while the rate of growth in GDP may recover to something like its long-term average, all our simulations show that the level of GDP in the next two years or more remains well below that of

productive capacity.

... We conclude that at some stage there will have to be a relaxation of fiscal policy large enough to add perhaps 2 percent of GDP to the budget deficit.Moreover, should the slowdown in the economy over the next two to three years come to seem intolerable, we would support a relaxation having the same scale, and perhaps duration, as that which occurred around 2001.

Our projections suggest the exciting, if still rather remote, possibility that, once the forthcoming financial turmoil has been worked through, the United States could be set on a path of balanced growth combined with full employment.

Raving sane?

"Deepcaster" (Financial Sense, January 4) looks again at the mysterious ownership (and creation) of the US dollar by a private bank, the Federal Reserve. The more one reads about it, the weirder it gets - it's like finding out that ET really does exist!

The conspiracy theory here is that the Fed and other central banks are a cartel that not only inflates the money supply, but has created trillions in derivatives, partly to manipulate the investment markets. "Deepcaster" accuses this cartel of engineering drops in the gold price, just when you'd think gold should be emerging as a natural currency.

He brings in the Amero theory, too - ultimate replacement of the destroyed dollar by a new North American currency, presumably so the crooked poker game can continue with fresh cards.

Can anyone please shed light on all this? For example, who EXACTLY are the owners of the Fed?

If nobody knows or is willing to tell, perhaps one of us should claim ownership - "finders, keepers".

The conspiracy theory here is that the Fed and other central banks are a cartel that not only inflates the money supply, but has created trillions in derivatives, partly to manipulate the investment markets. "Deepcaster" accuses this cartel of engineering drops in the gold price, just when you'd think gold should be emerging as a natural currency.

He brings in the Amero theory, too - ultimate replacement of the destroyed dollar by a new North American currency, presumably so the crooked poker game can continue with fresh cards.

Can anyone please shed light on all this? For example, who EXACTLY are the owners of the Fed?

If nobody knows or is willing to tell, perhaps one of us should claim ownership - "finders, keepers".

Unemployment B-L-S---

Market Ticker: The Recession of 2008

Karl Denninger reports that the US unemployment rate has hit 5%. He thinks - and it's certainly plausible - that we're already in a recession. Especially if Rob Kirby is right, and the Bureau of Labor Statistics (BLS) is lying about the scale of job losses in the financial industry.

Karl Denninger reports that the US unemployment rate has hit 5%. He thinks - and it's certainly plausible - that we're already in a recession. Especially if Rob Kirby is right, and the Bureau of Labor Statistics (BLS) is lying about the scale of job losses in the financial industry.

Friday, January 04, 2008

Marquess of Queensberry rules?

One envies the cheerful liberal economists such as those at Cafe Hayek, but will their principles work in a world where other, much darker forces are working? As I suggested in September, there may be those who will use the tools of international trade and investment as part of a vengeful and destructive plan.

Now, Jeffrey Nyquist treats us to another Sino-Soviet frightener, and Nadeem Walayat sees even more potential enemies, who may not refrain from below-the-belt blows. The enemies of the Open Society abide. Are our Western politicians prepared? Will they defend us?

Now, Jeffrey Nyquist treats us to another Sino-Soviet frightener, and Nadeem Walayat sees even more potential enemies, who may not refrain from below-the-belt blows. The enemies of the Open Society abide. Are our Western politicians prepared? Will they defend us?

Gold and the Dow

Prudent Bear's excellent presentation "The case for a secular bear market" includes a graph of the Dow divided by the price of gold, from 1920 to 2005.

Taking the present values - Dow 13,056.72, gold $864.80 - the formula works out at 15.098, which suggests that the Dow is still well above trend.

Some would see this as indicating a coming gold spike; but another way to rebalance is for the Dow to fall. As credit deflation takes hold, I suggest that in 2008, both gold and the Dow will drop below their current levels, but the Dow more than gold.

UPDATE

Gary Dorsch is looking at the same ratio ("By the end of 2008, the DJI to Gold ratio might tumble towards 10 oz’s of gold"), but thinks the rebalance could happen the other way, through destructive inflation.

If so (and he doubts that it's possible), Karl Denninger thinks you'd still be better off betting on the Dow, using call options:

So tell me again - if you believe in "hyperinflation" - why do you want to buy the clear LOSER of an asset that metals represent, when you can buy index CALLs and, if your thesis is correct, you will make an absolute stinking FORTUNE!

(Of course if you're wrong and the DOW is under 16,000 by the end of the year, that $20,000 is totally flushed. That's the price of poker - but again - just how sure are you that "The Fed" is going to "hyperinflate"? And by the way, no, I don't think they are - in fact, I don't think they CAN.)

SECOND UPDATE

Gary Tanashian sets a target of $920 for gold, but anticipates a drop-back anytime; but longer term, Julian Phillips can't imagine governments NOT hyperinflating, to avoid the horrors of deflation.

The astrologers continue to mutter and gesture over their charts.

Taking the present values - Dow 13,056.72, gold $864.80 - the formula works out at 15.098, which suggests that the Dow is still well above trend.

Some would see this as indicating a coming gold spike; but another way to rebalance is for the Dow to fall. As credit deflation takes hold, I suggest that in 2008, both gold and the Dow will drop below their current levels, but the Dow more than gold.

UPDATE

Gary Dorsch is looking at the same ratio ("By the end of 2008, the DJI to Gold ratio might tumble towards 10 oz’s of gold"), but thinks the rebalance could happen the other way, through destructive inflation.

If so (and he doubts that it's possible), Karl Denninger thinks you'd still be better off betting on the Dow, using call options:

So tell me again - if you believe in "hyperinflation" - why do you want to buy the clear LOSER of an asset that metals represent, when you can buy index CALLs and, if your thesis is correct, you will make an absolute stinking FORTUNE!

(Of course if you're wrong and the DOW is under 16,000 by the end of the year, that $20,000 is totally flushed. That's the price of poker - but again - just how sure are you that "The Fed" is going to "hyperinflate"? And by the way, no, I don't think they are - in fact, I don't think they CAN.)

SECOND UPDATE

Gary Tanashian sets a target of $920 for gold, but anticipates a drop-back anytime; but longer term, Julian Phillips can't imagine governments NOT hyperinflating, to avoid the horrors of deflation.

The astrologers continue to mutter and gesture over their charts.

Dead Cat Splat

Some expect the market to drop, but bounce quickly as in 2000. Vince Foster says not, since this boomlet has been credit-fuelled.

His view: housing is woeful, emerging markets look as though they may be topping-out, the Ted Spread is signalling insolvency fears, the 10-year bond rate augurs slowing growth; so cash is king.

His view: housing is woeful, emerging markets look as though they may be topping-out, the Ted Spread is signalling insolvency fears, the 10-year bond rate augurs slowing growth; so cash is king.

Little boxes, revisited

I've previously suggested that you don't need to be too technical, as long as you focus on the reward systems (the cui bono?). Here, Michael Panzner quotes and discusses an article by Nat Worden on the failure of ratings agencies in the subprime debacle.

I think it's in "Jane Eyre": a teacher who wishes to instil piety into a little boy, asks him whether he'd rather have a biscuit or a blessing. When he answers, a blessing, he gets two biscuits.

When recession empties the the biscuit barrel, maybe we'll get authentic leadership.

UPDATE

My beloved recalled it better, and so I've found the quote on the Net:

...I have a little boy, younger than you, who knows six Psalms by heart; and when you ask him which he would rather have, a ginger-bread nut to eat, or a verse of a Psalm to learn, he says: "Oh, the verse of a Psalm! Angels sing Psalms," says he. "I wish to be an angel here below." He then gets two nuts in recompense for his infant piety.’

I think it's in "Jane Eyre": a teacher who wishes to instil piety into a little boy, asks him whether he'd rather have a biscuit or a blessing. When he answers, a blessing, he gets two biscuits.

When recession empties the the biscuit barrel, maybe we'll get authentic leadership.

UPDATE

My beloved recalled it better, and so I've found the quote on the Net:

...I have a little boy, younger than you, who knows six Psalms by heart; and when you ask him which he would rather have, a ginger-bread nut to eat, or a verse of a Psalm to learn, he says: "Oh, the verse of a Psalm! Angels sing Psalms," says he. "I wish to be an angel here below." He then gets two nuts in recompense for his infant piety.’

We need recession, to avert total disaster

In a sock-to-the-jaw article that I think everyone should read, Nadeem Walayat shows the political-economic forces tides beating against our cliffs and undermining our liberty and prosperity. Like me, he sees sovereign wealth funds as part of this process.

It seems that we must wish our own countries a spell of hard times, in order to stimulate the changes that will defend us from permanent ruin.

It seems that we must wish our own countries a spell of hard times, in order to stimulate the changes that will defend us from permanent ruin.

Thursday, January 03, 2008

Ta-ta industrial wages, hello Mcjobs

India's leading car-maker Tata seems likeliest to take over Jaguar and Land Rover. The fiddle plays, Rome burns.

Mirror, mirror

A few days ago, I said, "This is where I thought we were in 1999. Thanks to criminally reckless credit expansion in the interim, we're still there, only the results may be worse than I feared then." Now, Tom Madell draws comparisons between 2000 and 2007.

Few are brave enough to come out and declare the start of a bear market; but the watchword is "proceed with caution".

Few are brave enough to come out and declare the start of a bear market; but the watchword is "proceed with caution".

Wednesday, January 02, 2008

Consequences

Michael Panzner turns his attention to the human implications of recession, as I have been doing for some time, most recently here, here and here. At least America is a democracy and so politicians must have some incentive to clean the Augean stables; I don't know about the UK.

Bad news: we depend on the banks

The long-experienced team at Contrary Investor thinks the credit market needs watching, not the equity market. Outlook: oh, dear.

When things turn vengeful, let's take a careful look at the banks, and those who give them their orders. Not for the first time, they've lifted us up, and are making ready to drop us from a great height.

As the song from Mary Poppins has it:

If you invest your tuppence

Wisely in the bank

Safe and sound

Soon that tuppence,

Safely invested in the bank,

Will compound

And you'll achieve that sense of conquest

As your affluence expands

In the hands of the directors

Who invest as propriety demands

[...]

You can purchase first and second trust deeds

Think of the foreclosures!Bonds! Chattels! Dividends! Shares!

Bankruptcies! Debtor sales!

... for the whole lyric see here.

The scene ends, happily enough, with a run on the bank as young Michael loudly demands the return of his twopence.

When things turn vengeful, let's take a careful look at the banks, and those who give them their orders. Not for the first time, they've lifted us up, and are making ready to drop us from a great height.

As the song from Mary Poppins has it:

If you invest your tuppence

Wisely in the bank

Safe and sound

Soon that tuppence,

Safely invested in the bank,

Will compound

And you'll achieve that sense of conquest

As your affluence expands

In the hands of the directors

Who invest as propriety demands

[...]

You can purchase first and second trust deeds

Think of the foreclosures!Bonds! Chattels! Dividends! Shares!

Bankruptcies! Debtor sales!

... for the whole lyric see here.

The scene ends, happily enough, with a run on the bank as young Michael loudly demands the return of his twopence.

Monday, December 31, 2007

Small is beautiful

J R Nyquist argues that internationalism is used as a cover for expansion by aggressive states, and the nation-state is our stoutest defence.

I think this links in with our domestic EU in-or-out debate, on which the allegedly Conservative British MP David Cameron has recently been making flirty noises. I say "flirty" because although the headline talks boldly of tearing up the un-referendum-ed Constitution, the leader of the Opposition says "We think the treaty is wrong because it passes too much power from Westminster to Brussels." How much is enough?

Perhaps some will say mine is a typical reaction from a little Englander, but originally that term meant an opponent of imperialism. Well, I'm used to ignorant brickbats. It was Philip Toynbee who - his son told me - called me a Colonel Blimp while I was still at school, I think because I had dared to ask him about the significance of colour in Lorca's poetry. What I gathered from this experience was: never ask a posh leftie for an explanation, he'll only look down his egalitarian nose at you. (I haven't met his daughter Polly, though.) Intriguingly, though the term "little Englander" is said to date from the 1899-1901 Second Boer War, there is an 1833 German dictionary-cum-phrasebook (published in Grunsberg) called "Der kleine Englander ober Sammlung". I do hope the title wasn't intended to have a pejorative tinge, but you can never be sure with the Germans - they do have a wry sense of humour.

The relevance of all this, aside from the asides? I think the themes of diversity, dispersion and disconnection will grow in importance over the coming years, in politics and economics. As with some mutually dependent Amazonian flowers and insects, efficiency and specialisation will have to be balanced against flexibility and long-term survival.

I think this links in with our domestic EU in-or-out debate, on which the allegedly Conservative British MP David Cameron has recently been making flirty noises. I say "flirty" because although the headline talks boldly of tearing up the un-referendum-ed Constitution, the leader of the Opposition says "We think the treaty is wrong because it passes too much power from Westminster to Brussels." How much is enough?

Perhaps some will say mine is a typical reaction from a little Englander, but originally that term meant an opponent of imperialism. Well, I'm used to ignorant brickbats. It was Philip Toynbee who - his son told me - called me a Colonel Blimp while I was still at school, I think because I had dared to ask him about the significance of colour in Lorca's poetry. What I gathered from this experience was: never ask a posh leftie for an explanation, he'll only look down his egalitarian nose at you. (I haven't met his daughter Polly, though.) Intriguingly, though the term "little Englander" is said to date from the 1899-1901 Second Boer War, there is an 1833 German dictionary-cum-phrasebook (published in Grunsberg) called "Der kleine Englander ober Sammlung". I do hope the title wasn't intended to have a pejorative tinge, but you can never be sure with the Germans - they do have a wry sense of humour.

The relevance of all this, aside from the asides? I think the themes of diversity, dispersion and disconnection will grow in importance over the coming years, in politics and economics. As with some mutually dependent Amazonian flowers and insects, efficiency and specialisation will have to be balanced against flexibility and long-term survival.

Sunday, December 30, 2007

Recession QED

In an educational (and mercifully profanity-free) essay, Karl Denninger builds up his case from first principles, explaining the processes of creating and destroying money. He expects house prices to fall back by 30 - 50% and notes that in a recession, equities typically lose 30%.

He says the media is not reporting the truth. I tend to agree: I now throw away the Sunday football and financial supplements at the same time. If you want to know what's really happening, he says, watch what is going on at the banks, the Federal Reserve and Goldman Sachs, all of whom are battening the hatches, while CNBS (also castigated by Jim Willie) plays a cheerful tune to the proles.

I've written before how in 1999, as a financial adviser, I sat through a presentation from a leading UK investment house about tech stocks, which were supposedly about to start a second and bigger boom. I suspected then, and even more so now, that they were looking for the fabled "bigger fool" to offload their more favoured clients' holdings. Denninger intimates the same:

Are these shows, newspapers, and others reporters on the financial markets, entertainers, or worse, puppets of those who know and who need someone – anyone – to unload their shares to before the markets take a huge plunge, lest they get stuck with them?

Then he gives his predictions - which are grim, but not apocalyptic. It's the fools who will get roasted, not everybody. (By the way, Denninger is another Kondratieff cycle follower.)

What to hold, in his opinion? Cash, definitely; anything else, check the soundness of the deposit-taker. If you want to gamble on hyperinflation, he thinks call options on the stockmarket index are likely to yield more than gains on gold, even if the gold bugs are right.

This is where I thought we were in 1999. Thanks to criminally reckless credit expansion in the interim, we're still there, only the results may be worse than I feared then.

Oh, and he thinks the dollar will recover to some extent, because the rest of the world is going to get it just as bad, and probably worse. (Interesting that the pound is now back under $2.)

He says the media is not reporting the truth. I tend to agree: I now throw away the Sunday football and financial supplements at the same time. If you want to know what's really happening, he says, watch what is going on at the banks, the Federal Reserve and Goldman Sachs, all of whom are battening the hatches, while CNBS (also castigated by Jim Willie) plays a cheerful tune to the proles.

I've written before how in 1999, as a financial adviser, I sat through a presentation from a leading UK investment house about tech stocks, which were supposedly about to start a second and bigger boom. I suspected then, and even more so now, that they were looking for the fabled "bigger fool" to offload their more favoured clients' holdings. Denninger intimates the same:

Are these shows, newspapers, and others reporters on the financial markets, entertainers, or worse, puppets of those who know and who need someone – anyone – to unload their shares to before the markets take a huge plunge, lest they get stuck with them?

Then he gives his predictions - which are grim, but not apocalyptic. It's the fools who will get roasted, not everybody. (By the way, Denninger is another Kondratieff cycle follower.)

What to hold, in his opinion? Cash, definitely; anything else, check the soundness of the deposit-taker. If you want to gamble on hyperinflation, he thinks call options on the stockmarket index are likely to yield more than gains on gold, even if the gold bugs are right.

This is where I thought we were in 1999. Thanks to criminally reckless credit expansion in the interim, we're still there, only the results may be worse than I feared then.

Oh, and he thinks the dollar will recover to some extent, because the rest of the world is going to get it just as bad, and probably worse. (Interesting that the pound is now back under $2.)

Saturday, December 29, 2007

The answer to Olduvai?

I am most grateful for a comment by "APL" on the heroic "Burning Our Money" blog, which directs us to an article on the potential of radiation-free fusion energy.

There is an international project (ITER) in the south of France to develop this, and if it works...

UPDATE

Thanks to GMG for a link to this discussion of fusion power, which tends to the conclusion that a successful and economically viable fusion system is a very long way off, if feasible at all, and we'd do better to concentrate on fission, i.e. the present type of nuclear power station.

There is an international project (ITER) in the south of France to develop this, and if it works...

UPDATE

Thanks to GMG for a link to this discussion of fusion power, which tends to the conclusion that a successful and economically viable fusion system is a very long way off, if feasible at all, and we'd do better to concentrate on fission, i.e. the present type of nuclear power station.

Spot the trends

The CIA World Factbook gives global GDP per capita as $10,200 (in purchasing power parity terms). This puts the average standard of living somewhere between Kazakhstan and Mexico. On the same basis, per capita income is $43,800 in the USA and $31,800 in the UK .

Generally, the poorer the country, the higher the income inequality as measured by the Gini Index (except for Azerbaijan, according to this from the ESRC).

The Factbook estimates 30% combined unemployment and underemployment in many non-industrialized countries; developed countries typically 4%-12% unemployment.

There are enormous fortunes to be made (by some) arbitraging the economic differences between countries.

In the USA and the UK, we are relentlessly spending more than we are earning.

What are our governments' plans for us to remain rich? And given the correlation between income and equality, do our business, media and political elites have much incentive to make and seek support for such plans?

Generally, the poorer the country, the higher the income inequality as measured by the Gini Index (except for Azerbaijan, according to this from the ESRC).

The Factbook estimates 30% combined unemployment and underemployment in many non-industrialized countries; developed countries typically 4%-12% unemployment.

There are enormous fortunes to be made (by some) arbitraging the economic differences between countries.

In the USA and the UK, we are relentlessly spending more than we are earning.

What are our governments' plans for us to remain rich? And given the correlation between income and equality, do our business, media and political elites have much incentive to make and seek support for such plans?

Contradicting the contrarians

Cash is king for now, but later next year it'll be equities up, dollar up, bonds down, according to the round table on Safe Haven.

UPDATE

But Tim Wood expects the market to hit a low - "The straw that finally breaks the camel’s back may be closer than you think."

UPDATE

But Tim Wood expects the market to hit a low - "The straw that finally breaks the camel’s back may be closer than you think."

Friday, December 28, 2007

Desperate hope

"Desperate hope" is an oxymoron, which sounds like a dumb bull: mine is that we will have a tough landing rather than a complete crash. Goading the dumb bulls is The Mogambo Guru (Richard Daughty), who delivers another comical end-of-the-world sermon on inflation. He thinks dropping interest rates will encourage borrowers to take on still more debt.

However, many have already pointed out that (a) lending criteria are tightening and (b) not all of the interest rate cut is being passed on to the borrower. So lenders are trying to reduce their exposure and are also being paid more for the risk they have already assumed. And we see from this Christmas shopping season that (c) the consumer is becoming more reluctant to spend.

That's not to say that we won't get inflation (in some sectors, not housing), since falling interest rates tend to depreciate the currencies of debtor countries relative to their cash-rich trading partners. On the other hand, the latter will continue trying to hold down their currencies, in an attempt to keep the show on the road - the show being the osmosis of wealth from the lazy, spendthrift West to the hard-working, hard-saving developing world.

We're going to be buying less, but I don't know how fast the Eastern co-prosperity sphere will take up the slack. In his book "The Dollar Crisis", Richard Duncan argues for a worldwide minimum wage to stimulate demand; but maybe events have overtaken him. Certainly, China aims to expand its middle class, rapidly.

But there's another way for China to stave off depression while waiting for the sun to rise in the East. According to James Kynge, manufacturing and transportation costs account for only about 15% of the end-price of Chinese exports to the US. Some of the expanding Chinese middle class will surely go into advertising, marketing, sales, distribution and finance. As China develops its own version of Wal-Mart, Omnicom and banking, credit card and financing operations, it'll own more of the total profit in the supply chain - some of which it can sacrifice to retain market share. And they're motivated to do so by the fact that domestic consumption yields very little profit for their companies: the money's in exports. The longer this game goes on, the more the decline of capital and skilled labour at our end.

So let's worry about the effects at home first. Yes, for investors inflation may be a worry, but perhaps they should extend their concern to include the stability of the society in which they live, as unemployment and insolvency stalk through the West. The issues are no longer financial, but political and social.

And we'd better hope that we don't go for the wrong solutions. Daughty quotes Ambrose Evans-Pritchard's 12 December article in The Daily Telegraph, which concludes (amazingly), "... it may now take a strong draught of socialism to save the Western democracies." I do not think Mr Evans-Pritchard is very old. Or maybe he's just saying that to bug the squares, an expression I'll wager he's too young to remember.

However, many have already pointed out that (a) lending criteria are tightening and (b) not all of the interest rate cut is being passed on to the borrower. So lenders are trying to reduce their exposure and are also being paid more for the risk they have already assumed. And we see from this Christmas shopping season that (c) the consumer is becoming more reluctant to spend.

That's not to say that we won't get inflation (in some sectors, not housing), since falling interest rates tend to depreciate the currencies of debtor countries relative to their cash-rich trading partners. On the other hand, the latter will continue trying to hold down their currencies, in an attempt to keep the show on the road - the show being the osmosis of wealth from the lazy, spendthrift West to the hard-working, hard-saving developing world.

We're going to be buying less, but I don't know how fast the Eastern co-prosperity sphere will take up the slack. In his book "The Dollar Crisis", Richard Duncan argues for a worldwide minimum wage to stimulate demand; but maybe events have overtaken him. Certainly, China aims to expand its middle class, rapidly.